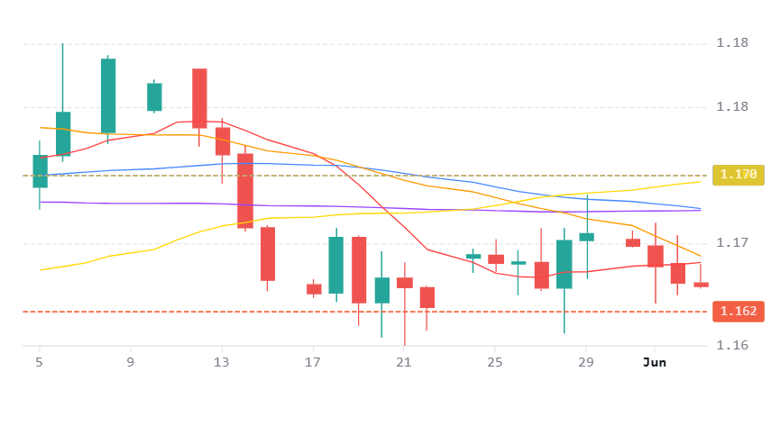

EUR / USD

Source: Massive (polygon.io)

EUR/USD continues to drift lower, trading near 1.1619 and remaining below its key moving averages, with the 200 day SMA, 50 day SMA and 20 day SMA all clustered around the 1.1700 area. The daily RSI at 43.5 suggests momentum remains weak without yet reaching oversold territory, while support at 1.1559 remains the key level to watch should selling pressure intensify. A break below this area could expose a move towards the March low near 1.1415.

The fundamental backdrop continues to favour the dollar. Recent US data has reinforced the view that the economy remains resilient, with April JOLTS job openings rising to a 23 month high and Federal Reserve officials maintaining a broadly hawkish tone. Markets continue to price the possibility of rates remaining higher for longer, while some investors have begun considering the risk of additional tightening should inflation remain elevated.

In contrast, the ECB faces a more difficult policy environment. While eurozone inflation has accelerated to 3.2% year on year and a June rate increase appears highly likely, growth conditions remain weak, particularly in Germany. Elevated energy prices linked to tensions in the Persian Gulf continue to weigh disproportionately on the eurozone as a major energy importer, adding to stagflation concerns.

Looking ahead, Friday's US nonfarm payrolls report is likely to be the key catalyst. A strong labour market reading would reinforce the dollar's yield advantage and could place renewed pressure on the 1.1559 support area. Conversely, softer data may allow EUR/USD to recover towards the 1.1700 resistance cluster, although we expect gains to remain limited while the broader macro backdrop continues to favour the dollar.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains firmly supported near the psychologically important 160 level, trading around 159.91 after steadily retracing nearly all of the decline triggered by Japan's intervention campaign earlier in the year. The pair continues to hold above all major moving averages, with the 20 day SMA and 50 day SMA near 159 and the 30 day VWAP around 158 reinforcing the broader uptrend. Daily RSI at 62 points to firm momentum, although conditions are becoming increasingly stretched.

The fundamental picture remains supportive for further upside. The wide interest rate differential between the United States and Japan continues to encourage carry trade demand, while stronger US labour market data reinforces expectations that Federal Reserve policy will remain restrictive. At the same time, higher oil prices continue to weigh heavily on Japan's trade balance and support further yen weakness.

Attention is increasingly turning towards the Bank of Japan meeting on 16 June and the Federal Reserve decision the following day. Markets are assigning a meaningful probability to further Bank of Japan tightening, but investors remain sceptical that policy adjustments alone will be sufficient to offset the powerful yield advantage offered by US assets.

A sustained move above 160.30 could open the way towards the April high near 160.65 and potentially higher levels beyond that. However, intervention risk remains elevated and Japanese officials continue to signal their readiness to act should volatility become excessive. We expect the area around 160 to remain a key battleground over the coming weeks.

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains range bound near 1.3450, trading below the 50 day SMA and 30 day VWAP around 1.3500 while continuing to find support near the 200 day SMA at 1.3400. Daily RSI remains subdued and reflects the lack of strong directional conviction that has characterised recent trading.

The fundamental backdrop remains mixed. On one hand, the Bank of England's hawkish hold at 3.75% continues to provide support for sterling, particularly as inflation remains well above target and markets continue to price the possibility of further tightening. On the other hand, stronger US economic data and expectations for higher US rates continue to support the dollar and limit sterling's upside potential.

Geopolitical developments remain an important consideration. Higher energy prices linked to the US Iran conflict create a greater challenge for the UK economy than for the United States, given the UK's exposure to imported energy costs. At the same time, domestic political uncertainty and fiscal concerns continue to weigh on investor sentiment towards sterling.

Looking ahead, the Federal Reserve meeting on 17 June and the Bank of England decision on 18 June are likely to determine the next major move. A break below 1.3420 would expose the 1.3270 support area, while a sustained move above the 1.3500 resistance zone could open the way towards 1.3550 and beyond. For now, we expect GBP/USD to remain trapped within its recent range as markets await greater clarity from both central banks.