Summary

Metals prices trended higher in Q2 as sequential economic data improved, and investors looked through lockdown data and concentrated on the staggered re-opening of the global economy. Expansive Monetary and Fiscal policy has aided liquidity and optimism to the benefit of speculators. However, the PBOC has paused liquidity measures and as data improvements become less pronounced we expect weak demand conditions to play a more prominent role in the market, especially as mine supply starts to come back online albeit at a reduced capacity. Unemployment policies have been successful, but they can’t go on forever and high levels on redundancies seem inevitable which may prompt stagflation. We expect stimulus and liquidity to remain extremely accommodative but gains and volumes to be less pronounced in Q3, with downside risks evident.

Aluminium

The carry trade prompted strong demand for aluminium in Q2, but underlying demand remains weak. While there are signs of recovery in the global auto market, which is positive for sheet consumption, Chinese semi exports have been lower as the export market is weak. We expect supply to remain strong as prices have recovered back above $1,650/t. Speculator sentiment is improving, which may aid the upside as liquidity measures remain expansive, but the fundamentals remain weak. We expect speculator moves to the upside to be exaggerated, but the threat of a second wave is pronounced and this should cap gains and presents a downside risk. Economic data-led speculators could push to $1,775/t, but we expect the majority of trading to take place between $1,610/t – and $1,810/t.

Copper

Tightness in the concentrate market due to mine suspensions and the global lockdown has caused TCs to fall, and we expect these to remain weak in the immediate term but as mine supply comes back online we should see availability increase with TCs. Operation rates and smelter production has been strong and the lack of scrap availability has supported cathode demand. Infrastructure investment and 5G will support consumption, but as the PBOC pause liquidity and special bond issuances reach their year maximum we could see positive speculator sentiment falter. The recovery of economic data should be less pronounced and as mine supply improves, this could prompt correction to the downside. In our opinion, the market is overextended on the upside but we anticipate trading between $6,000/t - $6,800/t, with prices well bid towards $5,800/t.

Lead

China’s auto market has recovered well compared to other majors, but some demand is from dealers looking to restock. In Europe, the order book is weaker with the IFO German automobile order assessment index at -49.8 for June, just off the low. Battery demand is expected to recover but operating rates in China at producers are still recovering, which in conjunction with the low collection rate of older batteries could create some tightness in the market. As mine supply comes back online, the availability of the raw material should improve. We expect the majority of trading between $1,730/t and $1,960/t.

Nickel

Nickel Ore inventories declined significantly in the last 4 months, following frontloading before the Indonesia export ban and reduced availability due to COVID. Maintenance in the immediate term may prompt some softness to stainless production but we could see low-cost producers continue to keep production high. Chinese NPI may increase as operation rates improve but Indonesia demand is expected to rise sharply in the next year as new RKEF lines are produced. EV sales in China are recovering well and Tesla emerged as a front runner in the market. Range: $12,109/t - $14,745/t.

Tin

The solder and semiconductor markets are expected to remain strong in Q3, we could see the smartphone market recover in H2 2020 as well. Mine supply has struggled but Chinese imports of refined tin were up 1,762% y/y in May with the majority of imports coming from Indonesia. Ore and concentrate imports into China were stronger in May, up 24% y/y; this affirms the trend that China is a net importer. The PHLX Semiconductor Index has benefitted from the equity rally, although Samsung did beat analyst earnings expectations for Q2. We expect tin to remain on-trend, trading a range of $15,650/t - $19,000/t.

Zinc

Galvaniser operating rates in China have remained strong but diecasting operating rates is lacklustre. Output of zinc in China has fallen from the recent high but production remains in growth on y/y basis. The reduction in mine supply prompted a decline in zinc concentrate imports into China but TCs have stabilised in recent weeks. We expect Chinese zinc concentrate output to increase. Demand remains weak and stainless steel consumption in the aerospace industry will be hit significantly due to COVID. Reduced demand and constant supply may present headwinds to zinc prices on a fundamental basis; however optimistic speculators aid a rally. Weak demand and supply resumption favours the downside but speculator demand has been strong. Range: $2,093/t - $2,460/t

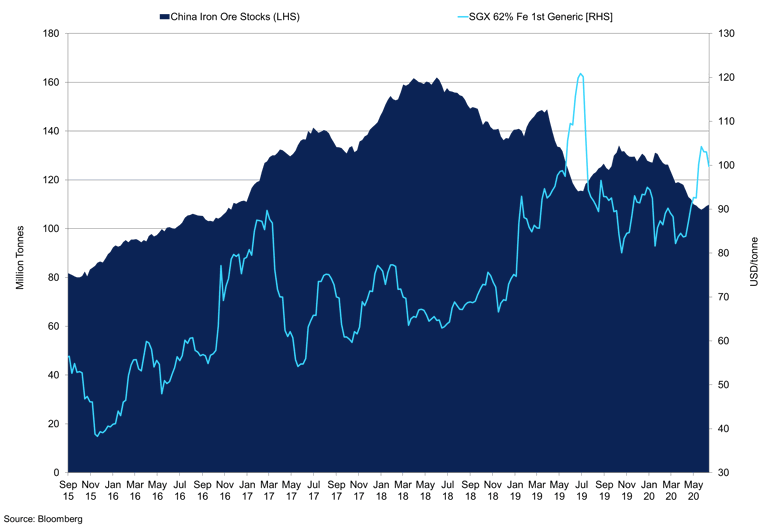

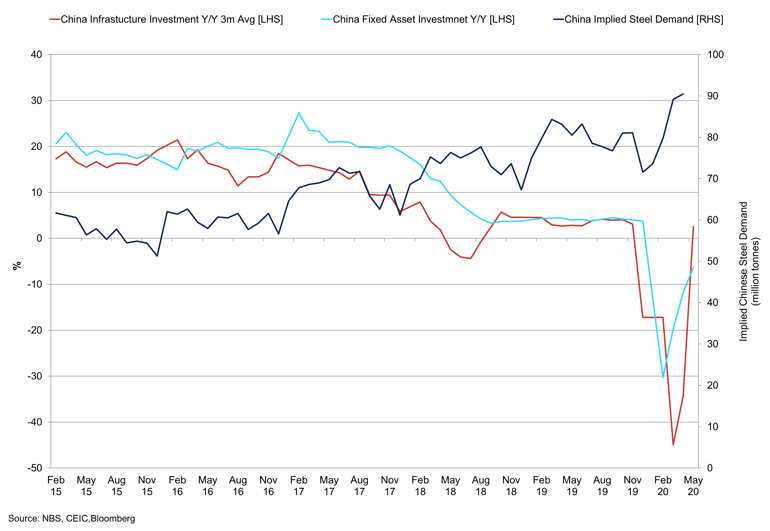

Iron Ore & Steel

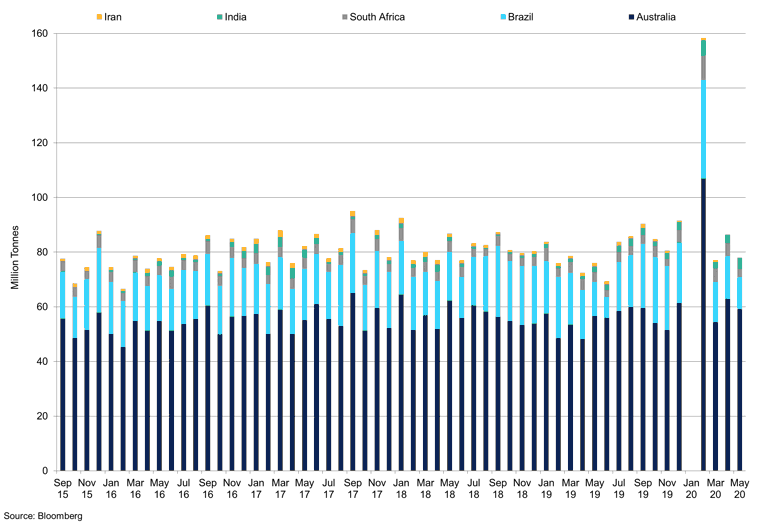

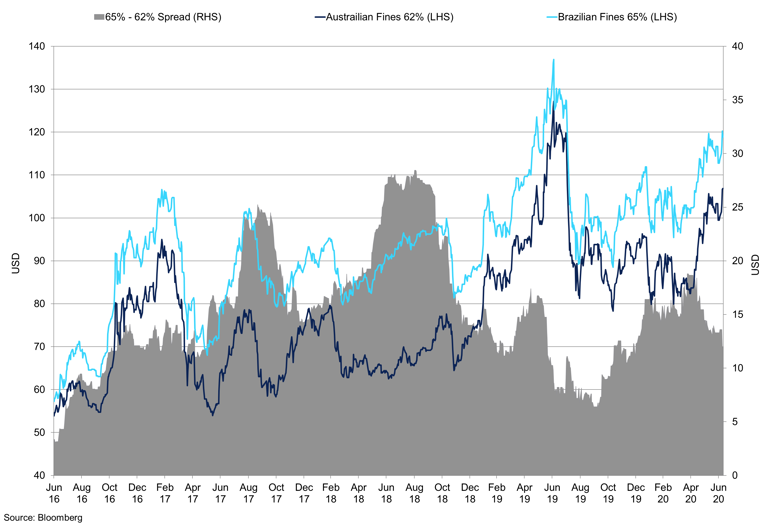

Iron ore prices firmed in recent months as stimulus measures, in China specifically favoured infrastructure and steel demand. Imports into China managed to maintain their strength but the higher quality fines from Brazil may have been in shorter supply as Vale had to halt production. The cases in Latin America remain high, specifically Brazil and this is a threat to exports. Port stocks have fallen and the spread between low and high-quality fines have softened slightly but remain elevated. Strong steel demand will keep prices elevated but the PBOC has paused liquidity. Special bond issuances will remain expansive in the near term despite using over half the year’s allocation. We expect relative tightness to remain in Q3 with a range of $90/t - $120/t.

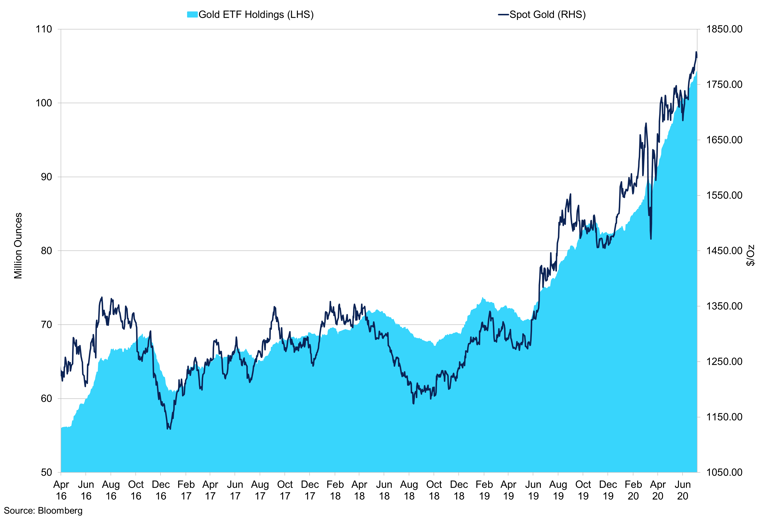

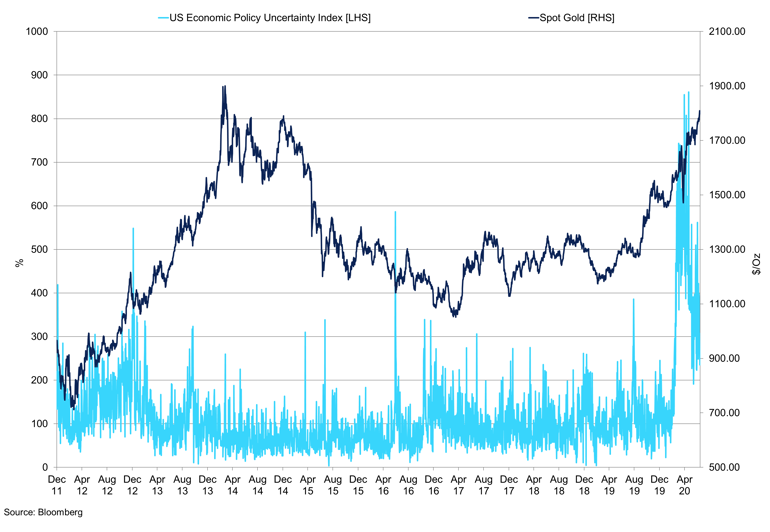

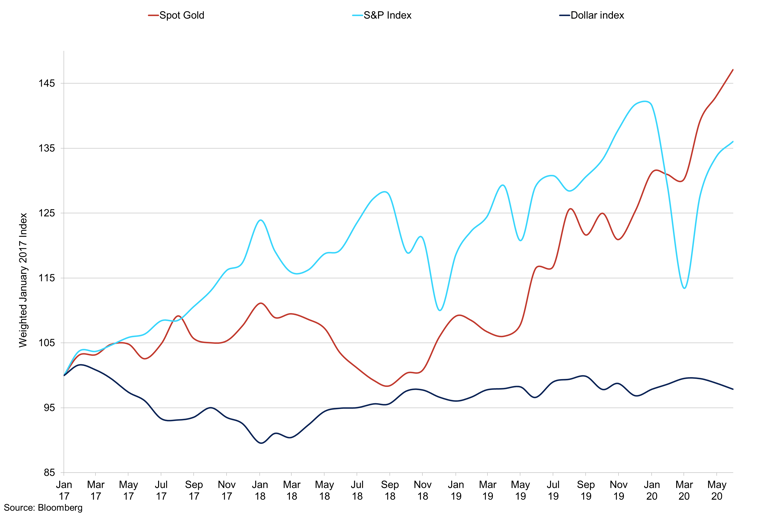

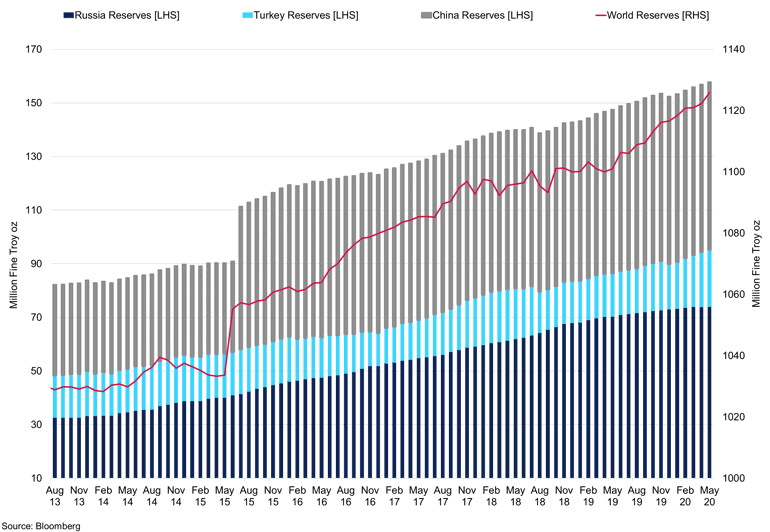

Gold

Increased speculative demand supported the precious metal in Q2, helping it recover from March sell-offs. Record low-interest rates, unprecedented government stimulus, and continued geopolitical tensions will be supportive of gold prices in Q3, as its opportunity cost of holding remains low. Gold is poised for another quarter of growth, yet, slower to the one seen in Q2. Jewellery demand is to remain subdued on the back of consumer uncertainty. The 2011 high at $1,921/oz but this may be out of reach in Q3. We expect the trend to remain on the upside given the monetary policy climate. Range: $1,765/oz – $2,000/oz.

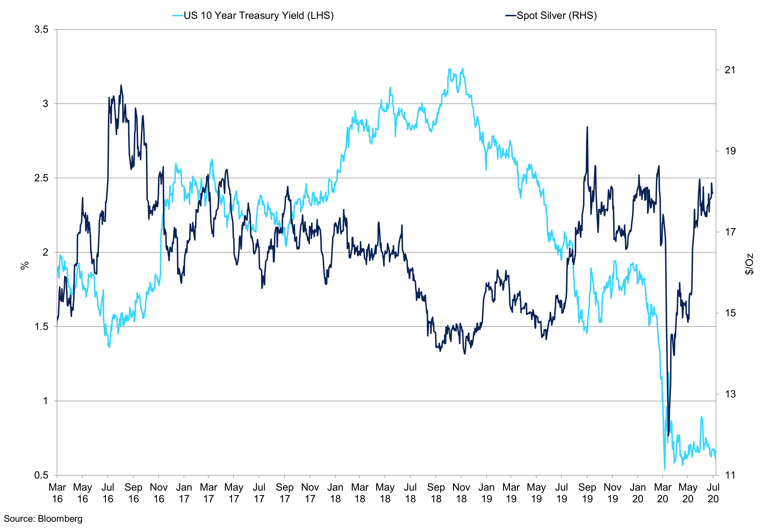

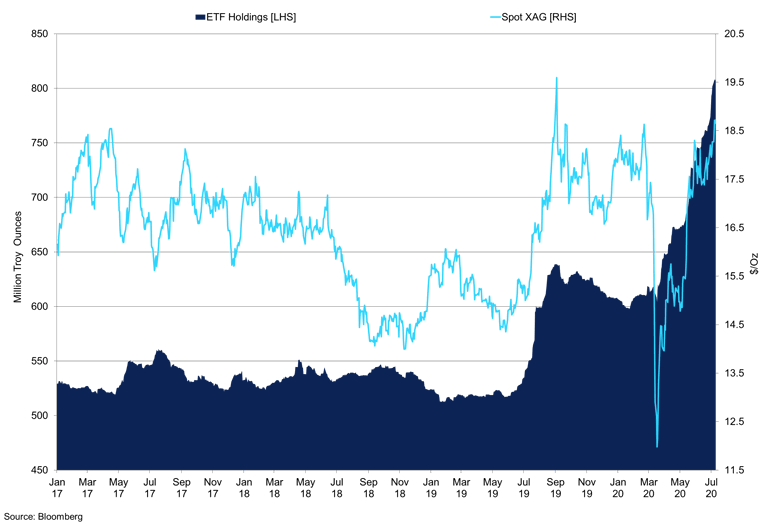

Silver

Investment appetite bounced back for silver as investors urged to safe-havens to hedge from risks posed by the spread of coronavirus. Global ETF inflows saw another round of expansion, while CFTC managed money remained subdued. While holding on to its safe-haven properties, we expect silver’s industrial demand to shine in Q3, thanks to a prompt recovery in Western economies. As risk appetite starts to improve, silver may correct to the downside, but with improving industrial and manufacturing outlook, we expect to silver to trend higher but the majority of trading to take place between $18.70 - $25.50/oz.

Palladium

Demand for palladium is likely to pick up in Q3, as reopening auto manufacturers and stricter emission regulations are likely to add to overall precious metal rally. The supply is likely to remain constrained across the world, apart from Russia, where output is to remain on track for the rest of the year. Nevertheless, the outlook for palladium remains to the upside thanks to improving economic and industrial demand. Range: $1,900-$2,450/oz.

Platinum

In Q2, platinum prices picked up from March lows due to bargain hunting interest from China. A risk-off market sentiment has kept economic activity subdued, weighing on manufacturing, capping the platinum rally. For the quarter ahead, we see recoveries in the automotive sector in Europe and the US, with China leading the way. Overall, autocatalyst demand is likely to bounce back from Q2 lows, reflecting plant openings along with a marginal rebound in consumer demand for new vehicles. Range: $800-$976/oz.

Market Overview

Global Outlook

The pandemic has been a hugely disruptive event, imposing a multilateral shock to the global economic system. In Q2 2020, the spread of the COVID-19 virus touched nearly every country in the world, causing huge global shutdowns, a surge in unemployment, the deepest recession we have seen since the Great Depression, and a lot of unprecedented policy actions.

While we saw China's cases subside at the beginning of March, the spread across the rest of the world has picked up. Developed economies, including the US and most of Europe, imposed strict lockdown measures, urging people to stay inside. As a result, global transportation nearly diminished, and demand growth has turned negative. As we begin to see the light at the end of the tunnel, we start to gauge the extent to which the economies have been hit. According to IMF, global growth for 2020 has been forecast at -4.9%, down 1.9 percentage points from a previous forecast in April.

The global economy has taken a huge hit from the pandemic, and central banks have acted aggressively to prevent a tightening in financial conditions and cushion economies. Indeed, the G4 (England, Japan, the US, and Europe) central banks' balance sheet is most likely to reach $20tr by the end of 2020. While we see demand growth picking up in Q3, it is most likely to remain under the pre-crisis levels for the medium term. Muted inflation and, consequently, lower yields should translate in low-interest rates policy from the central banks; that is until we see positive inflation growth.

Previous economic recessions and wars have had significant long-lasting economic consequences, such as a substantial increase in borrowing costs due to the destruction of physical capital and the need to rebuild. The current pandemic will most likely lead to a short-term impact on labour shortages. Additionally, governments have taken aggressive measures to offset the negative consequences of the virus, therefore boding well for a swifter recovery in Q3.

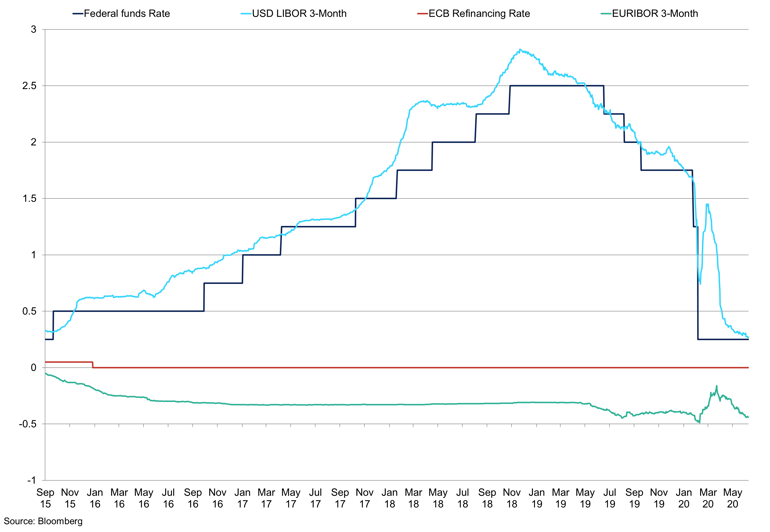

Western Economies Interest Rates

Central Banks lowered their interest rates to record lows to support the economies during the pandemic.

In Q2, markets rallied on hopes of a recovery as lockdowns across the world were eased. The rebound has helped the oversold investor sentiment, and markets and retail money seem to be priced for an optimistic outcome despite fears of a second wave. As for Q3, record levels of fiscal stimulus, sustained low levels of interest rates and muted inflation create a supportive environment for risk-asset performance. Ongoing low-interest rates will favour higher-yielding assets, such as stocks and property over government bonds and cash.

That said, the recovery will continue to look mixed as some economic indicators rebound faster than others. We attribute this to the inability of fiscal and monetary support to cushion all of the economic sectors equally. Despite big bounces, the levels of the GDP are going to remain repressed by the end of the year. Unemployment rates are going to stay elevated, especially in the US. And while we see containment policies being lifted in most of the economies, the behavioural response is going to be slower. Elevated rates of savings and subdued demand are going to weigh on consumer spending. Consequently, corporate profits are likely to be down. At the same time, a surge in national debt is going to be a massive burden for the economies.

Daily confirmed cases continue to rise across the world, with the US, Brazil, India and Russia leading the way. According to WHO, the pandemic has been accelerating at rates above acceptable and additional lockdown measures are necessary to halt the spread of the virus. Tracking the virus' progress remains a key market focus. Indeed, a vaccine is not expected in the medium-term, so finding a new normal will be key at maintaining the curve suppressed.

On April 20th, WTI crude oil futures fell into negative territory for the first time due to the combination of higher supply from a price war between members OPEC; the demand hit from COVID-19 and high inventories. While the oil market remains weak, the recent modest price recovery indicates that H1 2020 ended on a more optimistic note. Data shows that demand destruction has been less than expected; however, it is still unprecedented. Indeed, as American producers began idling rigs and laying off workers, Trump called Russia and Saudi Arabia to agree on output cuts, helping to lift prices to around $40 in June. Additionally, demand in China was almost back to pre-virus levels, and US consumption is gradually rebounding. The second wave of infections remains a downside risk for oil prices.

For Q3 2020, many workers might decide to stay working from home, and air travel will not recover to normal levels anytime soon. On the other hand, low oil prices and the desire to avoid public transportation had some people driving to work for the first time in months. Ultimately, demand will depend on how the pandemic impedes mobility and trade since more than 60% of oil is used for transportation. On the other hand, power demand is likely to increase in Q3, thanks to reopening of manufacturing facilities as well as air conditioning use during the summer season. OPEC+ expects a 1mb/d increase to come from power generation demand in 2020. Overall, according to IEA, oil demand in 2020 is expected to fall by 8.1mb/d, the largest in history.

From the supply side, record output cuts from OPEC+ and non-OPEC producers saw global oil production fall by a massive 9.4mb/d in June. In addition to a 12mb/d plunge in May, investment in oil has also collapsed, possibly supporting prices through lower supply in the long-term. To further speed up market rebalancing, OPEC+ decided to extend their historic output cut of close to 10mb/d through July.

The latest IHS PMI for the US suggests that economic activity continued to decline in June but at a much slower pace from a month before. This was mostly attributed to a decline in activity in the broad service industry. The PMI for manufacturing picked up from 39.8 in May to 49.8 in June, a record increase, as job losses eased and selling prices picked up, after having fallen very sharply in the previous three months. Overall, contraction in output slowed as new orders have stabilised amid relative improvement in demand conditions. The PMI for services improved from 37.5 in May to 47.9 in June. Overall demand remains weak; however, deceleration of the decline in economic activity reflected the easing of economic restrictions.

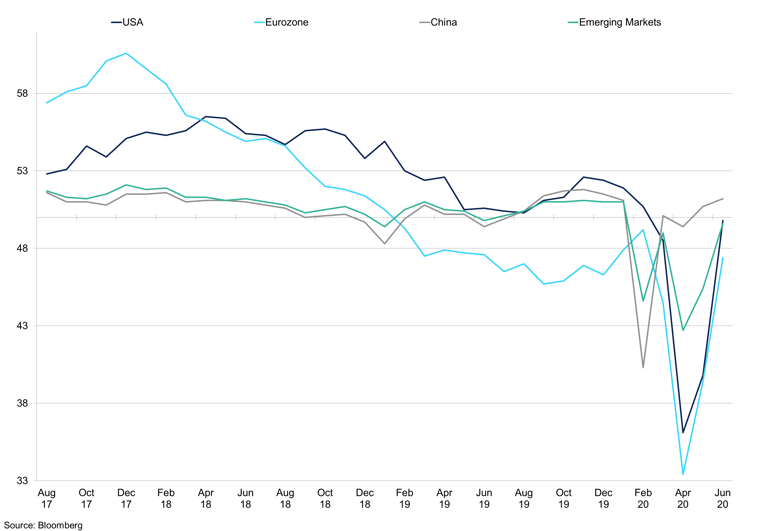

Manufacturing PMIs

While China's manufacturing is seen close to the pre-crisis level, Europe and the US are yet to recover fully.

The PMIs for the EU, similar to the one of United States, indicate that economic activity continued to decline in June, however, at a more modest pace than before. Indeed, the manufacturing PMI increased from 39.4 in May to 47.4 in June. While this shows a steep rebound, operating conditions remain challenging, as new orders remain subdued. All countries showed a relative improvement, with France posting at 21-month high at 52.3. Overall, the sharp turnaround implies monthly gains are likely to persist in the coming months. The PMI services index increased from 30.5 in May to 48.3 in June. Many other companies, both in manufacturing and services weakened demand as business, and consumer customers remained cautious with respect to spending.

In China, service sector activity expanded at the quickest rate for over a decade in June, thanks to rising business activity and new orders. Business confidence strengthened to a 3-year high. Unfortunately, employment continues to decline. Manufacturing activity strengthened, however, at a slower rate to that seen in services. The sector continues to recover from the COVID-19 crisis, as rising production and a renewed increase in total new business persist. External demand remains subdued. Manufacturing PMI increased from 50.7 in May to 51.2 in June, to signal a second successive monthly improvement in the sector. Exports, however, continued to fall amid reports of weak external demand. Although the rate of output softened from that in May, it remains solid overall.

It is important to note that the PMI index shows the change in activity, not the actual level of activity. Thus, when the PMI falls and bounces back to near 50, it means that activity fell sharply and then stabilised, whereas a move above 50, would indicate a V-shaped recovery.

US

The COVID-19 disease has dealt a severe blow to the American economy. In Q2, unemployment has picked up to record highs to 14.7% in April, up drastically from 3.8% in February. As expected, retail, entertainment, and hospitality have been hit the hardest, and all service-sector industries saw massive job losses. The decline in consumer spending drove the decline in economic growth in the US. Indeed, we saw declines down to -6.6% m/m in March, which have contributed to GDP growth of -5.0% q/q, and with consumer spending figures at -12.6% for April, we expect GDP growth to be much lower for Q2. While we see some recovery in retail, food and accommodation spending in the upcoming quarter, business and residential investments are set for further losses due to continuing high level of uncertainty and lower-than-expected incomes.

In the long term, this pandemic is likely to bring structural changes to the economy, and demand patterns are likely to change, especially if we see a continued incline of infections. Extended lockdown measures and their slow relaxation could keep businesses struggling even if venues fully open. Without a second round of stimulus checks, the impact of spending could be substantially negative. Indeed, the enhanced unemployment insurance is set to expire by the end of July, with the aim of boosting job numbers and encouraging people to return to work. Instead, the White House may consider a 'return to work' bonus pay to incentivise people to return to the offices. At the same time, nearly 43m people have filed for regular unemployment insurance, and more than 6m have filed for Pandemic Unemployment Assistance. Although unemployment rose very swiftly, we do not anticipate the recovery will be nearly as speedy. The unemployment rate could remain in the double-digits for the remainder of 2020.

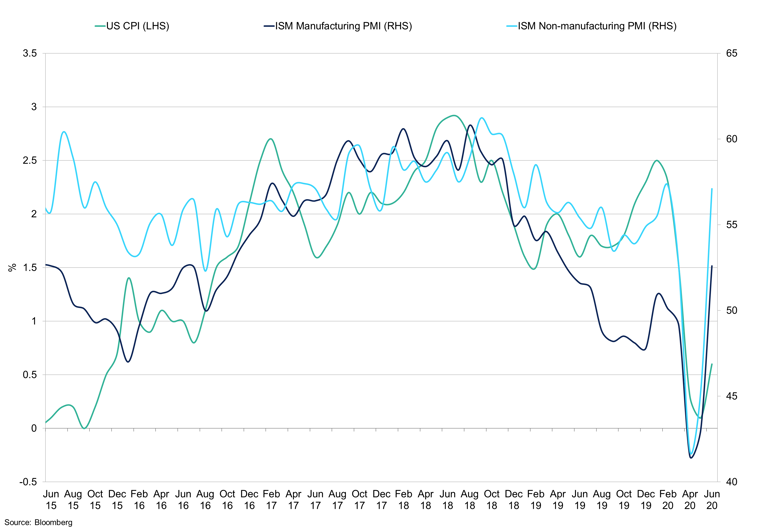

US CPI vs non- and Manufacturing PMI

Non-manufacturing and manufacturing activity bounced back to normal levels, while inflation remains dormant.

Overall, the economy should continue to recover in Q3 thanks to looser quarantine restrictions; however, GDP growth will likely remain subdued for 2020 until the disease is fully controlled or a vaccine is safely and effectively implemented. Trade, in particular, will face some strong restructuring challenges. COVID-19 erupted the way the supply chains operate, and the pandemic has created anxiety about food security and pressure for domestic production of medical equipment. We, therefore, see countries pushing forward with the protectionist measures and implementation of self-reliance techniques to ensure partial or complete self-sufficiency in the future. Additional strains of US-Sino trade war should make this transition more rapid for the US.

As far as the number of coronavirus-related cases, the number of infections from the first wave never fell except in New York, where there is the highest population concentration. Strict measures imposed in New York were the main reason behind a significant decline in numbers in May, replicating the curve seen in Europe. Meanwhile, there is currently a surge in new cases across the rest of the country, especially in Western and Southern regions, with the majority of the states reporting new spikes in new infections. While testing has uncovered cases which were previously undetected, the proportion of positive tests skyrocketed. Surprisingly, research showed that June's protests did not cause a spike in coronavirus cases. The latest flareup in the US has been spooking financial investors, jeopardising the case for economic recovery. So far, the outbreaks have been localised and are likely to stay that way. Therefore, it will be crucial that the government's response to the intermittent localised outbreak is appropriate and effective in spread control.

Indeed, a recovery in the stock market and the economy will provide Trump with his best chance for a win in November. At the time of writing, Trump is losing support in key states due to his handling of COVID-19, and lately, of the BLM movement. Falling unemployment levels, additional stimulus checks, as well as proper control of the virus spread, should provide support to Trump's poll popularity. On the plus side, if the high number of coronavirus cases persists, the US should be better prepared in terms of healthcare capacity and treatment. Also, news of the new vaccine looks promising; however, most likely to remain under development until next year.

In March, as the pandemic started to unfold, we saw many workers dismissed, resulting in disposable income falling 2.0% m/m in March, as consumers began to face economic restrictions, avoiding visiting non-essential shops and conducting leisure activities. In April, we saw unemployment peaking to record highs, and the government was urged to provide massive stimulus checks in the form of cash disbursements. As a result, real disposable income increased to a record 13.1% m/m, but much of it has been saved rather than spent. The US savings rate as a percentage of disposable income increased to 32.2% in April from 8.4% in February.

This trend, however, was short-lived. The pattern reversed in May as stimulus checks declined, leading to real disposable income falling 5.0% m/m. Nevertheless, spending on non-durable and durable goods increased by 7.0% and 28.5% respectively as people chose to cut down on savings. Spending on services, however, grew only 5.2% after falling 12.0% a month prior. As the US lifts its lockdown restrictions, we expect spending on services to increase, and the savings rate to subside further, however, remain at elevated levels. Indeed, retail sales bounced back after falling dramatically during the outbreak of the pandemic, as non-essential shops started to reopen. Clothing store sales increased by 188% m/m in May and consumer confidence stabilised. On the downside, if cases continue to rise and economic uncertainty persists, we would expect the savings rate to stay high.

Inflation has been subdued since January; however, we could see a change in that dynamic over the course of 2020-21. Lower oil prices and weak demand have been disinflationary so far; however, once the economy stabilises, there is a risk of a spike in inflation due to massive fiscal and monetary support provided by the government. Additionally, we have seen average wages rise since the beginning of the lockdown, pushed up by lower-wage earners losing their jobs. Similarly, earnings have declined significantly in industries such as energy, industrial and consumer sectors. The core consumer price index dropped to a 5-year low of 0.1% y/y. Disinflationary forces are likely to fade in Q3 2020 as the nation re-emerges from the containment measures; however, the recovery in demand will be gradual.

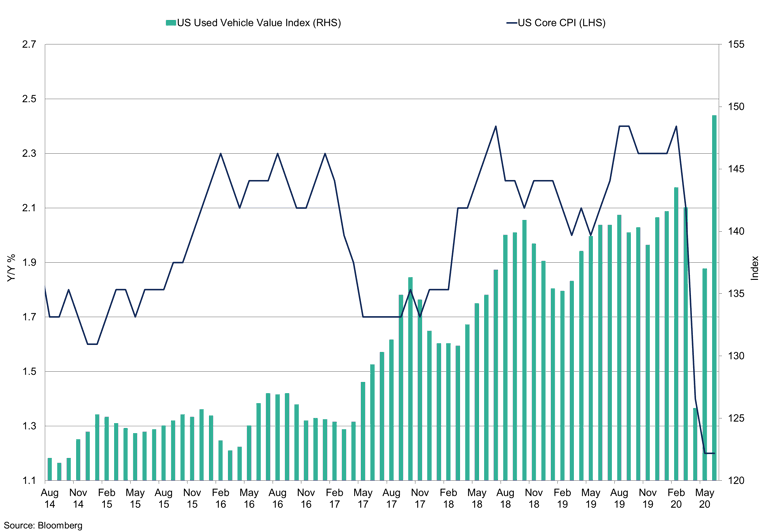

US Core CPI vs Used Vehicle Value Index

US Core CPI remains subdued, while used vehicle value index is seen picking up due to increased vehicle sales.

The Fed cut rates to 0.00-0.25%, committed to unlimited asset purchases and implemented lending facilities. These measures provided market liquidity and access to credit. Although the Fed has offered unprecedented support already, there is still capacity within the existing toolkit. Rates will be kept low for the long term, as clearly stated by the FOMC. Additionally, the US government has provided a massive fiscal stimulus to mitigate the permanent damage that could be done by consumers and businesses going idle. The fiscal stimulus packages include forgivable loans to small businesses and unemployment benefits for employees who lost their job. While this legislation supported the individuals and companies, it will not be able to help in relation to falling output and high unemployment.

In the Fed's latest minutes statement, the Fed confirmed its commitment to supporting the US economy through a full range of tools, aiming to promote maximum employment and price stability goals. The Federal Reserve will continue to increase its Treasury and commercial mortgage-backed securities security holdings to support credit flow to households and businesses. We believe that the provisions will be continued at a similar pace to support smooth market functioning. Another round of fiscal and monetary stimulus measures will be needed to underpin that recovery. The astronomical level of support; however, has come at a very high fiscal price, leaving the economy with a record high debt to GDP ratio, even higher than during World War II. Indeed, the Fed's quantitative easing programme has absorbed about 60% of the increase in public debt since February, preventing a spike in yields.

Europe

We have seen EU economies emerge from strict lockdown measures and, so far, there has been minimal evidence of the second wave of coronavirus-related infections taking hold. Even before the pandemic hit the bloc, the economies lacked policy ammunition. The European Central Bank policy rate was already negative, at -0.5%; there were strict rules around increasing fiscal spending, and high-debt countries like Italy were subject to posing a risk to Europe's financial stability. Indeed, the EU has suffered years of lacklustre growth, in which strong domestic demand offset faltering exports. As the pandemic hit Italy, demand collapsed, and lower export levels weighed on manufacturing. Unlike in the US, labour interventions have helped to keep workers connected to the workforce, preventing an unemployment spiral.

Economic estimates, such as GDP growth, confirmed lockdowns devastated the Italian economy in Q1 2020, as the virus hit. The economy shrank by 3.6% q/q in Q1. As a result, business and household activity have been suspended by the end of March. The economic blow was felt even more strongly in Q2, due to the expansion of lockdown measures, which are currently being lifted throughout the Eurozone. The unprecedented collapse of industrial production, retail sales, poor economic sentiment and PMI readings all point to the destruction in both service and manufacturing sectors. Indeed, industrial production in Europe sank to the record lows in April, down 28% y/y. Output for capital goods was 27.3%, and output for consumer goods fell 10.7%. In contrast, the energy was down only 4.8%.

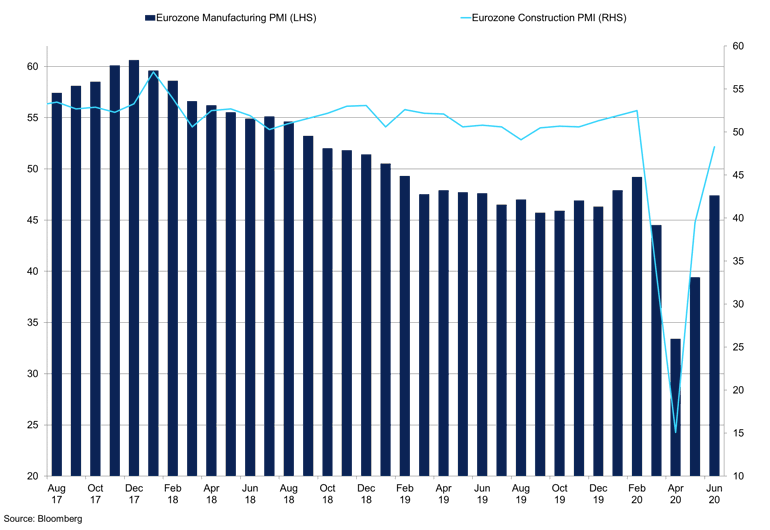

Eurozone Manufacturing and Construction

While EU's manufacturing is seen closer to the 2019 levels, construction is lagging behind.

In the upcoming quarter, June's PMI readings show that the recovery could be quicker than expected. In the political arena, divisions remain significant within EU leaders on the size and the composition of additional recovery measures. Moreover, statements by EU that they will go ahead with a European digital tax given the withdrawal of the US from OECD negotiations, risk heightening trade tensions.

The policy response has surprised to the upside. The ECB has expanded its asset-purchase programme by $263bn in May. Every member state in the bloc will run huge budget deficits this year, thanks to relaxed fiscal deficit rules. The work subsidy schemes implemented in most countries have kept the Euro area's unemployment rate low. The ECB expanded its pandemic emergency purchase programme, committing to purchase €1.35 trillion of bonds to lower borrowing costs and increase lending in the area.

Even a notoriously strict country like Germany has contributed to the most far-reaching response by proposing a €750bn recovery fund that will be funded by joint bond-issuance of all 27 members of the EU. Indeed, Germany's government spending has surpassed any other EU member, at 38% of GDP, including new spending, supply-side tax relief, and loan guarantees. This has been done in a desperate attempt to rebalance the demand collapse. Overall, somewhere around 25% of GDP has been pledged by the EU as fiscal support, with a similar amount pledged by the ECB in terms of QE commitments.

The UK has been hit hard by the COVID-19 crisis. It has suffered high infection and death rates, which have delayed the easing of lockdowns. Additionally, Brexit negotiations add to existing economic uncertainty. There is a year-end deadline for a trade deal; however, negotiations seem to be on a standstill. Real GDP in the UK declined by 20.4% m/m in June, a record low.

The accommodation and food service sectors experienced a near-total collapse as the UK's lockdown took hold. Indeed, according to McKinsey, in the first half of April, 73% of workers in accommodation and food services and 46% of those in construction had been furloughed. Due to delayed reporting of deaths, the public health response by the UK officials has lagged those in Europe. We believe that activity will rebound thanks to the lifting of restrictions in June-July, but the upturn should come later than that of most other developed markets.

China

As the first country to emerge from the COVID-19 crisis, China set itself on a path of recovery in Q2 2020. So far, the picture has been mixed. On the one hand, industrial production and investment in property infrastructure are up thanks to heavy government spending and incentives. On the other hand, retail sales, as well as overall investment, continued to decline, as the public fears economic uncertainty prevailed. Construction activity has improved significantly in the last quarter, and many infrastructure projects are underway. Overall, the Chinese economy has been reviving at a moderate pace, but activity mostly remains below the pre-crisis levels.

China's economic recovery is on track; however, for the first time in years, no GDP growth target has been set for 2020. That said, in Q2, the economic bounce has been more vigorous than expected, thanks to a rebound in manufacturing. In the upcoming quarter, industries are more likely to take a breather to replenish their inventories, in hopes of improved overseas demand. Overall, the PPI inflation is at 2018 lows, and CPI has moderated significantly on retreated food prices.

US & China & Eurozone CPIs

China's inflation is seen lower, however, remains elevated above those in the US and Europe as a result of high pork prices in 2020.

Industrial production was up 4.4% y/y in May, edging closer to pre-crisis levels as factories began to recover from coronavirus impact; however, the weaker-than-expected gain implied that the nation's recovery remained fragile. Manufacturing output increased up to 5.2%, including a 12.2% jump of the automotive production. There was also solid growth in the production of construction equipment, thanks to increased government spending on infrastructure. Indeed, investment in manufacturing fell sharply; however, recovered up to 2.5% y/y in June, thanks to massive issuance of bonds by local governments. Overall, in Q2, manufacturers have caught up on lost production; however, new orders remained weak as global demand has fallen off. Domestic consumption will be the main driver for 2020 growth, and an improvement in exports will be critical to Chinese industrial recovery.

Retail sales fell 2.8% y/y, well below the pre-crisis levels of 7-8%. Nevertheless, Chinese retail is recovering, with home appliances, automobiles, and furniture being the best-performing categories. The overall business resumption rate stands at 88% of a pre-crisis level, with restaurants still below January's levels.

China Retail and Industry Indicators

Main indicators show a quick bounce from April lows; however, a path to recovery to the pre-crisis levels is still ahead.

The renminbi has fallen significantly in Q2, likely because of weakening exports to the rest of the world, and fears over US-China disputes over trade and capital flows exacerbating the outlook. A lower-valued Chinese currency means greater competitiveness of Chinese exports and, subsequently, lower competitiveness of American exports. Yet, under the terms of a trade agreement with the US, China is obliged to significantly boost imports from the US, and a lower-valued renminbi works against that goal. Indeed, in their recent statement, the US Chamber of Commerce urged China to redouble its effort to implement the trade deal requirements. This would imply a significant increase in China's purchases of US goods and services. Recent decisions by China, including its uncooperative behaviour with US COVID-19 investigations, intervention in Hong Kong national security law and a border dispute with India are diminishing the country's goodwill.

The government has announced further stimulus measures, including coupons to households to encourage spending, and the PBOC has made monetary policy more accommodative. The stimulus size is nowhere near the size of 2015/16 or of the financial crisis of 2007-08 as the government is worried about excessive levels of debt. While geopolitical risks are on the rise, we believe the discussions between the US and China is unlikely to see the Phase One trade deal terminated in Q3 2020.

Emerging Markets

As the global COVID-19 crisis evolved in emerging markets, the rise in debt levels posed risks for already economically vulnerable economies. As global investors began to realise the magnitude of the pandemic, they pulled their funds from emerging markets and into safe-haven assets. Portfolio outflows from emerging markets outpaced those seen during the last financial crisis. The US Fed injected huge sums of liquidity into financial markets, helping emerging markets. Additionally, swap lines with the rental banks of overseas economies reduced the risks of drying up dollar liquidity in those countries. The IMF also contributed more than $9tr towards global fiscal support to fight COVID-19, with emerging and developing markets taking the biggest share.

However, these countries are still facing sharp increases in financing needs through increases in government spending to cushion the fall in demand, causing the rise in government debt as a share of GDP. Overall, according to the IMF's own estimations, emerging market financing needs to be at least $2.5tr, $1.5tr higher than the IMF's lending capacity budget. The IMF is unlikely to increase that budget this year due to America's reluctance. Meanwhile, global investors seem relatively optimistic about the emerging market economic outlook, further financing their economic needs.

Emerging Market Currencies

Weaker emerging market currencies will help support exports.

The issues in emerging market economies could have significant implications for the rest of the world. Indeed, foreign banks own about 50% of all emerging market external debt, exposing them to the risks of default. Should commodity prices and exports remain subdued, the risk of default could linger after the pandemic is over. Nevertheless, the impact on emerging economies in 2020 could be quite devastating, especially when comparing to other countries.

While emerging market equities enjoyed a V-shaped recovery, the economic outlook remains uncertain. The lockdown measures to contain the virus ease, but the near-term outlook for the emerging markets remains dire. Still, we expect growth to improve marginally as domestic demand picks up. The oil hit is gradually fading, commodity prices have somewhat stabilised, and inflation is tame. A rebounding US economy and steady growth in China also will be helpful. Historic low-interest rates and substantial fiscal easing in most emerging market economies will also support a gradual economic upturn this year. Additionally, a less-bleak external backdrop will support commodity prices and trade balances, but trade tensions and the virus spread are still threats. On the downside, monetary easing by central banks seems largely exhausted and mostly priced in, although unconventional policy measures could still provide further support in some economies.

The Americas, as a whole, represent 50% of global cases, with Brazil taking the biggest proportion of these cases. Bolsonaro has been criticising lockdown and social distancing measures, resulting in inadequate response to the virus. The country's fiscal and monetary response has been relatively positive; however, the nation's limited balance sheet, similar to the rest of the emerging markets, leave small room for other stimulus support. The Selic Target rate has been cut down to 2.0%, from 4.50% at the beginning of the year. The authorities estimate the direct fiscal impact at around 6% of GDP, just under 10% threshold. Overall, governments have addressed the pandemic differently, implying an uneven economic outlook for emerging market economies.

Aluminium

Summary

Global aluminium output has remained strong in 2020 despite the coronavirus and some loss-making capacity being taken offline. According to SMM, Chinese output of aluminium was 18m tonnes for H1 2020. However, underlying demand has been weak due to the coronavirus as sequential economic data improves this has buoyed market sentiment but on a historical basis demand is weak and coming from a low base. We expect H2 2020 to try and offset the losses incurred in H1 but the key will be where the demand recovery plateaus at, and how far below 2019 levels that is.

Q2 Review

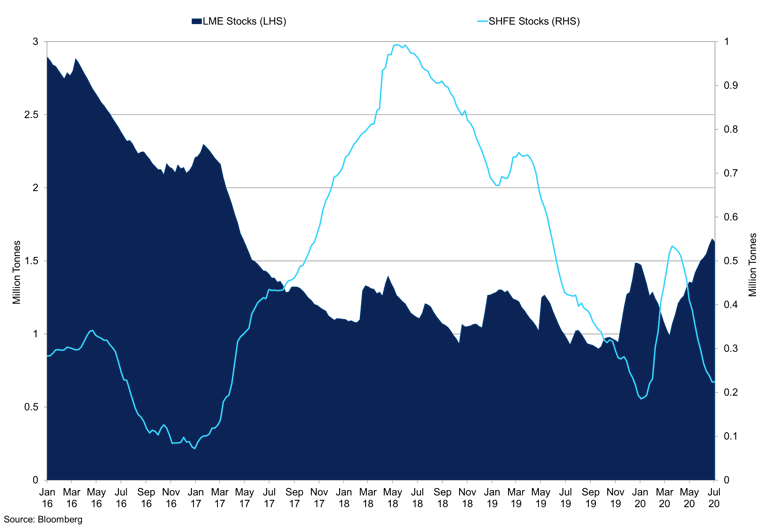

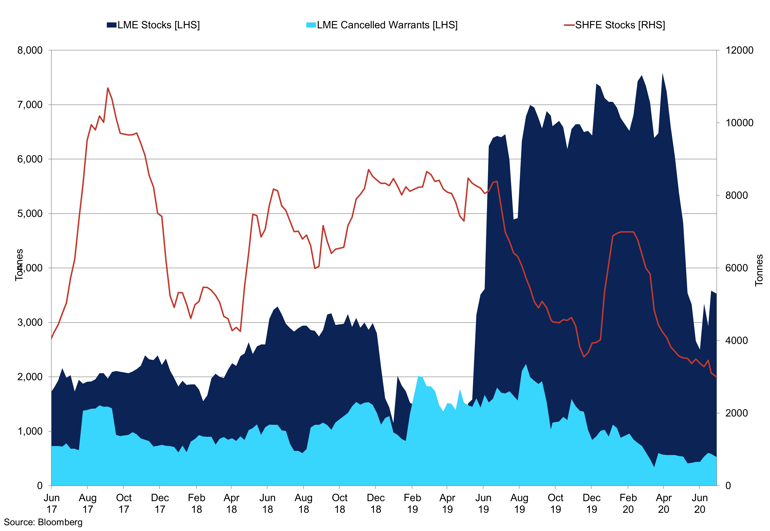

Activity in Q2 saw risk appetite return to the metals markets, despite the prospects of weak demand; and prices have gained 6% to close on the front foot at $1,527/t. YTD losses are 6.48%, and as positivity returns to the market, prices have surged in Q3 so far. Consumption for aluminium has started to improve as construction comes back online with economies reopening, on a month on month basis auto sales are recovering. This should be to the benefit of aluminium, especially in the US who favour aluminium sheet in autos. LME inventories have soared higher this year up 10.8% YTD; this does not tell the full story. In Q2 alone, stocks have gained 42% 1.63min tonnes and from the March low material inflows have improved 68.78% from 967kt to 1.633m tonnes as of July 9th. We did see the cash to 3-month spread tighten into $13/t contango, but the market has weakened back out to $31.5/t contango. Shanghai deliverable stocks have been falling in recent months, falling from 534kt to 224kt as of July 3rd, SHFE prices have rallied incessantly in recent months to RMB13,990/t up 21.18% in Q2.

LME vs SHFE Stocks

Exchange inventories have diverged in recent months. The carry-trade triggered flow into warehouses.

Outlook

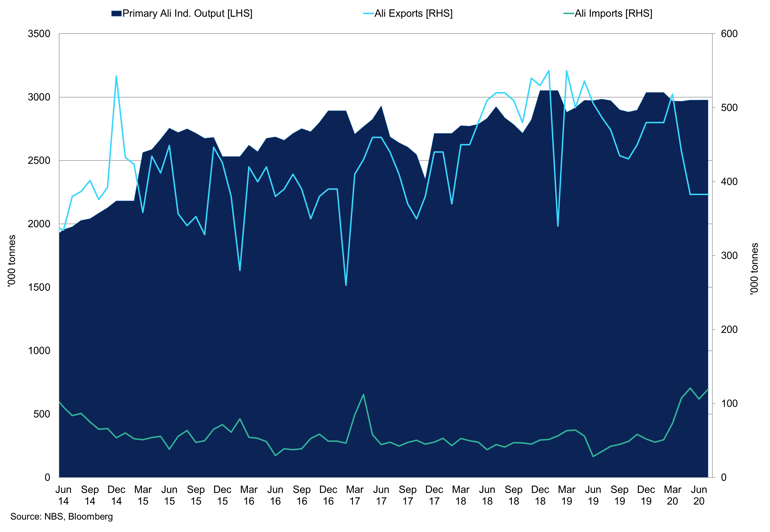

Chinese primary aluminium production increased in June by 2.42% to 3m tonnes according to SMM, primary capacity has increased on a month on month basis, by 180,000 tonnes bringing total capacity to 36.76m tonnes. Aluminium producers' operating rates have increased in recent months from the low in March of 87.85% to 89% in June. H1 2020 output of aluminium in China has remained strong despite large proportions of smelters losing money due to the sell-off. However, the recovery in prices has improved margins and could see the output in H2 2020 expand further, YTD production reached 18m tonnes up 2.93% y/y. We expect output to increase again in July, the most up to date NBS data indicates that output of aluminium products reached 5.1m, tonnes bringing total output to 20.95m tonnes up 14.5% y/y, we expect June's production of aluminium products to increase. Electrolysed aluminium production has remained constant in recent months around 300,000 tonnes. May production was 297,700 tonnes bringing YTD production to 1.4m tonnes, down 0.1% on the year.

China Industrial Output - Primary Aluminium vs Exports and Imports of Unwrought & Aluminium Products

Output of primary aluminium has remained near highs in 2020, but exports have fallen outlining weak ROW demand.

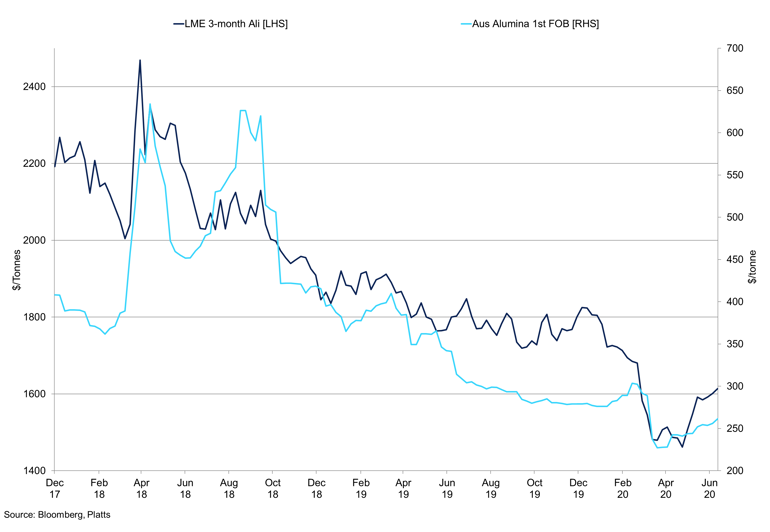

ROW production, according to the International Aluminium Institute (IAI) was 2,354,000 tonnes in May down 1% y/y. Production could fall further following the closure of Alcoa's smelter in July. Output losses due to the coronavirus are starting to come back online, and this may result in downward pressure on prices. With prices around $1,700/t, the majority of global production is in the money, and this could see further capacity come back online. The SHFE rally has also incentivised Chinese production with some idled smelters restarting production. The value-added output will also improve due to tax rebates. Alumina production has remained strong, and according to the NBS, output in May was 5.94m tonnes in China, down from 6.07m the month prior. Imports of alumina improved marginally in May to 268,573 tonnes from 219,000 in April. East China's 99% alumina index price was RMB2400/t as of July 9th with the 1st generic Australia Platts alumina contract at $263.78/t during the same period. The relative strength of alumina prices in recent weeks is due to the reduction in capacity at Alunorte.

3-month Price vs Alumina 1st Generic FOB

Alumina prices have rallied in tandem with 3-month aluminium prices, but for different reasons?

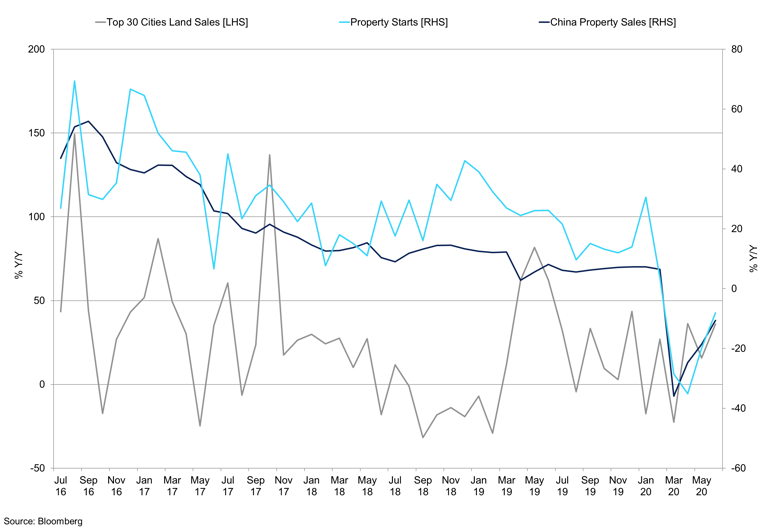

Operating rates have improved in recent months, according to SMM; however, some producers kept rates relatively high compared to other products and metals. Indeed, aluminium industrial extruder operating rates have increased in recent months to 63.77 in May, up from 56.10 in April. Construction extruder operating rates are 63.21% in May, down from April, which was 63.73%. China's construction PMI decreased to 49.9 from 54.07 the month prior; there are signs of improvement in the property sector; however, sales, starts, completions and land sales were all down in May. Land sales in the top 30 cities were positive and at 36.01% and this may indicate stronger demand for aluminium extruders in the longer term.

In Europe, the construction PMI is 48.3 and is still recovering from the lockdown low of 15.1 in April. The data is improving on a sequential basis, but demand outside of China remains weak, US housing starts did marginally recover in May to 974,000 up from 934,00 in April but remain far from pre-pandemic levels of 1.26m. Lacklustre demand for aluminium semis outside of China has led to a decline in imports and an increase in stocks on the mainland. Exports were down 28.6% in May at 383,000 tonnes, according to Chinese customs data imports into China of unwrought & aluminium alloys improved slightly in May to 87,871 tonnes up from 71,225 tonnes. The aluminium arbitrage has also declined and at the time of writing stands at $120 SHFE CIF physical premium over LME. The incessant rise in SHFE prices relative to LME has reduced propensity to export and narrowed the arb.

Chinese Property Market

The Chinese property market has shown signs of improvement in recent months, but there is still ground to make up.

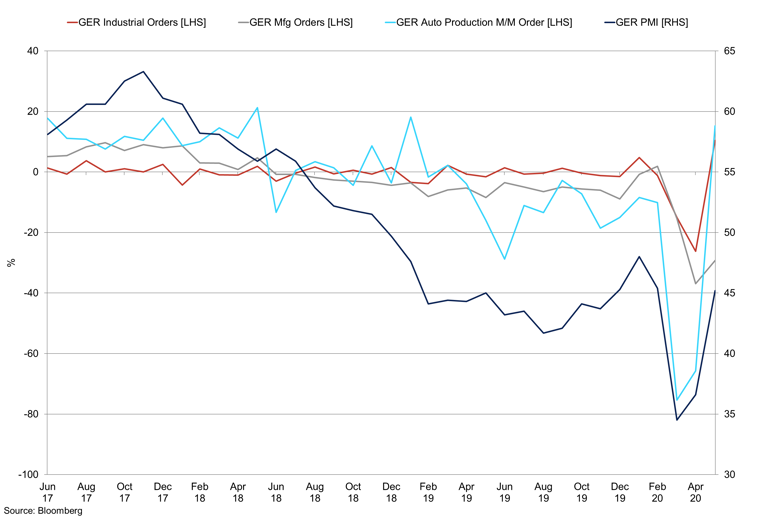

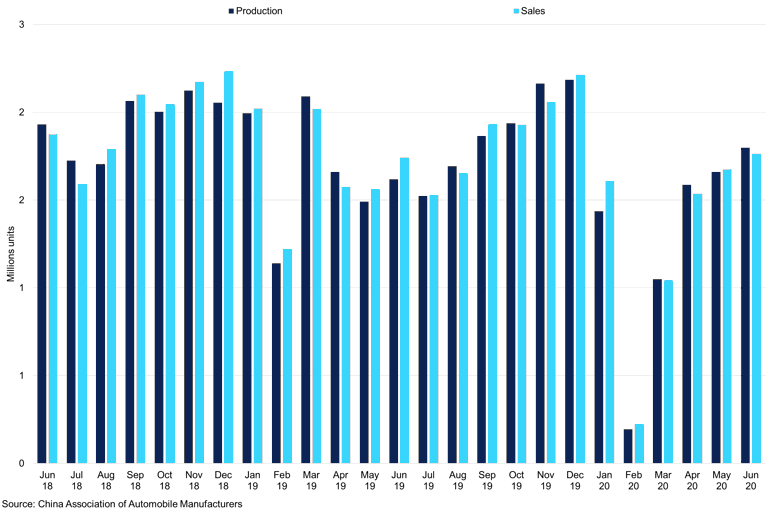

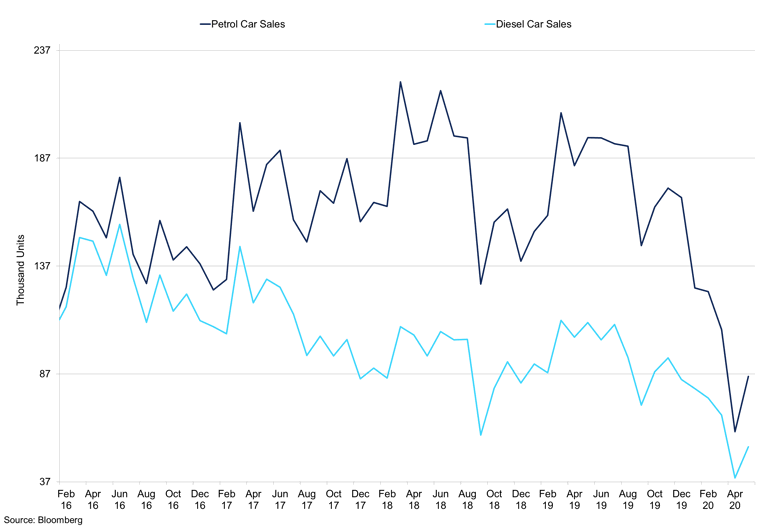

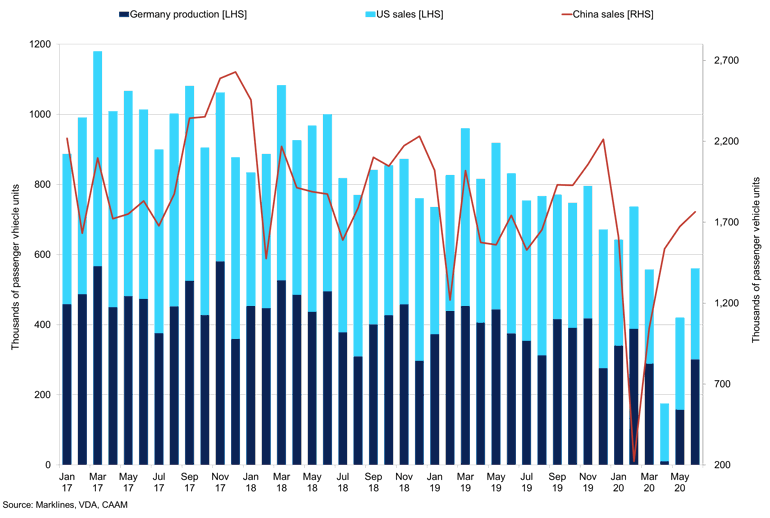

Auto production continues to recover on a month on month basis, growing 18.2% y/y in May, production YTD is down 24.1%. Passenger cars YTD are down 29.1%, but in May we saw output recover strongly to 11.2% y/y and 4.5% m/m, commercial vehicles output was also strong in May up 47.7% y/y but on a YTD basis production remains weak at -1.4%. In our opinion, we believe Chinese output of autos will continue to improve on a month on month basis, reducing the losses on year on year basis. In Germany the IFO auto production business climate index is still heavily negative at 35.9 for June but recovered marginally off the lows at -67.4 and -53.3 for May and April respectively, once again we expect this reading to recover in the near term although production and sales will remain weak due to the lack of appetite for autos in Europe. Order assessment for autos in Germany is still poor at -49.8 for June just off the lows at -52.8 in May, improvement in orders across the globe is more bullish aluminium but especially in the US where automotive sheet is more popular. We expect a strong recovery in automotive sheet production in H2 2020 and 2021 in tandem with auto output.

Copper

Summary

The recent rally in copper is overextended, and while there is tightness in the concentrate market, we expect this stress will be alleviated as mine supply comes back online, we look to TCs which remain low for an indication of improved availability. 5G and infrastructure investment in China is helping demand recover, but we are still down on the year. Consumer spending will start to improve on a sequential basis, but uncertainty surrounding unemployment will act as a headwind. While we expect a correction to the downside and gains to be less pronounced in Q3, the power of idle funds during the pandemic could increase the distortion in the market.

Q2 Review

Copper prices surged higher in Q2, outperforming most market expectations, 3-month LME prices gained 22.8% in the quarter and closed at $6,015/t. Prices gained further ground and tested appetite above $6,500/t, which we think is an overextension on the upside despite the tightness in the concentrate market and recovering demand. Stimulus from China has helped demand, but it is still off the previous year’s levels, however with significant funds on the side-lines due to uncertainty we believe CTA and system funds saw copper repeatedly break key resistance levels triggering further buy signals. In a similar vein to the stock markets, expansive liquidity measures by central banks and governments have aided the trend but do not reflect the underlying economic situation. The stimulus was necessary and still is, but when these measures are tapered, we could see reality set in, especially with redundancies after COVID unemployment benefit schemes stop. The rising cases across the globe and in particular the U.S. remains a concern, and we expect economies to run at a lower capacity for longer.

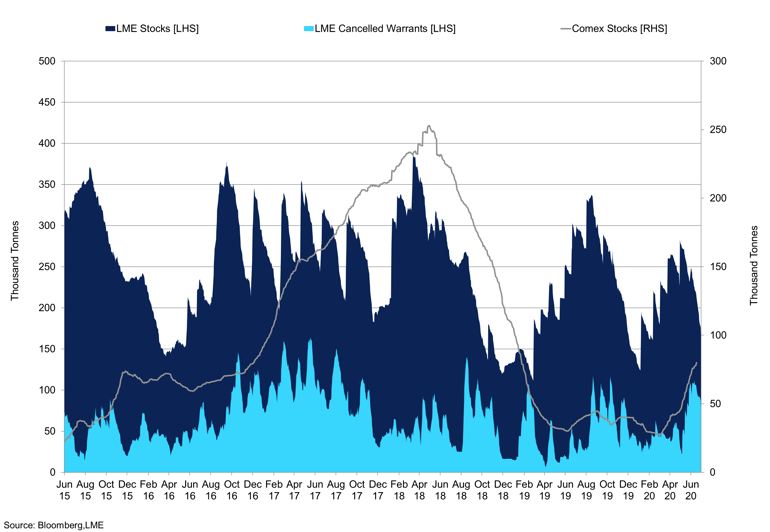

LME and COMEX Copper Stocks

COMEX inventories have been climbing as LME warehouse stocks have fallen recently.

Outlook

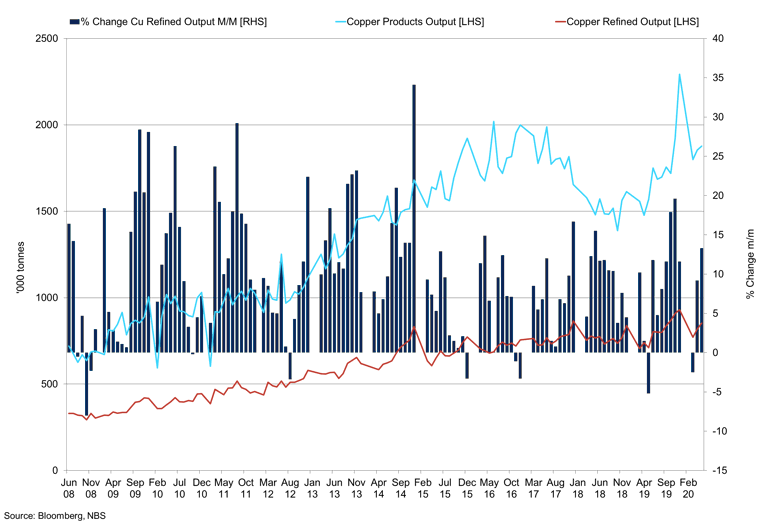

Refined copper production increased in June, according to NBS data to 860,000 tonnes, up from 853,000 the month prior, this brought total production to 4.82m tonnes. May production was up 3.5% y/y, and 4.6% m/m. Copper products production was also stronger in June, at 1.98m tonnes; YTD total reached 9.39m tonnes up 17.3% y/y and 6.1% m/m. Cathode production fell slightly in June by 1.42% m/m to 759,200 tonnes; the fall in production was attributed maintenance at some smelters. China copper cathode output stood at 4.43m tonnes through to the end of H1 2020. Smelter activity has remained strong, but we expect maintenance at the smaller smelters to be offset by strong production at larger smelters. This could cause production to be largely flat in July, and there is downside risk to copper production in July which would give rise to LME and SHFE prices. The lack of raw material could keep copper smelters from achieving their current output capacity. Imports of copper ore and concentrate have been declining since April as mine were forced to curtail production due to COVID-19. Imports for June were 1.594 tonnes according to Chinese customs data. Imports in June 2019 were 1.470m tonnes, so we have seen an improvement y/y; however, production of refined copper and copper products has been stronger this year, and inventories of concentrate in China are lower suggesting tightness in the market.

China Refined Output vs Cu Products

Output in China has remained strong despite COVID and concentrate tightness.

According to China customs data, imports of copper ore from Chile spiked in February to 1.284m tonnes, since then imports have normalised back towards the 2-year average of 595,000 tonnes, to 604,121 tonnes in May. Due to mine suspensions, we expect this figure to fall in June once again, outlining the tightness in the concentrate market. Chile copper production has a delayed-release and total production declined in April to 470,000 tonnes, however despite the pandemic and reduced personnel output has remained strong, but this will cost Codelco down the line. Workers are tired, and cases in South America are rising, which may present some downside to copper production in Chile and raises the risk of a strike down the line. Indeed, the repeated extension of lockdowns in Peru has decimated production, prompting a fall in monthly output from 205,000 tonnes in December to 111,700 tonnes in April, bringing production back to levels not seen since Q2 2015. We expect production to have fallen further since April. However, while lockdowns are eased, we anticipate monthly output in Chile and Peru to start to recover, helping to alleviate some of the tightness in the concentrate market. It remains to be seen how quickly miners can get the material out the ground, onto a boat to China and to a smelter. Major copper miners in countries across the globe are seeing mines start to re-open some at reduced capacity, and as production improves the current high prices may prompt some producer selling. The reduced availability has prompted TCs to fall, with copper concentrate TC 25% CIF $54.50/t, according to Asian Metal Inc. which suggests reduced availability of material The treatment charge index by SMM has also been declining since March 2020, standing at $51.71/t as of June 30th 2020. The dispute with workers and Codelco presents a threat to the recovery of activity at their mines back to full capacity, but on the whole global copper mine supply will improve in Q3, giving rise to TCs.

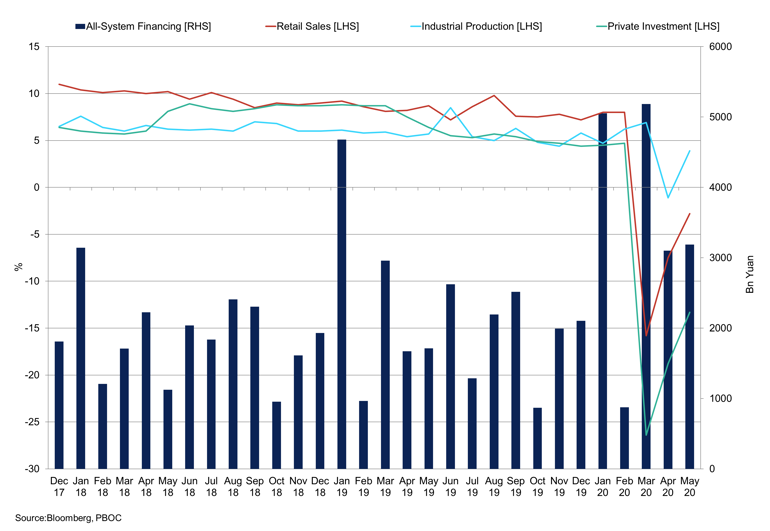

China Macro Indicators

PBOC liquidity measure and bond issuances have been strong so far in 2020, but some measures will be paused.

The Chinese export market remains weak, in May exports were 9,103 tonnes, down from 55,455 tonnes in February. Export destination economies are starting to improve, and we expect futures exports to improve as countries come out of lockdown and governments provide stimulus. However, there is a strong disconnect between major economies and developing countries. Developed economies can increase stimulus and debt levels to help the recovery, whereas developing countries have less ammunition to deal with the economic crisis, so we could see the divergence grow between developed and developing countries. The PBOC has stalled on loans after fears of asset bubbles after the recent trends, aggregate financing in June and May reached RMB3.43trn and RMB3.19trn respectively, there was also an increase in household loans to RMB981bn in June, fixed asset investment was also stronger in China in June, and this suggests infrastructure projects are on the horizon. However, the recent rally in prices and recovering demand does not necessarily suggest that all is well. The longer-term impacts of the recent liquidity injection across the globe will, in time cause cutbacks in spending. Indeed, smaller companies who have borrowed money may not be able to pay back debt, and once unemployment support schemes finish, we expect redundancies to be made.

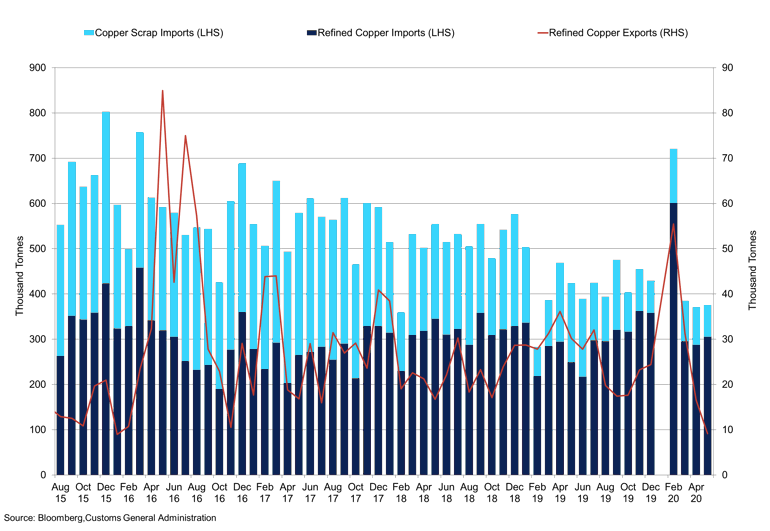

China Scrap & Refined Copper Imports/Exports

Both imports of scrap and ore have declined, tightening availability in China as demand recovers.

Downstream activity expanded again in June as investment came to fruition, the SMM PMI for copper downstream activity was 52.52. Sectors such as construction, home appliances, transport, and power electronics are part of the PMI, and there was some hesitancy from the producer side to buy and stockpile material. Inventories fell as prices increased and export orders remained weak. Operating rates were strong for wire and tube producers have increased back to pre-pandemic levels with wire producer activity are particularly strong. Plate/sheet producers have struggled to get back to operation rates pre-COVID 19. Copper premiums are recovering, suggesting demand for material, and we expect this to remain the case. However, the export markets remain weak, and as the U.S. has to scale back the re-opening of the economy, this will be a headwind to the market. Warehouse stocks have decreased significantly in the last year, falling from 600,000 tonnes as of April 2019 to 208,000 tonnes as of June 30th. The most recent decline was aided by the opening of the arbitrage window between SHFE and LME, which is closed again now. Exchange inventories have also been falling in recent months. The scrap market continues to provide support for copper cathode demand, the lack of scrap availability has been an important trend so far this year, imports have been down nearly 50% y/y in the year through to May at 362,000 tonnes. The high exchange prices have prompted some stock to be released improving scrap availability. We expect imports to remain weak in the near term in the U.S. and Europe, especially as collection rates and scrap activity has been weak in those regions. China is scheduled to change regulations this month, but the quota scheme will remain in place.

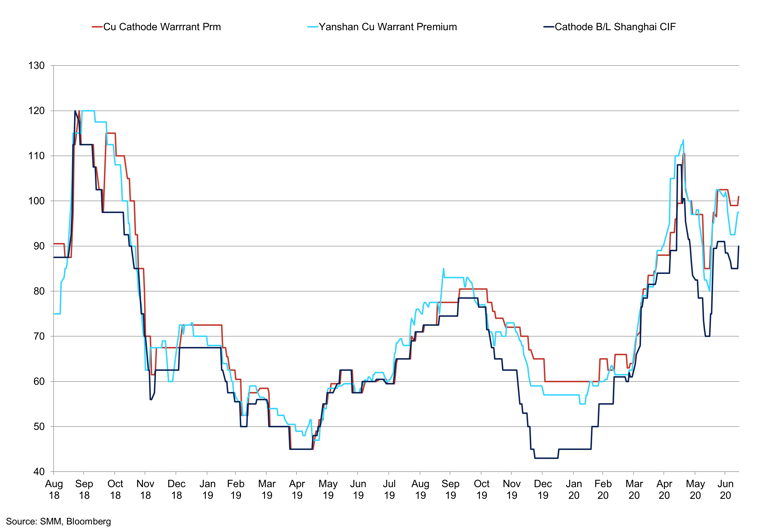

China Copper Premiums

Copper premiums have trended higher since February, but we expect gains to be less pronounced.

Lead

Summary

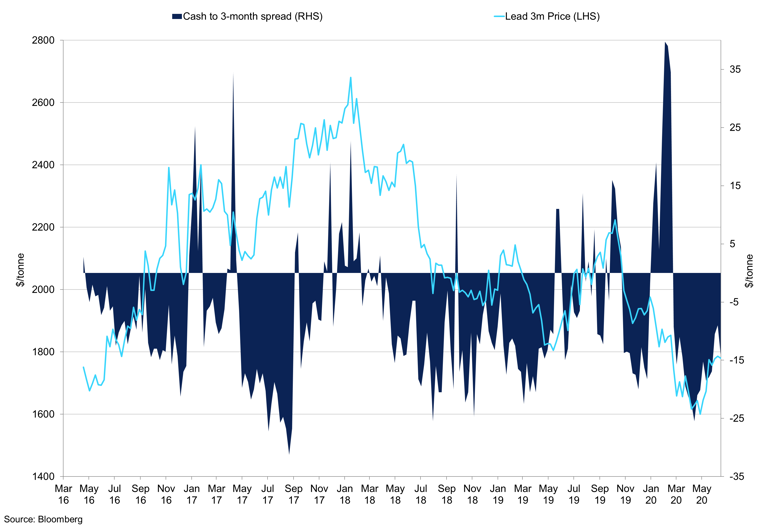

TCs have held up relatively well during the pandemic and stand at $145/t CIF, and availability should start to improve giving rise to TCs. The rally in LME prices has made importing concentrate and material in China expensive with the Arbitrage considerably offside. On and off-exchange inventories in China and historically weak demand would cap gains, as well as an improvement in secondary collection rates. If we see refined material flow into LME warehouses, this would also cap gains in the near term. We expect auto sales and production to start to improve on a month on month basis.

Q2 Review

Consistent with our previous report, demand for batteries was dire in Q2 due to the global lockdown. The availability of recycled material has been low during lockdown due to a lack of collection possibilities. This has caused prices to improve; E-bike battery scrap price increased in recent months from RMB7,425/t in March to RMB7,825/t as of June 24th. Prices for lead scrap recycled start-type battery ex-vat in China improved from RMB6,825/t to 7,275/t CNY June 24th. Battery demand has been weak, but we expect consumption to start improving in the coming months as orders pick up and facilities reopen. We continue to hear positive noises from China and the US; this has been represented in the uptick in LME prices.

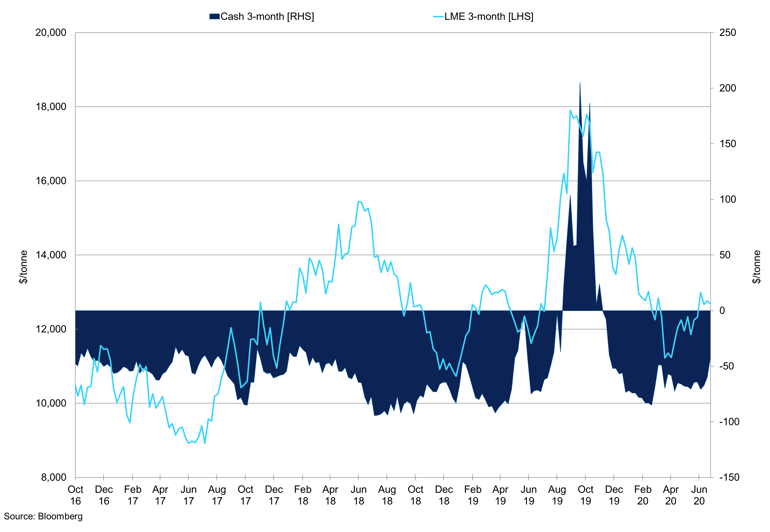

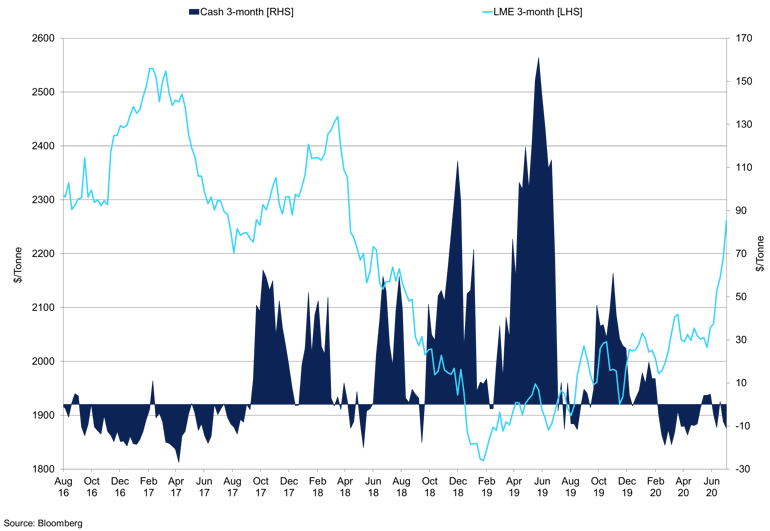

Cash to 3-month Spread vs LME 3-month Price

The cash to 3-month spread has tightened slightly but remains in contango despite the rally in a 3-month contract.

Outlook

Automobile production has been weak in recent months, understandably. Chinese production has started to recover, up from 195,000 units in February for passenger vehicles in China to 1.660m units in May. We would expect gains to be more gradual in the next couple of months, especially during the traditionally quieter period. The improvement in vehicle production in China suggests stronger demand for lead, and we have seen this play out in the physical market. With increased lead orders and growing demand from producers, we expect support for lead in the near term, especially given the shortage of scrap and refined lead in China. Commercial vehicle production has also recovered well, increasing from 89, 361 units in February to 527,219 units in May. The output of model type autos reached 2.187m units in May, up from 284,537 units. Sales have also rebounded relatively strongly; there may be a preference by citizens to use private cars over public transport due to the coronavirus. The accumulated output of cars in China was down a total of 29.7% y/y in May; however, May production was up 2% y/y in May.

German Mfg and Industrial Market

German auto orders have improved, but industrial and manufacturing orders are still negative, outlining the economic weakness.

German auto production has also declined, and in April y/y production was down 75.2%. The German car market employs over 1 million people, and this is a focal point for the German and European economy. Exports have tanked in recent months due to the lockdown and global pandemic. Since 2015 German car exports have averaged 331,000 cars per month, this year exports have averaged 180,000 units a month, and April saw exports of only 17,600 cars; in May this figure improved to 101,000 cars. Stimulus packages in Germany have been criticised by German automakers recently. Even with stimulus packages, cars are a luxury good, and while Chinese sales are recovering, we believe sales will be muted due to the loss of income as a result of the lockdowns and uncertainty surrounding future employment due to the recession.

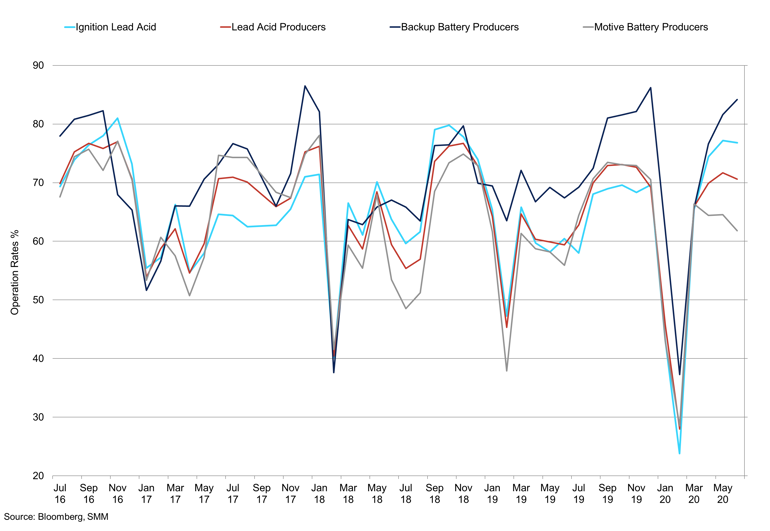

Mine suspensions due to COVID have starting to unwind, improving the availability of material. Most lead supply coming from secondary, e.g. in the US 80% of lead comes from secondary, compared with around 60% globally therefore even if mine supply improves we would need to see a recovery in secondary collections as well to confirm improving supply. According to the International Lead Association, the reduced processing at plants also tightened the lead market. Indeed, as orders improve this will increase tightness in the market. As smelters in China start to reopen, exemplified by the rising operation rates this will support primary and secondary supply, discounts for secondary lead are RMB150/t, and smelters discounts were deeper as flat prices rallied. Capacity for 2020 is higher on a year-on-year basis in China as both old and new capacity is available, however, due to the coronavirus and smelter shutdowns in Q1, production will be down on the year. The next couple of months remain uncertain due to the threat of another wave of the virus, but at the time of writing the virus is not reappearing in lead-producing provinces. Our base case is that output continues to recover for the remainder of the year; while the risk of capacity shutdowns is relatively high, we expect output to normalise with operation rates. Operation rates for ignition lead-acid batteries increased again in May to 77.16%, backup battery producers have recovered the strongest to 81.59% in May. Lead-acid battery producing operation rates are slightly behind the curve at 71.7%, but the improvement is still notable. We could see rates tail off slightly during the summer months as they are traditionally quiet.

China Battery Operation Rates

Lead-acid and backup battery producer operating rates have returned to normal levels.

Secondary smelter operation rates are low due to weak availability of battery scrap; rates averaged 50.4% up to June 24th. Some provinces' operation rates were lower than 50%, for example, Anhui Dahua. Maintenance at Guizhou and Jinglong has finished, and this could see production start to improve. Primary smelter operation rates were unchanged for the week to June 24th at 52.7%, according to SMM, Henan, Hunan and Yunnan provinces were at 62.9%, 38%, and 45% respectively. Imports of Chinese ore/concentrate have been weak in recent months, peak imports for 2020 were in February when the total was 9,617 tons compared to 4,692 tons in May. The cumulative total of imports so far in 2020 is 19,341.6 tons, incidentally the total number of imports for lead ore and concentrate for May 2019 on a tonnage basis was 20,132.3 tons. Last year did not have the supply chain problems we have had in 2020.

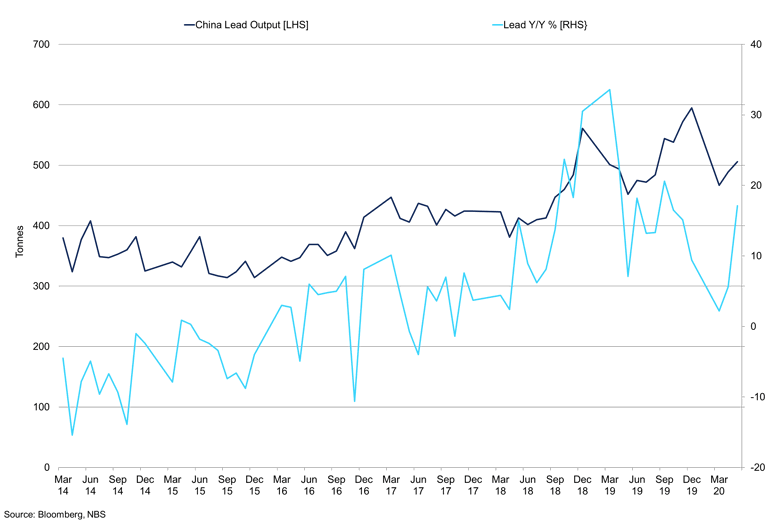

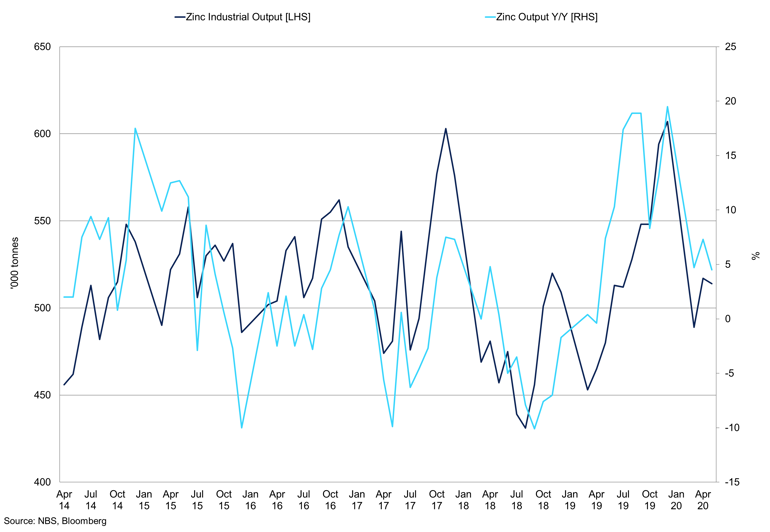

Chinese Lead Output vs Chinese Output Y/Y

Chinese lead production is trending higher, and Y/Y output has remained in growth just at a lower level.

Chinese lead production has started to recover, NBS data outlines that output for May was 506,000 tons; this was up 17.1% y/y. Chinese output has been improving in recent years; in Q4 2019 production averaged 568,000 tons compared to 500,000 tons in Q3 2019. We expect this to remain the case for the remainder of the year with output looking to return to the December 2019 highs at 595,000 tons. On a year-on-year basis, we have seen an output increase despite the coronavirus. Mine output for China has fallen from 2019 levels due to the coronavirus, South America seems to be the epicentre of the virus at the time of writing, and as miners attempt to contain the pandemic, we see mine supply falling in South America by 20%. We would anticipate this to reverse in 2021. The freezing of the secondary market and lack of new material as Chinese demand improved caused off-exchange inventories to fall significantly in China to 8,000 tons as of May 8th from 42,000 tons on February 21st. Since April we have seen stocks increase to 29,700 tons as of Wednesday June 24th, as smelter production increases but demand outside of China remains benign.

Nickel

Summary

Stainless steel demand and therefore nickel demand from the aerospace is likely to remain week in the near term. With production remaining elevated and demand weak, we may see inventories build, in turn suppressing prices. We anticipate exports of ni ore from the Philippines will rise again in May, after the 25% increase m/m to 1.68m tonnes, helping to alleviate some moderate tightness. Nickel ore inventories have started to rise at ports in China to 8.08m wmt as of Friday July 3rd, import losses caused bonded stocks to increase recently.

Review Q2

Nickel prices recovered in Q2 along with other risk assets as investors looked through poor economic data, towards a recovery in China and extensive stimulus from central banks and governments. Indeed, prices gained 11.89% in Q2 bring YTD losses to 5.94%. The rally in risk assets, led by US equity markets and copper indicate false optimism in the underlying economies. Cheap credit, retail flows and significant stimulus have supported assets. LME and SHFE inventories have diverged in 2020; SHFE deliverable stocks fell by 21.95% to 28,639 tonnes from February to July. Conversely, during the same period, LME inventories have increased 7.7% although this came in the month of February with stocks consolidating since. Prices in China have continued to edge higher in recent weeks with the #1 contract reaching RMB106,550/t as of July 7th.

LME 3-month Price vs Cash to 3-month Spread

Nickel prices rallied in Q2 but have failed to kick on despite the moderate tightening in the cash to 3-month spread.

Outlook

Stainless steel output has started to recover following the decline in production Q1, while it is worth noting that there is a seasonal fall due to Chinese New Year, it goes without saying that this year was more pronounced. We expect stainless production to continue to trend higher in Q3, despite recent maintenance cuts which were announced by small and medium mills. The maintenance is expected to take place during July due to weak profit margins. The omnipresent threat of weak stainless demand, especially during the summer period, will add to headwinds for the stainless market. Even though the maintenance will take place, we expect Chinese Ni stainless production push back to 2.2/2.3m tonnes in the coming months, if losses continue to worsen, we may see more maintenance from mills. Stainless production is coming off the back of a year where production increased 10% to 29.4m tonnes, according to Stainless Steel Forum. With maintenance taking place in small and medium mills, it is a chance for large producers to turn the screw by keeping output constant, giving rise to stainless inventories and capping gains.

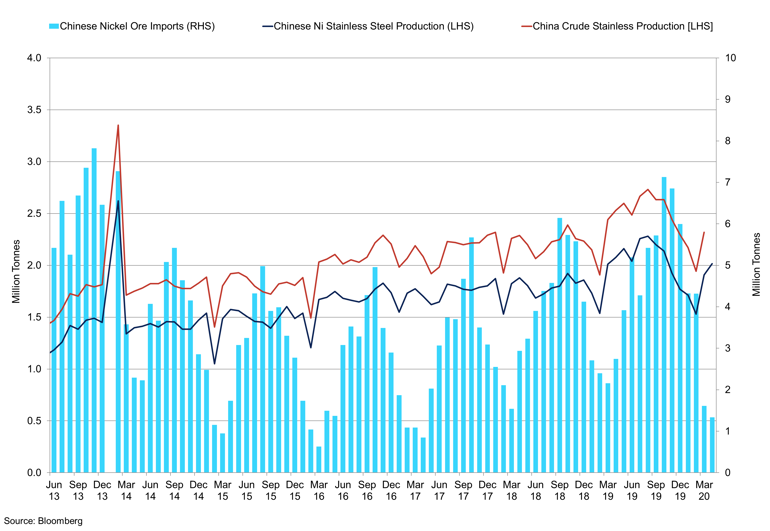

Chinese Nickel Ore Imports vs Stainless Steel Production

Stainless steel production has rebounded strongly, and this is expected to continue.

Stainless production is expected to trend higher, but we expect demand to remain weak, another area of weak demand for nickel is aerospace. The aerospace sector has been one of the worst-hit by COVID-19, exerting downward pressure on demand for stainless. Aerospace powerhouses such as Boeing, Airbus, and Rolls Royce are losing orders and jobs after travel ground to a halt. Even though tourists can travel, it is at significantly reduced capacity and prices which will not improve profits. Airbus is expecting to cut 15,000 jobs, to cut costs after revenues ground to a halt; the company have suggested they will cut 11% of their workforce, the company have not received an order for an aircraft for three months, with total net orders at 298 for 2020. They are also reviewing one of its production factories in North Wales; the company has three plants at its Boughton facility which predominately produce plane wings. Avalon has cancelled orders for 27 Boeing 737 Max aircraft, just after they settled most of the Lion Air 737 crash claims. We do not expect orders for new aircraft to increase anytime soon, and with some airlines going bust we could see companies purchase these older planes with some even going to scrap.

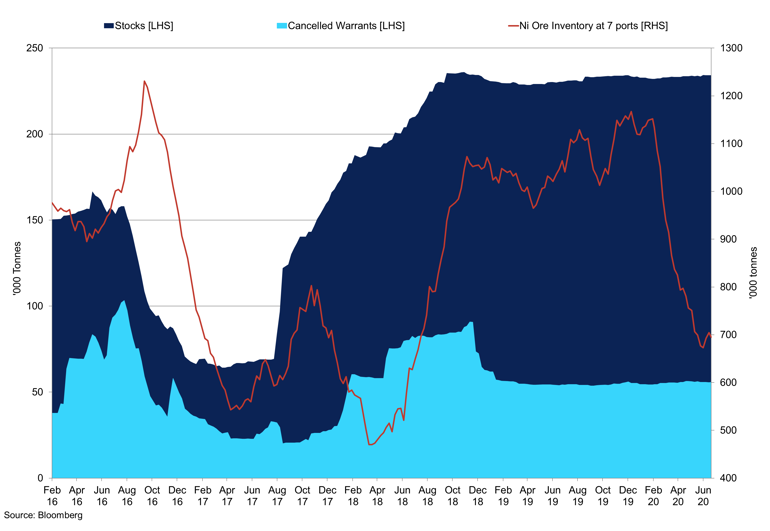

LME Nickel Inventory s vs Ni Ore Inventory at 7 Major Ports China

Nickel inventories at 7 of the top Chinese ports fell sharply as the supply chain faltered.

Chinese nickel pig iron mills are increasing their operating rates, according to SMM. July's operating rate is forecast to be 68.2%, an improvement in the last month. This could see nickel pig iron production increase once again on a month on month basis in China, NPI output increased 0.81% in June to 44,600 tonnes and was 9.85% lower y/y. High-grade NPI production was higher on the month at 37,500 tonnes; we anticipate production to edge higher in July. However, it is Indonesia that is increasing nickel at a rapid pace. The decision to ban nickel exports has led to an increase in exports for ferronickel. This is expected to increase further in the coming years as potentially more than 10 RKEF lines that are under construction now will be operational by year-end, with 12 more planned. This will not impact Q3, but it is the outlook for things to come and gives context to the speed at which Indonesia is ramping up production. We expect this rate to continue. Having said that, the nickel output for 2020 is expected to decline due to the ore export ban from Indonesia by 2.9% to 2.28m tons according to Wood Mackenzie. Refined nickel output is expected to increase to 2.46m tons in 2020 due to the expansions in Indonesia. According to SMM, two new production lines of Ferronickel in Weda Bay Industrial Park started in June, and the lines are able to produce 800 tonnes per month. The lines are phase 1 of a project by Zhenshi Group and Tsinghan; the four lines will have an annual output of 35,000 tonnes.

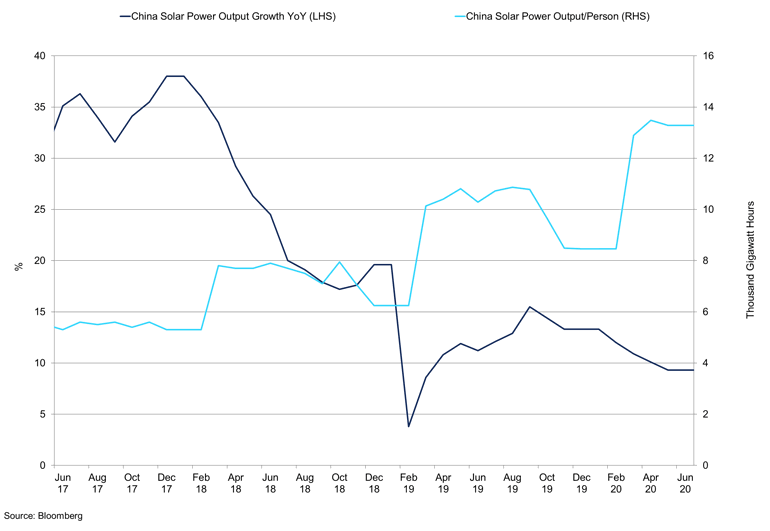

China EV Sales vs Production

EV sales and production in China have rebounded strongly with the help of new government policy.

EV sales have suffered due to the coronavirus, the loss of earnings due to redundancies or the increase in savings ratios across major economies suggests an unwillingness to purchase big-ticket items such as autos and therefore EVs. As uncertainty subsides, we expect to see EV sales improve on a month on month basis once again. This is exemplified by May EV sales in China, sales recorded the best month this year with PEV sales representing 4.4% of market share, total auto sales were positive for the month for the first time in 2020, this continued in June when sales reached 1.68m units up 6.5% y/y. However, NEVs were down 38.7% YTD in May and 23.5% y/y again, on a month on month basis were stronger at 12.2%. PHEV sales were significantly stronger on a y/y basis according to China's association of automobile manufacturers, with sales up 664% y/y in May but remained down YTD by -19.4%. In June, NEVs fell 35% y/y to 85,600 units, but battery EVs sales were 67,000 down 40% y/y. Tesla is gaining momentum in China; they made up 23% of EV sales in China in June, selling 14,954 Model 3 cars. Even though Tesla recently signed a deal with Glencore to supply cobalt for their 8:1:1 battery, they also recently got approval to build the Model 3 with lithium-ion phosphate (LFP) batteries. This, in conjunction with CATL moving towards LFP, could indicate some softness to the nickel content in batteries. It is worth noting that there are lots of different battery technologies in development; most have nickel in order to improve energy density.

Tin

Summary

Mine supply has struggled since Myanmar was disrupted. Imports of refined material and ore & concentrate have been strong, and this is expected to continue given the strong SHFE prices. Semiconductor sales have been strong so far in 2020, and we believe sales will continue to be strong for the remainder of 2020, with potential support in the U.S. from government bills. Smartphone sales are showing signs of recovery as well, but the uncertainty surrounding employment in the long run, and the ending to COVID unemployment support schemes may act as a headwind.

Q2 Review

Tin prices recovered well in Q2, gaining 16% and closing H1 2020 down 2.6% YTD at $16,690/t. The recovery from the low was 31.4%, and this exemplifies the improvement of risk appetite as economies boosted prices as funds flowed into the metals complex. SHFE prices gained 15.2% in China in Q2 and closed H1 2020 at 138,080 tonnes. Solder demand suffered as a result of the pandemic in H1 2020, impacting tin consumption. However, China’s recovery is ahead of the ROW, and this could support solder demand in the near term through demand for electronics, and semiconductors. Like other consumer goods, the lack of earnings due to high unemployment levels could provide headwinds to demand. Indeed, until there is more certainty surrounding employment and earnings, mobile and PC sales, for example, may struggle.

LME & SHFE Stocks

LME stocks have started to increase in recent weeks, but SHFE inventories have been falling since March.

Tin was supported by mine suspensions as countries tried to contain the virus. The tightness of supply was already an issue, and the reduced availability of concentrate compounded the issue. LME inventories declined 41.9% to 3,605 tonnes, the low was 2,425 tonnes at the beginning of June, but we saw some inflows last month. These have continued in recent weeks, but most inventory remains on warrant at the time of writing.

Outlook

The PHLX Semiconductor Index surged higher since our last report, gaining nearly 40% in Q2, and 71% from the YTD low as of July 13th. The index is making record highs once again, as retail flows and extremely accommodative monetary policy from central banks helping indices. This sets to continue in the near term as risk appetite has returned; however, there remain strong questions over the demand for semiconductors due to COVID-19. Technology firms have been well supported in recent months with many money managers suggesting a speculative bubble when you look at the underlying economics of the global economy. The current P.E ratio increased from 23 at that time of our last report to 29.19 as of July 13th, just off the 2016 level of 29.57. Gross margins per share is 52.54%, as the estimate for the return on assets for 2020 is 14.78% and return on common equity is forecast to be 24.45%, both below 2018 levels.

Despite the suggested weakness in the semiconductor and chip space, we saw some strong demand for Samsung chips in Q2. Samsung electronics beat Q2 forecasts despite the pandemic as consumption for server chips from data centres remained elevated as companies shifted to working from home and needed more server and storage space. Samsung sales were 51.6trn won for Q2 with an operating income of 6.8trn won. We expect a more granular breakdown of performance data in the near term, but there are early indications that demand for smartphones was recovering in June. A recovery in smartphone demand in Q3 would help demand for solder and therefore tin; however, Samsung’s chip business may not see same strength in Q3 as companies who purchased additional server capacity, or memory will not need to do so again.

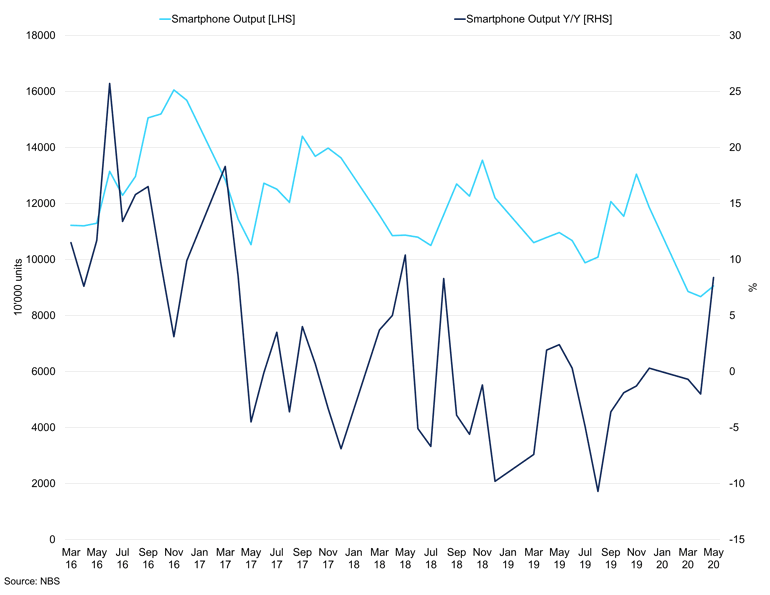

Chinese Smartphone Output

Chinese smartphone output has started to increase; 5G networks may buoy sales.

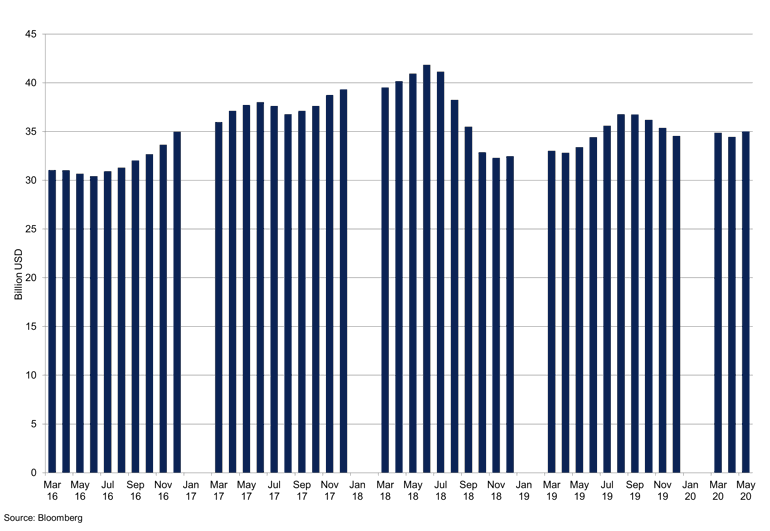

Semiconductor sales across the world recovered in 2020 and have shown resilience to the pandemic. According to The Semiconductor Industry Association (SIA), sales in May were $35bn up 5.8% y/y and 1.5% m/m which totalled $34.4bn. Uncertainty remains but sales figures from across major regions of China, Japan, and the Americas increased by 5.8%, 2.8%, and 1.9% respectively on a month-on-month basis. European sales were lacklustre, declining 6.5% m/m; however, the y/y figures are generally stronger with the Americas increasing 25.5%., China up 4.9% but once again Europe was a weak spot with sales declining 12.9% y/y. The World Semiconductor Trade Statistics estimate that the semiconductor sales are expected to increase 3.3%y/y in 2020 to $426bn, with the market expected to improve a further 6.2%. Integrated circuits are forecast to grow 5.3% in 2020, and as mentioned above, memory chips are forecast to rise 15% in 2020. Chinese output of optoelectronics is down 25.2% y/y in May according to NBS, outlining the weakness in the market this year.

Global Semiconductor Sales

Semiconductor sales are improving; China, Japan, and the Americas lead the way with Europe lagging behind.

The U.S. Congress is looking to pass two bills which will support semiconductors, the first of which is Creating Helpful Incentives to Produce Semiconductors (CHIPS) for America Act. This bill would create 40% investment credit to 2024, reducing to 30% in 2025, and 20% in 2026 before being completely phased out in 2027. A $10bn programme would also be introduced to incentivise companies to increase lab building and R&D. Secondly, the American Founders Act 2020 will aid semiconductor manufacturing with grants for companies. There is a maximum grant of $3bn per state, and there is another aspect of the act which will mean grants are put towards funding production facilities.

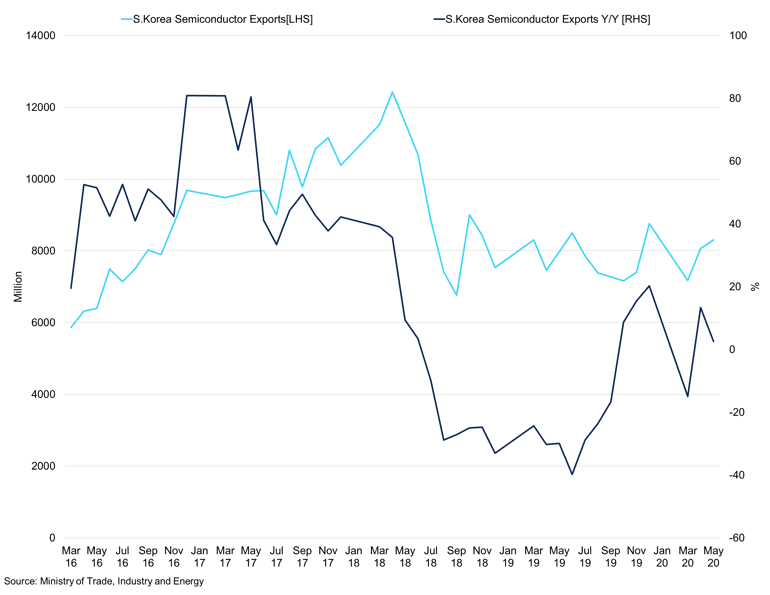

S.Korea Semiconductor Exports

Exports have stuttered in recent months due to COVID but are starting to improve once again.

Chinese customs data shows a huge surge in refined tin imports in May 2020 of 1,762% from May 2019, importing 3,674 tonnes. Most of the imports came from Indonesia and then Bolivia Exports totalled 503 tonnes suggesting that Chinese disappearance was 3,171 tonnes. YTD imports of refined tin through to the end of May reached 7,697 tonnes y/y with exports at 1,935 tonnes; China has become a net importer since September. From a raw material perspective, imports of ore and concentrate in May were 14,875 tonnes (gross weight). According to the International Tin Association, the estimated tin content these imports was 3,100 tonnes up 19% m/m and 24% y/y. Border controls continue, and mine supply may be restricted in the immediate term due to lack of workers, Myanmar’s lockdown was extended for mass gatherings once again to July 31st. Refined tin output reached 12,490 tonnes in June according to SMM, an increase in 6.5% in May.

Mine supply has been impacted to COVID, and this will start to improve as lockdown restrictions ease. However, despite the recent strong Myanmar exports of ore and concentrate in May, there has been a longer-term trend of less availability. Key producers are reducing their targets for 2020 with PT Timah reducing their target to 55,000 tonnes. PT Timah invested in $80m worth of construction equipment in West Bangka, but as of the beginning of July, the contractors were not able to enter Bangka. Alphamin and their Bisie mine have indicated that Q2 production reached record levels, concentrate production reaching 2,739 tonnes up 29% q/q, and grades were high. Full-year targets for Alphamin were 9-10,000 tonnes of tin concentrate. The tin grade extracted so far this year has been 3.9%, with an average recovery rate of 69.9%.

Zinc

Summary

Zinc off-exchange stocks 201,000 tonnes down from 294,000 tonnes, but according to NBS data, Chinese Zinc production has picked up again. With the demand outlook softer for zinc than other metals, we could see inventories increase in Q3. TCs have stabilised, and as mine suspensions come back online and availability improves, we expect TCs to recover. The cash to 3month spread remains rangebound, exemplifying the softer demand outlook. With refined production in China good as well as a softer ROW consumption outlook, and the potential of rising inventories, we expect the spread to remain on contango unless we see another wave of mine suspensions.

Q2 Review

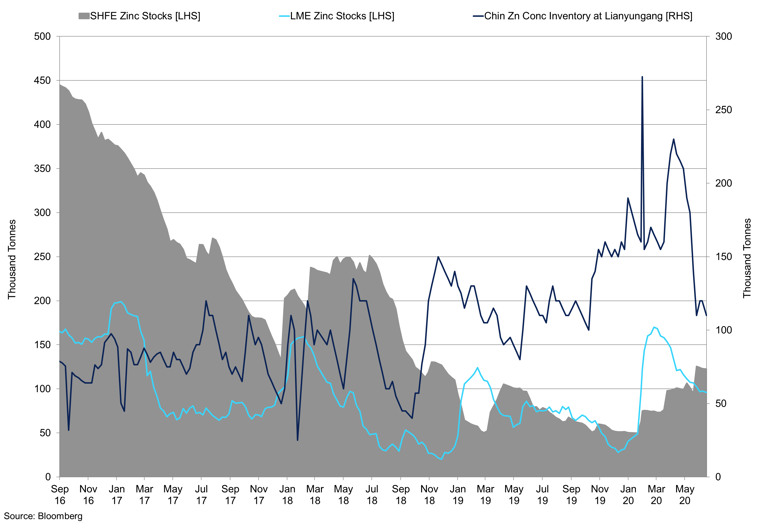

LME prices recovered somewhat in Q2 as optimism surrounding the relaxing of lockdown restrictions started in China, then spread to the US and Europe as we went through Q2. While economic data is still weak on a historical and y/y basis, m/m data is starting to improve. We expect economic data to remain weak in the near term, and recent data in the US has added confusion to the situation. Consumer demand remains weak, and the threat of a second wave in the US will add to the recent headwinds. LME prices gained 7.76% in Q2, but YTD prices are still down 10.06%. LME inventories have climbed as demand remains weak across the globe, YTD gains are up 139.2%, and QTD is 67.56% as material flows into warehouses, but SHFE stocks have declined 38.94%. The import arbitrage for spot and down the curve is offside; Zinc spot import arbitrage is RMB453.18/t with the SHFE/LME ratio at 8.23 as of July 2nd.

Zinc 3-month Price vs Cash-3-month Spread

The cash to 3-month spread has remained rangebound despite the 3-month contract gaining ground.

Outlook

The weakness in zinc consumption has been palpable in H1 2020, and while we have seen some positivity return to the base metals complex in the Q2, zinc gains have been slightly more muted. Chinese manufacturing PMIs suggest that recovery has been strong, and the sequential reading shows Caixin PMI expansion in the sector in recent months, with readings of 50.7 and 51.2 in May and June, respectively. Export orders remain weak and are contractionary at 42.6 in June, the weakest of all indices, stocks of finished goods were at 46.8. The output PMI was 25%, we expect the growth to continue exemplified by the improvement and return to y/y growth for industrial production, which was 4.4% in May, up from 3.9% in April. Outside of China remains weak, and in Europe, lockdowns have been managed with a firmer hand than the US., and while data from America is improving, and investors are looking through the weakness and rising cases in recent weeks. A second wave will threaten the recovery and will likely cause the economy to run at a lower capacity for longer. We envisage the themes for H2 2020 to be how much demand can offset the losses in H1 2020; how will economies prevent the threat of a second wave?

Zinc Operation Rates