Summary

Economic data growth has started to plateau as new COVID-19 restrictions have been put in place across Europe and in the U.S. Chinese economic data has improved but exports remains weak, limiting the upside for base metals. The U.S. election presents some downside risk, but this will be limited due to expansive stimulus measures at this time. While fundamentals for some metals are weak, we expect the basket to maintain its strength, with Chinese activity the focus. End-user consumption is expected to remain weak as unemployment levels are high and stimulus packages are reduced.

Aluminium

Aluminium prices were supported this quarter, as consumption outlook improved on the back of easing lockdown restrictions. However, as coronavirus cases continue to rise and we await the news around the vaccine, the sentiment should remain volatile. The strong rally in prices will keep production of primary aluminium strong, with most of the improvement coming from China, as the rest of the world struggles to catch up. From the demand side, consumption is to remain muted, and may prompt a rise in Chinese inventories. Range: $1,730-1,980/t

Copper

Copper prices improved in Q3, as demand optimism improved due to easing of lockdown restrictions, with prices peaking above $6,800/t. The value of exported products has been improving this year, and this is expected to remain the case despite the downside risks to prices from COVID-19, geopolitical tensions, and risk to the dollar. Stimulus measures remain strong, and this should continue to support consumption of copper. Headwinds, such as the US election prevail, but we believe that copper prices will prevail despite of the outcome. Range: $6,300 – 7,200/t

Lead

Lead prices were well supported in the first half of the quarter, testing $2,000/t, as auto demand recovered. While we expect this to remain the case in the near term, rising cases in Europe could present some downside to vehicle consumption. In terms of battery demand, low interest rates should keep financing conditions accommodative, providing support for purchases, and collection rates to improve as well. Supply is to remain strong and this should increase the availability of material. Range: $1,650 – 1,980/t

Nickel

Nickel prices performed well in Q3, as manufacturing and industrial production started to improve. However, data slowed as cases started to rise and restrictions were put back in place. Nickel supply for 2020 is expected to be lower this year due to the Indonesia ore export ban. Indeed, due to the reduction in nickel iron ore imports, we expect China’s NPI output to be limited, meaning the trend of higher ferronickel imports is expected to continue. Long-term demand is to remain soft and until there is a vaccine, orders for planes will remain subdued. Range: $14,000 – 17,200/t

Tin

Tin prices appreciated in Q3, but gains were less pronounced as economic data normalised. On a global scale, semiconductor sales have remained strong in recent months and we expect this strength to be carried into Q4, which will boost solder demand and, therefore, tin demand. Despite exchange inventories being relatively high, we could see imports for refined tin and ore increase as consumption improves due to the strength of the consumer electronic goods sector. Ultimately, the outlook for tin remains support with prices pushing higher to $15,600 – 19,000/t.

Zinc

Zinc prices were well supported in the first half of Q3, however, declined later in the quarter. We expect appetite for zinc to improve following the correction to the downside. Supply is likely to improve, and we expect output in H2 2020 to offset the losses in H1. However, the export market remains weak and the second wave will mean a delay to stronger demand. We see some downside to the USD in the near term, which could provide support to Zinc, pushing prices up to $2,200 – 2,700/t.

Iron Ore & Steel

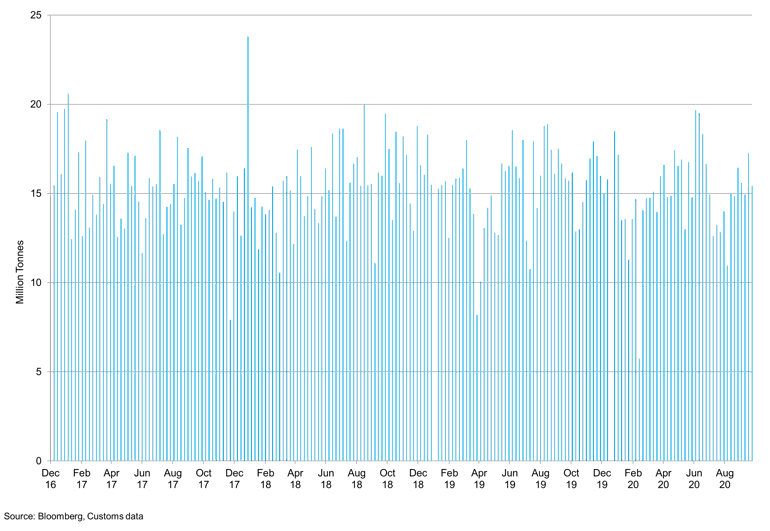

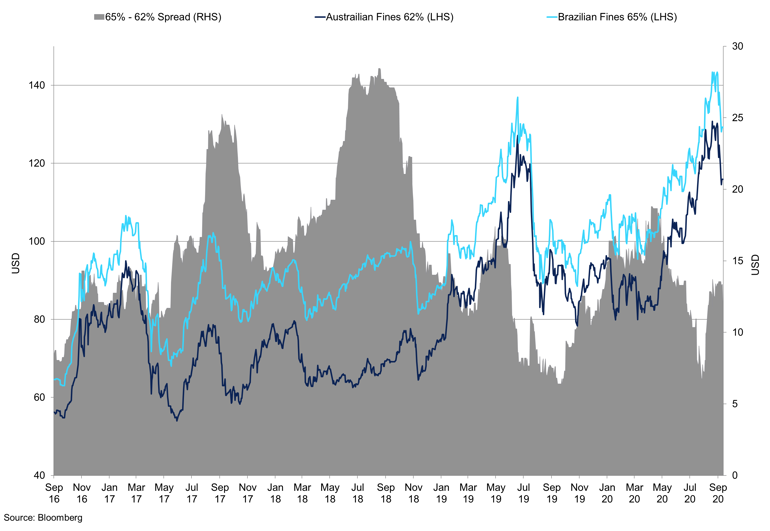

Strong iron ore demand and reduced seaborne supply prompted prices to test resistance at $130/t in Q3. Cases in Brazil have stabilised, but the threat of a second wave is still very prominent. Availability is improving, and this is likely to continue in the near term. We do not expect Australian exports to China to decline exponentially, but as tensions remain thwarted, China may look to higher quality fines from Brazil. We expect prices to trend lower in the coming quarters, but we know that demand from China is strong, and we believe prices will edge down to $80/t.

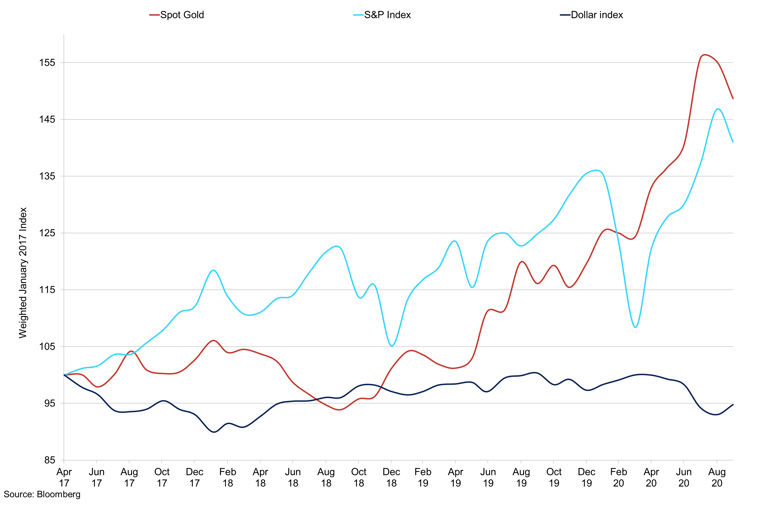

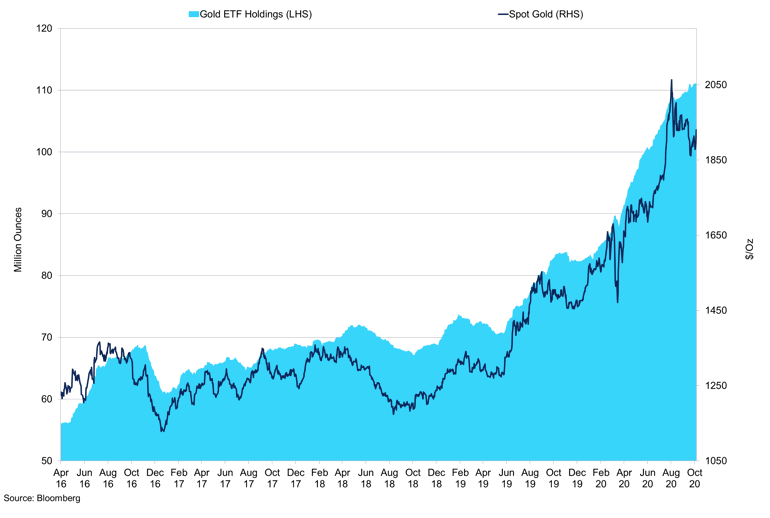

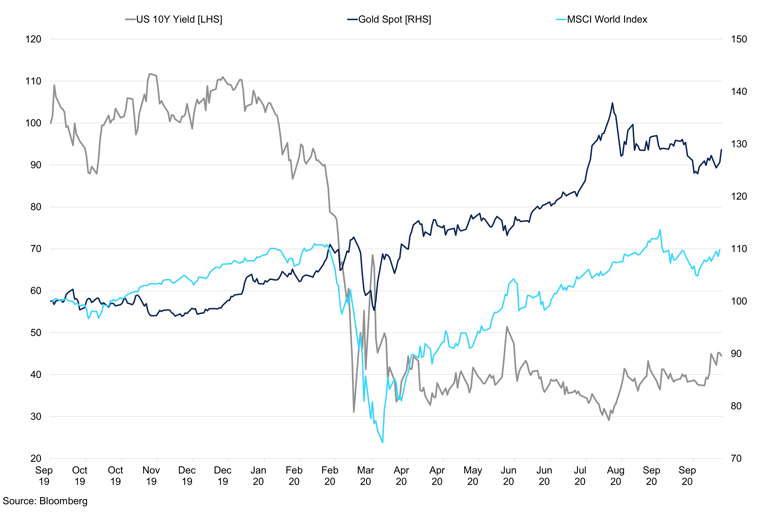

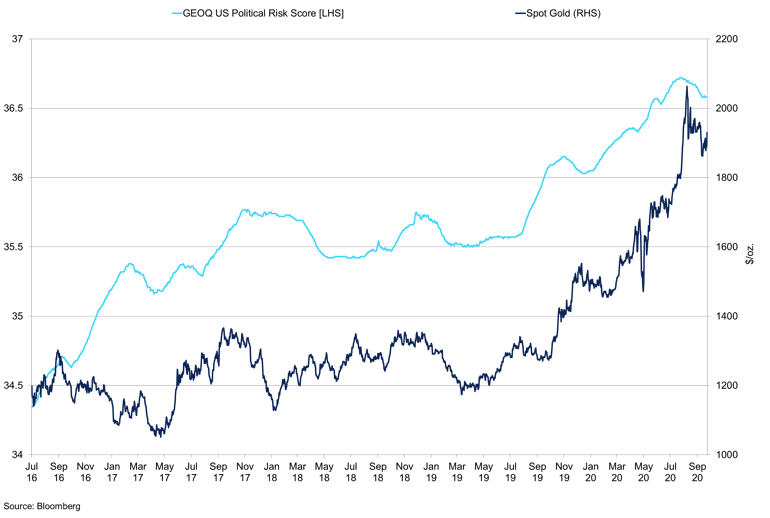

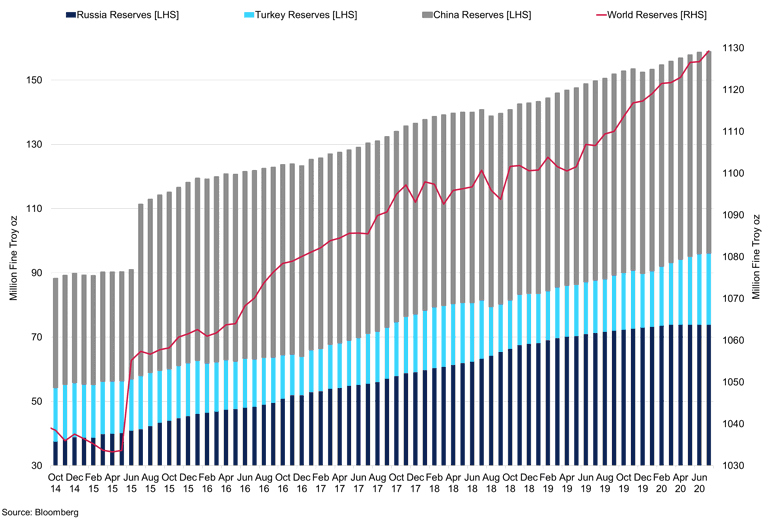

Gold

Investment appetite for gold has reached record highs as investors urged to safe havens to hedge from risks posed by the spread of coronavirus and continued global uncertainty supported gold as a safe haven asset. Additionally, while the news surrounding the release of the vaccine encouraged risk-on sentiment in the stock market, the yellow metal remained resilient, highlighting its strength during the crisis. Ultimately, the combination of high volatility, low opportunity cost and strong investment demand will support gold investment and offset weakness in physical consumption. Range: $1,800 - 2,200/oz

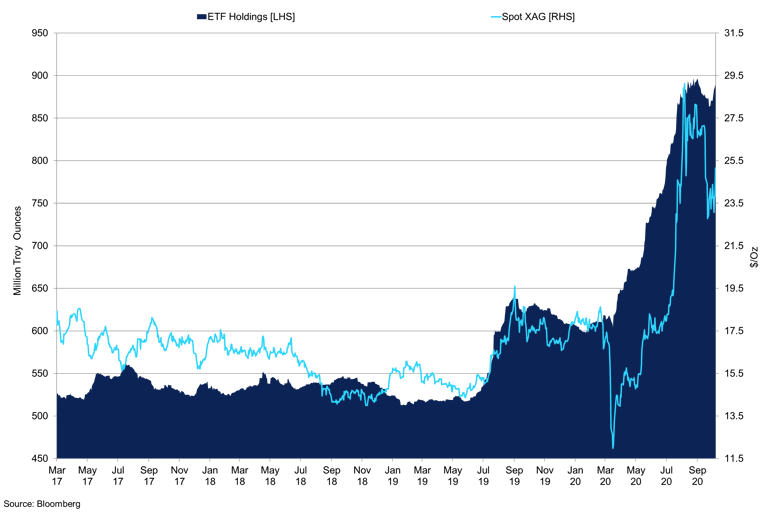

Silver

Increased speculative demand supported the precious metal in Q3, supporting its rally to $30/oz this quarter. Global ETF inflows saw another round of expansion, reaching record highs of 8.907moz in August. Silver is poised for another quarter of growth, yet, slower to the one seen in Q3. In Q4, as repeated lockdown measures threaten industrial demand, silver is likely to hold on to its safe haven properties. Ultimately, we do not foresee sustained dollar strength in Q4, especially as the next stimulus bill is in the talks, and the upcoming US elections could throw in some uncertainty into the US outlook, supporting the outlook for silver. Range: $23 – 33/oz

Palladium

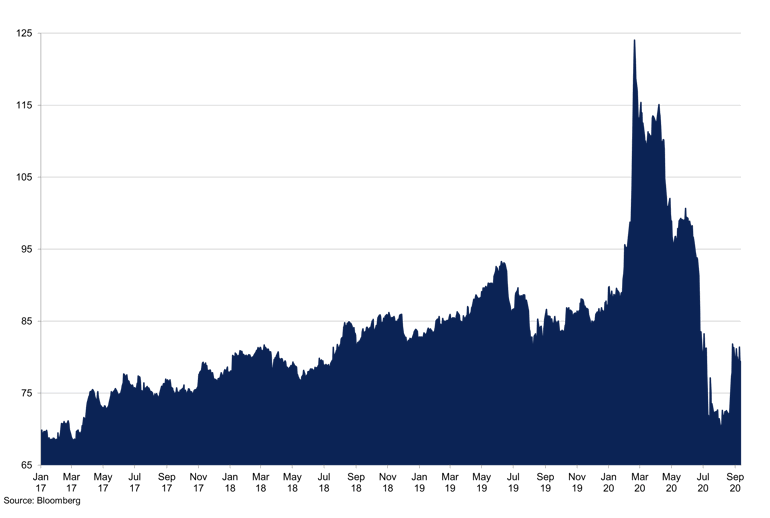

In Q3, palladium prices picked up higher to the resistance level of $2,400/oz, on trend to come back to record highs, as a rebound in Chinese car sales helped fuel demand for petrol autocatalysts. Indeed, the global ETF holdings picked to the highs last seen in March 2020, further widening the gap between platinum and palladium investor demand. The coronavirus crisis looks to weigh on the US economy heading into Q4, and while car sales are expected to grow month-on-month, demand remains low relative to 2019. As fundamentals remain weak and industrial demand to remain dormant, investor demand might support prices further into Q4. Range: $2,050 – 2,600/oz

Platinum

Industrial demand for platinum is likely to remain moderate in Q4, as the metal could continue suffering from the pressures of the second wave of coronavirus infections. The price of platinum, however, lagged palladium as diesel-engine catalytic converters lost ground to petrol-powered vehicles during the pandemic. Ultimately, lower-than-expected mining output should outpace softer demand, and, subsequently, support platinum prices higher in Q4. Range: $800 – 1,050/oz

Market Overview

Global Outlook

Markets rallied sharply from their virus lows, driven by continued policy support as well as the economic re-emergence from one of the deepest recessions in the last century. At the same time, activity restarts took place; however, the rate of recovery has not been uniform globally, driven by differences in containment measures. While new daily global cases continue to beat record highs, the number of daily deaths is lower than during the first wave, which might explain the market’s muted market response. The speed of vaccine development has surprised to the upside; however, even the most optimistic forecast is for the release to take place in 2021. The global sentiment has shifted once more – from increasing pressures to reopen to the reintroduction of lockdown measures to prevent the spread of the disease, and so we would expect the economic recovery to be gradual.

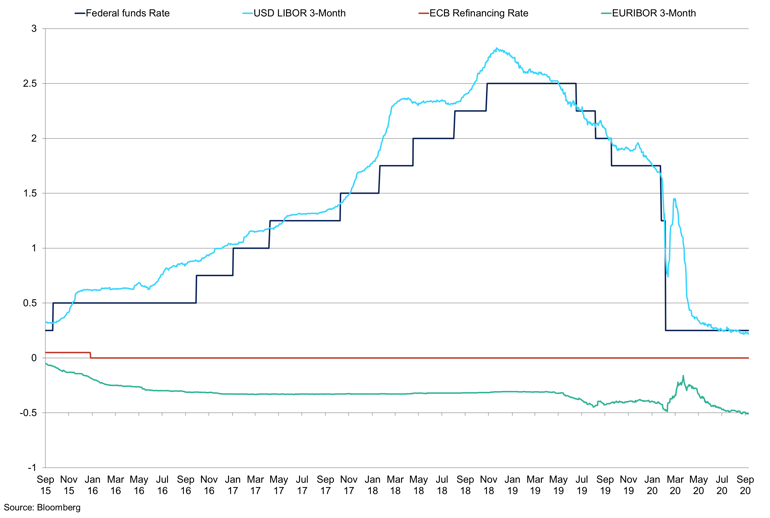

Western Economies Interest Rates

Global interest rates are to remain lower for longer.

In Q3, we saw a surprising behaviour in equity prices. Indeed, the S&P 500 is up 52% since bottoming in March, and is at pre-crisis levels. One explanation is investors' overestimation of economic contraction earlier in the year, reflected in price retraction. However, once it became clear there is a path to recovery, prices came back to normal levels. Record monetary injections by the central banks, along with low-interest rates, led to a surge of the money supply. Among the major advanced economies, the US saw the largest increase of 28.4% m/m in money supply in August. With less money being spent on goods and services, investors were seeking better returns, found in equities. Looking at current price levels, it seems that equity markets are exhibiting valuations typically seen after years of strong returns. Indeed, the pandemic-driven decline in the US bonds yields has pushed equities to the forefront of market focus. The price-to-earnings ratio is now at the highest level since the dot com bubble early in this century.

The global outlook remains supportive relative to the lows seen in Q2; however, we would expect to see increased volatility around the US elections. Indeed, if the risks surrounding the upcoming presidential elections in November prevail, this will create uncertainty around tax changes, government regulations and the trade relations with China. If the COVID-19 related uncertainty persists, we would expect the drag on global growth to limit the extent of the dollar decline, as its safe-haven status could shine once more. Additionally, if the recovery in the US continues, it would be hard for the US dollar to drift further down. On the flip side, the speed with which the vaccines arrive should also influence how fast the dollar falls from current levels.

Oil futures fell marginally under new pressures in Q3 on concerns that the demand might take much longer to bounce back. Indeed, while consumption did not recover to pre-pandemic levels, the combination of partial demand recovery and supply-side cuts supported the prices in August. Ultimately, in the absence of demand improvement in the upcoming quarter, we are likely to see more downward pressures as global oil prices continue to reflect the changes in demand.

In September, Brent crude prices averaged $41/bl; while up from $29/bl in June, still down $4/bl m/m. Indeed, in comparison to the May-July period that saw an increase of 4.1m bpd in consumption, consumption was only up by 1.0m bpd in the August-September period, highlighting the diminishing global demand in Q3. Even though inventory draws are expected in the coming months, EIA forecasts that high inventory levels and surplus crude oil production could cap growth in oil prices.

From the supply side, OPEC and Russia are currently withholding 7.7m bpd of combined crude oil production from the market in hopes of rebalancing supply to already-low demand. While OPEC has pressed for further compliance towards supply cuts, some producers, such as UAE, Iraq and Nigeria have already overproduced, threatening the legitimacy of supply cut promises.

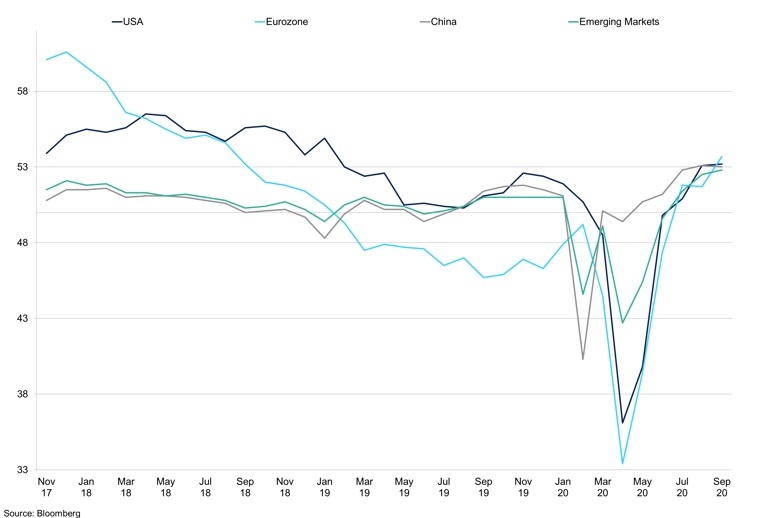

Manufacturing PMIs

Manufacturing activity is at pre-pandemic levels; however, month-on-month growth remains slow.

Unlike the service sectors, manufacturing in Europe continued to improve, with September PMI figures increasing to 53.7 from 51.7 in August. The September figure is the strongest level in two years, indicating the strength of global demand growth for eurozone exports as well as internal demand for durable goods. Indeed, rising levels of exports supported new orders and output, and operating conditions have now been improving for three months in a row.

In the US, manufacturing activity has also been trending higher, with the latest September Markit PMI index at 53.3, up from 52.7 in August. The data indicated the sharpest improvement in operating conditions across the sector since early 2019, supported by a faster expansion of production and new orders. As a result, firms continued to hire following further upward pressure on capacity. The outlook deteriorated, as companies grew more concerned about the repeated local lockdown measures and uncertainty caused by the upcoming presidential election.

China's manufacturing economy retained strong growth momentum in September, with firms signalling further increases in production and new work. The month-on-month growth, however, has slowed down, declining down from 53.1 in August to 53.0 in September. Nevertheless, new business expanded at the strongest rate since January 2011, supported by a strong rebound in exports.

US

In Q3, we expect to see a rebound in growth, especially after the economy has fallen by a record 31.4% annualised q/q in Q2, mostly led by a recovery across the states. For the last quarter of the year, headwinds prevail, as localised outbreaks and a delay in the next relief act by the Congress poses further threats to recovery. Indeed, if an agreement is not reached, 4% of GDP will be lost through a decline in consumer income. We assume that a drop in unemployment insurance payments will continue to impact consumer spending. Despite the US election becoming the spotlight of the upcoming quarter, the next round of stimulus is likely to arrive this year, with Pelosi set to achieve a deal in November.

As we set on a path of moderate economic recovery, the US dollar could weaken given its counter-cyclical behaviour. However, we expect that COVID-19 uncertainty will prevail through Q4, which will be the beneficiary of greenback performance as we have seen flows into the dollar following global uncertainty. Moreover, if the recovery in the US accelerates, it would be hard for the US dollar to drift further down.

Although the impact of the coronavirus on the US economy has been profound, the result of the upcoming presidential election in November is likely to have a significant effect on the global economy in the upcoming quarter. Trump's 4-year long term has led to restricted trade and immigration, enhanced domestic agenda and departure from major alliances and treaties. Biden, on the other hand, has differing opinions, looking to be more open in trade, immigration and cross-border investment. While policies of Biden vs Trump will differ significantly, both are likely to be big spenders. Indeed, we believe that both candidates are likely to enact policy that will have a positive economic impact to revive the economy from the COVID-19 crisis.

At the time of writing, the Economist forecasts that, with a 92% chance, Joe Biden will win the electoral college and, with a 99% chance, he will win most votes. Indeed, it is crucial for a candidate to achieve most electoral college votes to not to repeat the outcome of the 2016 election, where Clinton received more votes than Trump did, but Trump received the majority in the electoral college. With the BBC forecast more moderate, the national polls still favour Biden at 52% win. At the time of writing, Florida, a key state for Trump's win, is leaning towards Biden. Indeed, we believe that President Trump's recent COVID-19 diagnosis has added further uncertainty to the outcome of the election.

Despite Biden's consistent lead, headwinds to his win remain, including the Republicans' advantage in the electoral college and the significant lag in the processing of the mail-in ballots. Despite the continued uncertainty, we believe that the most likely scenario is the US ends up with a divided government, which could imply a Biden administration with a Democratic House and Republican Senate. This scenario would lead to a continuation of political gridlock that would prevent major legislative programmes. Another scenario would be that the Democratic sweep of the House and the Senate. This could significantly push the Biden's infrastructure and green policy packages on top of additional stimulus measures towards the pandemic.

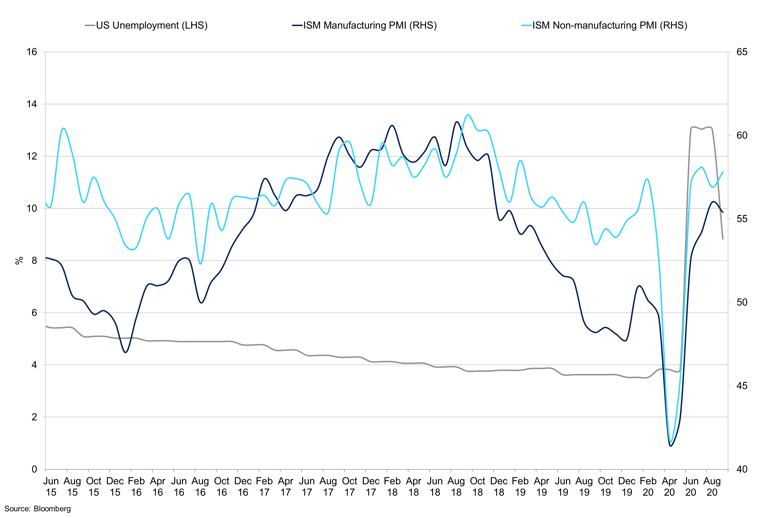

In September, the labour market slowed considerably, with the number of new jobs created at the lowest level since April. Overall employment remained far below the level seen in 2019, and the unemployment level fell to 8.83% in Q3, past its peak of 13.03%, as fewer people were seeking and finding work. Still, we saw that personal income fell sharply, down 2.7% m/m in August, due to the expiration of government transfer payments, which were down 14.8% m/m. Spending, however, decelerated only modestly even as households significantly reduced the use of savings. While the next stimulus bill is still in the talks, we would expect to see more fiscal support before the end of the year. In the meantime, we would expect spending to weaken ahead of a surge of employment.

US Unemployment vs Manufacturing vs non-Manufacturing PMIs

With unemployment levels still elevated, both manufacturing and non-manufacturing sectors remain under threat.

Europe

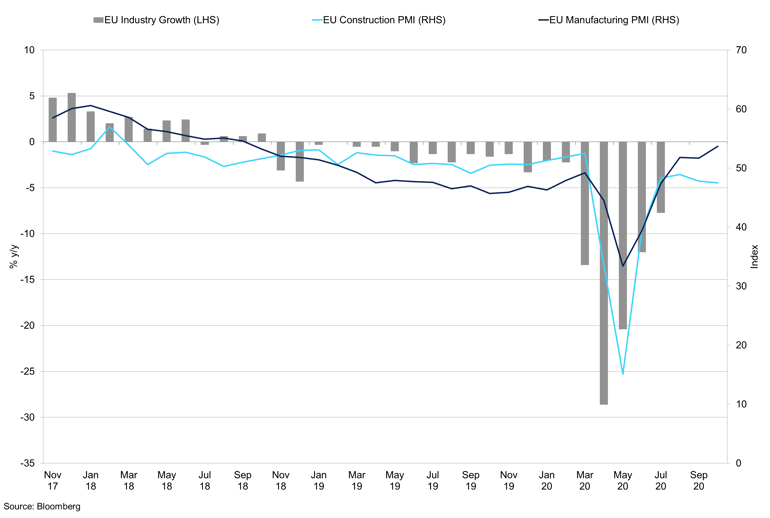

Economic indicators have rebounded through Q3 2020, thanks to the partial relaxation of lockdown restrictions. Infections have been rising, but death rates remain low due to the shift of infections towards a younger age group and, subsequently, more effective treatments. The Euro area's GDP fell 12.1% q/q in Q2, well below of that seen in the US and the UK. Europe's disadvantage heading into the pandemic has been the lack of monetary policy ammunition; interest rates were already negative and many countries, such as Germany, had strict fiscal deficit limits. This crisis, however, has urged the bloc to act immediately, and Europe has released the €1.6tr planned stimulus support and kept the pandemic emergency bond-buying programme running through mid-2021.

EU Industry Growth, Manufacturing and Construction PMIs

EU construction and manufacturing PMIs remain relatively unchanged, signalling stagnant growth.

Although the size of economic contraction in Europe may be smaller this time around, activity is clearly slipping in the most affected areas. While there has been a resurgence in infectious rates, the high-frequency economic data suggests a pause in the recovery rather than a decline, but economic conditions could deteriorate further should the number of cases continue climbing. One of the examples of the slowdown is the services PMI, which declined from 50.5 in August to 47.6 in September, indicating that activity contracted.

Q3 is projected to increase by 8.4%; thereafter, the rate of growth given the partial success in containing the virus. Continued measures, together with elevated uncertainty and worsening labour conditions, are expected to weigh on demand in Q4. Nevertheless, substantial support from monetary, fiscal and labour market policies should help support incomes and limit the implications of the effect of coronavirus. For 2020, the GDP in the euro area is projected to fall by 8.0%.

Fiscal stimulus has supported household consumption, mostly through furlough schemes, but weak labour markets are likely contributing to the low level of consumer confidence. In August, personal and business savings have increased, suppressing demand. However, while unemployment levels remain low comparing to other economies, many remain on the furlough schemes that have been extended until 2021-2022. We believe that re-introduction of strict lockdown measures, highlighted by the situation in Madrid, could further dampen the labour employment performance in Q4 2020.

The UK has been hit hard during the pandemic, and additional travel and domestic measures have been reintroduced to contain the second wave of coronavirus-related infections. Economic uncertainty is compounded with Brexit negotiations in Q4 2020. As the deadline for the agreement is approaching, it is becoming clearer that the UK and the EU are not going to reach the deal this year, which is most likely to cause a significant shock to the UK economy. Indeed, the BoE has begun to consider the implications of negative interest rates on the economy, given their implementation in the case for a hard-Brexit scenario.

China

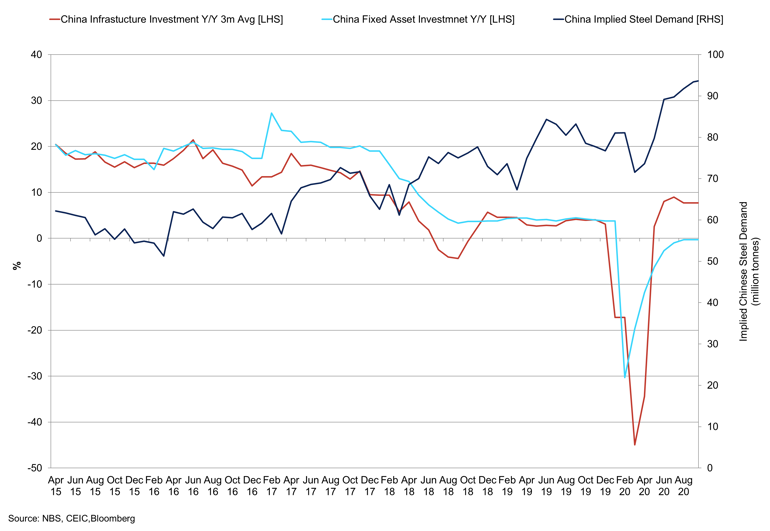

The recovery in China has continued through Q3 2020, with the service sector catching up with the manufacturing. Construction activity has seen a significant improvement in the last couple of months, and there is a large pipeline of infrastructure projects to be started. Indeed, infrastructure investment has picked up by 7.70% y/y in August, in line with the pre-pandemic levels. To encourage spending, the government announced further stimulus measures, including coupons to households. At the same time, the central bank has made the monetary policy more accommodative, by lowering the loan prime rate from 4.15% in January to 3.85% in September. While the fiscal policy is set to remain supportive through the rest of the year, the stimulus still will not match that seen in 2015/16 as the government remains worried about excessive levels of debt.

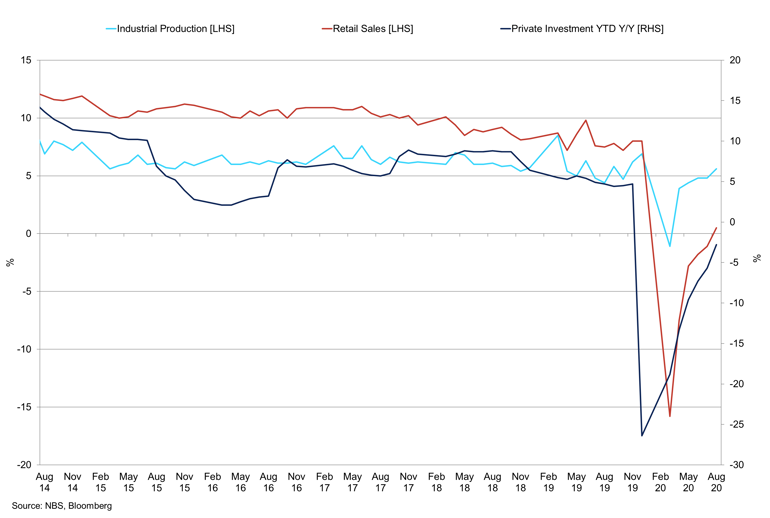

Retail Sales vs Private Investment vs Industrial Production

While industrial production is back at the pre-pandemic levels, retail and investment demand remains muted.

Meanwhile, high-frequency data shows that consumption recovery momentum has remained intact. In July and August, most activities returned to normal, from restaurants to air travel internally for vacations. The hotel occupancy ratio returned to 70% in August, and domestic travel is up to 90% of pre-pandemic levels. One of the biggest trends of consumption is reshoring of overseas consumption. Indeed, with international travel remaining low, Chinese consumers shifters their purchases to the homeland. Indeed, luxury goods reported a 20% y/y growth in Q2 in China.

While geopolitical risks are on the rise again, we do not foresee Phase One of the trade deal to be dissolved in the short term. Additionally, improved domestic performance should support recovery in Q4, especially, given controlled outbreaks across the rest of the world. Nevertheless, we think the phase one of the trade deal will remain intact as the election comes to the forefront of market focus. Indeed, a new threat could become a risk and further strain US-China relations, especially if Trump is re-elected in November. Biden's win could reduce the chance of new tariffs; however, China's reputation as a "trade abuser" could put the trade relationship on hold for the long term.

Nevertheless, despite this situation, the Chinese government continues to encourage inbound investment by US companies, and many appear to remain committed to participating in the Chinese market. Indeed, in September, US import levels from China have remained on-trend in the last two years, pointing to continued trade flows between two countries. Meanwhile, global investors remain optimistic about China. Inflows of FDI was up a strong 18.7% y/y in August, as the government encouraged an inflow of capital as part of its aim to create a larger capital base from which generate future growth. Also, the government reported that Chinese banks increased lending by 29% m/m in August, with lending to businesses up by 119% m/m. The rising credit demand highlights the growing business confidence about the state of the economy, as well as the easing of credit conditions by the PBOC. We, therefore, believe that this rise in business credit could lead to an acceleration in investment in the medium term.

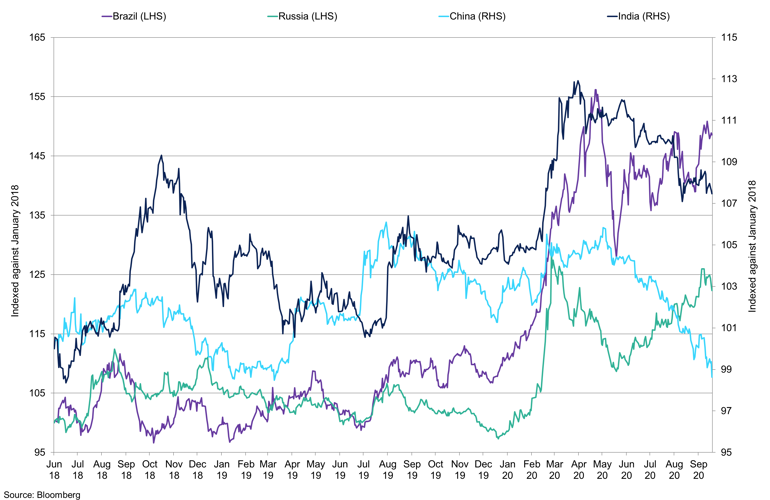

Emerging markets

In Q3, in line with the rest of the world, we saw significant recoveries in emerging markets, with MSCI EM Index rising 8.90% to climb just below the pre-pandemic peak. Emerging markets owed their positive performance to a global risk-on environment. Indeed, the Fed inspired investor confidence by leaving the interest rates low and adjusting their policy to new inflationary targets for the long term. However, just as in the US, equity performance was attributable to technology and e-commerce success in the quarter. We expect a bumpy recovery, with repeated coronavirus outbreaks having a long-lasting impact on the outlook. However, the major headwinds prevail – upcoming US election, as well as the trade, spat between China and the US.

Emerging Market Currencies

Brazil and Russia, the countries with one of the highest cases of infections, have suffered currency devaluations.

With some countries still struggling with second or third waves of coronavirus-related transmissions, others are seeing containment measures eased to gradually reopen the economies. The economic shock's size, however, varies greatly across the region, depending on the size of balance sheets. Asian economies, for example, remain resilient to the shocks as strict lockdown measures stalled within-country travel. Other economies, such as India, Russia and Mexico, have crossed the highest level of new daily infections globally and, therefore, are likely to suffer significant economic damage. The most optimistic forecast of a vaccine release in 2021 suggests that the economies will have to open up irrespectively to set on the path of economic recovery. Indeed, despite the newly-introduced pension reform as well as the interest rate cuts throughout the quarter, the continuing number of cases are likely to add additional pressure to strained fiscal accounts in Brazil. Their budget balance as % of GDP has already fallen sharply, down to 12.98% deficit, the lowest level since the recording of data in 1996.

Aluminium

Summary

Falling inventories, rising investment funds net long position, and the weaker US dollar helped give rise to aluminium prices. However, production in China remains very strong, and high bauxite imports and alumina production suggests aluminium production will continue in the coming months. High levels of monetary and fiscal stimulus will help provide support to the construction industry, especially residential housing. The automobile sector has woken up, which provides tailwinds to demand, but the rising COVID-19 cases and increasing lockdown restrictions continue to prevent economies from recovering further.

Q3 Review

Aluminium prices gained ground this quarter, as investors become more optimistic about consumption as lockdown restrictions were eased across the globe and the industrial, manufacturing, and construction industries restarted and with-it material consumption. Aluminium prices gained 9.12% this quarter and closed at $1,765/t after prices failed above $1,800/t. We have seen prices push to $1,850/t since the start of the Q4. Sentiment has been volatile as investors have to deal with vast stimulus measures, rising virus cases, and ever-changing lockdown restrictions. We expect this trend to remain the case as we await a vaccine and cases in Europe increase significantly threatening the recovery. Economic data has plateaued, and the recent spikes in cases give data a moderate downside bias in the near term. SHFE aluminium prices consolidated in Q3 up 2.34%, after a strong period Q2.

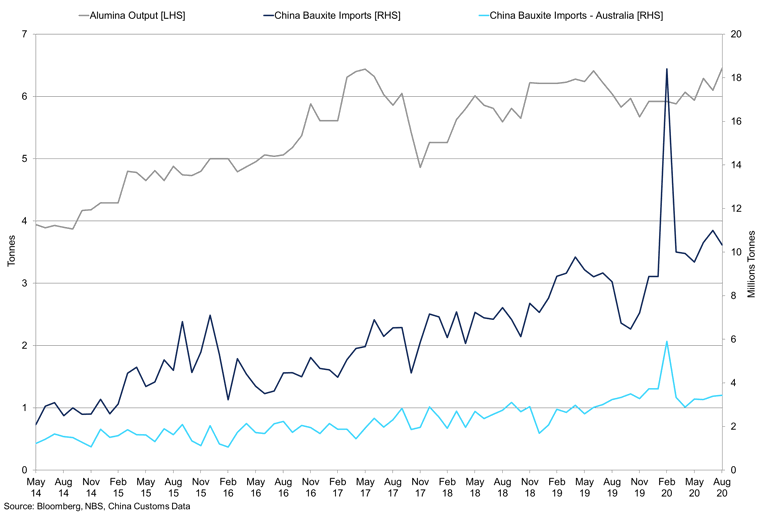

China Industrial Output – Primary Aluminium vs Imports

Bauxite imports into China and Alumina output suggest high output of primary aluminium in the coming months.

Outlook

Chinese aluminium output has continued to trend higher in recent months, with NBS data suggesting output surpassed 3m tonnes a month every month since June. Output of primary aluminium reached 3.171m tonnes in August after 3.096m tonnes in July, up 5.5% y/y and 3.10% y/y respectively. We expect production of primary aluminium prices to continue as new capacity has been commissioned this year. The strong rally in prices will keep production of primary aluminium strong as higher cost producers keep production levels elevated, in the long run, this will keep prices subdued. Lower cost producers have suppressed the cost curve, and this will also suggest higher output levels for longer. Cumulative production of primary aluminium reached 24.2m tonnes in August, up from 23.46m tonnes through to the same period last year. Output of aluminium alloys consolidated in 2020 with August production falling to 812,000 tonnes, down from 816,000 tonnes in July. Incidentally, this was the lowest level this year since March when output was 727,000 tonnes. In line with weaker production levels aluminium alloys on a month-on-month basis, cumulative production reached 5.86m tonnes in August, which is down from 6.086m tonnes at the same period last year. According to NBS data, output of aluminium products has fallen from their high in June from 5.57m tonnes to 4.86m tonnes in August, up 11.4% y/y. Cumulative output for aluminium products reached 34.99m tonnes in 2020 through to the end of August, up 5.5% y/y. According to IAI, global production of aluminium decreased to 5.485m tonnes in August, down from 5.489m tonnes the month prior. We expect most of the improvement in output from China as the RoW struggles to keep up.

Chinese bauxite imports trended higher with aluminium production. Unsurprisingly, in August imports totalled 10.32m tonnes, down slightly from 11m tonnes in July. We expect this trend to continue as new capacity for aluminium comes online, and production levels push ever higher. Imports from Guinea fell back to 4.9m tonnes in August. Bauxite CIF edged to $39/t as of October 12th, and we expect demand from China to remain strong as they keep aluminium production at high levels. Domestic prices of bauxite have remained relatively constant. Alumina chemical grade production on a global scale has weakened according to the IAI, with production at 625,000 tonnes at the end of August, 296,000 tonnes was produced in China. NBS data shows that output of aluminium oxide reached 6.45m tonnes in August, up from 6.10m tonnes in July. According to SMM alumina production was 5.76m tonnes in August, up 1% m/m from July and 3% y/y. Cumulative output is slightly down on last year, but rising production will present further pressure on alumina prices. China imported alumina min 98.5% from Australia FOB has started to fall to $276/t. Alumina prices in China have consolidated in recent weeks, and stand at 2,334RMB/t. With bauxite imports strong we expect alumina to soften in the coming quarter as production remains strong.

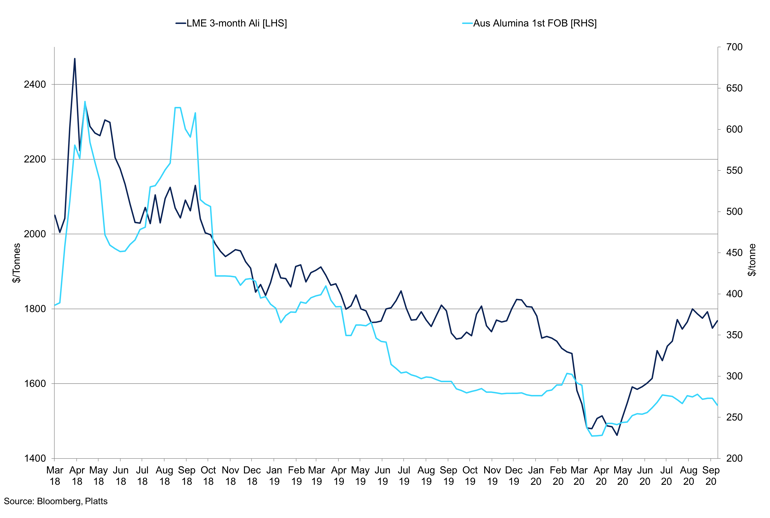

3-month LME Aluminium Price vs Alumina 1st Generic FOB

Strong Alumina production will cap price gains in Q4.

On the demand side, we are seeing some softness in demand from China following the national holiday. According to an SMM survey, downstream business owners are not optimistic about consumption in October, but as we move into the final months of 2020, we could see consumption improve once again. However, extrusion demand in September was unchanged from August and with expectations for an October low, there is little prospect for change in the near term. Stimulus measures around the world still hugely expansive, but rising cases in Europe will certainly cap demand as restrictions in the bloc rise once again prompting leading economic indicators to weaken in the near term. Operating rates at construction aluminium extruders have remained constant since April, above 60% and rates ran 62.32% in August. Industrial extruder operating rates have been slightly more volatile and increased up to 64.6% in August. As mentioned, demand has plateaued, and we could see inventories rise in the near term. Inventories of billet at five major consumption areas have risen sharply in recent weeks to 105,700 tonnes as of October 9th, a weekly rise of 42,000 tonnes. Imports into China of unwrought aluminium & products rose sharply in 2020, reaching 429,000 tonnes in August, up from 391,000 tonnes in July. As mentioned, demand conditions have started to waiver, and this may prompt further rises in domestic inventories.

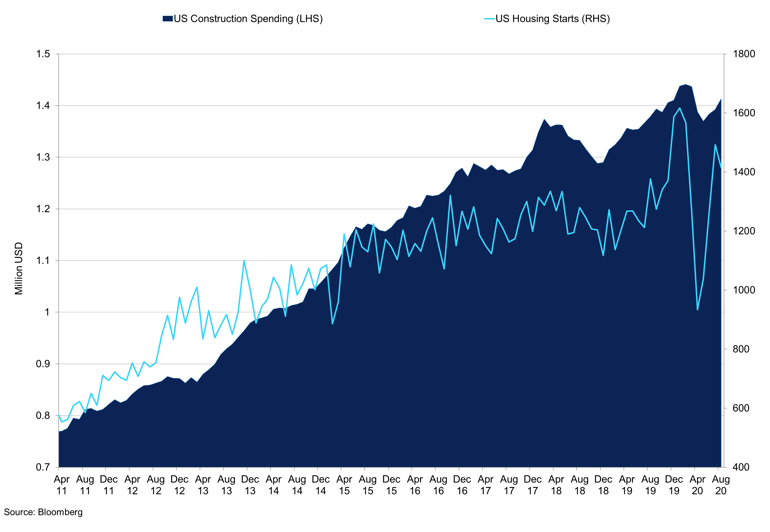

The export market is weak; Chinese exports of unwrought aluminium and aluminium products have been low this year due to COVID-19. However, following the easing of restrictions and mass economic stimulus, month-on-month figures have shown signs of improvement. In August exports reached 395,000 tonnes, up from 373,000 tonnes in July. YTD exports reached 2.46m tonnes in August, but the primary market still lags, data suggests that exports of primary aluminium were 249 tonnes in August. We expect demand in the construction sectors to improve, especially in residential housing, due to low interest rates boosting mortgages and housing. Housing starts in the US strengthened since April, reaching 1.416m units in August, slightly down from 1.492m units in July. However, the trend remains intact, and we expect cheaper access to capital through low rates to support housing permits which increased to 1,476m in August, marginally down from 1,483 in July. In Europe, construction PMI was 47.5 in September, the lowest level since May as construction output in Germany and France declined. New orders and employment declined once again, and this is expected to remain the case in October and November as cases rise, overall business expectations are weak, and this will suppress demand for aluminium.

US Construction Spending vs US Housing Starts

The US housing and construction market is benefitting from reduced borrowing costs, this will continue.

Auto demand for aluminium is improving, not just through stronger production levels as the globe recovers from the first wave of COVID-19, in some regions more successfully than others. In China, vehicle production was 2.119m units in August, marginally down from July and June at 2.201m and 2.325m units respectively. Passenger vehicle production also started to plateau in August at 1.694m units, down from 1.729m units in July. In the US, seasonally adjusted producers reached 11.3mn units in August, down from 11.9m units in, total autos were 2.5m units with trucks making up most of the output at 8.8m units. The trend of higher aluminium content will continue this year, in the US vehicles on average contained 449/lbs of aluminium, higher than the aluminium content in China’s vehicles which have 400/lbs per vehicle.

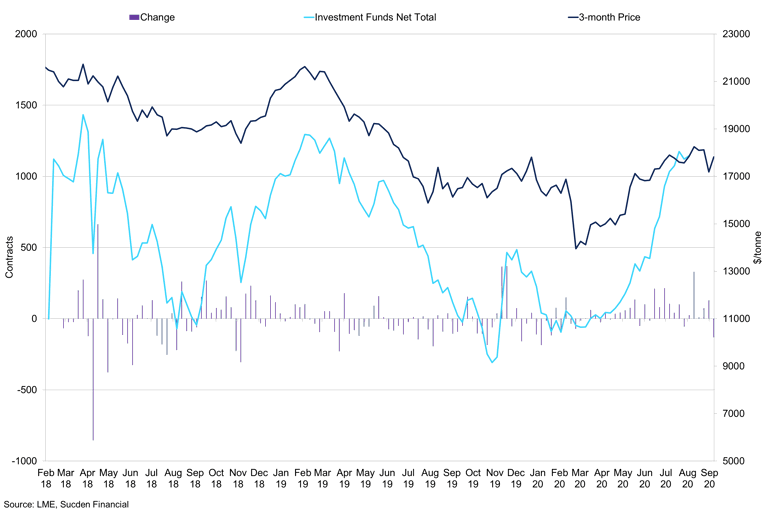

Investment Funds Total Position vs Change in Investment Funds Position vs 3-month LME Price

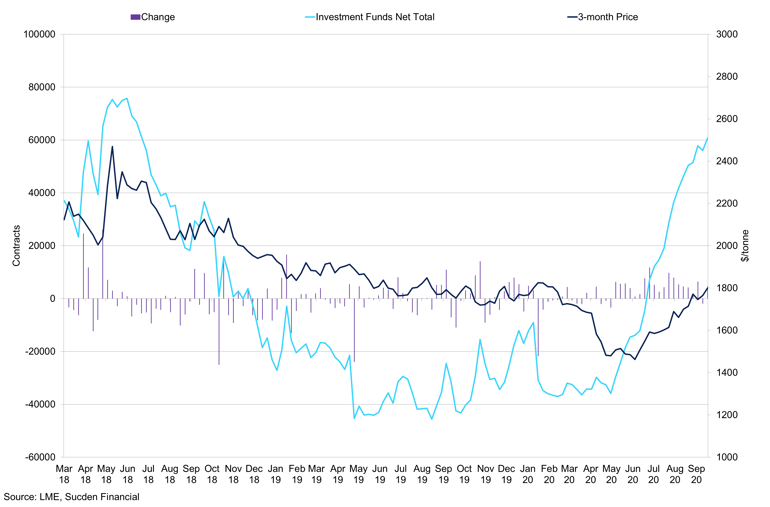

The rally in the LME 3-month price has been prompted by a strong increase in the Investment Funds Net Length.

The commitment of traders’ reports for the LME has seen an increased correlation between the investment funds position and the change in 3-month LME price. The correlation reached 0.4 compared to the investment funds and credit constitution correlation, which stands at -0.06146. LME prices rallied in recent months despite the downbeat demand outlook, but the vast amount of stimulus measures and backwardation in SHFE is supportive in. The commercial undertaking short position also declined in recent months as prices have rallied away from them. Low levels of social inventory in China could support prices, and in the longer run stimulus measures could cause premiums to rise, as we have seen with the US Midwest aluminium ingot premium rally to $320.90/t as of September 2020. Falling inventories have helped support the outlook of aluminium demand with LME inventories falling to 1.42m tonnes as of October 12th. Continued withdrawals would prompt further positivity into the market, but we doubt physical demand is strong, and production levels in China remain very strong.

Copper

Summary

The copper market fundamentals point to a correction in the downside as output in China is strong, and inventory levels have increased, however, risk appetite remains with the expansive monetary conditions. Demand in China is robust, and global fiscal stimulus should support RoW consumption. Rising cases in Europe are a worry and will act as a headwind to price, but a weaker dollar from the US election outcome is supportive. On the supply side, output is improving, and we do not expect any further declines at this time. We expect TCs to improve in the coming months above $58/t. We expect investment funds to maintain a long position but do not expect economic data to post strong gains in Q4 which will dampen sentiment. The US election is a risk event, but when we look at the possible scenarios, there is a bullish case for copper for most outcomes.

Q3 Review

Copper prices continued the trend from Q2 as demand optimism improved due to the easing of lockdown restrictions. Consistent with our previous report and our upside forecast, prices peaked above $6,800/t at $6,877.50/t. As we moved through the quarter, economic data plateaued and cases of COVID-19 started to rise once again in Europe, prompting restrictions to increase once again. Prices on the LME gained 10.5% in Q3, aided by falling LME inventories which declined 66% to 73,625 tonnes. However, inflows of material in September saw stocks fall 20%. We also saw some support from the weaker dollar and strengthening CN, but prices have stalled as these currencies have consolidated. SHFE prices also consolidated up 4% in Q3, after failing above 54,000RMB/t. SHFE deliverable stocks have improved in Q3 to 156,454 tonnes as of October 9th. We saw the cash to 3-month spread tighten into $40/t backwardation in Q3, as there was some tightness in the market and cash was continually bid, this pressure eased, and we traded at $10.25/t contango.

Outlook

Copper mine supply, like other base metals, has been heavily impacted in 2020 due to social distancing measures, and national wide lockdowns. Major mining countries saw declines in output in H1 2020 which caused tightness in the concentrate market. Codelco, Southern Copper, First Quantum Minerals and Lunding Mining saw year-on-year gains for production. Peru was heavily impacted by the global lockdown, with output down by 20.4% y/y in H1 2020, other metals mining activity such as zinc, lead, tin, gold, and silver were also down year-on-year during the same period. Peru copper output has started to recover and was at 180,000 tonnes in September, up from 111,700 tonnes in April. We expect mining output to have increased since the start of H2 2020. Copper production in Chile is well known for disruption due to worker strikes, but this year COVID-19 has prompted the government to extend the state of catastrophe for another 90 days.

Theoretically, this would keep mine supply on the back foot, but in practice, output has managed well through this catastrophe period. In the first seven months of 2020, output increased to 3.31m tonnes, up 1.86% y/y compared to the same period last year and Codelco output was up 4.1% in H1 2020 to 744,000 tonnes. Even with the virus not under control, we do not expect mine output to see a considerable downside. The SMM copper concentrate index with concentrate having a copper content of 22-36% CIF has been falling since April 2020 from $68/t to $48.45/t in September. Chile concentrate exports have started to improve in recent months, and this has helped the relative tightness in the market. Total production has been strong as mentioned above, and the value of exported products has been improving this year, and this is expected to remain the case in the coming months despite the downside risks to prices from COVID-19, geopolitical tensions, and risk to the dollar. Output from Chile is improving, and we expect this to remain the case in Q4. China copper concentrate TC 25% CIF has fallen since March due to the reduced availability and steady demand from Chinese smelters.

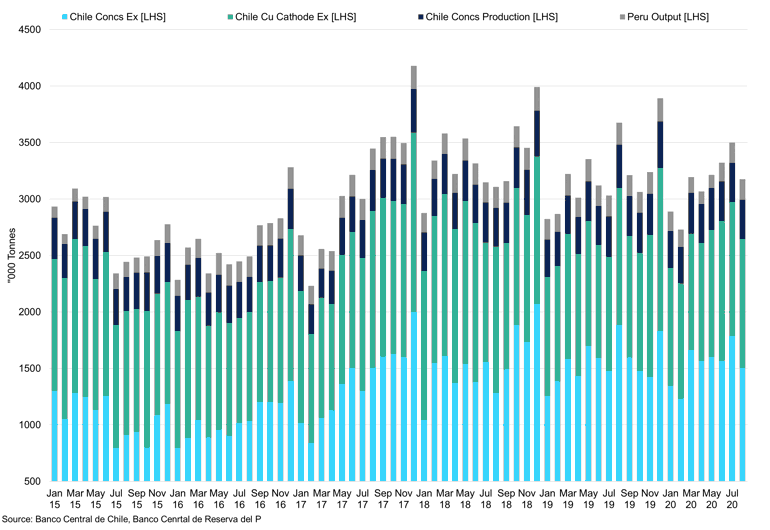

Chile Concentrate and Cathode Exports vs Chile Concentrate Output vs Peru Output

Output has started to recover in Q3 2020 from the lows in Q2, improving concentrate availability.

Output of copper from China continued to remain strong despite tightening mine supply. Chinese copper cathode production reached 815,900 tonnes in September up from 810,500 tonnes the month prior and the strongest monthly output this year, according to NBS data. Indeed, refined copper production was the same, posting a YTD high in August 894,000 tonnes, up from 814,000 tonnes in July. The year-on-year output of refined copper was up 20% in August and has been up every month so far this year. This outlines the strength and resilience of the smelters, however, if output remains this high, we expect further tightness in the concentrate market, as well as some excess material in the market due to weak consumption outside of China. Cumulative output for refined copper has reached 6.527m tonnes as of August 2020, with cumulative output of copper products at 13m tonnes. These figures are higher year-on-year, but we know global demand is down. This outlines strong consumption from China this year but also the disconnect in the market between the current price and underlying demand. We attribute this to the expansive stimulus measures from governments and central banks, boosting liquidity and future demand.

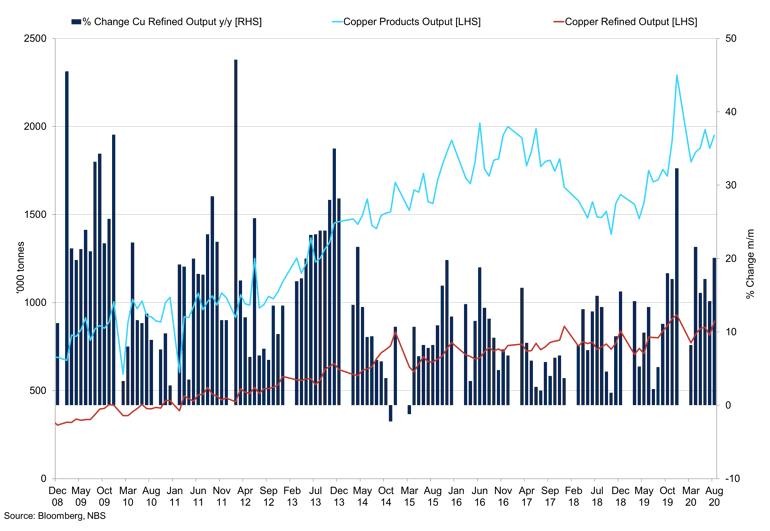

China Refined Output vs Copper Products

Output in China has been strong, and this is expected to remain the case.

Low interest rates and stronger sequential economic data through Q3 improved risk appetite and the weaker dollar gave rise to prices. The strengthening renminbi was exemplified by the increase in Chinese imports in September, and this will continue to in the near term. The exports of unwrought copper and products have started to improve but are still coming from a low base, standing at 54,290 tonnes. Imports of unwrought copper and copper products have also surged this year off the back of strong industrial and construction activity. Imports reached 722,000 tonnes in September against this year’s monthly average of 584,881 tonnes through the first nine months of the year compared to 417,000 tonnes for 2019. China is also accumulating reserves, and this will keep imports elevated. SRB inventory has been increasing through Q3 and reached 12,750,000 tonnes at the end of September. Bonded warehouse inventory has been declining since May 2019 and stands at 2,495,000 tonnes as of September.

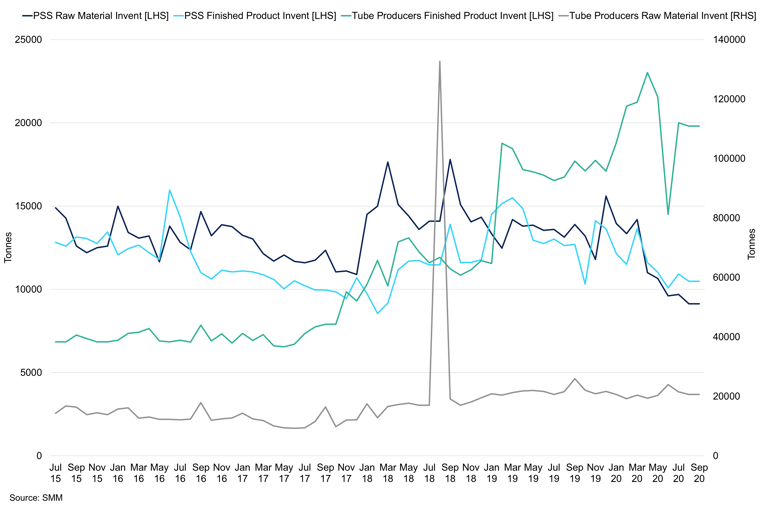

China Copper Products Monthly Inventory

We are seeing drawdowns of stocks for some copper products suggesting strong demand.

Domestic inventories for copper products in China are mixed, we have seen a strong rebound in tube producers finished product inventory in Q3, however conversely stocks of PSS finished products have been falling, but so have inventory of PSS raw materials. Finished inventory at wire producers have also increased to 23,300 tonnes, with raw material stocks also rising, consumer stocks are also trending lower. Smelter and refinery inventory has been falling, a continuation of this trend will prompt further excitement about Chinese demand. Stimulus measures remain strong, and this will continue to support consumption of copper. Retail sales are positive at 0.5%, and industrial production is also strong at 5%. China’s all-system financing was 3.582trn in August, up from the month prior and as stimulus remains strong, we expect Chinese demand to be elevated as infrastructure investment accounts for a large proportion of China’s copper demand. High-speed railways are particularly supportive of copper demand, as well as smart cities, 5G, and data centres. According to Bloomberg, national grid expenditure is up 1% y/y, which has prompted strong demand, consumer demand is more fractious, especially outside of China. Employment is declining, and as we move into Q4 and another wave of virus infection, the outlook is uncertain. While countries have managed to avoid national lockdowns, consumer and business sentiment is downbeat about future activity.

Copper investment funds are at the top of the recent range of their net long position; they seem reluctant to add further length. This could be due to the stabilising dollar but also reduced risk appetite due to rising cases. We have seen more producer selling as prices have rallied and this could trigger some producers to be stopped out if prices break $7,000/t, prompting further gains.

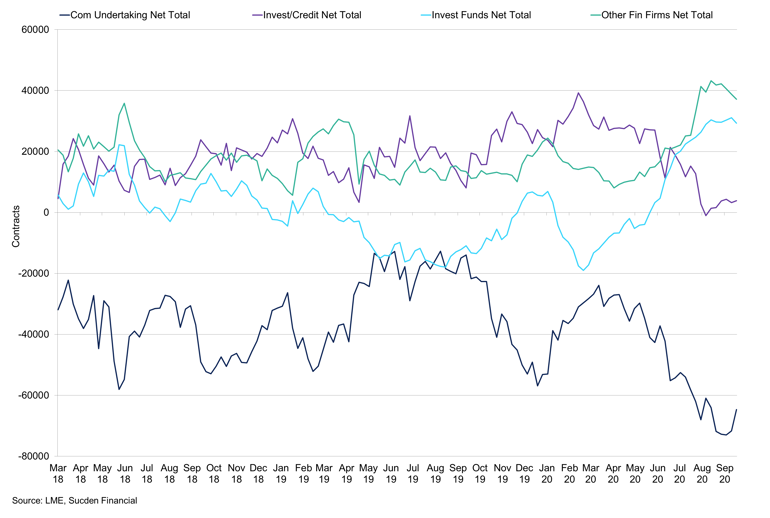

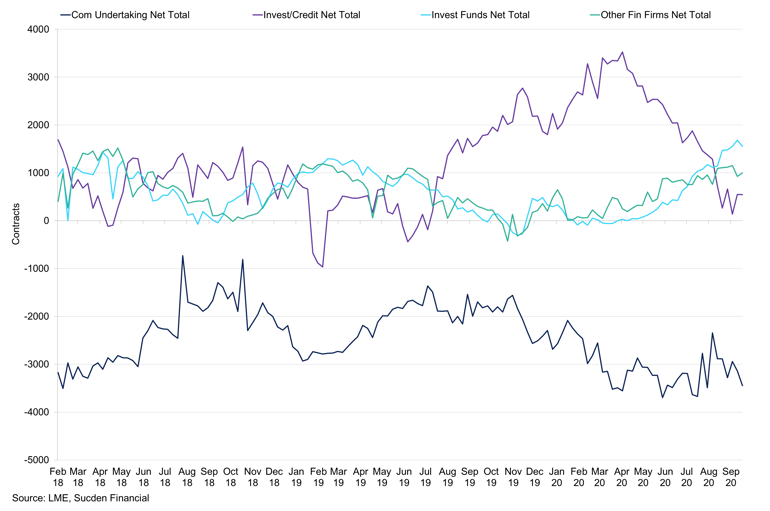

Copper Commitment of Traders' Report Total Positions

As Investment Funds have been increasing their net long position, whereas commercial firms have been upscale sellers.

Lead

Summary

The auto market has continued to recover, and new orders in Germany suggest this trend will continue in the near term. We expect battery replacement demand to remain strong in Q4 following vehicles being idled for a long period of time, and supply chain constraints. Domestic TCs in China and imported concentrate TCs have fallen, and this could suggest some tightness in the concentrate market; however, Chinese lead output has been trending higher, and this is expected to continue. Investment funds have switched to a net short, and the correlation between their net position change and weekly LME price change has grown stronger. We anticipate lead suffering from high inventory levels, and strong output in China, as demand continues to recover.

Q3 Review

Lead prices were well supported in the first half of the quarter as they tested $2,000/t, but as the fund position started to liquidate their longs, and as material flowed into warehouses, futures retreated through major support levels to $1,794/t. The auto sector has started to recover, and we expect this to remain the case in the near term, which is a bright spot for the market. SHFE first month prices stood at 15,105RMB/t before the holiday. We have seen some withdrawals from SHFE warehouses, and deliverable stocks stand at 16,804 tonnes.

LME Lead Warehouses vs SHFE Deliverable Stocks

LME and SHFE inventories have increased in recent months, but LME cancelled warrants remain subdued.

Outlook

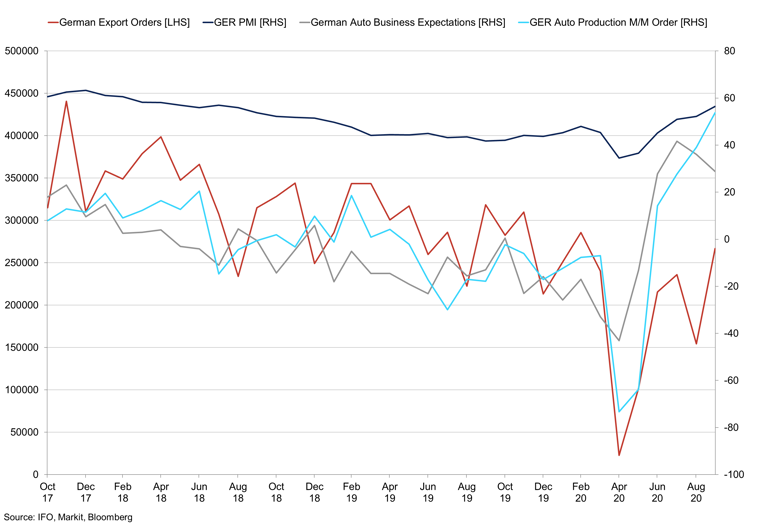

VDA German car production partially recovered from the pandemic low but we saw output soften again in August to 203,100 units, down from the 334,000 units in July. Exports have trended higher since April but continue to struggle. Demand for autos has recovered since the lows, but the lack of certainty surrounding future employment will reduce demand for luxury items such as autos. The rise in COVID-19 cases in Europe during August and September will present some downside to vehicle consumption. German exports in August were 154,300, down from the previous month at 242,800 units, however, in September the export market rallied to 266,600. Low interest rates will keep financing conditions accommodative and could provide support for vehicle purchases, and we do not expect rates to rise in the next 12-18 months, which may help to support battery demand. We are seeing order books for German autos continue to improve with the IFO New Order Index reaching 53.7, the highest the index has been since records started. Business expectations have suffered slightly since cases have started to rise once again, business expectations fell to 28.8 in August, down from 41.6 in July, which was the highest since 2004. Production of autos in China reached 1.69m units in August, with year-to-date production at 11.17m units which is down 9.6% YTD Y/Y. August production data was up 6.3% y/y but down 3.7% y/y. Commercial vehicle output from the record high in June at 527,000 units, to 424,952 units, YTD production has reached 3.25m units which is up 19.3% YTD Y/Y.

German Automobile vs German Manufacturing PMI

German auto exports are recovering, along with production and business expectations.

The lead battery market witnessed stronger demand in Q3, with improved mobility across the globe following lockdowns supporting automobile demand. However, we also saw stronger demand for battery replacements following the long period where cars were idled. The issue was that collection rates and supply of secondary batteries was low; however, this market has begun to wake up. Manufacturers were slow to restart, which presented even more problems for companies who adopted a lean ‘just in time’ supply chain model. The shift in demand seen in H1 2020 has become apparent since the lockdown restrictions were eased. We expect this demand recovery to continue in Q4, and collection rates to improve as well. Prices for recycled scrap lead start-type batteries ex-VAT have increased significantly in recent months, due to reduced availability and low collection rates. From the March low, prices have gained 15.3% to $7,875/t; similarly, the deep scrap battery ex-VAT has gained 14.92% to $8,475/t. As availability has improved, prices have edged lower, and this could remain the case as producer’s operation rates have recovered. We expect demand from the automobile market to improve as production of new cars rises.

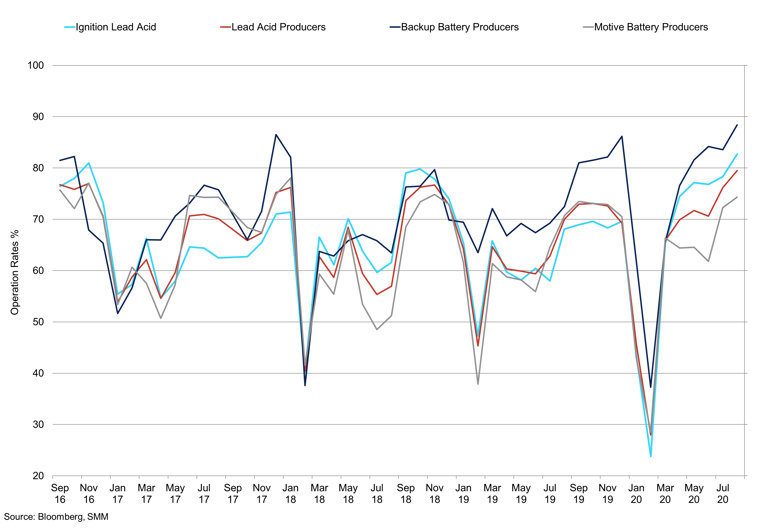

China Battery Operating Rates

Operating rates have pushed back to pre-pandemic levels, and in some cases surpasses previous levels.

Operation rates for lead-acid producers and ignition lead producers in China have been rising in recent months back to pre-pandemic highs, with both around 80%. Lead-acid battery producers in the top 5 regions averaged 72.72%, with the highest level of 88.28% in the week to September 25th. Chinese battery exports reached 298.5m units in August, which suggests continued improvement in the export market Incidentally this is a record amount of exports and we attribute this to improving business conditions and a backlog of orders. Domestically, stockpiling was taking place in the run-up to the holiday in China, we expect operation rates to remain constant throughout the holiday in large producers. Medium and large Chinese secondary lead producer operation rates have recovered, large producers are at the pre-pandemic highs, around 57% and medium producer operation rates have surpassed previous highs, operating at 54% capacity. Operation rates at primary lead smelters have held steady in recent weeks at some of the major lead provinces. Henan, Hunan and Yunnan provinces operation rates averaged 59.3%, with Henan rates were the highest at 75.5%, according to SMM.

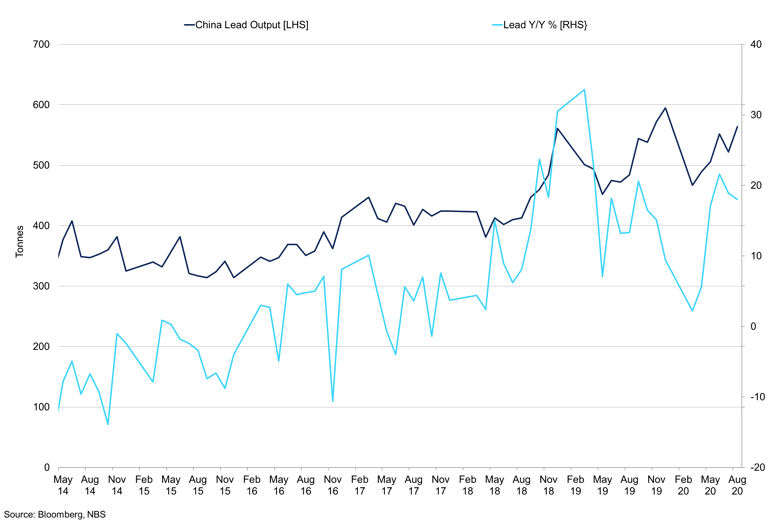

Chinese Lead Output vs Chinese Output Y/Y

Lead output in China is growing at a robust level once again, but reduced mine supply could present headwinds.

Global lead supply has continued to recover, the most up to date data suggests that global mine supply reached 425,864 tonnes in June, 55% of which came from China. RoW production remains sluggish due to capacity constraints and social distancing measures. South American supply reached 28,762 tonnes up from 3,272 tonnes in March. We expect this trend to continue in the near term and increase the availability of material. Global refined lead production has continued to pick up in line with mine supply. China output produced 50% of the worlds refined lead in June, with operation rates remaining high in recent weeks we expect refined metals availability to improve. Chinese lead production has trended this year despite the pandemic; August production was 564,000 tonnes which was up 18% y/y, bringing cumulative output 3.98m tonnes up 7.6% y/y. With the holiday in full swing, do not expect this to hinder production for October. With demand still recovering we have seen an increase in exchange warehouse stocks with LME stocks up 106% in Q3 to 137,000 tonnes as of October 1st, we have seen cancelled warrants increase recently suggesting improved demand. SHFE inventories have fallen in recent months by 37.85% to 16,804 tonnes. Off-exchange lead stocks in China have fallen in Q3, declining from 47,700 tonnes on July 17th to 23,000 tonnes. Chinese lead ore imports have fallen from the YTD high of 134,000 tonnes in July to 107,000 tonnes in August, significantly below 2019 levels. This is expected due to the reduction in mine supply this year. Similarly, exports ground to a halt this year with a total of 51.39 tonnes in July, in August we saw exports improve to 596.70 tonnes which is significantly below the 7-year average at 1,888.85 tonnes.

Chinese domestic TCs edged lower in the last month in dollar terms TCs have traded a range of $278.92-$322.92/t, with the average at $300.94/t, $14.6/t lower than the previous month, according to SMM. TC for imported lead concentrate has decreased by $35 this month to a range of $90-120/t, averaging $105/t, according to SMM. Chinese lead concentrate TC 50% CIF stands at $125/t as of September 29th. The lower TCs suggest stronger demand for available material. Concentrate availability has dwindled as a result of lower mine supply, and as Chinese ore/concentrate imports fall material will become scarcer, even as Chinese mine output improves. The import arbitrage window into China is shut down the curve, and this looks set to continue. Increasing tightness in the concentrate market may exert downward pressure on TCs in China but with LME inventories have risen sharply, indicating plentiful refined availability at this time.

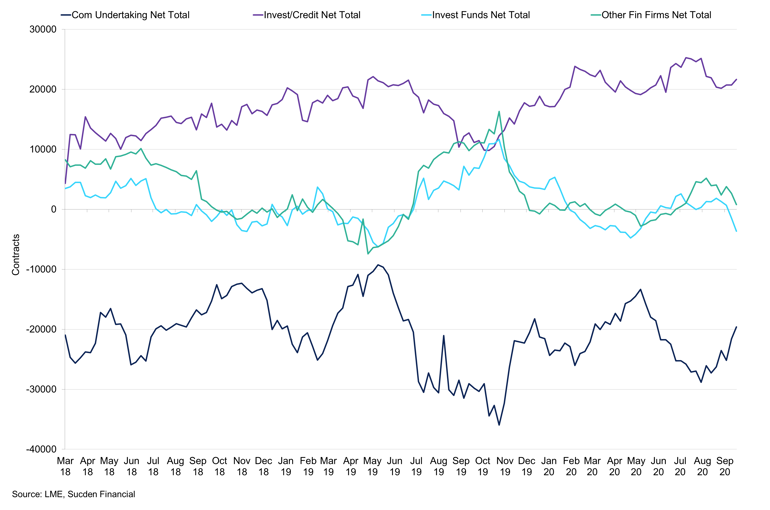

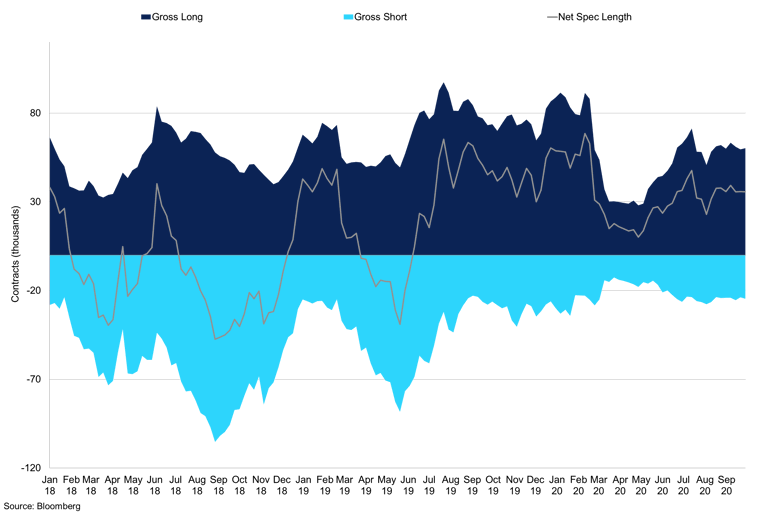

Copper Commitment of Traders’ Net Total Positions

Investment Funds have flipped to a net short, and we have seen commercial firms reduce their net short position.

The commitment of traders reports from the LME show that investment funds recent reduced their long exposure and have flipped to being short. The 30-day rolling correlation between the change in the investment funds net position and the change in LME price has edged higher to 0.531 as of September 18th, the highest it has been since February. As funds are now short, and the correlation is stronger, this could trigger lower prices in the near term as the selling continues. While demand is improved, the large inflow of stock will likely weigh on prices even though cancelled warrants have also increased. We expect material to stay on warrant, the grand position for net other as reported by the LME suggests a reduction in the long position as well. The z-score for lead’s grand other position is 1.4, above the upper quartile, which is 0.71, marginally below the 4-week average as well. This suggests a reduced appetite for lead from the long side. Indeed, we have seen a moderate increase in the commercial short in recent weeks which could have been down to opportunistic hedgers.

Nickel

Summary

Chinese NPI has plateaued in recent months, and as mentioned in previous reports, we expect the reduced amount of Indonesian ore imports to keep this trend intact. Chinese nickel ore imports have started to increase from the Philippines, but we expect the annual imports to be lower in 2020. Stainless steel output has recovered well, and this will remain the case in Q4 which will be a boon for nickel prices. EVs position in the market is going from strength to strength, and we expect higher nickel content in batteries in the coming years to increase the energy density and range of batteries and vehicles. We expect nickel prices trend higher in Q4 even with demand outside China lagging.

Q3 Review

Nickel prices performed well in Q3, gaining 13.3% to close at $14,517/t. Industrial metals have performed well as data from China showed a strong recovery, throughout Q2 and Q3. Economic data in the US and Europe responded as lockdown restrictions eased and manufacturing and industrial production started to improve on a sequential basis; however, data plateaued as cases started to rise and restrictions were put back in place. There is a clear divergence between the health of the US, and the European economy and China. China’s strength can be attributed to strong stimulus and domestic investment in resource-intensive supply-side policies. SHFE prices also improved in Q3 with the 1st generic contract testing 123,000RMB/t, but in September, bullish momentum subsided, and the market closed at Q3 at 113,000RMB/t. Nickel inventories have remained constant for much of 2020, with LME stocks at 236,088.

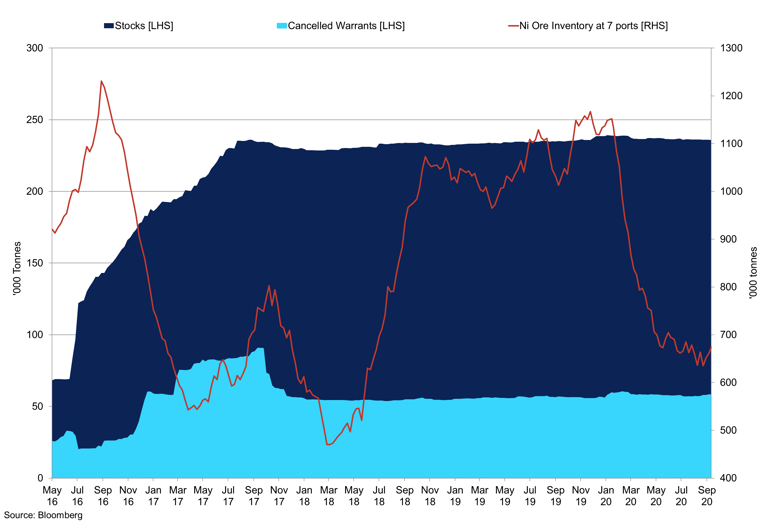

LME Nickel Inventory vs Ni Ore Inventory at 7 Major Ports in China

Ore inventory has fallen at Chinese ports, but exchange inventories have remained constant.

Outlook

Nickel supply for 2020 was expected to be lower this year due to the Indonesia ore export ban, and this has rung true. However, output is expected to increase in 2021 as the Indonesian smelting nickel smelting industry continues to grow. We saw some mild flooding in Indonesia recently, which halted some production in August, but this only had a mild impact on output. Class 2 output of nickel is rising significantly in Indonesia, and this will continue. Indeed, this comes at a time when Tesla has suggested they will remove Class 1 nickel from the dissolution process. Refined nickel production will continue to rise due to developments in Indonesia; forecasts suggest we could see output rising to 2.50m tonnes in 2021 before edging towards 3m tonnes in 2022 and 2023. The reduction in nickel ore from Indonesia has had a negative impact on Chinese NPI production with estimates for the year at just over 500,000 tonnes. There is some downside to this figure as the exports from the Philippines have been lower due to reduced mine output for H1 2020, which was 102,300 tonnes, down from 141,600 tonnes last year. However, we have seen exports to China increase in recent months and Wood Mackenzie suggest nickel exports to China could fall to 28m tonnes in 2020, down from 30m tonnes in 2019.

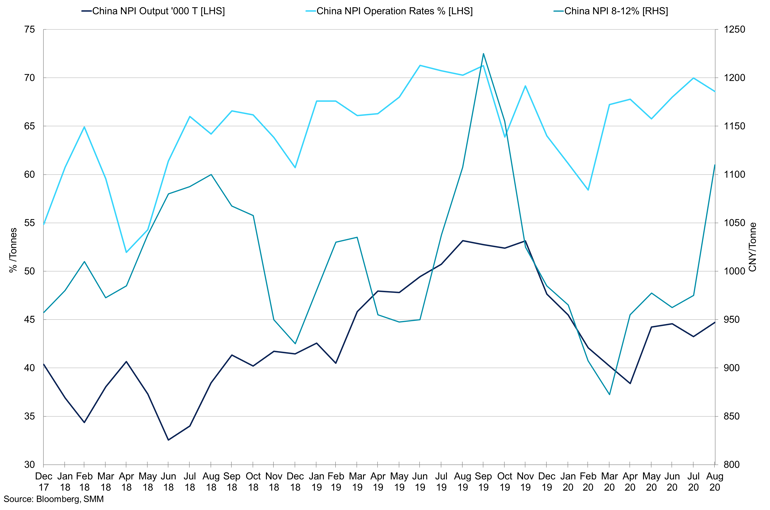

Chinese NPI vs China 8-12% NPI Price

NPI output has remained constant as have operating rates, and we expect this to remain the case.

Chinese imports of nickel ore have been increasing in recent months reaching 4.903m tonnes in July and August shipments were slightly down at 3.745m tonnes. Unsurprisingly, shipments for this year have been considerably lower and have averaged 3m tonnes a month, versus 5m in 2019. We expect arrivals to remain above this year’s average for the remainder of the year. Ore inventories at Chinese ports have remained steady in Q3 and closed the quarter at 9.13m wmt up from 6.74m wmt at the same period last year, according to SMM, with the majority in Lianyungang. Due to the national holiday and stockpiling Shanghai bonded inventories have increased to 22,800 tonnes of refined nickel, according to SMM. Imports of ferronickel have also been on the rise since 2018, after spiking higher to 473,000 tonnes in February 2020, when both January and February were combined. Imports have steadied but remain on course to break 300,000 tonnes in the coming months. Imports for August were 291,924 tonnes, with domestic production of nickel pig iron are 44,680 tonnes in September, near flat on the month as August output was 44,720 tonnes. As mentioned, we expect China’s NPI output to be limited by the reduction in nickel ore imports, meaning the trend of higher ferronickel imports is expected to continue. Nickel pig iron 8-12% prices have been trending higher since April up 32.9% to 1,160RMB/t, and operating rates at domestic NPI mills have started to plateau at 67.94% for September, along with prices and production. There is clearly spare capacity at operating mills, but we anticipate output to consolidate for the remainder of 2020.

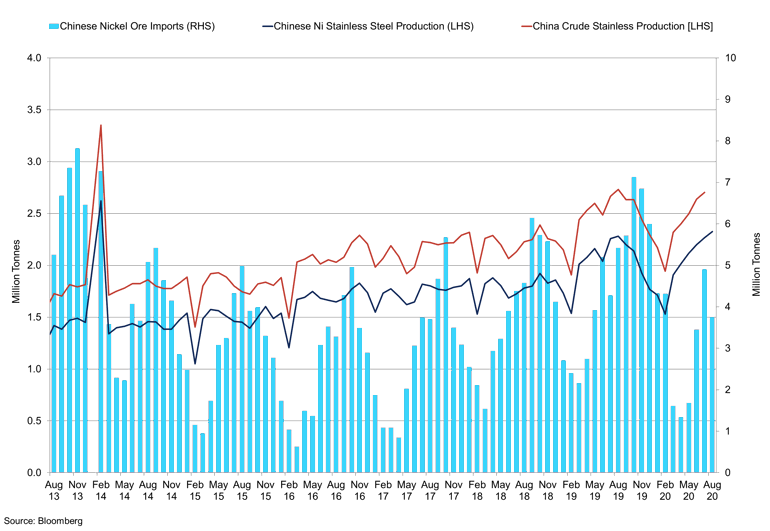

Chinese Nickel Ore Imports vs Stainless Steel Production

Ore imports have improved, and so has stainless steel production in China.

Crude stainless-steel output increased substantially in China from the February low of 1.9m tonnes to 2.831m tonnes in August. This was an improvement from July’s 2.704m tonnes, and we expect production to remain strong in the near term, but output gains will be more muted as operation rates are at 99% unless more capacity is added, which is not possible in the short term. Nickel bases stainless steel production also recovered, reaching a new high at 2.335m tonnes as of August 31st. We have seen a return to stainless steel billet production as it is exempt from the anti-dumping duty, this has triggered output of billet to reach 180,000 tonnes in July and August, and exports to China in H1 2020 reached 310,000 tonnes. We continue to watch this trend, but according to reports, inventories of long product semis as inventories start to rise in China. Inventories for cold-rolled coil have been falling, and since March/April this year, Steelhome CRC stocks declined to 1,300,000 as of October 2nd, with SMM suggesting total CRC inventories at 1,005,000 tonnes. Indeed, CR steel stocks at mills have started to increase during the national holiday and stand at 350,000 according to SMM.

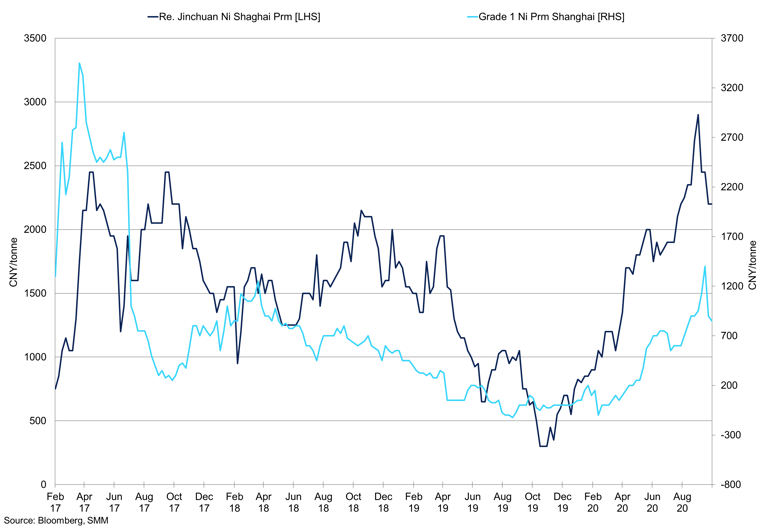

Nickel Premiums

Chinese Nickel Premiums have improved, suggesting stronger physical demand for the metal.

Non-stainless-steel demand for nickel has been split in half due to COVID-19, as industries such as the aerospace have been negatively impacted, whereas there has been strong environmental push throughout 2020 which may fast track demand from EVs. Orders from the aerospace are weak, and we expect this to remain the case as travel is restricted. Until there is a vaccine, orders for planes will remain subdued. Nickel alloy demand as a result of the activity decline will reduce consumption of nickel. The aerospace was rattled before COVID-19 after the fatal crashes of 737 Max, Boeing has since significantly reduced their orders of aircraft. In recent months we have also seen adjustments in Rolls Royce’s strategy, causing a reduction in the number of orders delivered. The EV market has recovered well, and we expect demand for EVs to kick on in the coming months and years. Tesla battery day confirmed the company’s drive to reduce cobalt in their batteries; however, the search to green nickel continues. Current waste management measures such as deep-sea disposal have raised serious questions around nickel production in EV batteries. Production of EVs in China has started to improve, but on a YTD, basis remains below 2019 levels. Total production for January to August is down 27% at 6,020,000units for NEVs. August production reached 1,060,000 units up 17.7% y/y and 6% m/m. Sales have also picked up in recent months, however, with August sales down 32.8% on the previous year according to the China Association of Automobile Manufacturers. While sales were down 5.5.% at 980,000 units, on year on year basis, sales were 19.3% stronger. With more EV models in production from car manufacturers, improving battery ranges, and the costs of vehicles declining we expect nickel demand from the EV sector to kick on in the near term, but what type of nickel? We heard from the Tesla World Battery Day, that class 1 nickel will not necessary be for battery production. Class 1 nickel has a purity over 99.8% and is around 55% of global production, and is nickel powders, briquettes, carbonyl nickel and electrolytic nickel. Class 2 has a lower purity and is NPI, laterite ores, nickel oxide ferronickel <99.8%. Subsidies in Europe will incentivise consumption in the bloc, autos registered up to the end of 2020 will have a 10yr exemption and with if the price is less than € 40,000 will qualify for a €9,000 until the end of 2021. We expect the demand for EVs in Europe to rise towards 2m in the coming years, prompting a large increase in nickel demand, in addition to this, production of EVs that are exported will rise. However, in Q4, we expect EV sales and production to rise, boosting nickel demand.

Tin

Summary

Demand is improving, outlined by the continued improvement of global semiconductor sales, and earnings potentials for key semiconductor and consumer electronic goods. We expect producers are holding back for higher prices before hedging as the balance of supply and demand moves to a deficit, and the supply outlook in the longer term is convoluted. We believe that China’s appetite for refined tin will remain strong, as well as for ore and concentrate. The outlook for tin remains supportive and expect prices to push higher in Q4.

Q3 Review

Tin prices appreciated in Q3, but gains were less pronounced as economic data normalised, prices closed 3.79% at $17,494/t. The high of the quarter was $18,225/t, but investors struggled for conviction above this level as we saw inflows into LME warehouses. Inventory closed the quarter at 5,475 tonnes up 54% in the quarter. SHFE prices gained 3.62% at 144,000RMB. Deliverable inventories have edged marginally higher in the last quarter. After the initial shock of the pandemic, demand recovered well, and technology has benefitted from the shift to home working and the digital age. This has also been to the benefit of China and other Asian countries. The headwind to the solder market is sanctions from the US on Chinese companies and Huawei who have had to shift their business plan towards the cloud.

Global Semiconductor Sales

Global sales are recovering, and we expect this to remain the case in Q4 despite trade tensions.

Outlook

The PHLX semiconductor index continued to push higher in the last quarter, gaining 12.55%. The technology rally has continued as the current world order of working from home and quarantine benefits the technology sector, despite large levels of unemployment. This shift to at-home-working has benefited the semiconductor sector, as well as other tech sectors such as chips which is less relatable for tin. The P/E ratios have increased further in Q3 to 32.43, up from 27.03 in 2019, gross margin for 2020 is down slightly from our previous report at 51.09%, whereas the profit margin for the index stands at 18.5%. The US election is on the horizon and if we see a Biden win, with full control of the Senate and House of Representatives. This may mean a more China-friendly trade deal which could be bullish for some aspects of the technology sector; however, increased regulations is a strong caveat. A Democrat win could raise more questions than answers; however, the strong levels on monetary policy stimulus from the Fed and other Central Banks will limit the downside. The end of some unemployment schemes due to the coronavirus will provide headwinds to the electronic products. If the US government and House of Representatives can agree on another pandemic relief package, some of these fears will subside.

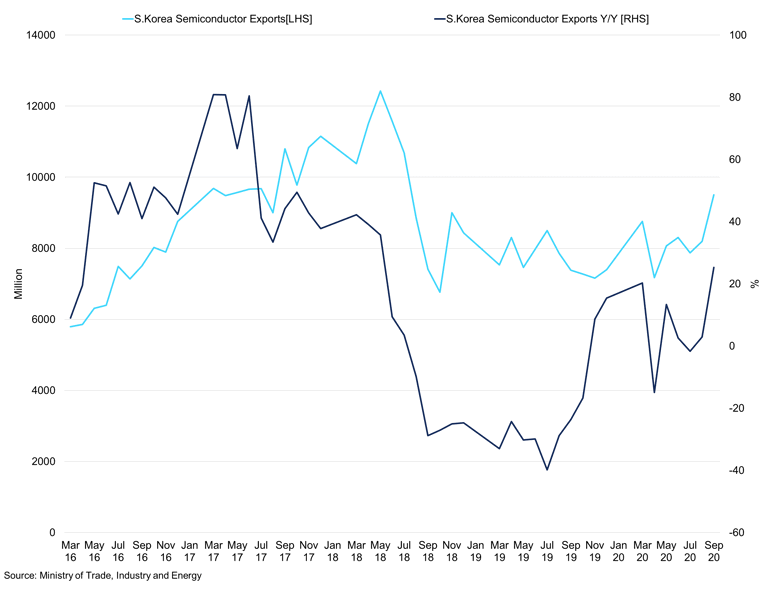

South Korea Semiconductor Exports

South Korea exports are rising, and this is expected to continue in 2021, boosting solder demand.

On a global scale, semiconductor sales have remained strong in recent months and have shown strong resilience this year. After the strong revenue in Q1 due to the shift to a working-from-home economy across the globe, sales of semiconductors in June and July were up 5.1% y/y and 4.9% y/y at $34.5bn and $35.2bn, respectively. This strong year-on-year comparison saw global semiconductor sales improve to $103.6bn up 5.1% y/y from 2019, but down 0.9% Q/Q. From a regional perspective, the sales in the Americas were up 26.3% y/y, China 3.5% y/y, and Asia Pacific/All Other 1.4% according to the World Semiconductor Trade Statistics (WSTS). We continued to see this strength in August with global sales of $36.2bn, up 4.9% y/y with the US once again showing strong signs of growth up 23.6% y/y with China up 3% y/y. We expect this strength to be carried into Q4, which will boost solder demand and therefore tin demand.

When we look at more specific companies for an idea of the strength in the market. Taiwan Semiconductor saw net revenue of $10.38bn in Q2, and guidance for Q3 is expected to be $11.2-11.5bn. Gross margins for the latter quarter are expected to be 50-52%, with operating margins at 39-41%. On a month-on-month breakdown, the company continues to show strength with revenue up double digits every month thing year on a year-on-year basis, in February saw revenue up 53.4% y/y. Figures have slowly normalised with revenue up 40%y/y, 25% y/y, and 15.8%y/y in June, July, and August respectively. Taiwan exports have been strong this year as a result, in August exports reached $31.17bn as we saw frontloading of Huawei purchases before the sales ban, according to the Ministry of Finance. Electronic parts comprised of 40% of total exports at $12.48bn, up 19% y/y. This highlights the strength of the electronic and semiconductor markets. Strong figures from Samsung, where we expect total revenues to be over $50bn, and we could see the company benefit from the sales ban on Huawei. We expect to see server DRAM orders recover from North America in the coming months and into 2021.

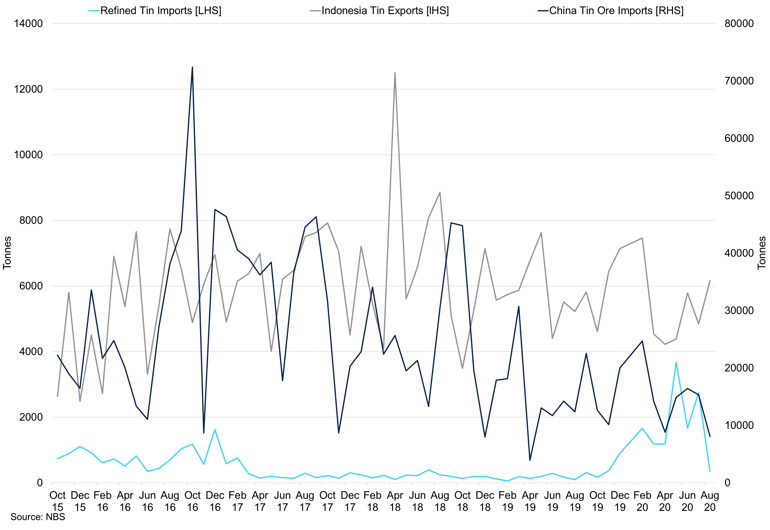

Chinese Refined Tin Imports vs Ore Imports and Indonesia Exports

Refined tin imports into China have improved as demand remains strong for consumer electronics.

Chinese customs data shows the trend of increasing refined tin imports. Refined imports reached 2,750 tonnes in July, but we did see this figure decline in August to 348 tonnes. Ore imports have averaged 14,636 tonnes and data for 2019 is not complete, but the average in 2019 to the end of September was 15,515 tonnes. Despite exchange inventories being relatively high, we could see imports for refined tin and ore increase as consumption improves due to the strength of the consumer electronic goods sector. Smelter output for tin has improved in conjunction with demand, following maintenance during June and July, in line with higher refined imports. We expect smelter output to trend higher in the near term; imports from Myanmar have struggled due to flooding and restrictions at the board due to COVID. Indeed, imports were down 36% y/y in August and 45% m/m at 1,900 tonnes of tin concentrate, following an estimated 3,500 tonnes July from Myanmar. Indonesian exports to China have been hampered by the confirmation from PT Timah in the last few months of lower output, H1 2020 production was 26% lower y/y. Assuming PT Timah reach their target of production cut of 30%, this would mean an annual output reach 45,000 tonnes of refined tin, according to the International Tin Association, PT Timah have a sales target of 55,000 tonnes this year. We know that COVID disruptions have presented downside risk to output across the metals complex this year, helped of course by weaker consumption. With SHFE and LME inventories stand at 8,452 tonnes as of October 7th, imports into China have become more volatile, and this could trigger drawdowns of exchange inventories, and in turn, supporting prices. However, stocks have trended higher since April but remain low historically and as mentioned consumption is strengthening from consumer electronic goods, as well as the growing market of energy storage and batteries.

Tin Commitment of Traders' Report Total Positions

Investment credit firms drastically reduced their net long as investment funds have slowly increased their net long.

Investment Funds Position vs 3-month LME Price

The 3-month price has trended higher as has the investment funds position, reached the highest level since the new report started.

The commitment of traders’ reports for tin show an increase in the net length for the last few weeks, to a net length of 1,556 contracts, up 249% from the beginning of July. The correlation between the change in 3-month price and the change in net funds position has started to push towards 0.2, conversely. The commercial undertaking position has consolidated recently suggesting they may be holding out for higher prices. Given the bullish structure from a demand perspective and supply constraints from Myanmar, and PT Timah we expect the balance to be in a deficit going into next year which is unlikely to such a devasting demand shock. The total position for other financial firms has declined towards the median, which has a z-score of -0.00448, once we normalised for all metals. The current position z-score is 0.1701, down from a previous of 0.4738, for context the highs point is 2.19. This suggests there is a large amount of capacity to the upside for tin; however, investment funds hold the largest long position since the new the LME COT reporting started in 2018.

Zinc

Summary

The recent decline in prices brought the rally into question. Premiums are still low and, but we expect appetite for Zinc to improve following the correction to the downside. Demand ex-China is still lethargic, which continues to cap gains. The LME inventories have been rising, with SHFE stocks falling helping affirm this trend. TCs are falling in conjunction with imports suggesting some moderate tightness, but zinc output in China is still strong. A continuation of this trend would see TCs fall further. We see some downside to the USD in the near term, which could provide support to Zinc, and the US election could present further downside risk to the dollar initially.

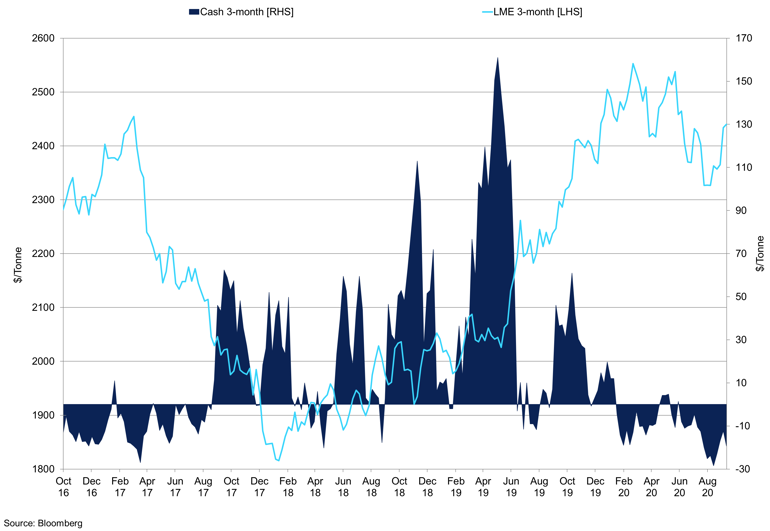

Q3 Review

Zinc prices were well supported in the first half of Q3 as sequential economic data was strong, providing positive sentiment to the market. As we moved through the quarter and economic data, normalised gains were harder to find. The second wave of cases in Europe set in, and the situation in the US is convoluted, and prices failed to maintain their strength, closing the quarter out at $2,403/t, up 17.9%. SHFE futures closed at 19,400RMB/t before the national holiday. Zinc deliverable stocks have declined and since their peak in February are down 71%. LME inventories have seen completely the opposite flows, with stocks up 287% this year and in Q3 we saw inventories rise by 76% to 216,725 tonnes.

Zinc 3-month Price vs Cash to 3-month Spread

The cash to 3-month spread has been in constant contango despite the really in the flat price in recent months.

Outlook

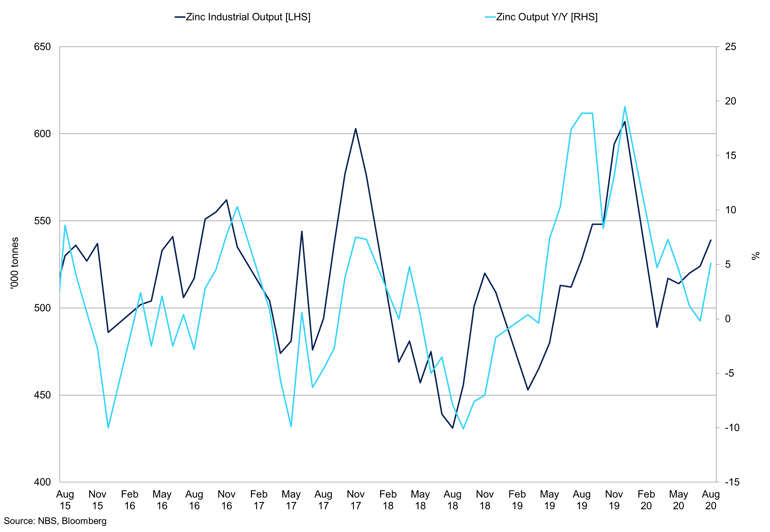

Mine supply has started to improve, helping ease some of the supply chain restrictions which has caused prices to soften recently. Even though mine capacity is not 100% due to restrictions at the mine until there is a vaccine these constraints are likely to continue, however, producers will continue to learn what measures have worked and what doesn’t, helping improve efficiency and productivity. Mines with high levels of mechanisation will be able to get reach higher production levels, which mean large miners are not too far away from predicted production levels for 2020. Global monthly mine output reached 1.105m tonnes with half of this coming from Asia, an improvement from 1.01m tonnes the month prior. Output at this level is near last year’s highs, and we expect output in H2 2020 to offset the losses in H1. CAML has resumed mining at their Sasa mine in North Macedonia; they expect to achieve their ore production guidance of 825,000 and 850,000 tonnes this year. According to the International Lead and Zinc Study group, there was a surplus of Zinc in the H1 2020; this was despite a 7.5% decline in mine supply. We expect the surplus to continue, weighing on metals prices. NBS production data for Zinc declined on a y/y basis in July by 0.3% y/y but recovered in August up 5.1% y/y. Production has been improving to 540,000 in August, and 524,000 tonnes in July. Last year’s high was 604,000 tonnes suggesting there is spare capacity in the market if this capacity is utilised this will put further pressure on prices as social inventories and exchange inventories continue, social inventories of refined Zinc have fallen to 129,500 tonnes, according to SMM. This was due to restocking as exchange prices weakened and some local inventories needed to be replenished.

Zinc Output vs Zinc Output Y/Y

Zinc output has been strong in recent month, but there is still upside capacity.

Chinese imports of zinc ore have risen sharply in recent months above 400,000 to 411,000 in August. We saw imports peak in February at 693,000 tonnes; however, we expect this figure to January and February combined. With production continuing to rise, this could cause imports to increase further, even as Zinc concentrate stocks at Lianyungang to 130,000 tonnes. However, this is marginally above the long-term average of 128,000 tonnes, but more recently, stock levels have been higher. Imports of refined zinc imports have edged higher in August to 46,610 tonnes which is marginally lower and this year’s high, weaker production outside of China and strong output in China will keep imports refined material muted. Unwrought zinc & alloys imports were 52,384 tonnes, another modest improvement. The export market is weak and due to COVID and the second wave will mean a delay to stronger demand.

TCs have started to decline, and this suggests stronger demand from smelters, and we saw some stockpiling of material before the national holiday. Even with mine supply improving, there are fears of tightness in the zinc ore market. TCs for domestic concentrate have fallen to average 5,100RMB/t with the range $4,900/t and $5,300/t, imported TCs have also declined to average $110/t and $100-120/t. Chinese output of zinc concentrate was down 3.1% in September according to SMM, but profitability is strong and concentrate output will attempt to remain high. The softer imports of concentrate and lower domestic production could see TCs continue to weaken as supply becomes tight and output of refined material remains strong. Chinese zinc production recovered in August, and the tightness in concentrate supply may prompt stocks at Lianyungang to decrease back below 100,000 tonnes. The Shanghai bill of lading CIF has improved in recent months but has steadied at $90/t. The zinc ingot grade 1 Shanghai premium has declined to $30/t as of September 29th, down from $200/t on September 16th. The Chinese warrant premium for Zinc in Shanghai bonded warehouse has also started to edge higher trading at $100/t., well below the 5-year average of $135.66/t. With LME prices falling in recent weeks, and premiums lower, this suggests that even though we have seen an improvement in demand in the near term. Global consumption levels are still low on a historical level.

Zinc Operating Rates

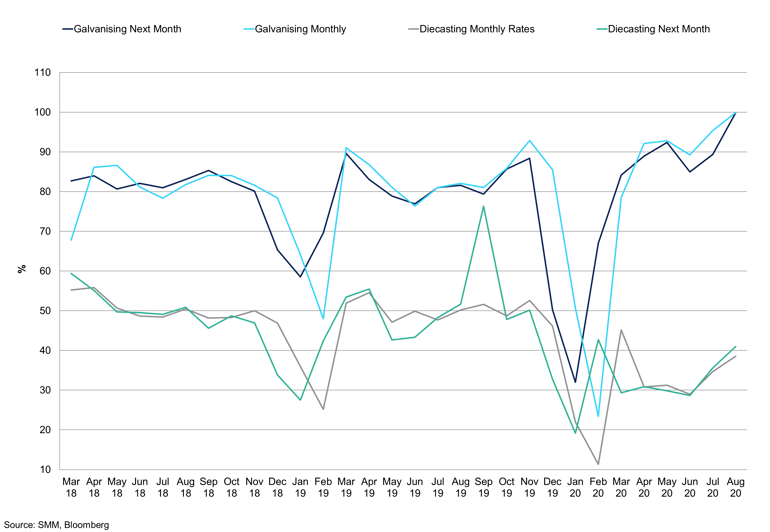

Galvanising rates have been rising, showing strength in the market. However, die casters struggle.