EUR / USD

Source: Massive (polygon.io)

EUR/USD remains under significant bearish pressure following the Federal Reserve’s decisively hawkish pivot under new Chair Kevin Warsh, which has widened the US-Eurozone monetary policy divergence. The Fed’s upward revision to its 2026 rate forecast at 3.8%, with nine policymakers now backing at least one hike this year, has strengthened the dollar’s appeal. That divergence was reflected clearly in price action on June 17th, when EUR/USD fell roughly 1.2% from 1.1615 to 1.1478 on heavy volume, leaving the pair near 1.1521 and well below its 200-day, 50-day, and 20-day simple moving averages clustered around 1.16–1.17.

The technical picture reinforces that bearish view, with daily RSI near 39 signalling sustained downside momentum within a broader three-month decline of more than 3%. Underlying US inflation dynamics also continue to support the dollar, with core PCE running at 3.4% and producer prices rising 6.5% year-over-year in May, pointing to persistent pipeline cost pressures that validate the Fed’s hawkish stance. While the US-Iran interim peace agreement and lower oil prices near $78 per barrel may eventually ease some inflation concerns, Fed officials have stressed that price pressures predate the geopolitical conflict and remain evident across services, goods, and housing, limiting hopes for a near-term dovish turn.

Looking ahead, the key technical level to watch is the 1.1478 session low. A failure to hold above 1.1500 would expose the March low near 1.1415, while any rebound is likely to meet strong resistance at the overhead moving average cluster around 1.16. For now, widening rate differentials continue to favour further dollar strength against the euro.

USD / JPY

Source: Massive (polygon.io)

USD/JPY surged during the North American session, rising from around 160.20 to a high near 160.78—its strongest level in more than a year—as the dollar drew renewed support from the Federal Reserve’s hawkish pivot under Chair Kevin Warsh. The pair has since consolidated between 160.50 and 160.70, while holding comfortably above the 20-day moving average at 160.05 and the 50-day moving average at 159.09, reinforcing a firmly bullish medium-term trend structure.

The fundamental backdrop continues to favour dollar strength against the yen, with the Fed signalling a higher-for-longer policy path while the Bank of Japan remains limited to a much slower tightening cycle. That keeps the US-Japan rate differential firmly in place, with US 10-year yields near 4.48% versus roughly 0.9% in Japan, preserving the carry appeal of borrowing cheap yen to fund dollar exposure. Although softer oil prices following the Iran–US peace agreement may ease some inflation concerns, Fed officials have made clear that underlying price pressures remain broad enough to justify a restrictive stance.

From a technical perspective, the key near-term level is the 160.72–160.78 resistance zone. A decisive break higher would pave the way for a retest of the all-time high near 162.00, while repeated rejection there could trigger some profit-taking and pull the pair back toward initial support around the 20-day moving average near 160.00. For now, the broader bias remains tilted to the upside as long as USD/JPY holds above its major moving averages and rate differentials remain heavily dollar-supportive.

GBP / USD

Source: Massive (polygon.io)

GBP/USD suffered a sharp 1.21% intraday selloff on June 17th, falling from 1.3420 to a low near 1.3263 before stabilising at 1.3319, as the pair broke through the 200-day and 20-day SMAs at 1.3400 on heavy volume. The move was driven by the Fed’s hawkish pivot at its June meeting, where nearly half of policymakers now project at least one rate hike later this year—a marked shift from the March median expectation of a cut—thereby strengthening the dollar side of the equation by keeping US borrowing costs elevated.

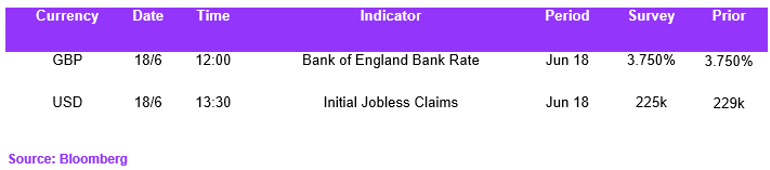

The fundamental backdrop increasingly favours dollar strength, with US inflation running at 4.2% versus the UK’s relatively softer 2.8%, while US producer prices rose 6.5% year-over-year, pointing to pipeline pressures that may delay any Fed easing well into the future. This inflation gap limits the Bank of England’s room to match US tightening, particularly with expectations that the BoE will hold rates at 3.75% on Thursday while the Fed has stepped away from signalling near-term cuts.

From a technical perspective, the pair now trades well below the 50-day SMA near 1.3500, with daily RSI slipping to around 40—its weakest reading in recent weeks. A failure to sustain the early Wednesday bounce would risk a break below 1.3260, opening the door toward the 1.3175–1.3150 area and extending the broader three-month downtrend.

Economic Calendar