Our coffee crop update covers commentary on recent price activity, coffee market forecasts and potential futures and options trading strategies to take advantage of market movements.

The weather in Brazil is still not preferential for a large 2022/23 crop, aiding bullish fundamentals further, but there is a long way to go. Shipments and inventories are starting to fall as we move into a deficit, but the front months are plagued by macro events. Traders need to be patient, but what are the key themes for the market in the next month?

Executive Summary

- Commodities have retreated following the Fed’s change in language on inflation, in conjunction with action from China to cool prices may ease price pressure somewhat.

- However, PPI and prices paid by manufacturers continue to rise, suggesting input costs are high and will be passed onto the consumer.

- While the Fed talk about tapering bond-buying, it is worth remembering that stimulus is historically incredibly accommodative with the Fed balance sheet $8trn.

- We have seen EM currencies that have been importing inflation hike rates swiftly in recent months; we expect this to continue in the coming months. This BRL benefited from this, and higher yields could prompt further inflows of funds.

- However, when the Fed turn hawkish, we believe the dollar will turn, and EM currencies with higher levels of denominated debt will weaken similarly to 2018/19.

- The Brazilian election will come into play in H2 2021 and particularly Q4. In May, a survey by Datafolha indicted that President Lula would beat Bolsonaro in the election race, with Lula winning 41% of the vote in the first round of the election.

- Weather in Brazil has not been preferential, and while there was no frost last week, these are not conducive to conditions. We do not see a bumper crop in 2022/23, compounding the fundamental outlook.

- We saw a reduction in long traders in the last few weeks as funds take profit and re-assess the commodity rally following the Fed. We expect new longs to be added as we move into the deficit year.

Exports from Brazil have been falling, and we are starting to see inventories respond with drawdowns, and this will be the start, with the outflow of Peruvian coffee a substitute for Brazils.

Container shortages significantly impact the availability of Robusta coffee from Vietnam, keeping the London contract supported and capping the arb. - We expect the arb to tighten in the longer term and break above 100 once again as the Arabica shortage compounds and Robusta availability improves.

- Specs have had their confidence knocked, even with the strength of the BRL, but we expect the trigger to be Brazilian farmers who sold coffee at R$500-600/bag struggling to sell this coffee now that local prices are >R$800/bag. We have our doubts that farmers will honour these contracts and could be the catalyst for higher prices.

- The Colombian market is also struggling, and the situation is not likely to be rectified in the near term. Exports are suffered heavily in May as the port of Buenaventura was blocked.

- We do not think roasters have bought their winter roastings yet and expect commercial buying as prices drift lower. They may be waiting for prices below 150cts/lb, but they may be lucky to get this, and we advise locking in some product now.

- Coffee prices remain cheap given the fundamental outlook, and if you are trading the futures market, we favour buying dips.

- In our opinion, we favour deferring a position down the curve to mitigate macro swings. However, we think the options market is more suited to today’s market currently.

- Looking at the options market, as of July 14th, a call spread is our preferred option for December, with 180 calls at 582bp vs the 200 calls at 332. We would sell the Dec 140 put at 4.83cts too.

- Those looking further out may have to pay up for the call spread with the March 180 call at 9.39cts vs the 210 calls at 6.16cts. Selling the 150 puts at 11.29cts.

- Traders not wanting to limit upside could look at selling puts or a put spread, which would make it easier to your gamma.

Macroeconomic overview

In recent months we have seen asset prices continue to rise in conjunction with vaccination rates and risk appetite. Tailwinds due to economic data buoyant economic data, but the investors continue to grapple with inflation fears that central banks either label ‘transitionary’ or suggest it is not near target rates yet. Emerging market countries such as Brazil, South Africa, and Mexico feel the pinch, with some raising rates to curb inflationary pressures. We expect further tightening from EM countries which will keep the high yielding EM currencies carry intact. Macroconditions favour EM currencies for the time being, and the BRL has, rising commodity price is beneficial for the export-heavy countries like Brazil, Russia, and South Africa. However, economic conditions on the ground are weak but are showing signs of improvement.

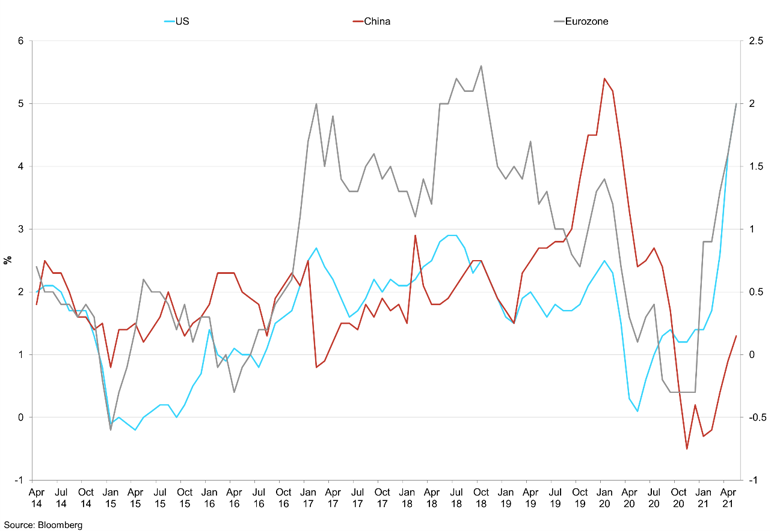

US vs Eurozone vs China CPI

Inflation is starting to pick up in major economies, but commodity prices have softened since.

Investors believe central banks in the UK, EU, and the US are looking at tapering their bond purchases in the coming months. However, the ECB reiterated their stance on preserving the favourable conditions to ensure a balanced recovery for all sectors of the economy. The ECB indicated that they would keep their asset purchases at €20 billion and run if necessary. Business conditions are improving; in line with economic data, the ECB expect GDP to accelerate in H2 2021 with real annual GDP at 4.7% in 2021, 4.7% in 2022 and 2.1 in 2023. Vaccination rates in Europe have caught up well, which has been the reason behind stronger consumer and business sentiment. Risk appetite in the bloc has caused the euro to strengthen in recent months, but it remains down on the year and fails to break 1.22. We expect the economy to accelerate in the H2 2021 in line with ECB expectations, but price pressures are likely to hit the 2% target in the near term, with the bloc is vulnerable to higher prices due to its propensity to import materials.

In the US, price pressure is more evident, exemplified by May’s CPI at 5% y/y, unit labour costs are also rising. We also saw the ISM manufacturing prices paid component rose to the highest level since 1979 in June at 92.1, up from 88 the previous month. The cost of raw materials has impacted the housing market in recent months, with housing permits down 9.5% in April and housing starts at 1.569m for the same month. The cost of lumber and other raw materials increases the costs of construction and manufacturing, but the Fed remains convinced it is transitionary. If prices start to plateau, inflation pressures will follow on a month on month basis, but after stimulus measures in the last 18 months and higher commodity prices, it is unsurprising to see cost-push inflation.

The other side of the equation is lagging; still, the unemployment level globally is improving, and the services sector is showing signs of thawing. This is particularly prevalent in the US, where demand for employment in the services sector is gaining traction judging by the traffic on open table and google analytics; bookings on OpenTable between April and May are in line with a 1m+ gain jobs in hospitality and leisure. Unemployment benefits are generous; health concerns are still deep despite the vaccine, which aids the labour shortage. However, nearly 50% of US states are ending their employment benefits in June or July, and this will incentivise citizens to return to work, especially for summer jobs in hospitality. Average hourly earnings are up 0.3% y/y and 2% y/y, in April and May, respectively, with the average weekly hours also rising. Companies could hike wages to reduce labour shortages, but hospitality companies cannot afford higher costs. We could see another weaker than expected reading for US employment, but we expect the labour market to improve. The lack of new candidates has prevented some companies from increasing output, and this dynamic is likely to continue in the coming months. NFPs have been below expectations for the last two months due to the above reasons. The labour force participation is at 61.6%, with the unemployment rate at 5.8% as of June 4th.

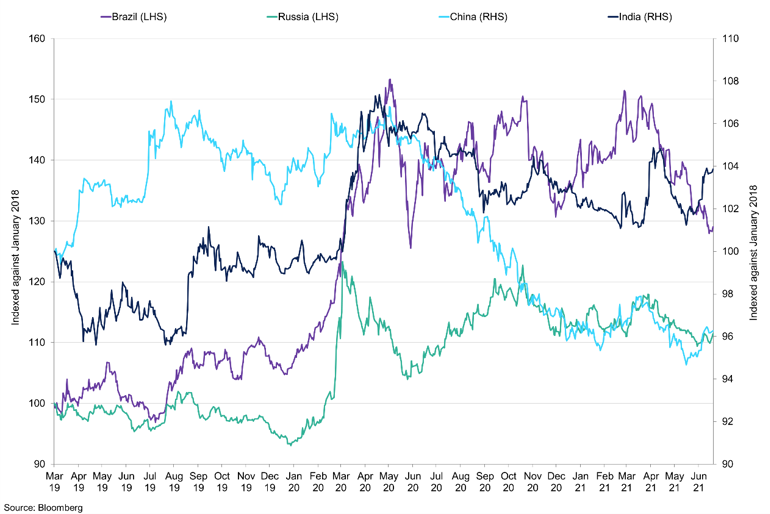

Emerging Market Currencies

Brazil, Russia, and China’s currencies have rallied in the last few months as they tighten monetary policy.

In Brazil, the economy has shown vital signs of improvement in recent months, causing the BRL to really towards 5 to the $. Risk appetite in Brazil due to vaccine calendar, driving a stronger currency and BOVESPA. Inflation expectations are rising, with forecasts for CPI at 5.82% for year-end, with the Selic rate at 6.25%, up from 5.75%. IBGE inflation IPCA was 8.06% y/y, with the month on month figure at 0.83% in May. The rise was attributed to higher commodities prices and electricity bills. GDP is improving, and the Q1 solid growth coupled with robust exports will boost economic expectations; Brazil’s net debt has started to fall and stood at 60.5% of GDP, with personal loan defaults at 4% as of April. China is looking to curb prices of commodities and has reduced the participation of speculators and rumours of SRB releasing inventory into the market; we are yet to see any evidence of this. This may be a short-term measure as the market remains tight for a lot of the metals complex. Iron ore prices have rallied 115% from June 2020 to June 14th, 2021. Brazil is a significant exporter of high-quality ore, and this will benefit the economy in the near term, but China’s economy will moderate in years to come as they prioritise quality growth over industry and construction like in previous years. The labour market has a way to improve, but the signs remain optimistic, especially with the new vaccine calendar. The leading risk economy in the next six months is political; the election is in 2022, and Bolsonro’s approval rating still falling, with 24% believing he is good or excellent in May, it seems that the country is waiting for him to lose the next election. Recent polls suggest that former president Lula would beat Bolsonaro in a runoff vote in 2022. There is a downside to the BRL with COVID deaths and cases not falling sharply; however, up until recently, any BRL strength was more in the form of USD weakness, but the tide seems to be changing, which will favour coffee we prefer selling USDBRL rallies. The change in language from the Fed could cause Brazil to raise rates faster, another boon for the BRL in the next six months.

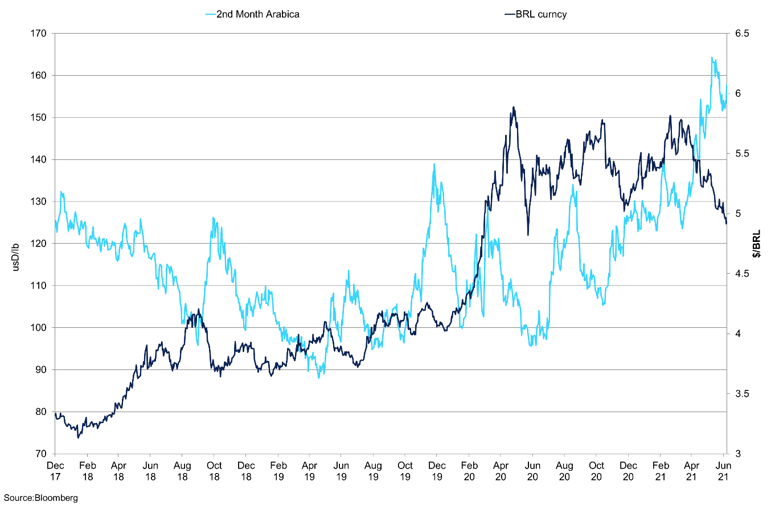

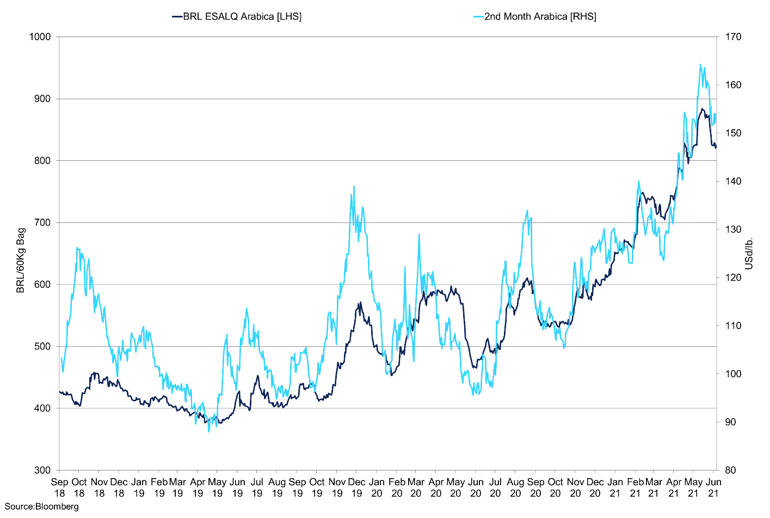

2nd Month Arabica vs BRL Currency

The recent strength in the BRL aided the rally, and this is expected to continue in the near term.

Supply and Demand

Our April report reiterated that traders should remain patient despite the market sell-off and correction back to 120cts/lb. However, since then, the market has not looked back and now trades at 156.20cts/lb as of June 14th and not far from the YTD high at 168.65cts/lb. We have seen a moderate sell in the last days, which started in the grains space but has spread to softs. We maintain our bullish rhetoric on coffee and continue to favour buying the dips, and in our opinion, it is not inconceivable that the arb breaks 100. After years of focusing on demand, COVID-19, and large crops, the market is now focused on a deficit and rightly so. Consumption in 21/22 has been robust considering the underlying economic conditions. Employment has improved in recent months, but the labour market now faces high employment benefits, but companies are unable to offer higher wages at this time due to months of no cash flow. This is particularly prevalent in the US, as we have seen from NFPs and weekly claims. In Australia, the JobKeeper benefits finished, and we did not see a significant rise in unemployment, but this may not be the case for all economic regions, and our base case is still for unemployment to rise as when these schemes fall. This could present some downside to coffee consumption.

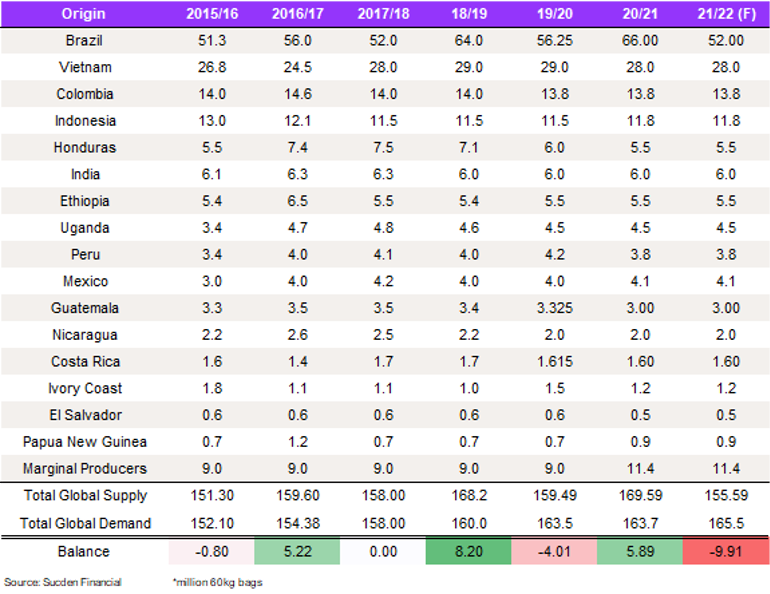

SFL S&D Balance Sheet

As things stand, we maintain our consumption figure at 165.5m bags; while lockdown periods have been extended, we do not expect much impact on consumption as a result. Any weakness will likely be recovered in H2 2021. ICO import figures into the European Union were down 6.9% y/y in February 2021 for 5.696m bags, bringing total imports to 9.8m bags for the first two months of the year, down 1.1% y/y. March 2020 to February 2021 imports are 77.469m bags, down 3.2% versus the previous 12 months. Imports into the US have increased by 10.2% y/y, to 2.225m bags but imports for March to February were down 6.5% y/y to 28.382m bags from 30.329m bags. In our opinion, imports into America will rise in the next data releases as their economy continues to re-open. Tracking data from Opportunity Insights shows that only three states, Missouri, Ohio, and the District of Colombia, had negative total consumer spending in the week to May 16th, compared to January 2020, only Ohio and Missouri had negative readings to January 2021. Grocery spending is up 17.21% compared to January 2020. Across the US, spending in restaurants and hotels is up 1.9% compared to January 2020; we expect this to improve consumption in the coming months, but to see strong consumption growth, we need to see more significant employment in low income (<$27K) and middle income ($27k-$60K) sectors, which are down 23.6% and 4.5% compared to January 2020.

Pre-COVID-19, we had the US and Canadian consumption at 34m bags, coffee consumption will reach these levels once again this year, but as mentioned, to experience sustained growth, we need to see further gains in the employment market. Out-of-home consumption is improving but will take time to recover fully, especially in Europe who have seen restrictions in place longer than expected. Import figures from the ICO indicate that demand growth in Europe is sluggish. However, data was from months prior, and we expect more recent data to be more robust. Shipping delays will remain prevalent, especially with rates still at elevated levels; just in time, supply chains will continue to struggle.

Brazilian Supply

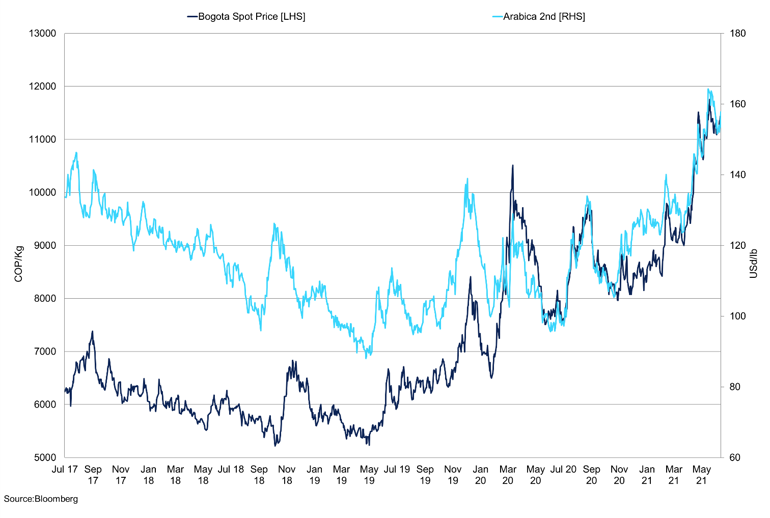

Brazil Coffee Local Prices vs 2nd Month Arabica

The BRL has strengthened as the Central Bank tightened monetary, with local arabica prices holding above R$800/bag.

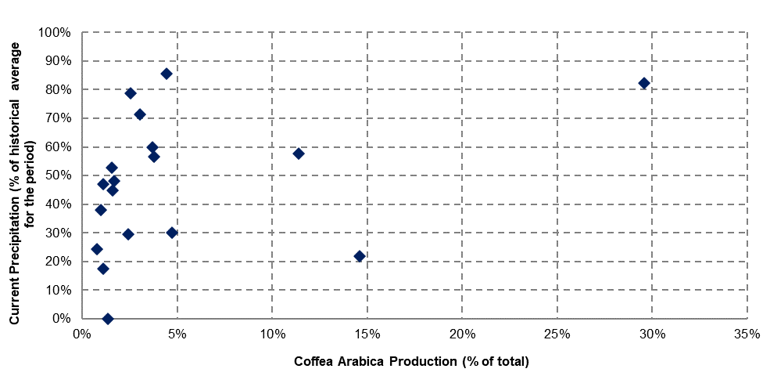

From the supply side, in our April report, we highlighted that weather in Brazil was far from ideal for next year’s crop. Despite rainfall in recent weeks providing some relief to the crop, precipitation levels are below historical levels. We did see improved conditions in Sao Paulo and Parana, but regions such Zona da Mata, Sul de Minas and Alto Paranaiba, which are the largest proportions of the Arabica crop, have, on average, currently have 56% of their historical level of rainfall. Therefore, as things stand, these areas are unlikely to show solid yields and a large crop that would have been expected from an on-year crop. While there is still key fazes of the crop to go, conditions have been far from ideal. Carry-over from this season is likely to be low due to the significantly lower Arabica crop, but also the elevated local prices have promoted producers selling down the curve. The ESALQ arabica price stands at R$824.19/bag, but this has declined from the recent high of R$884/bag; farmers will find it challenging to deliver coffee at 5.50BRL/R$600/bag when the market is at R$850/bag as of June 29th. The harvest is increasing availability of Arabica, but there is little selling pressure from producers. Coffee exports from Brazil have been declining as we approach the end of the crop year. This is in line with our expectations in our last report. Green coffee shipments were 2.6157m bags for May, and as exports have tumbled as the local prices have rallied significantly. Arabica shipments have fallen to 2.05m bags in May, Brazilian exports according to Cecafe issues were 2.098m bags for June as of June 21st, 2021, boarding was 1.155m bags, this suggests we could see shipments improve in June. Conlon exports were also marginally softer in May at 287,627 bags, but demand for this coffee is strong, and we have seen orders at 11+ in Brazil.

Brazil Weather

The weather has improved in recent weeks but reports from farmers suggest they are writing off parts of their crops.

We expect the Conillon crop for the 21/22 to be at 20m bags, but there is more downside to our Arabica number by 1m bags, which would bring Brazil’s total number at 52m bags for 21/22. Maintaining the same assumption of 3million bags of semi-washed Arabica from this crop, which leaves a 16m bags whole of unwashed Arabica in the market, would bring our global deficit to 9.91m bags. This insolation presents a bull story given the lack of substitutes and a significant role in the global balance. However, the 9.91m deficit is compounded by the prospect of a weak on-cycle crop in 22/23. If challenging conditions persist, and we get another dry patch in September, and October the 16m bag hole in the crop will not be replenished, and this will facilitate the bull story. Recent reports of a 19m bag carry over in Brazil are hard to believe given the local prices, lower crop, and strong demand. Using our total figure of 66m bags for 20/21 and the total number of Brazilian exports for the 20/21 season at 42m through to the end of May, assuming Brazil exports 3.2m in June, total exports would reach 45m. 45m bags plus 20.5m bags for Brazil consumption is 65.5m bags, leaving 0.5m bags for carry-over. Even using 72m bags for 20/21, this would mean a carry-over of 6.5m bags; to achieve a 19m bags carry-over, the crop would have had to be 84.5m bags, which we see as inconceivable.

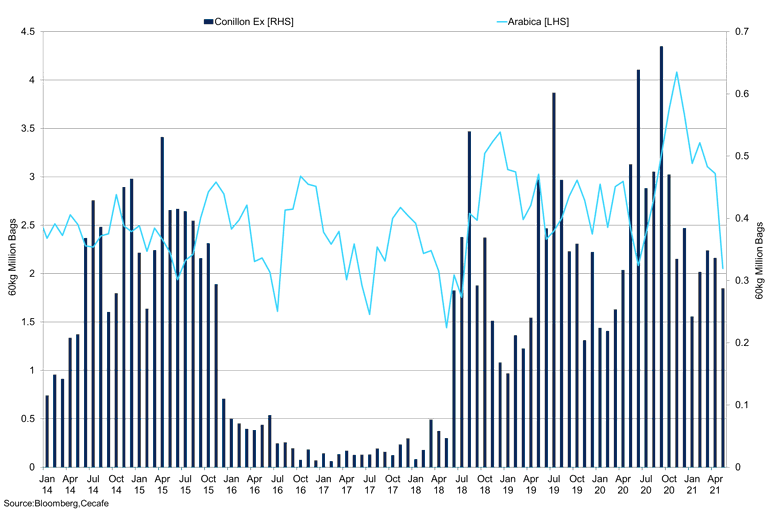

Brazil Conilon vs Arabica Exports

Arabica exports have declined sharply in recent months in line with our estimates.

Washed Arabica

Colombia Exports FOB vs Colombian Production

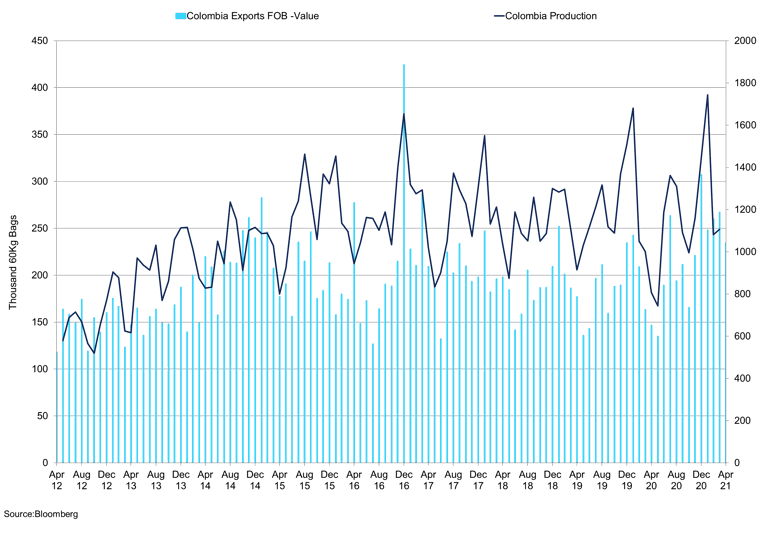

Colombian exports were robust up until May when roadblocks capped shipments from Buenaventura.

Political turmoil in Colombia capped exports of washed Arabica, and protests have caused roadblocks. Exports in May have declined 52% y/y to 427,000 bags, down from 894,000 bags in 2020. This was due to blockades, but exports on the year are still up 7% to 4.936m bags, from 4.626m bags in 2020. For this year’s Colombia crop, shipments are up 2% to 8.575m bags from October to the end of May, with the same period for the 2019/2020 crop at 8.386m bags. The blockades were at Buenaventura, this is a major port, and in 2020 this port shipped 8.77m bags and 9.282m bags in 2019. It is the largest port for Colombia’s shipments, with the next largest port at 3.09m bags in 2020. The most recent breakdown of Colombian export data is April when exports from Buenaventura reached 669,387 60kg bags, 636,958 bags of green coffee, 29,373 bags of soluble, with extracts and roasted the remainder. In the month of April, we saw shipments of green coffee to Europe soften in April to 358,591 60kg bags from 420,318 bags in March and 500,366 in February. We expect May’s figure to be considerably lower but still make up most total shipments. Belgium, Canada, and Japan were the next largest receivers of Colombian coffee with 102,183 60kg bags, 83,046 bags, and 64,117 bags, respectively. According to the ECF stocks, there were 260,301 tons of washed Arabica in European warehouses. Given the decline in Colombian shipments in May, we expect to see a draw in these inventories as just in time supply chains struggle for the product.

Colombian Bogota Spot Price vs 2nd Month Arabica

Local prices remain at multi-year highs, and this is expected to remain the case.

Honduran exports for the first four months of 2021 have reached 2.665m bags compared to 2.976m bags in the same period in 2020. Demand for Honduran coffee will remain strong, with withdrawals from ICE warehouses. Certified coffee in warehouses remains the cheapest coffee, and this will remain the case in the near term even with Honduran diffs have softened slightly in recent weeks. Guatemala continues to focus on the harvest, but producers have sold into the recent rally and have reduced their inventory.

Robusta

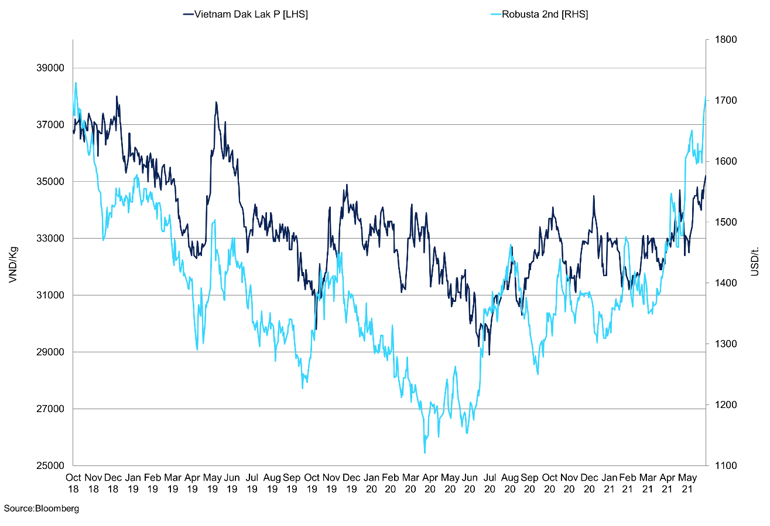

Vietnam Dak Lak Price vs Robusta 2nd Month

Local prices have outperformed the London contract.

The Vietnam crop for 21/22 remains at 28m bags; local prices have rallied in recent weeks and now stands at 34,700VND/kg. This is just off the recent high of 34,800VND/kg, this is a 7% increase since mid-May, and we have seen the produce short positions increase in that time frame. Producers are making the most of the rally, with the July-Sept spread at -$27. This is wide enough to carry coffee. Inventory levels have declined in recent weeks, reaching 15,255 lots as of June 23rd. Conilon coffee will continue to add pressure to the Robusta market, with higher crop numbers being normalised in the long run. Shipping delays out of Vietnam and container shortages continue to cap exports; shipments increased in May to 135,000 tons, up from 110,000 tons the previous month. Total exports from Vietnam remain low compared to last year and could aid further withdrawals from exchange warehouses as just in time supply-chains struggle. Diffs have softened as the market has rallied, we continue to see order delays, but we did see the industry cover as the market edged lower. Even though we see a stronger Robusta balance sheet in the coming year, the more profound micro-situation regarding shipping and freight availability, freight rates are high, helping to tighten the Robusta market. Therefore, we expect Robusta prices to remain elevated in the near term.

Commitment of Traders’

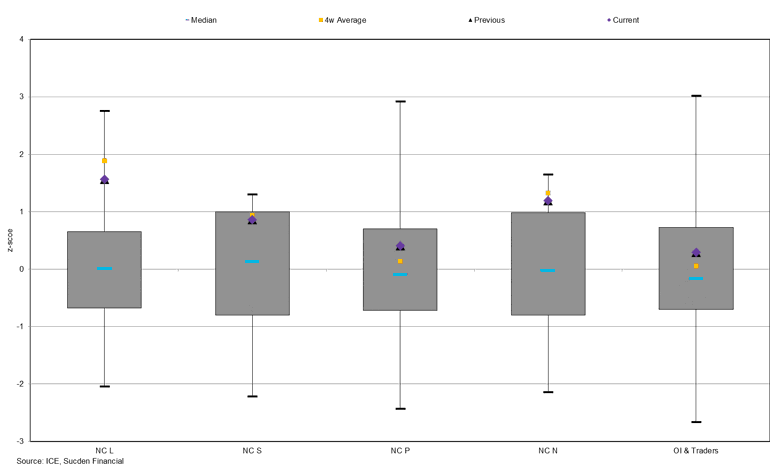

Non-Commercial Supplemental Arabica Normalised Positioning

We can see the net position has fallen back slightly in recent weeks, as has the total OI.

Supplemental data for Arabica shows a reduction in the non-commercial position by 8,150 contracts. The net position now stands at a length of 23,365 contracts; this was achieved by increasing shorts positions and reducing longs. There were fewer long traders in the market this week; reducing the length was needed to help the market in the longer run. We still have 177 traders long of the market in the non-commercial bracket, with 72 shorts. The number of long traders has declined from just above 200, the market was overbought, but the correction and reduction of traders show we saw some profit-taking and some reduced activity in the market. Could this be from funds worried about inflation? Possibly. More likely, it was triggered by the broad commodity sell-off with some funds liquidating longs to pay margin calls elsewhere or to lock in a profit before quarter-end.

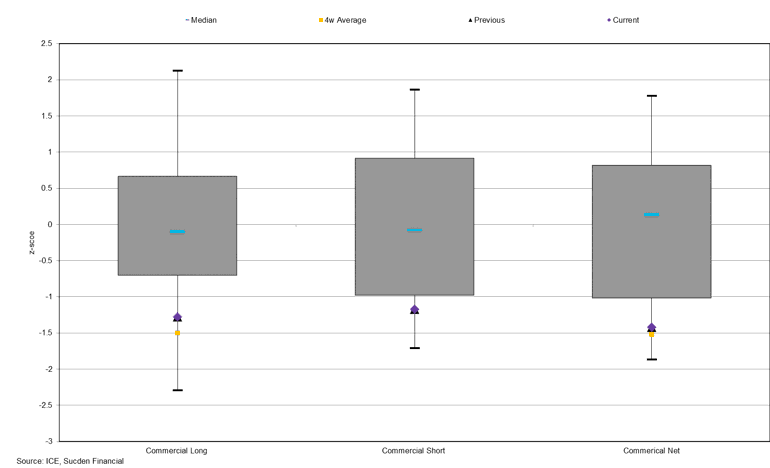

Commercial Supplemental Arabica Normalised Positioning

The net position and gross short have both fallen below the 4-week average.

The commercial position also tells an interesting story; we saw a reduction in the net short position in the week to July 9th, reducing the net position by 8,074 contracts to a -102,046. The gross short position has declined as well; the total gross short is 197,948 contracts, a decline of 1,619 contracts in the week to July 9th There has been a large amount of forward selling, but we expect the rally to continue in the coming months due to the fundamental outlook, and the gross short will increase once again. We still think the roasters are chasing the market higher and have failed to increase their cover on the dips; we expect the market to rally as we enter the deficit year.

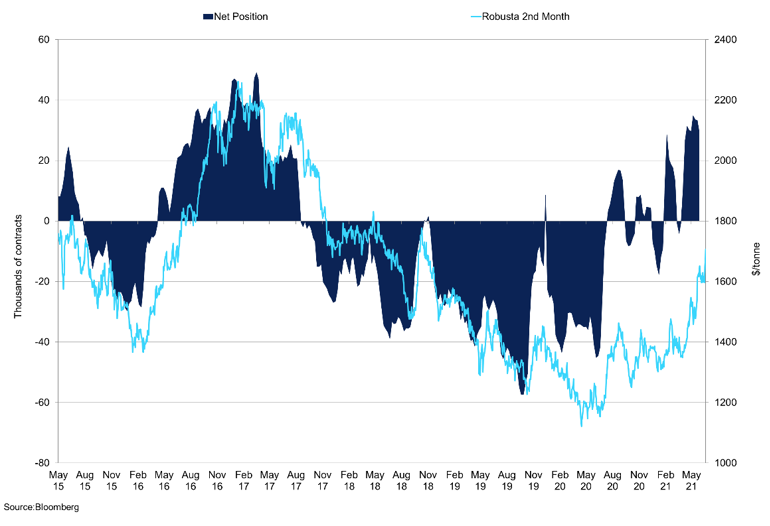

2nd Month Robusta vs Managed Money Net Change

The net position has been trending higher in recent months, but we expect a surplus in Robusta.

The Robusta commitment of traders for managed money shows an increase in the net long by 124 contracts to 30,236. The gross long for futures and options stands at 34,165, a reduction of -1,555 contracts. We also have seen more managed money traders to 43 in recent weeks suggesting improving conviction in the market. The producer net position has also declined to a net short of 44,494. The gross short has declined to 75,677; the net position was 90,290 contracts. In our view, the fundamental outlook for the Robusta market supports the downside, and we anticipate strong selling into the rallies, especially with the market.