EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair strengthened on Monday amid a powerful shift in geopolitical sentiment, as growing optimism surrounding US-Iran peace negotiations and plunging oil prices drive a broad retreat from safe-haven dollar positions. This erosion of the inflation premium that had been supporting the dollar is compounded by narrowing policy divergence expectations, with the ECB signalling potential rate hikes while Fed tightening odds diminish alongside falling energy costs.

From a technical perspective, the pair recovered approximately 0.33% from its late-week low near 1.1598 to reach 1.1643 but faces a significant overhead resistance zone where the 100-day moving averages is at around 1.1699. The daily RSI remains subdued near 46, reflecting the broader one-month downtrend from April highs near 1.1835, suggesting that while momentum is building, buyers have not yet decisively seized control.

Key catalysts this week include FOMC Member Logan's speech on Wednesday and Thursday's PCE inflation data, which will be critical for determining whether the Iran-deal-driven dollar weakness is sustained or reversed. Holiday-thinned liquidity on Monday has amplified geopolitical moves, leaving Tuesday's full-liquidity session as the true test of whether buyers can defend 1.1600 support and mount a convincing push through the 1.17 moving average cluster.

USD / JPY

Source: Massive (polygon.io)

USD/JPY is consolidating near the psychologically critical 160 level, currently trading around 159.00 in a tight congestion zone between the 50-day SMA at 158.77 and established resistance near 159.80. The pair remains fundamentally supported by exceptionally high correlations (near 0.90) between USD/JPY and US-Japan yield spreads, which have been reinforced by the market's hawkish repricing of the Fed's rate path following Governor Waller's dismissal of near-term rate cuts.

On the Japanese side, the Bank of Japan remains structurally constrained despite markets pricing roughly an 80% probability of a June rate hike, with Japan's core inflation slowing to a four-year low reducing immediate pressure to tighten. The proximity to the 160 intervention threshold—combined with thin liquidity from the US Memorial Day holiday—elevates the risk of a BoJ intervention episode, though analysts broadly view such events as providing better entry points for dollar longs rather than altering the pair's fundamental trajectory.

The technical picture suggests a bullish bias remains intact as long as the 50-day SMA and near 158.50–158.80 holds, with upside targets at 159.80 resistance and potentially the late-April highs near 160.70. The near-term trajectory will be shaped by whether additional Fed officials echo Waller's hawkish tone, BoJ Governor Ueda's upcoming communications, and the evolving Middle East diplomatic situation—where lower oil prices from US-Iran negotiation progress have offered temporary yen support but remain fragile given Japan's structural energy-import vulnerability.

GBP / USD

Source: Massive (polygon.io)

GBP/USD has rallied approximately 0.5% from 1.3428 to 1.3508, driven primarily by a sharp decline in oil prices following reports of a US-Iran agreement in principle to reopen the Strait of Hormuz, which has significantly eroded the safe-haven premium supporting the US dollar. The pair now trades above both the 50-day and 200-day SMAs at 1.34, with the daily RSI at a neutral 53, suggesting further upside room exists should momentum persist toward the key resistance level at 1.3649.

Monetary policy divergence continues to favour sterling, as the Bank of England's hawkish pause at 3.75%—driven by UK CPI running at 3.3% with expectations of further acceleration—contrasts with a Federal Reserve holding at 3.50-3.75% amid softer US growth of just 2.0% annualized in Q1. Thursday's Core PCE inflation release represents the pivotal event risk, where a reading above 2.7% could reignite Fed hawkishness and reverse dollar weakness, while a sub-2.5% print would further undermine the greenback.

Several risks could disrupt the current bullish trajectory for cable. UK political uncertainty surrounding Prime Minister Starmer's leadership, the inherent fragility of US-Iran negotiations that could rapidly restore safe-haven dollar demand, and thin liquidity conditions due to Monday's dual bank holiday closures all warrant caution, though the underlying macro backdrop—including the UK's relative insulation from tariff disruption and early US trade agreement—supports continued pound resilience near term.

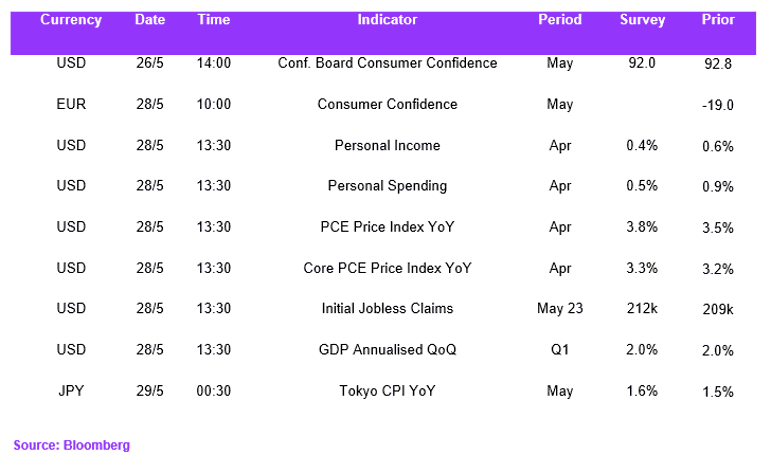

Economic Calendar