EUR / USD

Source: Massive (polygon.io)

EUR/USD is trading near 1.1610 after a 0.2% advance over the past 24 hours, with momentum transitioning from bearish to neutral as the daily RSI climbs to 51 from sub-45 readings last month. The pair faces a pivotal catalyst in Wednesday's FOMC decision, where Chair Warsh is expected to hold rates at 3.50%–3.75% but where the tone of forward guidance and the updated dot plot will determine near-term direction. U.S. inflation at 4.2% year-over-year eliminates any near-term rate cut case, yet the U.S.-Iran peace deal driving Brent below $80 provides the Fed breathing room that could soften its hawkish messaging.

On the euro side, the ECB's June 11 hike to 2.25% and Chief Economist Lane's signal of continued proactive tightening provide a fundamental floor, as the rate differential trajectory may narrow if further ECB hikes materialize while the Fed remains on hold. German ZEW sentiment returning to positive territory and eurozone economic resilience through construction recovery and growing real earnings reinforce the structural case for euro support.

Technically, the pair has reclaimed the 20-day SMA around 1.1600 as support, with key resistance clustered at the 50-day and 200-day moving averages near 1.1700. A sustained break above 1.1690 could target 1.1810, while failure at 1.1620 and a breakdown below 1.1570 would expose the monthly low at 1.1508, making Wednesday's Fed communication the decisive catalyst for resolving this consolidation.

USD / JPY

Source: Massive (polygon.io)

The Bank of Japan's widely anticipated 25 basis point rate hike to 1.0%—its highest since 1995—failed to provide meaningful yen support, as cautious forward guidance from Deputy Governor Uchida and the absence of a specific timeline for further tightening left the fundamental bearish case for the yen intact. The persistent interest rate differential between U.S. Treasuries at approximately 4.2% and Japanese government bond yields near 0.9% remains the dominant driver of USD/JPY strength, with markets now pushing its expectation for the first Fed rate cut to March 2027, reinforcing the "higher for longer" narrative that underpins the pair's elevated trading range.

Technically, USD/JPY continues to trade with a constructive bias, holding above all key moving averages—including the 20-day SMA at 159.80, the 50-day at 159, and the 200-day at 155.97—while the daily RSI at 62 reflects sustained but not overextended bullish momentum just below the three-month high of 160.65. A decisive break above 160.65 would open the path toward the all-time high near 162 established in mid-2024, while downside risk is contained unless price retreats below the 20-day SMA.

The near-term catalysts remain asymmetrically skewed toward further yen weakness, with the Fed meeting under Chairman Warsh on Wednesday posing risk of hawkish messaging that would widen differentials further, even as Japanese authorities—having already deployed approximately $73.5 billion in intervention during May—face diminishing returns near the psychologically critical 160 level. The structural unwinding of yen carry trades as Japanese rates rise introduces a latent source of volatility, but absent a material shift in U.S. rate expectations or explicit BOJ hawkishness, the path of least resistance for USD/JPY remains to the upside.

GBP / USD

Source: Massive (polygon.io)

GBP/USD is consolidating near 1.3429, trading just below the 50-day SMA at 1.3475 and hovering around the 20-day SMA at 1.3421, with the daily RSI crossing above the neutral 51 level after spending the prior month predominantly below it. The pair remains range-bound as markets await two critical catalysts: the Federal Reserve's FOMC decision on Wednesday and UK inflation data the following day, with the Fed universally expected to hold rates at 3.50%-3.75% and UK CPI forecast at 3.3%.

The macro backdrop is defined by elevated US inflation, a resilient labour market adding 172,000 jobs in May, and the disinflationary tailwind from the US-Iran peace agreement driving oil prices lower. The narrow monetary policy divergence between the Fed and BoE—both holding rates amid persistent inflation—explains the pair's compressed trading range and lack of directional conviction.

From a technical perspective, a sustained break above the 1.34–1.35 moving average cluster could open a path toward 1.3522, while rejection at these levels and a slide below the 200-day SMA near 1.3417 would expose support at 1.3308. The key directional catalyst will be Chair Warsh's inaugural press conference tone: a hawkish emphasis on services inflation persistence would pressure sterling lower, whereas acknowledgment of falling energy costs and the Iran deal's disinflationary impact could provide the pound a tailwind to clear overhead resistance.

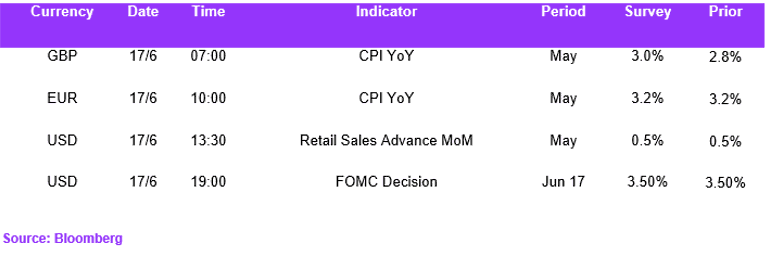

Economic Calendar