EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair is under sustained pressure from a widening monetary policy divergence between the ECB and the Federal Reserve, with Eurozone inflation dropping sharply to 2.8% in June versus expectations while US Treasury yields push toward 4.47% on hawkish Fed pricing. This fundamental backdrop has manifested clearly in price action, as the pair declined approximately 0.4% over the latest session, sliding from 1.1421 to close near 1.1377 amid steady selling that only briefly paused on a high-volume bounce from the 1.1362 session low.

Technically, EUR/USD is deeply oversold with a daily RSI near 33, trading well below all key moving averages including the 200-day SMA at 1.17 and the 20-day SMA at 1.15, confirming an entrenched downtrend that has accelerated since the late January high near 1.2042. The critical near-term level is last week's low around 1.1329, which if broken decisively would open a path toward the 1.1250–1.1280 support zone.

The immediate catalyst for directional resolution is Thursday's June nonfarm payrolls report, where the consensus expectation of approximately 110,000 jobs added sits against a softer ADP print of 98,000 and a modest ISM manufacturing miss at 53.3. A stronger-than-expected employment reading would reinforce hawkish Fed expectations and likely drive EUR/USD through its 1.1329 support, while a significant miss could trigger an oversold mean-reversion rally back toward 1.15. The structural balance remains tilted against the euro as long as the ECB appears poised to pause while the Fed maintains its tightening bias.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair has climbed to approximately 162.70-162.84, marking the dollar's strongest position against the yen in four decades, driven primarily by the wide interest rate differential between the United States and Japan. With the Federal Reserve maintaining rates in the 3.50-3.75% range and traders now pricing in a 67% probability of a rate hike by September—up from just 20.5% one month ago—the policy contrast against the Bank of Japan's benchmark of 1% continues to fuel dollar demand and sustain the carry trade, where net speculative short positions against the yen have climbed to $11.3 billion near two-year highs.

Technically, the pair remains firmly in overbought territory with the daily RSI at approximately 80, trading well above all key moving averages, though the intraday rejection from the all-time high and subsequent drop to 162.30 on elevated volume suggest profit-taking is emerging at these extended levels. Intervention expectations are mounting, with Japanese Finance Minister Katayama reiterating readiness to take "bold action" and the upcoming U.S. Independence Day holiday viewed as a potential intervention window, as thinner liquidity would amplify the impact of any official yen purchases.

However, multiple analysts caution that intervention alone cannot reverse a fundamentally driven trend without a meaningful narrowing of the U.S.-Japan rate differential. The Thursday nonfarm payrolls report represents the next critical catalyst, with a strong reading potentially pushing the pair toward 163-165 while a downside surprise could trigger a corrective move toward the 160.79 level. The broader macro environment—characterized by resilient U.S. economic data, AI-driven capital inflows, and Japan's structural vulnerability as an energy importer—continues to favour dollar strength against the yen in the near to medium term.

GBP / USD

Source: Massive (polygon.io)

The GBP/USD pair is caught between divergent central bank trajectories, with the Federal Reserve maintaining a hawkish posture anchored by Chair Warsh's commitment to the 2% inflation target, while the Bank of England remains constrained by weakening UK domestic momentum following a decline in household disposable income despite headline GDP growth. Mixed US data — softer consumer confidence offset by surging JOLTS job openings and continued ISM Manufacturing expansion — has kept the dollar broadly supported without triggering a decisive breakout.

Technically, the pair settled near 1.3277 after staging a sharp intraday reversal from the 1.3220 low, but remains structurally bearish below the key confluence of the 200-day SMA, 50-day SMA at 1.34, and the 20-day SMA at 1.3296. The daily RSI's recovery toward a neutral 47 reading suggests selling pressure has eased temporarily, though overhead resistance remains formidable.

Looking ahead, Thursday's US Non-Farm Payrolls report will be the primary catalyst for near-term direction, with a strong print likely reinforcing dollar strength and driving a retest of last week's low near 1.3147. The fundamental asymmetry — a Fed poised to maintain or tighten policy versus a Bank of England with limited room to act — continues to favour the bearish case for GBP/USD unless sterling can decisively reclaim the 1.33–1.34 moving average cluster.

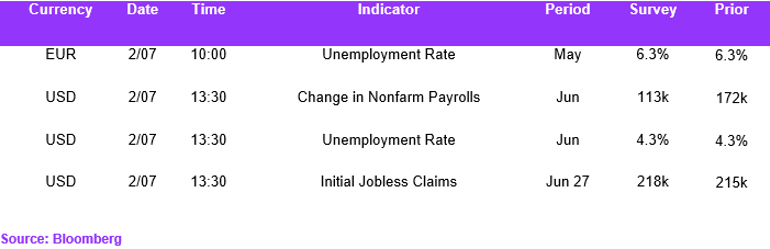

Economic Calendar