Executive Summary

-

More than 100 central banks have now hiked rates this year, with many promising that more is to come.

-

The extreme heat across the world exacerbates the climate crisis, and the decline in water levels and drought became increasingly likely during summer periods, affecting crop potential.

-

The US economy, in comparison to other countries, is in better shape to take the hit of rising interest rates.

-

We expect the spending power to further diminish in the coming months and spending to contract consistently month-on-month as incomes deteriorate in the face of elevated inflation.

-

However, the question remains whether the central banks can quell inflation without pushing the economy into recession.

-

The risk of a euro-area recession has now reached the highest level since November 2020, with the probability of a technical recession increasing to 60%.

-

Overall, the bloc is preparing for a contingency situation of overall cut-off, but rationing would still need to take place to reserve energy.

-

In China, economic uncertainty prevails, driven in large by the presence of tough lockdowns, meaning businesses are hesitant to borrow and reinvest.

-

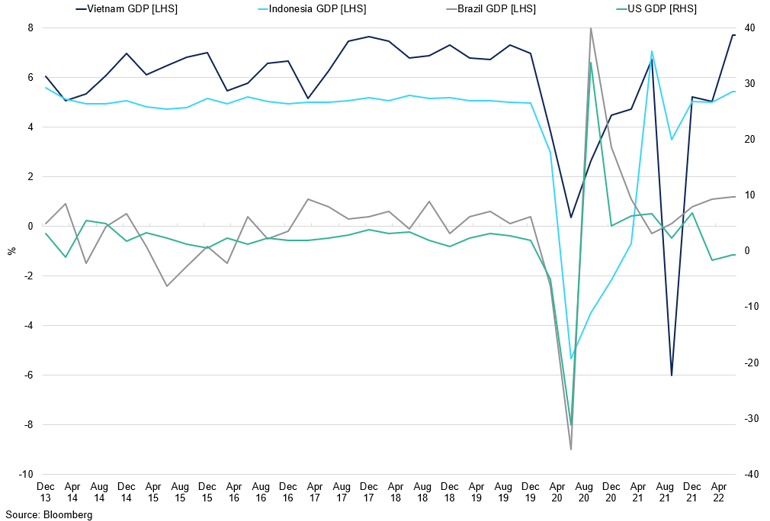

Brazil and the US are feeling the bite of slowing growth, while Indonesia and Vietnam are benefiting from relaxing the lockdown measures so far this year.

-

As a result of a runoff taking place by the end of this month, the gap between two Brazilian presidential candidates should further narrow as cash continues to be distributed to poor households following Bolsonaro’s reform.

-

Companies are posting positive revenues in the quarter, as higher coffee prices are making up for a lower volume of sales.

-

Inflation, as of now, is currently not seeing a measurable reduction in customer spending on coffee products.

-

We see stagnant growth in European coffee consumption due to the cost-of-living crisis, however the U.S. and Southeast Asia demand will edge higher for the 22/23 crop year.

-

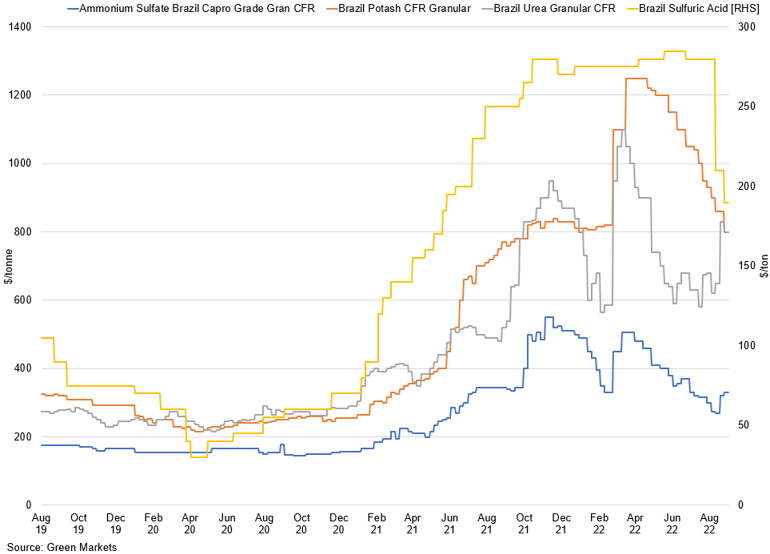

Brazil imports 85% of its fertilizer needs, this has left them vulnerable to higher prices as capacity in Europe is closed due to gas prices, and exports are weaker from producers.

-

Imports from Russia have increased as Brazilian farmers look to apply inputs, prices have moderated in recent months but remain historically high, increasing COP when coupled with the strong dollar.

-

The slowdown in China will present softness to coffee consumption, but the increase in imports into China suggests the market is expecting stronger demand.

-

According to Deloitte, consumers are increasing in complexity asking for better flavours and quality coffee. In our opinion, this will cause a significant rise in the Arabica deficit.

-

For 'Fast Coffee', 80% of the market was from shops near their office, and 80% of consumed coffee and other products such as baked food, juices and tea, and dine-in meals.

-

We see the potential for another substantial deficit for the 22/23 season due to issues in Brazil.

-

There have been some beneficial rains over the main coffee areas recently, but the total rain amount is still low, but the constant nature of the precipitation will help replenish soil moisture.

-

Fertiliser imports into Brazil have started to increase in recent months, reaching 3.367m tons of fertiliser; the price of fertiliser surged higher at the beginning of August to $40,000 FOB, and the price now trades around $23,191 FOB as of August 22nd.

-

Total Conilon shipments this calendar year have been low at 939,334 bags, compared to the Arabica at 19.29m bags. Total shipments this calendar year stand at 22.443m bags; Germany, Belgium, and Italy have received the most coffee, at just over 10m bags.

-

At the time of writing, the rain was sporadic but only covered Parana, Sao Paulo, and areas in the South of Minas. The harvest is finished at the time of writing, and we see this year's crop at 59m bags for the 22/23 crop.

-

This has also delayed the harvest, and with high fertiliser prices, reducing fertiliser application will reduce yields. As a result, we see the crop at 12m bags, but as the cycle continues, we could see this moderated to 11.5m bags.

-

We have been saying for some time that the Vietnamese farmer has started introducing other crops such as pepper and durian fruit into their farms as it has been a lot higher yielding and the Chinese market is on its doorstep; this will continue, and at this time we do not see the crop above 30m bags from a capacity perspective.

-

Honduras diffs are 35 over but as the new crop has not started, we do not expect any coffee to be sold until October with the flat price around 220cts/lb; the market needs to reach 255cts/lb to see Honduras selling.

Our View

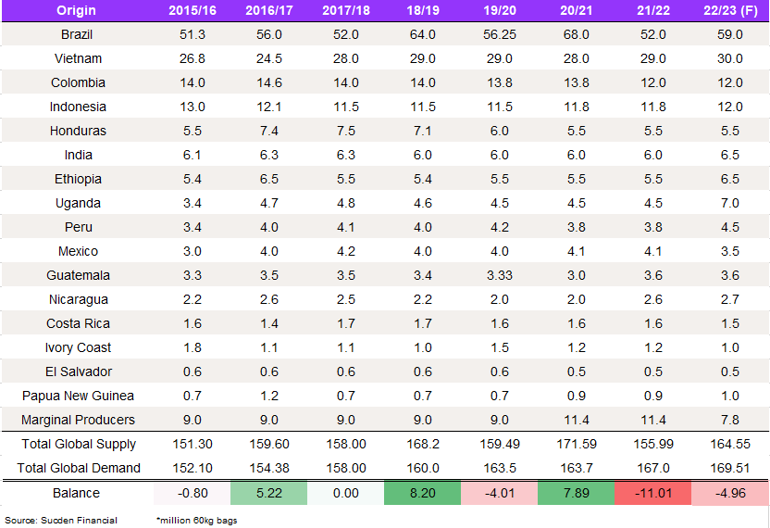

Following a deficit of 11m bags in the 21/22 season, following a revision of the Guatemala crop as exports from this region have been strong; we see another deficit in 22/23 to the tune of 4.96m bags. This is in the Arabica crop, as a result we expect diffs for Colombia, and Central America to remain strong. The flat price needs to rally to see selling from these origins, and with inventories declining steadily we expect considerable demand for what is left. Demand in the U.S., and Asia is steady, and we see consumption increasing by 1.5%, but the European cost-of-living crisis will test the in-elasticity of demand.

The front months are being whipsawed due to the macro and the spreads are at premium, indicating a disjointed market. The spreads show the fundamentals, but we would not want to be short the spread unless you have the product. Indeed, trading conditions remain tricky with the OI and number of traders low, meaning entry and exit of trades is tough as liquidity is thin. Options will become more expensive to hold due to the increase in interest rates, watch rho, and this could cause option liquidity to dry up. However, we remain constructive on the flat price, but the next few weeks and months are key as it is all eyes on Brazil due to the election, and low soil moisture which could reduce Arabica yields and cause larger deficit.

Trading Strategy

- In our view, there are legs in the Arabia rally and due to volatility in the futures contract, margin requirements we favour buying options. KCZ2 220 call as of October 3rd was 12.12cts, selling a 240 call would have 5.33cts. You would pay 6.79cts. Buying the 230 Call as part of the Call spread would be less expensive at around 8.12cts as of October 3rd vs 245 Call which is 4.30cts.

- We still have the index roll, and we expect the trade to still have hedges in December, which could prompt volatility.

- Tenderable parity is considerably above market, but current levels on the spread are tricky to enter the market from an outright perspective. We favour CSOs, and outright to be a delta hedge.

- Robusta is expected to rally, and while we favour owning futures and we favour buying dips to 2150, Vietnam diffs are expected to rally.

- Robusta options are favourably priced, and we favour selling at January $2,100 put at $55 but would buy a January $2,350 which has a premium of $63.

- As with all commodities now, we do not favour being short spreads unless you have the product. This is due liquidity risk, in conjunction with the risk reward at current levels not in your favour unless you have deep pockets.

- Cost of credit and margin requirements have stemmed flow, and we continue to favour the options market, for the flat price and spreads.

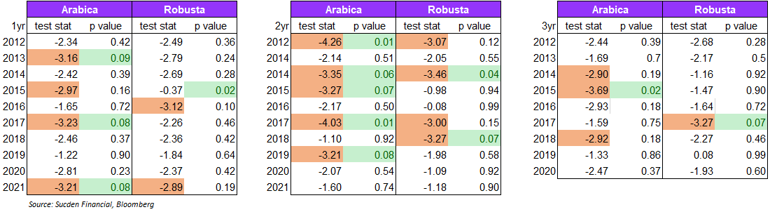

Augmented Dicky-Fuller (ADF)

We have also conducted an augmented Dicky-Fuller (ADF) test on Robusta and Arabica active contract prices to figure out whether coffee contracts have mean-reverting properties. Mean reversion theory suggests that considerable deviations in prices tend to return to their historical mean over time. This means that trading strategies could be built around in such a way that when the prices are strongly above or below the mean, they will return to the longer-term average. We have run the test on 1,2, and 3-year pricing windows. In the table below, the p-value readings below 0.1 suggest that with 90% confidence level, we can conclude that the time series is stationary in nature. Additionally, we back these properties using the t-statistics result. On average, the more negative the t-statistic is, the more likely the series to be strongly mean-reverting, Overall, the contracts across the 2-year window have strong mean reverting properties, with Arabica having more pronounced characteristics than Robusta. The 1-year showing similar but less strong features. Over the 3-year window, on the other hand, results suggests that prices tend to be explosive in nature, and in times of rallies and sell-offs, the trend could continue in that direction in the longer term. Additionally, when looking at the 2-year window, the mean reverting properties did not take hold in 2020 and 2021. Given the consistency of our results across time, we expect to see more mean reverting to take hold this or next year as prices stabilise from a surge in volatility that we have seen since 2020.

ADF Results for Arabica and Robusta Contracts Across Time

Both Arabica and Robusta contracts seem to have strong mean-reverting tendencies for the 2-year timeline duration.

Macro Overview

Global Outlook

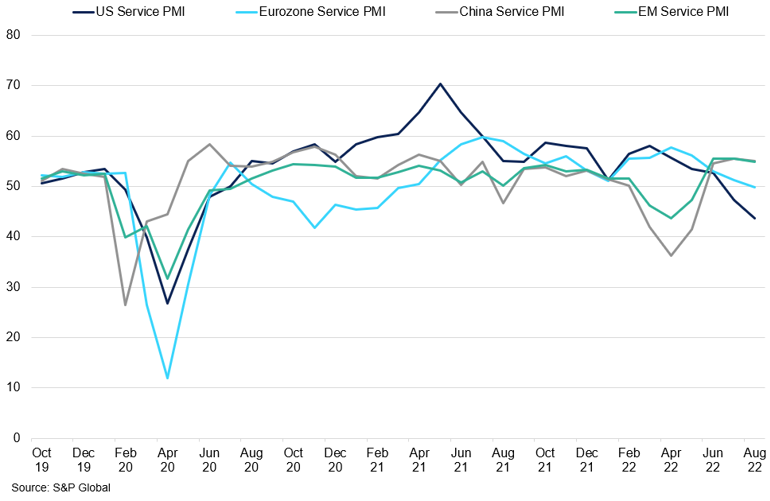

At the beginning of the year, it was unclear how aggressively the central banks would have to respond to a persistent rise in prices. Now, we are at the stage where the Fed hiked by 150bps in two months, and the ECB also increased its rates by 75bps in September. Indeed, the 150bps hike in federal funds rates across two months was the largest single rise in decades. More than 100 central banks have now hiked this year, with many of them promising that more is to come. The divergence between the speed of monetary policy actions a cautionary tale: it’s easy for policymakers to fall behind the curve once inflation takes hold. Meanwhile, the data points to a slowdown in global economic growth, with some countries better positioned for it than others. Manufacturing performance globally continues to grow at a decelerating pace. In almost every major economy, manufacturing PMI fell in July, with output indicating no real growth at all, as new orders and export orders declined. From the service sector, the deceleration of activity is also noticeable.

Global Economies Service PMI Performance

Whilst China and emerging markets are holding up better, both the EU and the US are starting to contract sharply.

In the last two years, a combination of the pandemic and the crisis in Ukraine led to a disruption in the production and distribution of food. This, coupled with rising food prices, is adding to the global food crisis that we have seen build-up strongly, especially in recent months. Bloomberg’s global food price index continues to increase, and food prices are growing rapidly in many regions. Furthermore, the extreme heat across the world exemplifies the climate crisis, and the decline in water levels and drought became increasingly likely. This means more crop failures and shortages of water used for existing food production. As a result of such shortages, we have seen producing countries hold back on their exports as they choose to prioritise domestic consumption, further limiting global production and distribution.

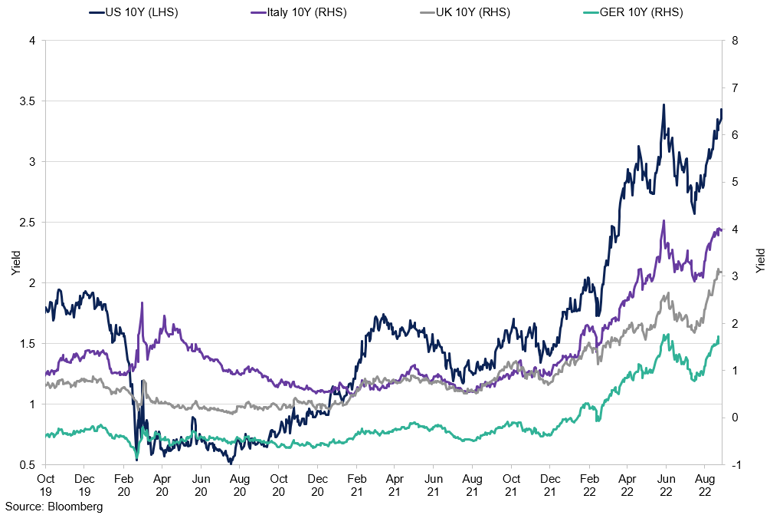

Developed Economies 10-year Bond Yields

Markets are bracing for further hikes in interest rates in Europe and the US as inflationary pressures persist.

US

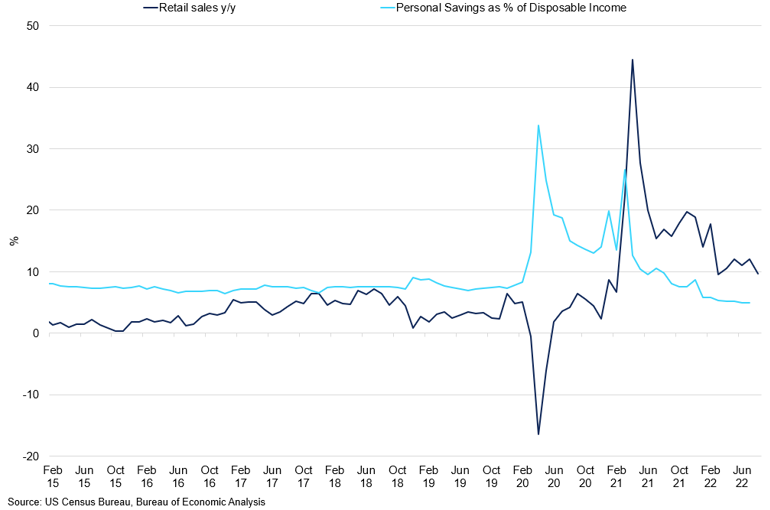

Despite major challenges in recent months, most obviously persistently growing inflation, the US economy, in comparison to other countries, is in better shape to take the hit of rising interest rates. Consumer spending and investment remained positive, suggesting the overall economic performance, albeit slowing, was expansionary. Meanwhile, the real US GDP figure declined at an annualised rate of 0.9% in Q2 2022, putting the economy in a technical recession. However, with the Q1 negative performance mostly attributed to strong export figures and bloating inventories while growth is slowing, the core part of the growth, spending, is not yet contracting. Purchases of goods and services increased by 0.1% in July after a rise of 1.0% a month earlier. Other categories that saw growth included exports, imports, and Federal defence spending. Therefore, spending remains positive, and savings as a percentage of disposable income are diminishing, currently at 5.0%, as consumers choose to continue spending. However, with wages not keeping up with the inflationary figures, the pool of available funds is diminishing, and households are cutting down on some of their purchases. In July, real disposable personal income was up by 0.2% m/m and 2.2% y/y.

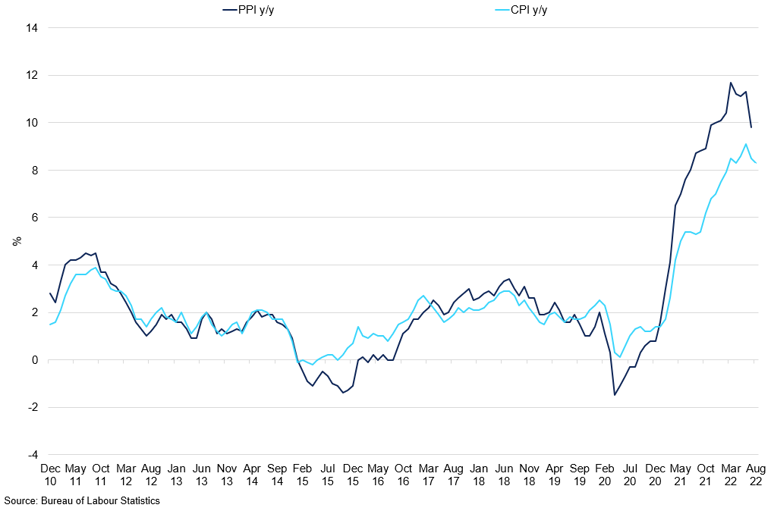

CPI vs PPI Y/Y

Prices are seen softening from recent peaks in the US, although the speed of the decline is below market expectations.

We expect the spending power to further diminish in the coming months and spending to contract consistently month-on-month as incomes deteriorate in the face of elevated inflation. At the same time, we saw data point to softening pricing pressure in August as US CPI showed signs of easing month-on-month as it grew by 8.3% y/y and 0.1% month-on-month. Petrol prices fell by 10.6% m/m and offset increases in food and shelter. The food prices continued to rise, increasing by 0.8% m/m. Therefore, inflation is seen shifting away from volatile components such as energy to more core components of living. And while we expect the CPI reading to soften slightly in the coming months, the core index is set to remain historically high as households feel the bite. US PPI followed the trend after the price fell by 0.5% m/m unexpectedly in July, for the first time in two years, a reflection of softer energy costs. In the longer term, the historically high inflation is to stay at elevated levels, and we do not expect it to fall to the Fed target of 2.0% this or even at the beginning of next year.

Retail Sales Y/Y vs Personal Savings as % of Disposable Income

Retail sales, while softening, remain expansionary as consumers use the remaining covid handouts buffers to fund their purchases.

In July, the Fed hiked by 75bps for the second time in a row, in line with market expectations, pushing the overall Fed funds rate to 2.25-2.50%. Given that the Fed can only tangibly impact core prices, the policymakers are expected to continue hiking this year, with some policymakers seeing interest rates reaching as high as 3.9% by the end of this year. At the time of writing, swaps point to forecasts of a 75bps hike by the Fed in September, and, following the August inflation reading, 75bps in November too. This decision is set to slow down price growth through the reduction in credit market conditions and, in turn, the aggregate demand in the economy. It now has two options: a hard economic landing or high inflation expectations that would keep the prices elevated for a longer period of time. However, the question still remains whether the central bank can quell inflation without pushing the economy into recession. The data shows that while spending and production have softened, employment growth has remained robust and is yet to show signs of a slowdown. US companies increased the jobs 315,000 in August, whilst down from 528,000 a month prior, still a robust performance, despite the labour shortage. This suggests that inflationary pressures might still be a problem as employers pay the premium to attract the labour force. However, the report revealed that wages remained relatively tame, signalling that the tight labour market is not yet generating the kind of wage increases that could lead to a wage-price spiral. However, given our view that elevated inflation is to prevail in the longer term, the wages are set to increase further. The jobs report points to a robust labour market, however, is not a good indicator of recession as it tends to lag other data.

Manufacturing Performance Across Sectors

Manufacturing, a proxy for the country’s production capabilities, points to diminishing demand, while prices are only just starting to ease.

Europe

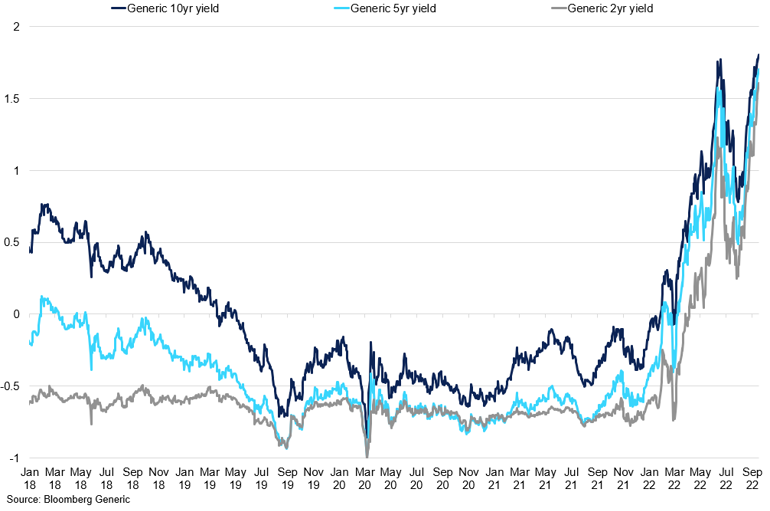

Generic Yields for 2,5, and 10 years

Yields rallied across the curve as inflation continues to beat record highs.

As a result of the escalating energy crisis, coupled with factors such as inflation and a start of tighter monetary policy from the ECB, the outlook for Europe has continued to deteriorate rapidly. However, in Q2 2022, Eurozone real growth increased by 4.0% y/y and 0.7% q/q, driven mostly by the pick-up of tourism activity. This comes at a time when the bloc is preparing for a possible severe shortage of energy in the winter months that would almost surely tip the economy into recession. In Q3, as tourism appetite diminishes, a multitude of factors is set to slow the economic growth significantly. Continued tightening from the ECB, declining real incomes as inflation exceeds wage gains, and a risk of a cut-off from Russian energy exports are set to continue to curb performance. The risk of a euro-area recession has now reached the highest level since November 2020, with the probability of a technical recession increasing to 60%, according to the Bloomberg survey. Meanwhile, Eurozone inflation continued to accelerate in July, growing at 9.1% y/y, another record high. Month on month, the performance accelerated, growing at 0.1%, and core prices inched up to a fresh high of 4.3%. Continued inflation increase is still creating more pressure for the ECB to continue hiking monetary policy. As a result, the ECB will have to make a tough decision on how to address the inflation without damaging too much of the growth while also trying to import gas from other nations. In September, to market surprise, the ECB raised interest rates, by75bps, as inflation continued to surge. The markets are now pricing in another 75bps hike in its next meeting.

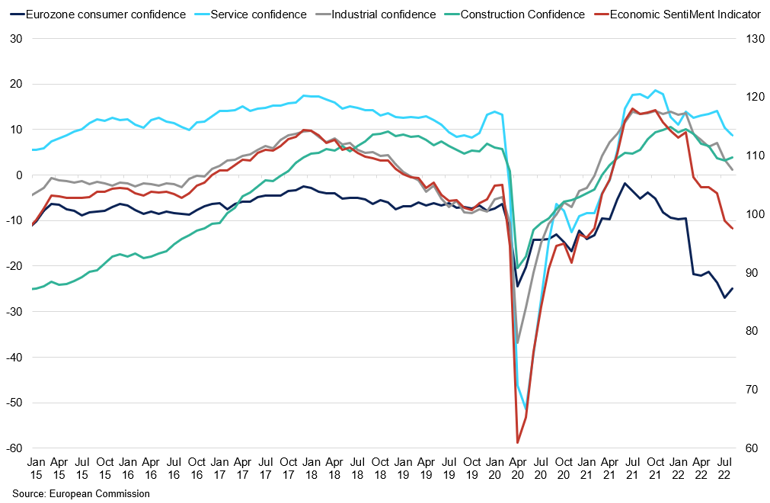

Eurozone Economy Confidence Indicators

Consumer confidence indicators saw some respite in recent months as energy prices eased from their highs.

At the same time, prices of natural gas continue to soar, breaking record highs, as Russian state-run producer Gazprom is adding uncertainty to imports into the bloc. More recently, the company said it would cut Nord Stream 1 deliveries after it chose not to resume supply through key pipeline after maintenance. The cutback, if sustained for a longer period of time, will significantly dampen the EU’s ability to stock up sufficiently by winter, with a current goal of 80% of storage capacity. At the same time, the bloc’s governments pledged to reduce consumption of Russian gas by 15% with exemption for those that heavily rely on its exports. Overall, the bloc is preparing for a contingency situation of overall cut-off, but rationing would still need to take place to reserve energy. We are of the belief that Russia will cut enough shipments to create artificial tightness in the market and keep its revenues elevated and would avoid a full-fledged freeze in the short-term. The IMF stated that a cut of up to 70% in the short term is manageable given the alternative supplies and energy sources and given the reduced demand from previous high prices.

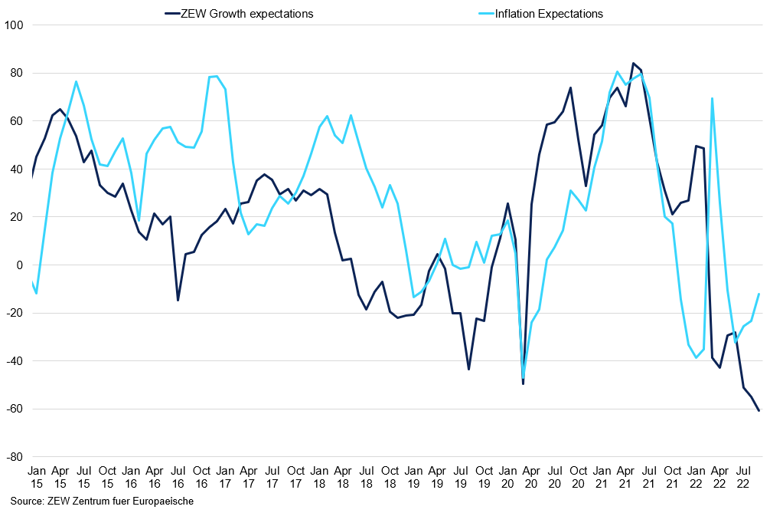

Eurozone Growth and Inflation Expectations

Inflation expectations are on the rise once again, as CPI continues to beat record highs.

China

After a strong start in Q1 2022, the Chinese economy continued to slow in Q2 2022, as it was affected by the impacts of the pandemic, and while we saw a partial reopening of lockdown restrictions, the recovery has been lacklustre, as the government chose to stick to its zero-covid policy and kept reimposing measures on areas where the number of cases is rising. In Q2, the growth figure disappointed to the downside, as the economy expanded by 1.0% y/y, vs 4.8% in the previous quarter. Higher frequency data suggests further declines in July, with retail sales, industrial output, and fixed asset investment all missing expectations by a wide margin. Industrial production increased by 3.8% y/y, down from 3.9% in June and a forecast of 4.3%. Retail sales grew by 2.7% y/y, and fixed-asset investment gained 5.7%. While cases are low in big provinces and areas such as Shanghai, numbers are seen on the rise in the Eastern part of the country, where authorities were quick to stall activity. Truck flows, which is a high-frequency proxy for economic output, were significantly lower in July than at the same time last year.

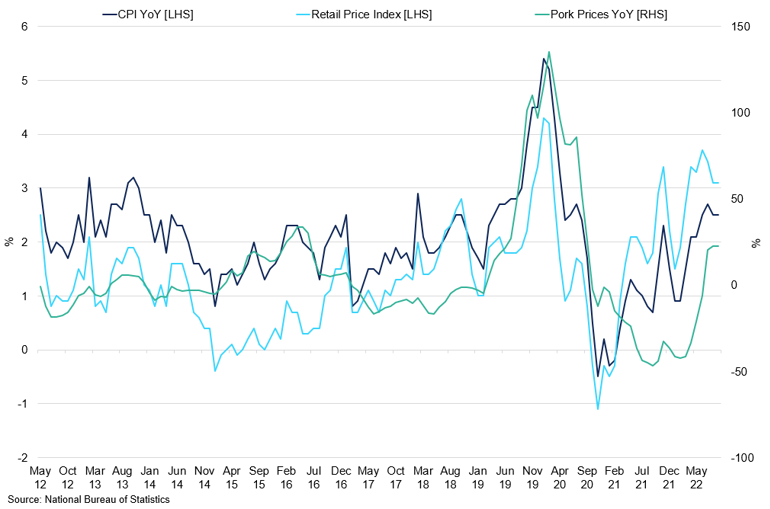

China’s CPI vs Retail Prices Y/Y

Lacklustre domestic demand is helping to keep the demand, and in turn, the pricing pressures subdued.

As a result, the PBOC has repeated its pledge to avoid the massive stimulus and excessive money printing to spur growth, however, it has unexpectedly cut a key policy interest rate, 1yr policy loans, making it the second surprise cut this year, as it lowered the rate by 10bps to 2.75% and withdrawing liquidity from the banking system. Interest rate cuts by the PBOC and the overall decline in growth in July suggests a significant stall in economic performance over the last couple of months. However, bank lending data indicates muted outlook that will not be eradicated by rate cuts alone. Last month, Chinese banks extended $101bn in new loans, less than 25% from the previous month. Yet economic uncertainty, driven in large by the uncertainty of China’s lockdowns, means businesses are hesitant to borrow and reinvest. Moreover, wider monetary policy divergence between the PBOC and other major central banks should continue to diminish the yuan’s value and Chinese debt in the short term.

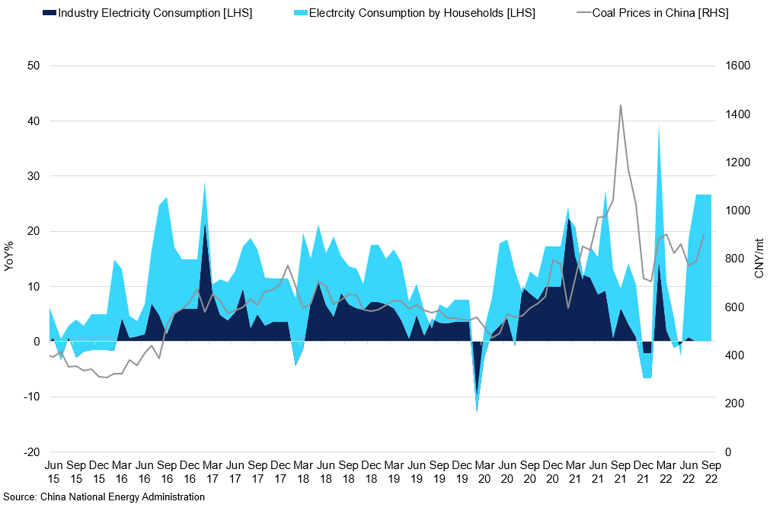

Chinese Energy Conditions

Energy prices are on the rise given the drought in August, and industries are pausing their production to avoid high energy costs.

The cuts have also done little to dispel concerns over the property sector and general recovery from covid. Given the lingering restrictions and fragile economic recovery, we expect the government to continue increasing policy support for the rest of 2022. The infrastructure stimulus is boosting activity, but it is not large enough to offset the hit felt by the property sector. Home sales continue to decline, falling by 28.6% y/y in July, and property investment shrank 12.3% over the same period, according to the National Bureau of Statistics. We believe that as global trade flows weaken and inflation persist, this should continue to dampen the region’s economic growth in the second half of 2022, although a general trend of recovery from tough lockdown restrictions at the beginning of the year will be maintained.

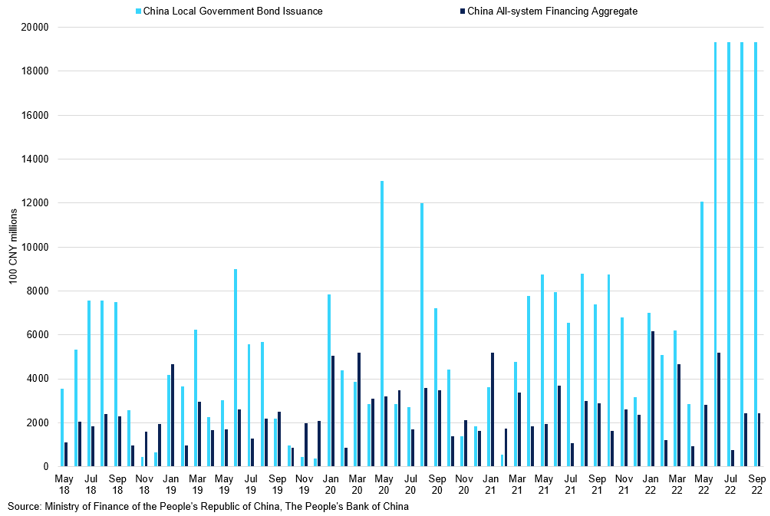

China Local Gov’t Bond Issuance vs All-system Financing Aggregate

Chinese government is providing ample liquidity into the market to support the economy.

Brazil

Brazilian economic activity expanded by more than forecast in Q2, showing resilience to diminished purchasing power and an aggressive monetary policy tightening that so far has been unable to contain inflationary expectations. The figure grew by 0.69% m/m and 3.09% y/y, as the economy bounced back slightly from the latest wave of covid cases. Given better-than-expected growth, swap contracts for January 2023 have increased by 1.5bps as a result, as markets now expect even further tightening from the central bank. Unemployment surprised on the downside as the figure reached 9.87%, the 2016 low. Retail sales decline by 0.4% y/y in July, the lowest level since January.

US and Producing Countries’ GDP Growth

Brazil and the US are feeling the bite of slowing growth, while Indonesia and Vietnam are benefiting from relaxing the lockdown measures this year.

Driven by a strong rebound in the services sector, Brazil’s economy is now forecast to grow by 1.7% this year, a substantial improvement from January when banks predicted a recession. After strong June performance spurred by the full reopening following Covid-19 restrictions, services sector activity has come down from the highs in July due to softer underlying demand, according to S&P Global. Price growth cooled, as they fell by 0.68%, suggesting the petrol tax cut benefitted the consumers. Yet, at 11.4% year-on-year, inflation remains high, and the relief may be temporary. Indeed, despite largely successful government efforts to tamp down the cost of fuel through tax cuts, food prices have also continued to rise. The price of staple products such as carrots and potatoes has increased by 70%, while milk has increased more than 30% in the last year. To further support the households, the government passed a $7.7bn spending package, which will increase monthly cash payments to Brazil’s poorest by 50% to BRL600 until the end of the year. Though central bankers said they would consider a smaller interest rate boost in September, markets believe the tightening is over. The key Selic rate is expected to remain unchanged at 13.75% in 2022 and drop to 11% by December of 2023.

Brazil Retail Sales & Service Sector

Both sectors are seen on decline as economic outlook deteriorates with rising inflation.

As the country geared up for elections this month, the economic performance has dominated the national debate. Lula struggled to gain the majority, meaning the runoff will take place by the end of the month. As a result, the gap between two candidates should further narrow as cash continues to be distributed to poor households following Bolsonaro’s reform, boosting his approval rating. However, double-digit inflation and borrowing costs are dampening the outlook for Latin America’s largest economy. At the same time, additional social spending is elevating inflation expectations above the target rate through 2024. The central bank estimates inflation to increase by 5.38% in 2023 and 3.41% in 2024. More emphasis will be placed on 2024 figures as recent tax cuts and fiscal stimulus has likely dampened the inflation figure in the near term.

Vietnam

Vietnam’s economy expanded by 7.7% in Q2 2022 as consumers satisfied pent-up demand and foreign tourism picked up. The economy also benefited from a $15bn fiscal stimulus and an easier monetary policy from the State Bank of Vietnam. Exports moderated in July, growing by 8.9% y/y, down from the 20% y/y growth seen in June. However, Vietnam remains the beneficiary of investment inflows redirected from policy uncertainty in China. In this case, Vietnam can gain additional benefits from the shift of investment capital. In the longer term, the country is expected to continue with robust FDI investment for the rest of 2022 and 2023.

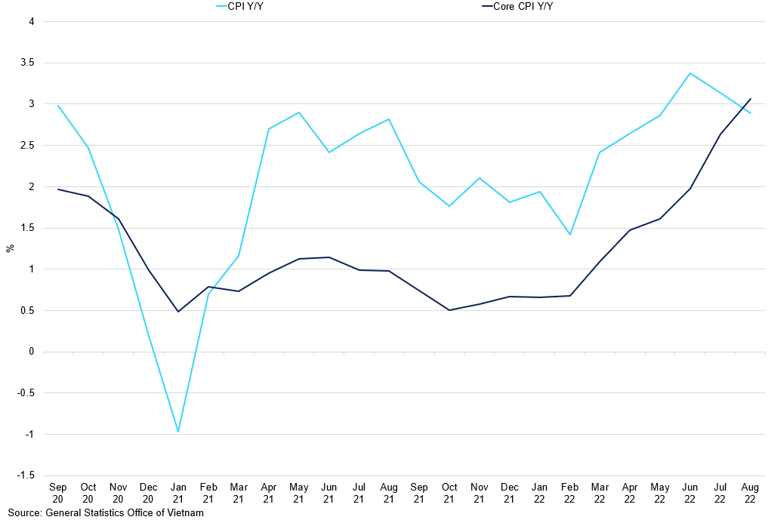

CPI Y/Y vs Core CPI Y/Y

Core prices are taking on the brunt of the price increases.

Inflation slowed by more than expected in July, growing by 3.14% y/y, allowing room for the central bank to stay accommodative to support economic recovery. The gains are well below the government-set 4.0% target and follow fuel tax cuts to ease price pressures. July core inflation increased by 2.63% y/y and 0.58% m/m and is expected to begin decelerating month-on-month, allowing the policymakers to focus on slowing growth as headline price pressures cool. The labour market is also not feeling the same strain of worker shortages that other developed nations are, which will also ease pressure on price-wage spiral. Unemployment level remains low, at 2.39% in H1 2022 and the total labour force totals 50.3m people.

According to the WorldBank, Vietnam’s economic growth is forecast to grow by 7.5% in 2022, with economic recovery accelerating in the second half of the year on the back of resilient manufacturing and service sectors. According to S&P Global, Vietnam’s manufacturing performance remained expansionary so far in Q3 with some signs of softening demand. Inflation is projected to average at 3.8%. However, this positive outlook is subject to heightened risks, such as growth slowdown or stagflation in main export markets, continued disruption of global supply chains, or new spikes of covid-19 waves. A combination of factors ranging from Covid-19 spread to a slowdown in global economic trade could impact the country’s performance in H2 2022. While the country will continue to face many challenges, including high energy prices and supply chain disruptions, its economy remains resilient in the longer term.

Indonesia

Indonesian economy performed better than expected in Q2 2022, growing by 5.44% y/y, led by a boom in commodity-led exports and robust domestic spending data. The figure is the fastest increase in a year and is up from Q1 growth of 3.72%. Reopening from lockdown measures spurred mobility and travel, and private consumption, which makes up more than 50% of the country’s GDP, grew by 5.51% y/y. At the same time, exports jumped by 19.74% as the world’s largest palm oil exporter enjoyed a windfall from rising commodity exports. On the other hand, retail sales grew just 4.0% in June, against the expected 15.0%, and retailers expect inflation to worsen over the next couple of quarters and are already seeing increasing prices for the products.

Indonesia’s Growth Per Quarter

Indonesian economy has benefitted so far from the relaxation of lockdown measures in the second quarter of the year.

As a result, inflation grew by 5.0% y/y in July, breaching the central bank’s target of 2.0-4.0% and reaching a 7-year high. While prices continue to grow year-on-year, in comparison to other Southeast Asian economies, the softer inflation and robust growth give the central bank more room to hike rates. However, the Indonesian central bank has stood out by keeping interest rates at record lows, stating that the spike in prices is mostly supply-driven and, therefore, short-lived. However, despite that, the country’s central bank unexpectedly raised the borrowing rate for the first time since 2018 to 3.75%, as mounting inflationary risks urged the bank to begin the tightening cycle. Instead, the central bank is shifting its attention to measures that could control inflation at its source, through local farms and markets. The central bank wants to increase the plantation of goods that face the fastest price increases, as well as establish better routes for its distribution. According to government data, inflation is expected to ease to 3.3% in 2023 from the government’s projected range of 4.0-4.8%.

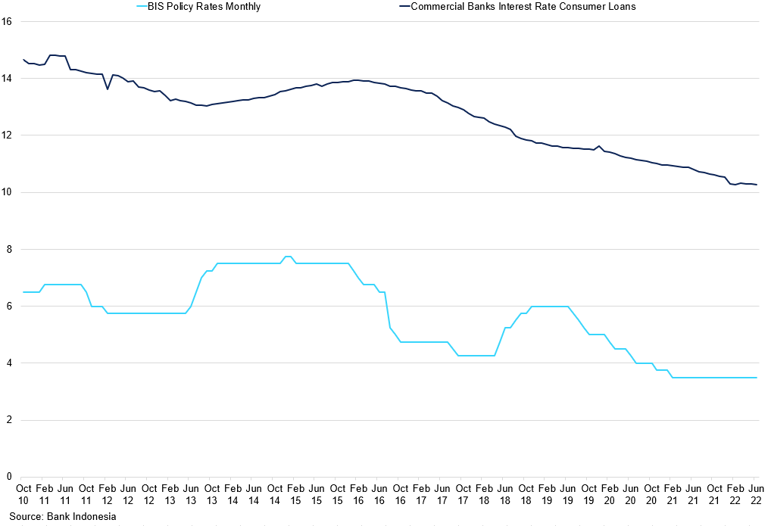

Indonesia’s BIS Policy Rate and the Commercial Rates Charged for Consumer Loans

Commercial rate continues to decline despite the pause that we have seen in the official central bank rate.

Still, policymakers may tread with caution due to global recession risks sparked by an aggressive monetary tightening in the US and stumbling growth in China. Bank Indonesia recently projected that GDP growth could tilt below the midpoint of its 4.5%-5.3% target range this year amid uncertainty about the global outlook. Despite already doubling this year, the subsidy bill will continue to swell next year to maintain the prices for fuel and electricity. At the same time, the Indonesian government is seeking to narrow the next year’s budget deficit to below 3% of GDP for the first time since 2019 as it balances the need to rein in the fiscal sector while supporting growth. The fiscal gap is projected to drop to 2.85% of GDP in 2023 from an estimated shortfall equivalent to 3.92% of GDP in 2022, even as the government increases the allocation for subsidies by 4.4% to 297.2 trillion rupiahs.

Corporate Earnings

Starbucks

Starbucks held up a positive performance in Q3 (13-week period ending on July 3rd). Global comparable store sales increased by 3.0%, with North America up by 9.0%, whereas international fell by 18.0%. Out of the international sector, China's growth decreased by 44%. The beverage sector growth remains robust overall, increasing 9% in the quarter. Across all categories, espresso, brewed coffee, and refreshers all saw strong double-digit growth. The average ticket -- or cost per order -- rose 6%, but comparable transactions fell 3%. This shows that higher prices are making up for a lower volume of sales. However, operating margin fell from 19.9% to 15.9%, primarily driven by inflationary pressures, investments in labour, as well as sales, and deleverage related to COVID-19 restrictions in China, which was partially offset by pricing in North America.

Regionally, North America's operating margin contracted to 22.0%, primarily driven by higher commodity and supply chain costs due to inflationary pressures and investments in labour. This contraction was partially offset by pricing. Cold drinks continue to drive customer demand, with them now accounting for 75% of the total beverage sales in US company-operated stores. US company-operated stores delivered record average weekly sales, with $410 million sales per week. Inflation, as of now, is currently not seeing a measurable reduction in customer spending or evidence of customers trading down. So, the region continues to spend despite elevated inflationary pressures. The company has faced criticism from union organisers as they claim that Starbuck has increasingly turned to anti-union tactics, like closing stores and firing workers.

In China, however, covid restrictions hampered the region's performance. On-and-off pandemic rules have restricted mobility in major cities, and comparable sales in the country fell 44% during the quarter. In June, given the relaxation of lockdown conditions, the company announced that indoor dining services had resumed at most Starbucks locations across Shanghai. A cold beverage is also now becoming popular in China. Iced Shaken Espresso, introduced in June, has already become one of our best-selling iced coffee beverages among Gen Z customers driving both sales and incremental traffic.

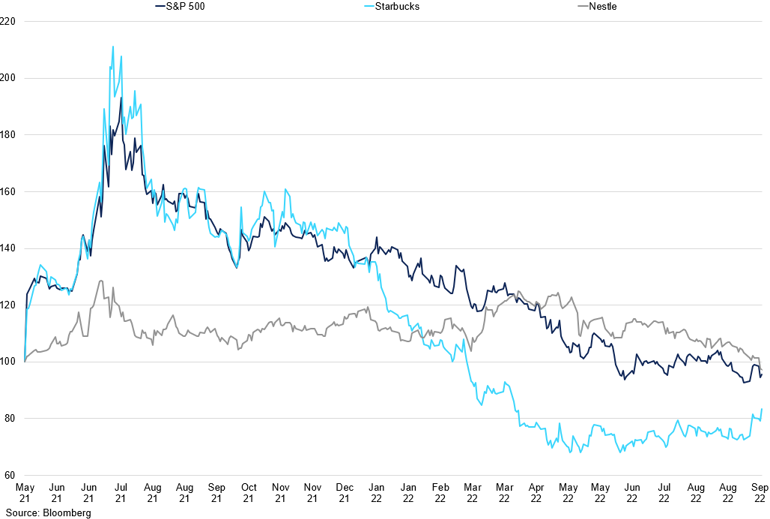

Starbucks vs Nestle vs S&P 500 Performance

Starbucks shares struggled to hold up since February, while Nestle continues to closely trace the S&P 500 index.

JDE Peet's

JDE Peet's organic sales increased by 15.7%, driven by a 15.9% price and stable volume in Q2. In-Home sales increased by 12.0%, and sales in Away-from-Home increased by 33.7% on an organic basis. As a result of persistent inflation, many coffee sellers pushed prices higher. JDE Peet reported that cost inflation increased by 36%, with green coffee (70%), ocean freight (80%), energy (100%), and pack materials (20%) all higher year on year. Despite that, the company only increased prices by 1 euro-cent per cup on average while still managing to report double-digit growth during the quarter.

The company expects the business conditions to remain volatile for the remainder of 2022 as input costs rise, geopolitical unrest and certain effects of the pandemic persist. However, the company still expects to deliver double-digit organic sales growth, attributed to disciplined pricing, while aiming for a stable level of gross profit and expects to deliver a free cash flow of at least EUR 1 billion.

In Europe, organic growth of 5.3% was driven by an increase in the price of 12.7% and a decrease in volume of 7.4%, given the high base in 2021 when lockdown measures were lifted, shifting the consumption back to the out-of-home sector. In the US, coffee retail stores delivered mid-teens growth. Growth in China remained robust, despite lockdown challenges, with the number of retail stores increasing at a double-digit rate, from 70 in December to 81.

Soluble, however, remains a strong performer. By segment, the biggest H2 performance was seen in CPG Larmea, which is Jacobs soluble. In a conference call, the company stated that drinking one less caffe latte (EUR4) would offset the full-year inflation of in-home coffee products on average. This is why the soluble category has been showing resilience historically at times of choice for the consumer, and the volume/mix growth in H1 remained stable year on year.

Nestle

Nestle's organic growth was up by 8.1% in Q2, with RIG of 1.7% and pricing of 6.5%. Pricing was the biggest contributor to growth in the first half of the year. Organic growth was at 6.7% in H1 2022, vs 7.3% same time last year, but higher than 6.3% in H2 2020.

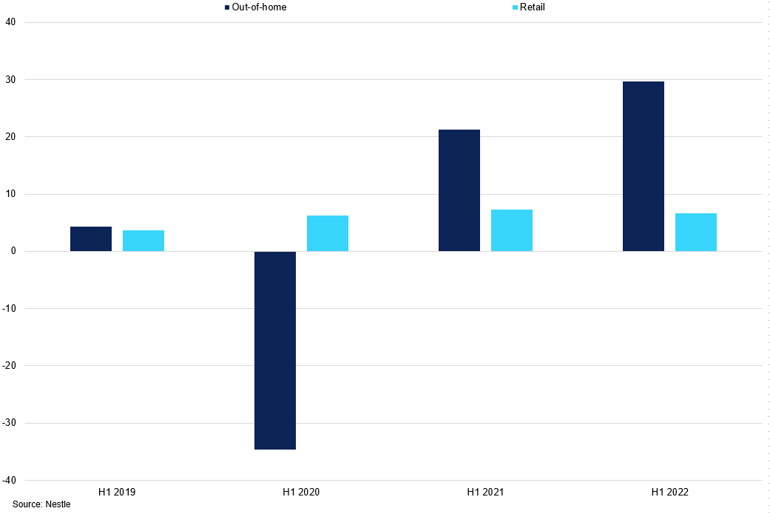

Out-of-home consumption continued to grow and stood at 29.6%, up from 21.3% in H1 2021. The company implemented price increases but still said that they managed the inflationary pressures through disciplined cost control and operational efficiencies.

Nestle Organic Sales Growth by Segment

Nestle continues to see an improvement in out-of-home region as lockdown restrictions are slowly removed worldwide.

Coffee sales saw growth at a high single-digit rate, with solid growth across geographies, supported by a strong recovery of out-of-home segments. In North America, the beverages category, Starbucks and Nescafé products, saw mid-single-digit growth, following a high comparison base in 2021. In Europe, coffee posted low single-digit growth, led by Nescafé soluble. Starbucks by Nespresso and other Nespresso capsules saw their market share increase in the retail segment. In China, coffee posted mid-single-digit growth, with Starbucks products and Nescafé soluble coffee seeing continued momentum.

For the rest of the year, the company expects organic sales growth between 7% and 8%, boosted by inflation. In the meantime, it pushed another round of price increases on consumers during Q2, as input costs rose at a rapid pace. North American consumers were hit with the most significant increase in pricing, with 9.8% in H1 2022, while prices in Europe rose by 5.0%. Despite rising prices, Nestle said volumes remained "resilient." Nestle indicated, however, that its profitability could decline for a second year, with an underlying operating profit margin will be about 17%. In 2021 it was 17.4%.

Fertiliser

Brazil Fertilizer Prices

Fertilizer prices have moderated this year but remain historically high. This increases the cost of production for farmers.

The fertiliser market remains tight as weather events continue to test food security, high power costs, and geo-political tensions are causing fertiliser availability to decline. The reduced nitrogen availability has compounded this tightness; shutdowns in European capacity due to power and gas prices have led to reduced urea supply. According to CRU, Europe has lost around 33% of its nitrogen fertiliser operations due to higher gas prices, and Yara has reduced output to 35%, equating to 3.1m tons of ammonia and 4m tons of finished products. Gas prices in Europe will remain high due to Nord Stream pipelines from Russia being cut off. Global prices of nitrogen products are high, with ammonia, urea ammonium nitrate (UAN) and ammonium sulphate firming.

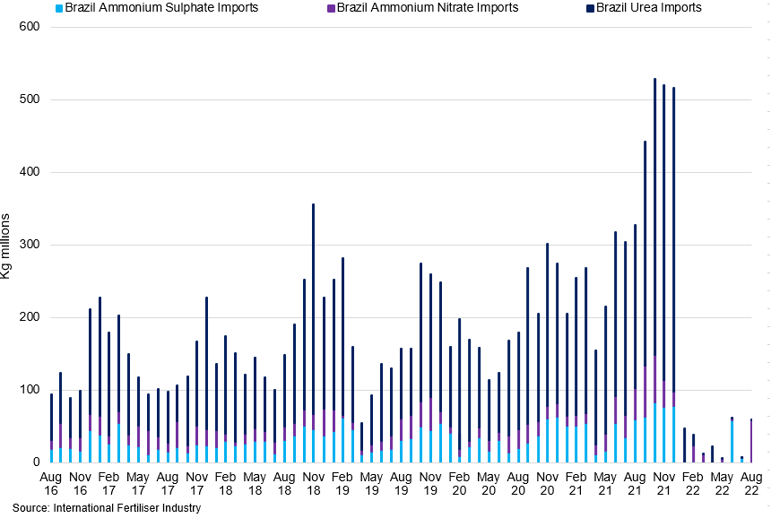

Brazil Sulfuric acid CFR prices have declined significantly to $190/t, compared to Urea prices which have surged higher in recent weeks to $800/t, however in the week to September 9th, prices edged lower as market uncertainty took hold and the range widened. Imports into Brazil slowed in August, with arrivals exceeding last year by 9.4%. Potash purchases are up 1.6m or 20.5% Y/Y. Year to date, urea imports are down 213,000 to 4.6% as demand increases; we expect imports to increase in Brazil. Ammonium sulphate imports had declined from June, when they reached 58.680m kgs, to 64 kg in August, according to Ministerio da Industria e do Comerica Exterior. Brazil imports 85% of its fertiliser needs, and weekly fertiliser imports in USD have increased in value in the last few weeks to $23,190; this is down from the high in June at $40,000. The import tonnage is due to reducing the flow of some products such as Urea and ammonium sulphate. According to Bloomberg Intelligence, Brazil imports from Russia are down year-on-year by 9%, which suggests vessel data shows over 1m tonnes of the product will arrive in August and September, shrinking the deficit. From January to September, Urea imports into Brazil stand at 4.92m tonnes according to the World Shipping Alliance, down from 5.37m tonnes; up to the end of July, imports had been 4.613m tonnes. Brazilian farmers were given a respite as the nitrogen ratio has fallen to July 2021, and demand is set to increase in Q4 and Q1. Contra to the above, Yara has indicated that through to July, imports of crop nutrients such as potash and NPK increased 15.5% Y/Y. Brazil needs to invest in more infrastructure, such as warehouses for storage, as most of them are private; the rise of 50% in imports continues to pressure the infrastructure.

Brazil Fertilizer Input Imports

Imports in recent months have moderated for fertilizer inputs.

Climate change has exemplified this issue, with global droughts impacting yields and production, prompting producers to consume more fertiliser to maintain yields. While in the long run, this degrades soil productivity, it may help farmers maintain production levels. However, dryness and droughts are something farmers will have to contend with in the long run due to climate change, India has experienced this issue for some time, and according to the Composite Water Management Index (CWMI) and NITI Aayong-a, approximately 600m Indians will face high-to-extreme water stress. Water scarcity is compounded in India as 60% of its agriculture is irrigated. Water risk continues to threaten the commodity complex, and volatile weather conditions will continue to challenge farmers and with the temperatures warming the probability of dryness and low soil moisture rises.

Supply & Demand

Demand

As things stand, we see a 1.5% increase in global demand for 22/23, with consumption reaching 169.51m bags, up from 167.5m bags. For the coffee season, 21/22 imports into consuming countries have increased from 86.635m bags to 91.266m bags. For May 2022, total imports were 12.028m bags, up from 11.10m bags, and the U.S. imports were down Y/Y to 2.39m bags, from 3.757m bags. However, imports from October to May for the U.S. at 19.959m bags, up from 18.780m bags for the previous year.

According to GlobalData, in Q1 sales in coffee and tea shops were down 1%, while the cost of products increased 10.5%, while this data was before the cost-of-living crisis really took hold it indicates the resilience of the U.S. consumer. A Q3 2022 survey by GlobalData shows that 24% of consumers visited coffee or tea shops. U.S. personal consumption expenditure has been steadily declining but stood at 4.6% Y/Y in July, below February data of 5.316% and still historically very high. The high inflationary environment is proving to be upwardly sticky, and as a result, the savings ratio in the U.S. has declined sharply to 5%, the lowest level since 2009. Sales will plateau for out-of-home consumption, with consumers continuing to prefer in-home consumption. Reports from corporate earnings indicate that sales volumes are suffering, but margins remain steady due to higher prices. U.S. retail sales in food and beverage stores continued to climb despite the inflationary conditions and were $81.44bn in July, according to the U.S. Census Bureau; E-commerce sales of food and beverages had continued to edge lower and stand at $6.88bn in June 2022, the record high was in December 2020 when it reached $7.88bn. While this data is not coffee specific, it highlights that consumers in the U.S. are still spending; the caveat is that prices are higher, so the total value of sales will still be around record highs despite the lower volumes. However, with imports into the U.S. strong, this indicates robust and resilient consumption.

A large proportion of the increase came from the European Union as consumption so far has increased from 52m bags to 55.5m bags, but for the next 12 months, we see stagnant growth from the bloc due to the higher cost of living. According to IRI, retail sales of roasted coffee were €700m, down by 5.8% in volume terms but up 1.4% in value. Pods in Italy saw considerable growth at 27.6%in value and 8.5% in volume terms, indicating the rise of in-home consumption throughout COVID. Through the retail channels, sales have declined from hypermarkets by -3.9% and supermarkets by -5.7% to independents, which is down 5.2%; in addition, moka, capsules, espresso, beans, and filters were down in volume terms. JDE Peet's 3-5% organic volume target relies on the inelasticity of coffee, and with Europe representing 51% of their revenue, this will be tested.

Keurig Dr Pepper's new coffee machine with smart technology allows consumers to replicate buying a coffee from a shop. They have indicated that consumers do not just want a black cup of coffee, and the new machine allows a broader experience. The K-café Smart technology BrewID gives the consumer a review of different recipes best suited to the pod in the machine. The Barista mode in the machine takes the consumer through a step-by-step guide with demonstrations for making drinks. There are 70 different types to choose from, allowing the consumer a better experience. This can provide a better in-home consumption experience for consumers who work-from-home and, in the long run, offer a cheaper alternative than coffee shops. Keurig indicates that over 35m households use their brewing system and target an extra 2 million yearly.

China's slowdown has heavily impacted the economy, which will have a ripple effect on coffee demand, which is not very sophisticated. This is evidenced by the decline in sales reported by corporates which have declined significantly. The younger generations are the largest consumers, and youth unemployment was 19.9% in July, up from 19.3% in June. In conjunction with their COVID policy, this has meant sales are likely to suffer. Imports increased from the February figure of 3,525 tonnes and stood at 12,891 in July. The record monthly imports were a spike in 2012 to 15,141 tonnes, but the consistently higher imports for China could indicate that consumption is starting to pick up, and while we do not expect their COVID policy to change after the party congress, if the imports continue to remain high, we could see sales improve. June exports of roasted coffee to China from Japan were 73 tonnes, soluble coffee exports were 229 tonnes, with other coffee exports at 181 tonnes.

According to Deloitte, coffee consumption will continue to increase as more citizens have a better education and their disposable income increases, with 10.7m students graduating. Deloitte has indicated that Latte will continue to be the most consumed drink, but brewed coffee will continue to increase as consumers start to prefer coffee which retains flavour. This will continue in the long term as consumers' preferences become sophisticated. We expect independent coffee shops to reach 81% of the market by 2023, totalling 123,884, up from 108,467 in 2020, a CAGR of 5%. The report from Deloitte highlighted the most common reasons consumers changed their freshly brewed coffee brands, 57% will vary due to the emergence of a brand that better meets their costs, 43% which can meet their taste demands, and 41% which meets their convenience. For 'Fast Coffee', 80% of the market was from shops near their office, and 80% of consumed coffee and other products such as baked food, juices and tea, and dine-in meals. The trend suggests that demand for Arabicas from China will only increase as consumption patterns become sophisticated. This will exaggerate the deficit in arabica coffee in the long run, and the Brazil crop would have been above 65m bags consistently to enable this, as well as Colombia producing more than 14m bags. Coffee shops in China would benefit from focusing on the quality of coffee and other drinks without investing too much in baked goods. Young consumers prefer coffee from independent boutique cafes, and 27% of consumers who have drunk coffee for more than 5 years are pursuing better-tasting products, compared to 13% for those drinking less than 1-year.

S&D Balance

We see the potential for another substantial deficit for the 22/23 season due to issues in Brazil. Good flowering in sul de minas last month was premature; rain is needed to get flowering to set and hold. There have been some beneficial rains over the main coffee areas recently but the total rain amount is still low but the constant nature of the precipitation will help replenish soil moisture. While more rains are forecast next week, a period of further dryness will put more stress on the trees, this is not bullish yet, but it is undoubtedly a flag to the crop number and yield. We do not expect a record crop currently, as soil moisture is still low, and in recent years, we have seen dryness in September and October. At the time of writing, the rain was sporadic but only covered Parana, Sao Paulo, and areas in the South of Minas. The harvest is finished at the time of writing, and we see this year's crop at 59m bags for the 22/23 crop. This is comprised of a split of 38m bags Arabica and 21m bags Conilon, coffee. This is lower than the previous estimates, but this highlights the problems in Brazil, which we do not think is priced into the terminal. Producer stocks are either low or sold, exports from Brazil have been strong in recent months, and we expect this will mean that public warehouses have low stock levels. As a result, if our Arabica number is correct, diffs will remain strong, and the flat price will have to rally, along with the spreads for the coffee to be shipped. Colombian and Honduran crops are also lower, and the deficit will be in Arabica.

The market will increase Robusta blends, and we see value in Vietnam diffs at current levels. However, we expect roasters in Europe to be impacted by power and energy costs; this may prompt out-of-hours roasting, with some reduced capacity to sell power on the spot market back to the grid. The cost-of-living crisis will undoubtedly test the inelasticity of demand for coffee. The shift towards Robusta blends could help the price of coffee; this, in conjunction with a shift to at-home consumption, will allow consumers to demand coffee. However, we believe that some households will not be able to afford heating and food this winter unless the government steps in. We have seen European governments act, but the U.K. is yet to do so. New Prime Minister Liz Truss has presented a support package that will cap energy prices, but the year-on-year increase will be considerably higher, household finances will be impacted, but only a small sector of society may reduce their coffee demand. This will not define the whole market, but we expect European demand to stagnate. We adopt the 80/20 rule and expect slower growth for demand.

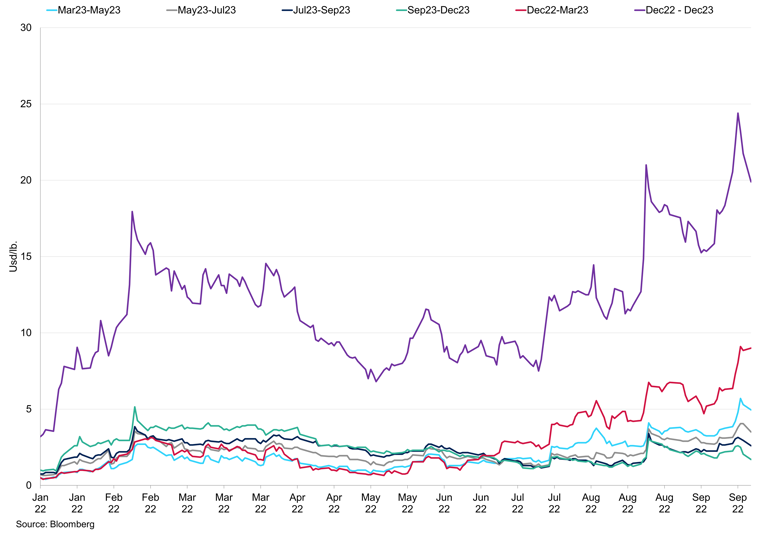

Robusta Calendar Spreads

Near dated calendar spreads outline the tightness in the market, and we expect premiums down the curve to persist in the near term.

Accordingly, we see consumption rising by 1.5%, causing demand to rise to 169.505m bags, up from 167m bags. Most of this growth still comes from Southeast Asia and some moderate growth in the U.S. we expect growth in Europe to be limited due to the cost-of-living crisis and economic woes. As this stand, we see a total supply of 164.15m bags with a consumption of 169.505m bags, leaving a significant deficit of 5.35m bags. With inventory at 635,196 at the time of writing, we expect ECF, GCA, and JCA stocks to be depleted sharply, as well as any inventory off-exchange. The flight price needs to rally to catch up with diffs and spreads, but macro noise clouds the outlook.

Arabica Calendar Spreads

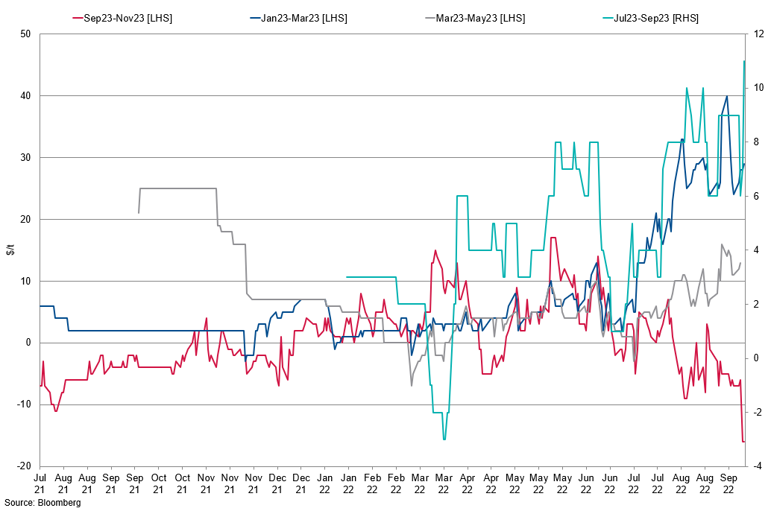

The Dec/Dec spread has tightened significantly and stands at 20cts/lb, tenderable parity is above the market there is further to go in calendar spreads.

Across the commodity complex, the spreads continue to outline the fundamental outlook, while the flat prices are dominated by macro and geo-political news. In conjunction with poor liquidity, volatility in the flat price makes trading tricky, with entry points distorted. The decline in inventories has not caused the flat price to rise, but spreads have been at a premium for some time. If tenderable parity is anything to go by, spreads have further to go on the upside, especially for Arabica. The curve at a premium show there is no carry in the market, which will reduce coffee inflows into warehouses. The spreads highlight the tightness we see, but this was threatened when we saw gradings surge higher to around 260,000 bags and caused the spread to be weak marginally. However, Dec/March rallied again to 6.50cts /lb, with Oct/Dec at 3.20cts /lb. The March/March spread has weakened off the highs recently but still trades at 13.35cts /lb. Spreading positioning data for futures and options has seen a large increase in open interest at 69,326 contracts as of September 2nd, and the number of traders has increased to 125, outlining and improving appetite. Continued dry weather in September and October will worsen the fundamental outlook and give rise to the flat price but also spreads. Once again, the spreads show bullish fundamentals, and while options are expensive, we favour trading CSOs with spreads at current levels. The ever-shrinking Colombian crop and high diffs will also cause the spread to the firm.

Brazil

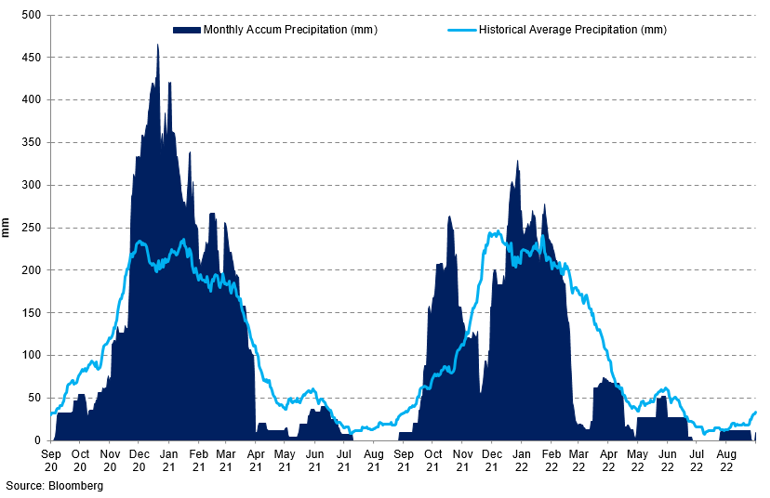

Monthly Precipitation (mm)

Monthly rains has been below the historical average since February, and this means the crop is in a precarious position.

The market continues to be dominated by Brazilian coffee, recent weather has not been preferential, and while it is very early to call, we do not see a record crop for 23/24. We have seen early flowering; this is only an issue if dry weather kills the flowers and, therefore, a reduced yield or quality. Rains have been sporadic so far, which is not conducive to the crop. While we do not write the crop off, there is a decreasing probability of a record crop. This issue is compounded by the fertiliser costs, which in conjunction with fuel prices, have increased the cost of production for farmers. Fertiliser imports into Brazil have started to increase in recent months, reaching 3.367m tons of fertiliser; the price of fertiliser surged higher at the beginning of August to $40,000 FOB, and the price now trades around $23,191 FOB as of August 22nd. The cost of production has risen in the last year, specifically in the less connected areas; the strong dollar will compound the issue. Husbandry has been good; if it wasn't, the crop would significantly suffer.

Rains in Brazil Coffee Regions

We can see the majority of regions have received less rain than necessary, and if this continues, we expect a decline in yields.

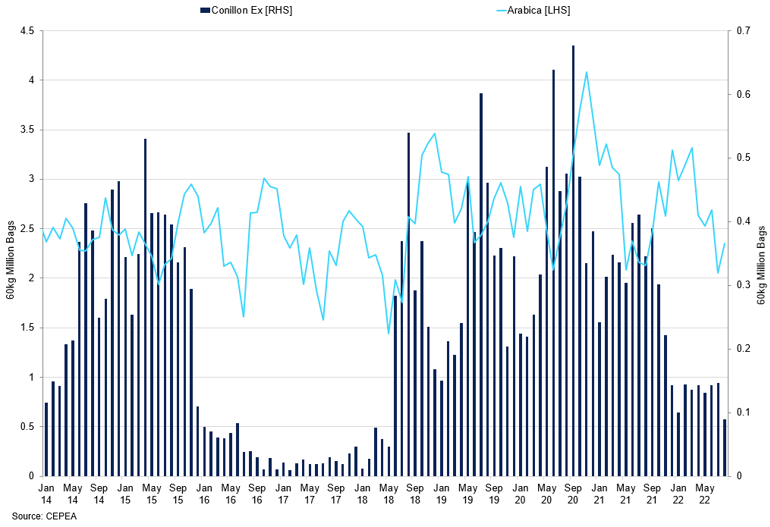

We have it as 60% sold for the current crop, and unless we see a rally back towards 250cts/lb, we do not envisage much producer selling. The COT shows a mild increase in producer selling in recent weeks, with the short at 146,320, but this is just off the lows, which was the lowest short since October 2019. Shipments in August are expected to reach 2.65m bags, but Conilon exports will continue to be too low, this highlights not only the need for Vietnam coffee but also the robust internal demand for Conilon coffee. September data so far suggests that boarding is 177,929 bags, with issuances at 379,355, the latter down 16.1% while boarding is up 24%. In July, exports in Brazil were low at 2.476m bags, with Conilon at 144,625 bags, soluble coffee was 306,384 bags in July, down from 348,583 bags in June. Total Conilon shipments this calendar year have been low at 939,334 bags, compared to the Arabica at 19.29m bags. Total shipments this calendar year stand at 22.443m bags; Germany, Belgium, and Italy have received the most coffee, at just over 10m bags; clearly, the Belgium imports are for storage to be re-exported. Japan has imported 991,898 bags of coffee, and this will help supply Southeast Asia as well as Australia and New Zealand.

Brazil Conilon and Arabica Exports

Exports of Conilon have dropped sharply despite stronger crops, this is putting pressure on Vietnam.

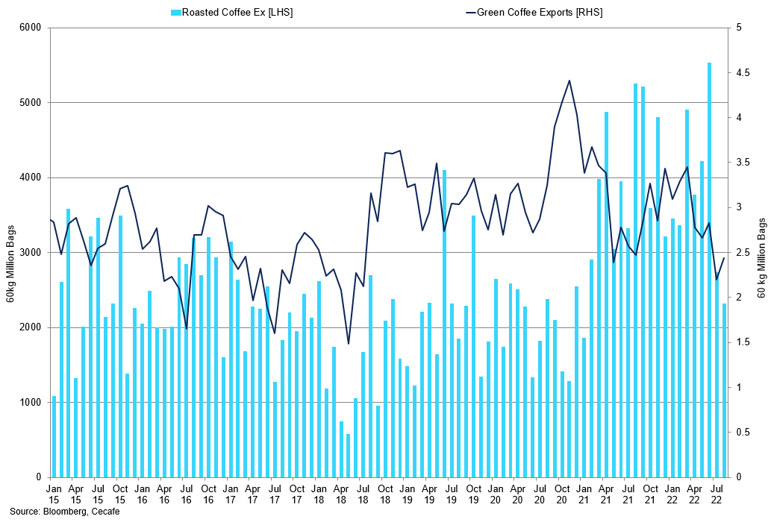

Brazil Roasted Coffee vs Green Coffee Exports

The lower crop has clearly played out in the exports, but on a coffee year basis we have seen stronger exports than expected, suggesting lower carry-over going into 22/23.

For the second year in a row, we have a crop figure below 60m bags, and we expect the 22/23 crop to be 59m bags at this time, with Arabica at 38 and Conilon at 21m bags. We revised our Arabica number lower from 40m bags, and once again shows a deficit in Arabica coffee, and this will keep spreads at a premium as inventory falls. The global deficit is largely from the low crop in Brazil; consuming countries demand 40m bag; this year, the 38m bag crop will come off the back of a 31m bag year where local stocks have been depleted. The low Conilon exports for the 21/22 season could mean this coffee is shipped in the coming months or has been held back in Brazil. Brazilian consumption is 21m bags, which, in conjunction with the need for 40m of exports for consuming countries, brings a 2m deficit in Brazil alone as we do not expect carry-over. In our opinion, the strong exports last year were carry-over from previous years, this will compound the issue and prompt diffs to rise with farmers potentially holding back sales as they expect higher prices. The ESALQ arabica indicator reached R$1,335.47/bag, and we expect this to rally in the next couple of months as the dollar continues to strengthen and the lack of Arabica availability. Local prices remain high historically, but higher costs will squeeze margins, and farmers are likely to hold out for higher prices; with the flat price falling, we do not anticipate much Brazil selling. We have not seen much activity from Brazil group ones which goes some way to confirm the previous statement, however there is a little more group 2 activity.

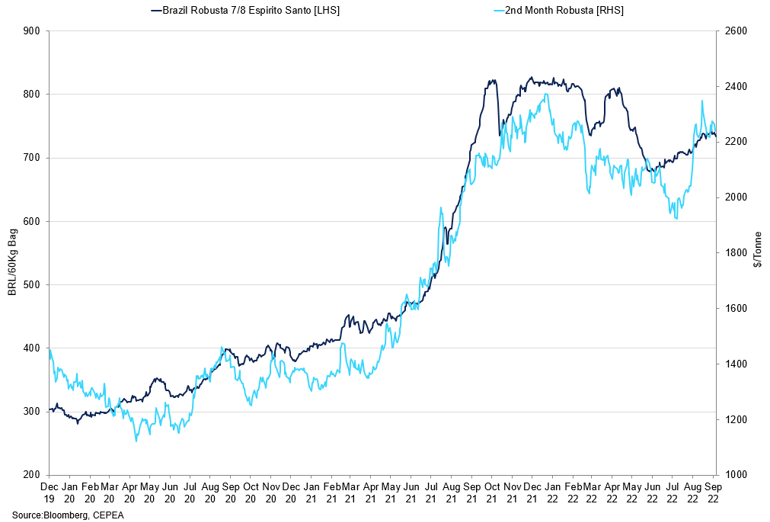

Brazil Robusta 7/8 Esprito Santo vs 2nd Month Robusta

The sharp rally in the London contract has not been mirrored in the local price.

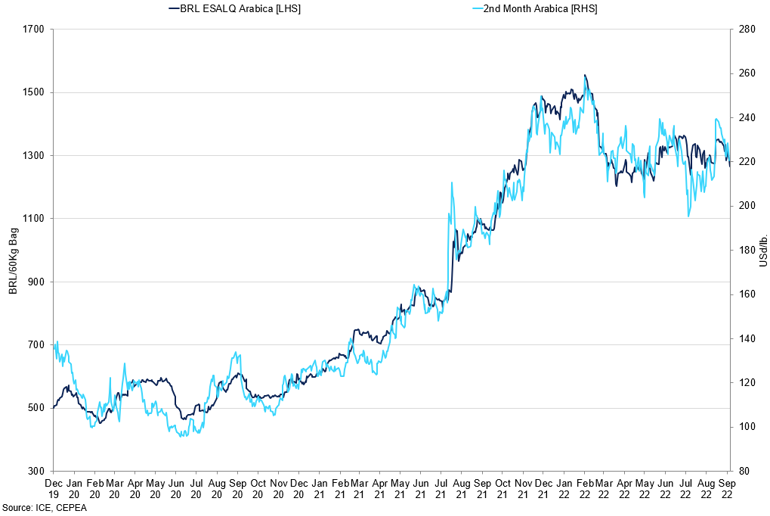

Brazil Local Arabica Price vs 2nd Month Arabica

Local and exchange prices for Arabica have tracked sideways in recent weeks, the market lacks direction.

Colombia

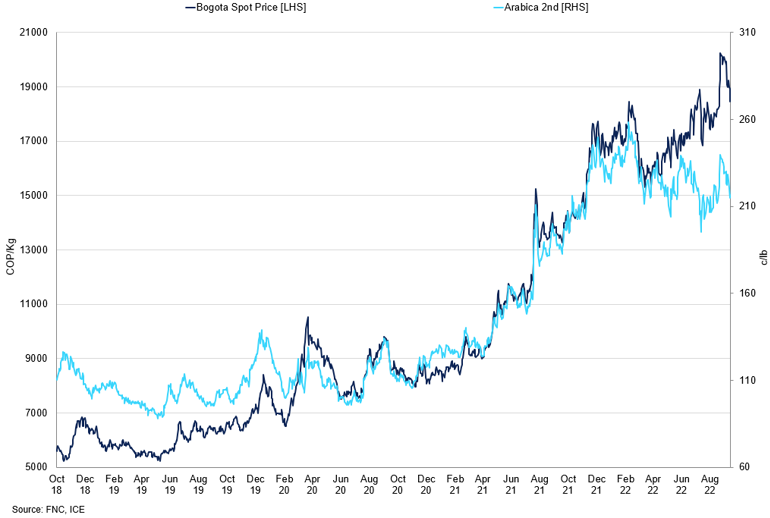

Colombia Bogota Price vs 2nd month Arabica

The market needs to rally before we see any Colombia coffee sold, as the diffs remain very strong.

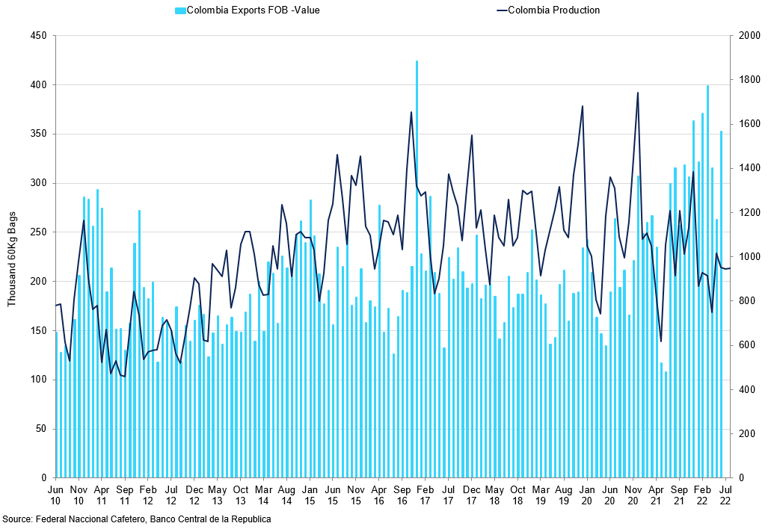

The Colombian crop is underperforming as the weather has not been preferential; rains have damaged the crop and reduced the flowering. This has also delayed the harvest, and with high fertiliser prices, reducing fertiliser application will reduce yields. As a result, we see the crop at 12m bags, but as the cycle continues, we could see this moderated to 11.5m bags. The crop is starting to get going, and according to FNC data, August grew 4% Y/Y to 949,000 green coffee. As a result, the production for January- August at 7.3m bags, down 7% Y/Y in the same period last year. Between September 2021 and August 2022, output was 12m bags, down 9% Y/Y. According to FNC, the production for this year's crop is down 11% so far at 10.849m bags. With our crop number for the 21/22 season at 12m bags, there would be around 400,000 bags carry-over, assuming this coffee is not consumed internally. Colombia is still importing around 1m bags from Brazil, which will help with domestic consumption.

Colombia Exports FOB vs Colombia Production

Colombia exports FOB have maintained their value, this is expected to remain the case as supply struggles.

Colombian exports continue to remain on the back foot with the August shipments at 872,000 bags, down 23% Y/Y. Coffee year exports have reached 11.05m bags, down 6% from the previous year; we do not anticipate strong exports for September due to the softer crop. Colombia also saw coffee exports average of 987,998 bags between February and July, but we expect September shipments to be below this level. Differentials for Colombia at 78 over would bring the market to 307.5cts/bag. As a result, there will be limited Colombia selling in any rally towards 250cts/bag; the WCI container freight benchmark rate per 40ft box continues to decline but stands at $5,661/box. For diffs to soften, we need to see the flat price rally, but the dollar continues to strengthen, and macro jitters plague prices.

Vietnam

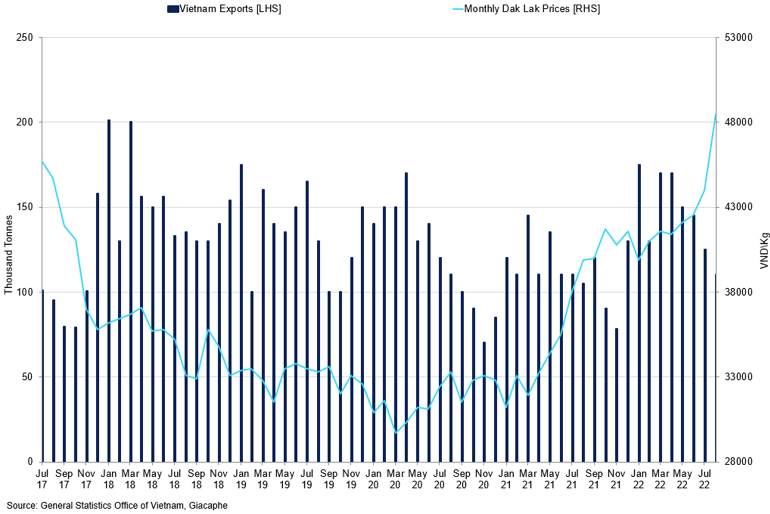

The strong performance of the London contract has seen diffs weaken, however with the reduced availability of Conilon to the export market, and we expect diffs to firm. Demand for Robusta is strong, causing farmers to hold back coffee, and differentials will firm, which could cause the flat price to rally further. Prices for immediate delivery have been seen at 48,000VND/kg, and demand for the existing crop is steady and will be until year-end. The industry continues to go ship coffee using bulk, and exports have started to creep higher as freight availability improves and visible stocks decline in Ho Chi Minh at 2.718m bags as of August. This is down 1.1m M/M and 2.273m bags annually. We expect this coffee o continue to flow in the near term despite China's COVID policy.

Vietnam Exports vs Monthly Dak Lak Prices

Exports from Vietnam will rally into year-end due to the new crop, and local prices will stay firm as demand for Robusta is strong.

Our crop number for 21/22 stood at 29m bags, but we see this increasing marginally in the 22/23 season to 30m bags. We have been saying for some time that the Vietnamese farmer has started introducing other crops such as pepper and durian fruit into their farms as it has been a lot higher yielding and the Chinese market is on its doorstep; this will continue, and at this time we do not see the crop above 30m bags from a capacity perspective. The fertiliser cost continues to hit Vietnam farmers, which has also impacted the crop. In addition to these factors, the rains have not been conducive to a significantly bigger crop. This trend will continue, and if Brazil holds back Conilons, Vietnam coffee will be increasingly sorted after, and diffs will be firm.

Domestic consumption remains 2.5m bags, but the Southeast Asian market will continue to consume more coffee. The European market will remain stagnant this year due to the cost-of-living crisis; however, roaster cover is still stagnant, and with delayed shipments, the situation will become increasingly tight until container availability normalises. Demand for Robusta coffee will be substantial due to the reduced Conilon exports, and while the diffs for the new crop are considerably below the current crop, we expect this coffee to be consumed and shipped. It will likely go straight to the industry because of changing blends.

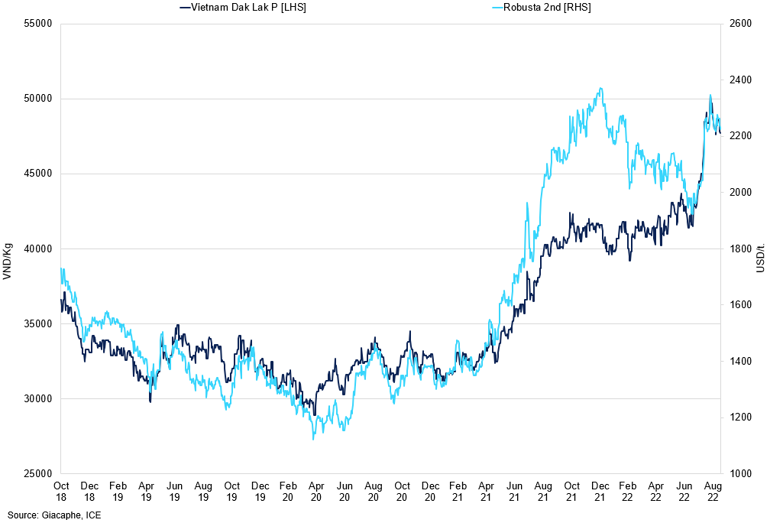

Vietnam Dak Lak vs 2nd Month Robusta

Local prices are high and that will improve profitability for farmers but cover crops continue to hinder supply growth in Vietnam.

Central America

Honduras diffs are 35 over but as the new crop has not started, we do not expect any coffee to be sold until October with the flat price around 215cts/lb; the market needs to reach 250cts/lb to see Honduras selling. In our opinion, there won’t be much let up in the diffs in the near term as the terminal price fails to catch a bid and sustain a rally, the physical market is quiet at current levels. Our crop number stayed at 5.5m bags for the 22/23 season after a 5.5m bag 21/22 crop. Exports from Honduras have averaged 550,00 bags since February and totalled 3.3m bags (February to July). July data was the lowest at 390,000 bags. From October 2021 to July 2022, Honduras exported 4.28m bags, leaving 1.3m bags to be exported in August and September. Due to high diffs and freight, we do not expect many exports in August and September, and tenderable parity is above the market, even with the spread at a premium. In our opinion, terminal prices would be higher if it wasn't for macroeconomic fears, but the spreads show the fundamental story.

Guatemala for the 21/22 crop was 3.6m bags, and we see 3.6m for 22/23, despite the higher fertiliser costs and strong USD. The strong exports suggest that production has been strong. In our opinion, the 22/23 crop harvest is starting and is around 15% sold as of September. Differentials are strong, but there have been limited FOB sales recently. Shipments are behind last year, with shipments from October 21st to July 22nd around 3m bags, this is flat on the previous year, but shipments in August and September are likely to be lower. With diffs, high and shipping still lagging volumes have been small, but the demand for Guatemalan coffee is strong, specifically for high-grade coffee for the U.S. and European markets.

Nicaragua produced 2m bags in the 21/22 season, and we see a large crop in the 22/23 season at 2.7m bags. Consumption of Nicaraguan coffee has remained strong, and this will remain the case in the near term, especially given the shortage of Arabica coffee. The shipment delay is clearly problematic for the crop, but exports are still strong, which suggests we have a strong crop. As a result, our number for 22/23 is higher due to resilient exports and steady conditions during the winter.

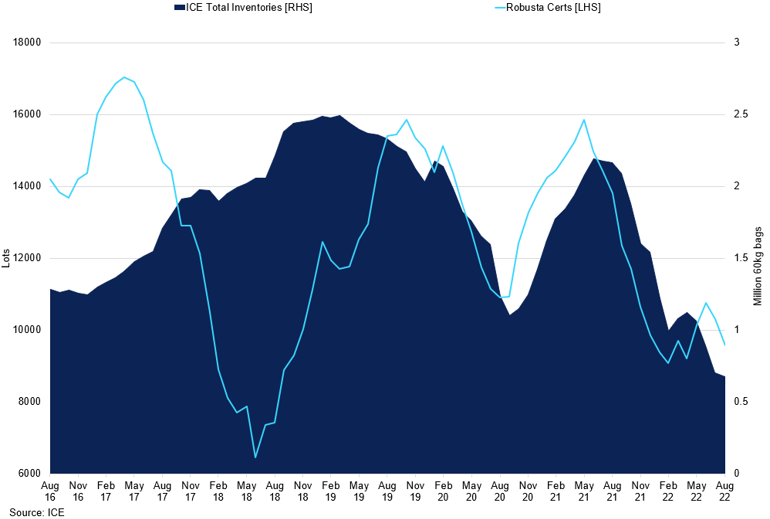

Inventories

We have previously highlighted that unsold inventory was between 550,00 and 750,000 bags, with stocks at 627,750 bags at the time of writing, we hold firm with the prediction. We have seen a substantial decline in stocks since the beginning of May, as the old crop started to wane, and diffs rallied the industry went for the certs, which have been the cheapest coffee around for some time. Arabica remains about Brazil, and the deficit, combined with high freight costs and bottlenecks, compounded the issue as some roasters scrambled for a product. Pending grading in August has shot up, peaking at 250,000 bags and now stands at 212,056 bags; this is mostly old coffee that was brought in 18 months ago; there are question marks over the quality and appearance of this coffee. The marginal uptick in certs is due to the bags passing, with a small number of bags failing, but the rejected coffee is likely to be still sold OTC; the official pass rate is high, around 80%. The regrading will enable traders to benefit financially if the bags pass as some of this coffee could have received an age penalty, but the passed bags would be priced at the current price. The coffee cannot be carried with the spread at a premium, so we expect this coffee to be pledged to a roaster in the coming months.

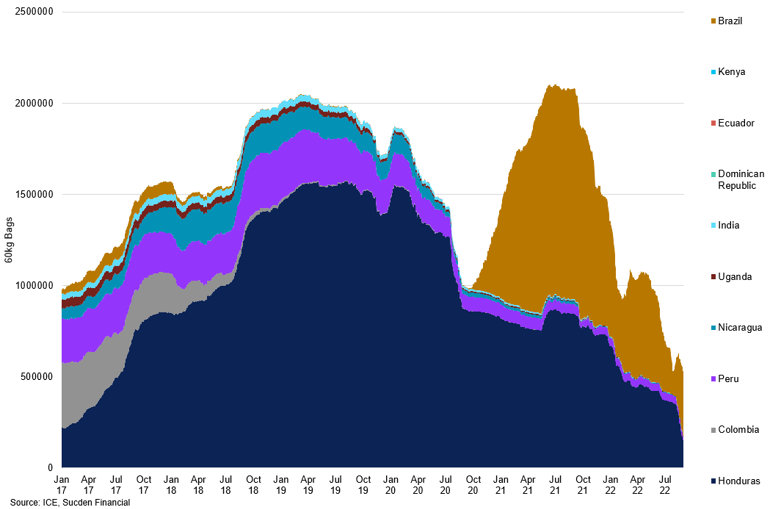

ICE Inventories by Origin

Brazil coffee in inventory has declined sharply, and we expect were withdrawals in the coming months.

We expect this to be the case as the coffee is old. August shipments from Brazil totalled 2.476m bags, the lowest since September 2017, with Arabica at 2.023m bags. This lends itself to more withdrawals from certified stocks. The low exports, in conjunction with high differentials and the market not near tenderable parity, suggests roasters and industry will go for certs in the short term, assuming that they can assure the quality of the product, something that is increasingly hard to do.

ICE Total Inventories vs Robusta Certs

Low inventory is causing further tightness in the spreads, but there is no carry due to the curve and this will likely cause coffee to go straight to industry.

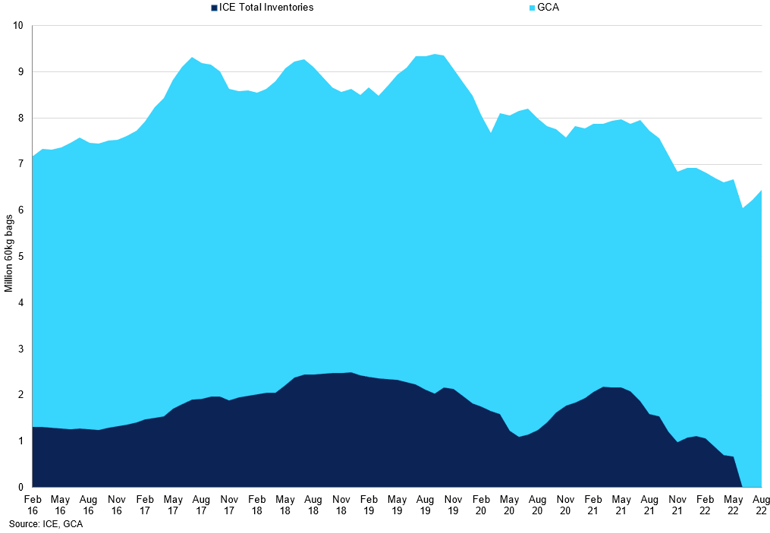

GCA stocks are rising, up from 6.2m bags to 6.45m bags in August; New York warehouses hold 2.084m bags, with Houston having the next largest at 859,069 bags, with San Francisco next in line at 649,399 bags. Certs from Europe have been shipped to America in recent months instead of coffee coming straight from the origin. Inventory data in Europe suggests coffee is there to be consumed with ECF stocks at 817,837 tonnes (13.34m bags), Robusta stocks stand at 315,637 tonnes with naturals and washed Arabica at 237,954 and 264,246 tonnes, respectively. ECF stocks have trended higher this year, and with the structure at a premium in recent months, the increase in off-exchange stocks can be partly attributed to the lack of carry in the market.

GCA vs ICE Inventories

GCA stocks in America continue to oscillate but they do not show the whole picture.

JCA flows have been slower, with inventories rising to 190,880 tonnes from 171,840 tonnes in January. Inventory data see 3.18m bags; most single-origin coffee is from Brazil with 70,998 tonnes in warehouses, Vietnam at 27,060 tonnes, and central origins coffee at 29,029 tonnes. China is Japan's largest destination of soluble coffee, and data indicates 85 tonnes in May, significantly lower than the 217 tonnes exported in April. Roasted coffee to China was higher in May at 142 tonnes compared to 52 in April; both soluble and roasted exports to China are down sharply Y/Y. With Japanese stocks supplying a large proportion of China's coffee consumption, we could see reduced outflow in this area as China has a lower elasticity demand with only the younger generation drinking it, and with unemployment levels in this demographic, their propensity to consume less is higher.

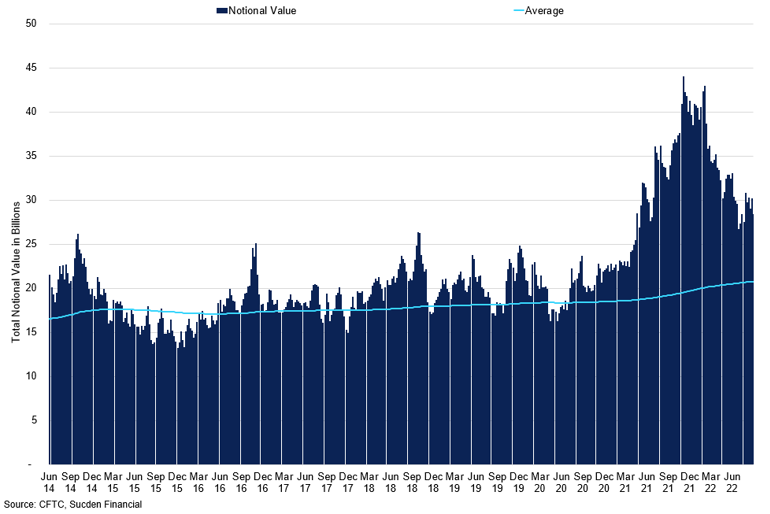

Commitment of Traders'

Total Exposure to Arabica Coffee vs Average

Total exposure is high due to the flat price but the number of traders is low than previous months.

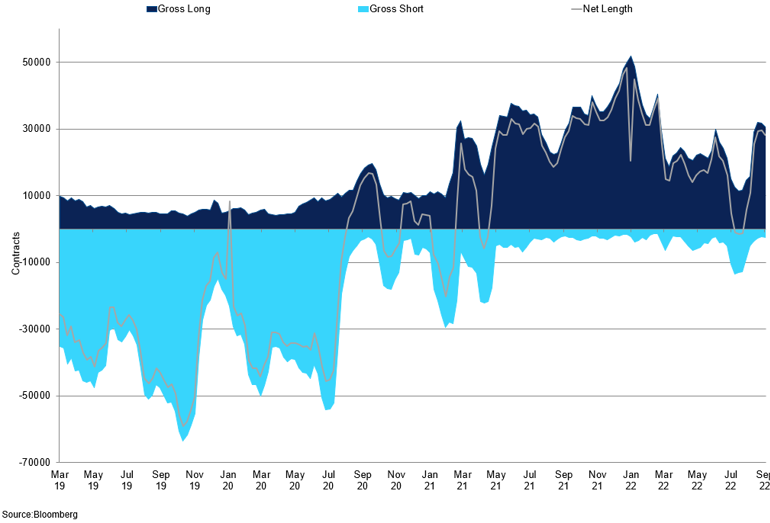

The net length of the managed money for Arabica has reduced due to the macro fears and slowing economy. The sell-off in the flat price and high volatility caused funds to reduce their exposure, and the net position stands at 18,849 contracts as of August 19th; however, since then, the position has increased back to 28,752 contracts with the number of long traders significantly on the long side rising to 138. Spreading positions have also grown to 70,237 contracts after grading has increased and the premium has narrowed, but we expect the structure to remain strong and at a premium. The market is caught between bullish fundamentals due to weather in Brazil and macro fears. Balance sheets have been downgraded but the fundamentals are playing out in the spreads, and we wouldn't be short unless you have the product. The high volatility and high notional prices are causing traders to run lower risk and VAR levels. We expect upside moves and an increase in the net length as fundamentals come back into play and slower growth is priced into the market.

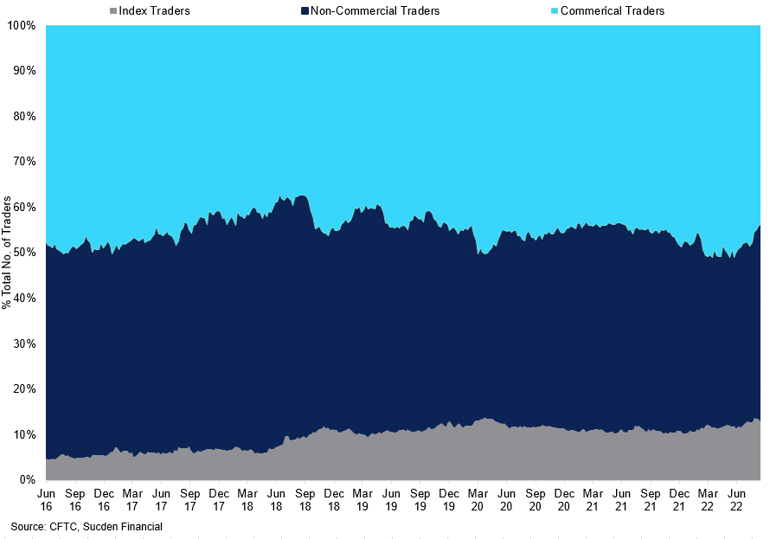

Total Number of Traders by Group as a Percentage

There have been an increase in non-commercials in recent weeks which outlines an increase in spec involvement.

Commercial positions have significantly reduced their gross short and stand at 146,661 contracts as of September 9th. The net short has increased to 76,094 contracts as of September 9th, but with the flat price falling this week, in our opinion this was not producer selling. However, with the market not at tenderable parity, there has been no new selling, although many shorts have rolled down the curve. If the crop comes in lower than expected, this will present significant difficulty for producers who may have sold their coffee forward. Local prices are still elevated, with the ESAQL Brazil Arabica indicator at R$1,313/bags. The commercial long has also declined sharply to 70,567contracts as of September 9th. This implies lower cover from roasters and could indicate them going for the certs.

Normalised KC COT Report

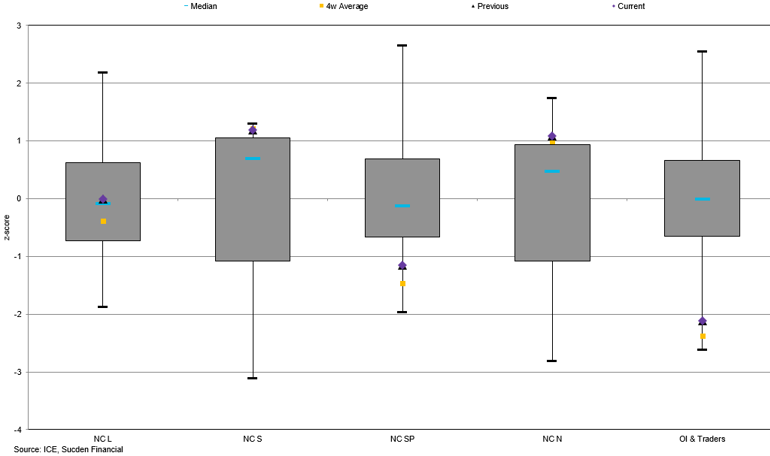

The number of traders and OI is significantly lower compared to historical levels, and the net length is on the median suggesting significant capacity either way.

When we look at the normalised COT positions, we highlight that the net length has been below the lower quartile for the last 4 years; the short is still near the record, suggesting little bearish sentiment in the market. The open interest and number of traders are still near the record low and considerably below the 4-week average suggesting that appetite has declined in recent weeks, this is in line with the summer months but also poor liquidity. As traders return to their desks, we expect volumes to pick up in the coming weeks.

Robusta Managed Money

Managed Money have pushed prices higher as they increase their longs.

For Robusta, managed money saw a significant increase in the net length in recent weeks reaching 28,003 contracts as of September 9th. The funds have seen the rally in Robusta and increased exposure; with the Brazilian crop being marked down, the increase in Robusta blends is likely and would tighten the Robusta balance sheet, as well as early rains in Vietnam, which was not conducive to the crop. The producer net position shows a short 35,575 contracts and a sharp rise in recent weeks as the farmers and producers sell into the rally; we saw a change of 14,107 contracts a few weeks back and now marginal selling as prices plateau. This was mainly due to a sharp increase in the gross short of 72,269 contracts with 7,415 shorts added in the week to 2nd September, there was a significant reduction in longs at 9,415 contracts. The decline in positioning for Robusta will undoubtedly impact the commitment of traders and the net length available.