EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair is currently navigating a muted environment, with the pair constrained between the 1.1600 level and a cluster of moving averages at 1.1660-1.1690, which are capping significant moves beyond this range.

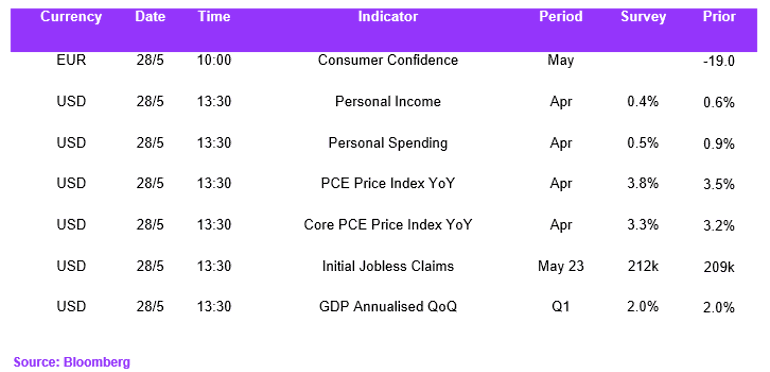

The fundamental backdrop supports the euro's current positioning. ECB Governing Council member Yannis Stournaras explicitly stated that a rate hike in June is the likeliest outcome, and swap markets are pricing in a 92–95% probability of a 25-basis-point increase at the June 11 meeting. This creates a fundamental floor for the euro through widening policy divergence with the Federal Reserve. The Fed, under Chairman Kevin Warsh, faces a different calculus as sticky US inflation—with headline PCE expected at 3.8% and core at 3.3% for April—keeps the central bank in a higher-for-longer posture, with about 50% odds of a rate hike by year-end. This hawkish recalibration across both central banks creates a tug-of-war dynamic; however, the Fed's hawkish pivot is proving the more powerful cross-current, suggesting the euro may struggle to sustain gains.

The divergence between oil markets—still pricing in a deal—and FX markets—beginning to hedge deal risk—creates a fragile equilibrium, where any definitive geopolitical development could trigger a sharp directional move in the pair.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair continued to edge higher on the back of dollar strength and sustained carry trade flows, pushing the pair to 159.50. The Bank of Japan's policy trajectory remains a central driver of the pair's movement ahead of the June 15–16 meeting, where markets are pricing about a 70% probability of a quarter-point rate hike. Governor Ueda struck a hawkish tone on Wednesday, warning that the war-driven oil shock could become persistent amid high inflation expectations and rising wages, while Deputy Governor Himino reaffirmed the BOJ's commitment to further rate increases. Chicago Fed President Goolsbee added external pressure by stating the BOJ risks falling behind the curve if it delays tightening, given that Japan's core inflation continues to exceed the 2% target.

The interest rate differential between the U.S. and Japan—while compressing—remains wide enough to sustain carry trade flows that have structurally supported the pair since 2021. Until that gap narrows substantially, fundamental upward pressure is likely to persist.

Markets remain mindful of an intervention threshold at 160, which is likely to keep the pair’s ascent gradual. However, until the rate differential narrows, fundamental upward pressure on the pair should persist.

GBP / USD

Source: Massive (polygon.io)

The GBP/USD pair weakened, with downside capped by the 200-day moving average at 1.3423. Conflicting headlines about a potential framework deal to reopen the Strait of Hormuz have injected significant uncertainty; this back-and-forth has left currency traders in a cautious, directionless stance. The near-zero UK–US 10-year yield spread means the pair lacks any meaningful interest rate differential driver and is instead being pushed primarily by macro narrative and risk sentiment.

Fundamentally, sterling faces domestic headwinds, including slower-than-expected GDP growth, composite PMI readings below 50 indicating contraction, and a 13% rise in the energy price cap from July, driven by elevated oil costs from the Middle East conflict. While UK inflation has moderated, rising energy prices pose a renewed threat that complicates the Bank of England's policy calculus and limits its ability to signal further tightening relative to hawkish peers.

The broader global monetary tightening cycle is creating headwinds for the pound as a semi-risk-sensitive currency, making the Bank of England's relatively cautious stance a comparative weakness for sterling.

Economic Calendar