EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair faced downward pressure as a divergence between US and Eurozone macroeconomic fundamentals favours the dollar. Stronger-than-expected US inflation data — with April CPI hitting its highest annual pace in nearly three years and PPI surging 1.4% month-over-month versus a 0.5% forecast — has eliminated expectations for Fed rate cuts and widened the transatlantic yield differential. Meanwhile, the Eurozone's confirmed Q1 GDP growth of just 0.1%, contracting industrial production, and weak German ZEW sentiment data paint a picture of fading momentum that limits the ECB's ability to adopt a hawkish stance.

From a technical perspective, EUR/USD has declined to a critical confluence zone near 1.1700–1.1710, where the 200-day and 100-day converge, with the daily RSI at approximately 49 reflecting neutral-to-weak momentum and institutional volume confirming the sell-off. Geopolitical risks compound the bearish outlook, as the Strait of Hormuz disruption driving Brent crude toward $105–$110 disproportionately damages oil-importing European economies while bolstering safe-haven dollar demand.

A decisive break below the 1.1700 support cluster would open the path toward 1.1632, and absent a meaningful de-escalation in geopolitical tensions or a stabilization in European economic data, the structural macro environment continues to favour further dollar appreciation against the euro.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair remains elevated near 157.80, driven primarily by the persistent monetary policy divergence between a hawkish Federal Reserve and a gradually normalizing Bank of Japan. Stronger-than-expected US inflation data has repriced Fed expectations sharply higher, pushing the 10-year Treasury yield to 4.46% and maintaining a roughly 190 basis point spread over JGB yields that continues to incentivize carry trade flows against the yen.

From a technical perspective, the pair is consolidating below key resistance levels, with the 20-day SMA at 158.27 and 158.50 capping upside, while the 155 level provides substantial support below. The daily RSI near 48 confirms the neutral posture, suggesting the market is awaiting a catalyst to break out of its current range.

Japanese intervention efforts — estimated at nearly 10 trillion yen since late April — and implicit US diplomatic support represent the primary constraint on further yen weakness, with the 160 level appearing actively defended. However, the geopolitical backdrop of elevated crude oil prices near $107 Brent continues to deteriorate Japan's terms of trade as a major energy importer, simultaneously feeding US inflation prints that reinforce the hawkish Fed pricing underpinning dollar strength.

GBP / USD

Source: Massive (polygon.io)

GBP/USD weakened, with the pair slipping from 1.3543 to 1.3522 and touching a session low near 1.3486 before recovering. The immediate catalyst is a dramatic upside surprise in US inflation data — April headline CPI at 3.8% and PPI at 6.0% year-over-year — which has prompted markets to reprice Federal Reserve policy expectations, with the probability of an additional rate hike climbing to around 35%.

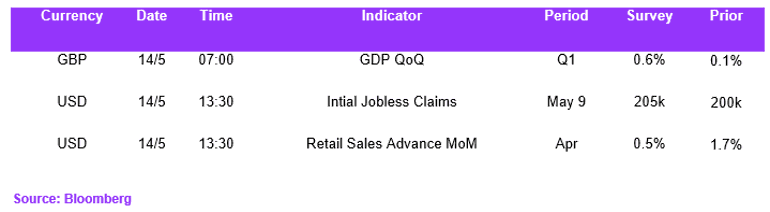

On the sterling side, political turmoil within the Labour Party poses a growing risk, as over 100 MPs have called for Prime Minister Starmer's resignation, with a potential leadership challenge raising fears of more expansionary fiscal policy that could reignite the fiscal-monetary conflict behind sterling's 2022 collapse. The Bank of England remains trapped in a stagflationary bind, with inflation re-accelerating to 3.3% and services inflation at 4.5%, while growth stagnates at just 0.1%, leaving policymakers with no clear path forward.

Technically, the daily RSI has cooled to nearly 50, signalling a shift to neutral momentum as the pair converges on its 20-day SMA at 1.3540, with the 1.3483 level now acting as critical near-term support. A decisive break below this zone would likely accelerate selling toward moving averages clustered around 1.3400, particularly given the bearish fundamental backdrop of surging energy costs, UK political uncertainty, and the upcoming Q1 GDP release on Thursday.

Economic Calendar