EUR / USD

Source: Massive (polygon.io)

EUR/USD is under significant pressure, driven by hotter-than-expected US CPI data—with headline inflation at 3.8% and core at 2.8%—which has reinforced expectations that the Federal Reserve will maintain its restrictive stance, effectively widening the policy divergence with the ECB. Geopolitical risks from the US-Iran conflict have pushed crude oil back above $100 per barrel, disproportionately impacting the energy-import-dependent eurozone and creating stagflationary pressures that constrain the ECB's ability to match the Fed's hawkish posture.

On the European side, the fundamental picture offers limited support, as German ZEW current conditions deteriorated to a five-month low while ECB officials acknowledge that sluggish growth limits their policy options despite persistent inflation. The resulting safe-haven dollar demand has driven the pair down approximately 0.34% over the past 24 hours, with the price sliding to a low near 1.1723 before recovering modestly to 1.1739.

Technically, the pair is now trading in a notable compression zone where the 200-day, 50-day, and 20-day SMAs all converge around 1.17, with the daily RSI at a neutral 52.6 reflecting diminished momentum. A decisive break below this dense support cluster would likely accelerate selling toward structural support at 1.1631, while the fundamental backdrop of Fed-ECB policy divergence and ongoing energy shocks favours continued downside pressure.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair remains fundamentally underpinned by the wide interest rate differential between the United States and Japan, with hotter-than-expected U.S. CPI data at 3.8% year-over-year effectively eliminating prospects for Federal Reserve rate cuts and pushing Treasury yields higher across the curve. The resulting carry trade dynamics continue to pressure the yen, compounded by surging energy costs stemming from the Strait of Hormuz disruption, creating a particularly damaging feedback loop for Japan as a net energy importer and further eroding its terms of trade.

From a technical perspective, the pair settled near 157.61 after trading in a 156.80–157.76 range, sitting below key resistance at 158 and the 50-day SMA at 159, while breaking above the structural 100-day SMA level at 157.39. The neutral RSI reading around 47 suggests the pair is at an inflection point, with a sustained break above 158 needed to open a path toward 159.

The primary risk to the current bullish bias comes from the Bank of Japan, where growing hawkish sentiment has raised the possibility of a rate hike as early as June, which would structurally undermine the carry trade sustaining yen weakness. Until such a policy shift materialises, Japanese intervention—recently estimated at $64 billion—serves only to moderate the pace of depreciation rather than reverse the broader trend, leaving the pair biased higher within its current technical range.

GBP / USD

Source: Massive (polygon.io)

The GBP/USD pair is under significant downward pressure from both sides of the equation, with hotter-than-expected US CPI data at 3.8% year-over-year effectively closing the door on Federal Reserve rate cuts, while an escalating political crisis surrounding Prime Minister Starmer uniquely punishes sterling assets. The monetary policy divergence has shifted meaningfully against the pound, as Fed futures now price a 60% probability of a rate hike by early 2027, while the UK political turmoil threatens to undermine the Bank of England's tightening stance and remove the carry advantage that had previously supported sterling among G10 currencies.

From a technical perspective, the pair has already declined sharply from 1.3615 to test support near 1.3500—the 20-day SMA—with the daily RSI dropping to 51 from a recent baseline of 57, signalling fading bullish momentum. The 50-day and 200-day SMAs clustered near 1.3400 represent the next critical support zone should 1.3500 fail decisively.

The combination of surging UK gilt yields drawing uncomfortable parallels to the 2022 Liz Truss episode, persistent energy-driven inflation from the US-Iran conflict, and prediction markets assigning an 80% probability of Starmer's departure creates a uniquely challenging macro backdrop for the pound. Until the political uncertainty in Westminster resolves and the fiscal risk premium dissipates, the path of least resistance for GBP/USD appears skewed to the downside, with a break below 1.3500 likely targeting the 1.3400–1.3410 support region.

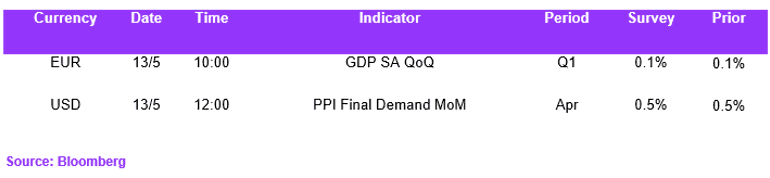

Economic Calendar