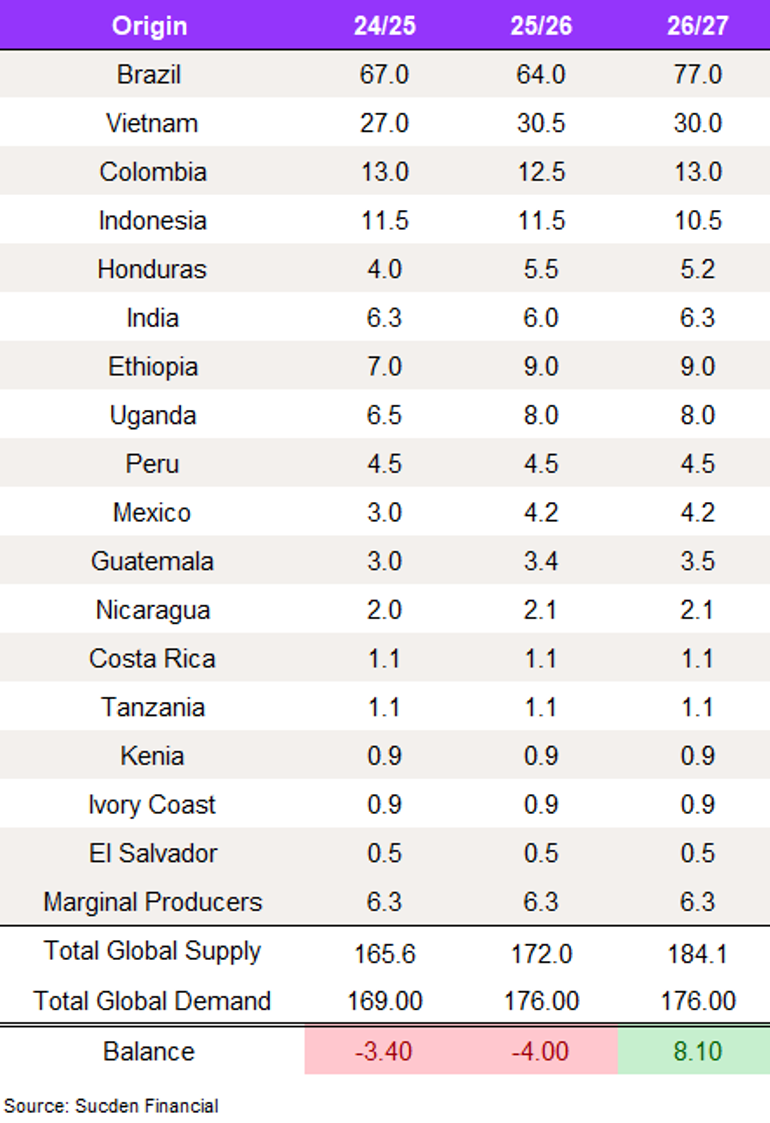

Our View

We believe the second half of 2026 will be shaped by a gradual shift from tight nearby Arabica supply towards a larger Brazilian crop. On paper, the outlook is improving: Brazil’s 2026/27 production is moving towards 77m bags and the forward balance looks more comfortable after a weak 2025/26 export pace and low certified stocks. Macro and shipping disruption have added cost and volatility, but coffee has been less sensitive than energy and broader commodities, and attention is increasingly on physical supply rather than the conflict itself.

Brazil remains the decisive driver. Carryover should improve materially if the crop reaches current expectations and exports recover. Even so, there are grounds for caution. Weather, particularly the developing El Niño risk, is the main unexpected variable that could quickly change the picture, especially for Robusta in Southeast Asia. Farmer behaviour is the other. With good cup prices averaging around BRL1,700 over the past two years, producers are under little pressure to sell aggressively, so the larger crop may reach the market only gradually.

Robusta has helped bridge Arabica tightness through substitution and firm Asian soluble demand, though Vietnam has largely front loaded exports. Other Arabica origins provide only mixed support. Overall, we see a market moving from tight nearby conditions towards a more comfortable balance, but that improvement is not assured: through August and beyond, weather and farmer selling are likely to matter more than the size of the Brazilian crop alone.

Our Supply and Demand Projections

Macro Overview

Commodity markets enter the second half of 2026 against a macro environment shaped above all by the Middle East conflict. Fighting from late February has left the Strait of Hormuz largely closed for around 100 days, triggering what the IEA describes as the largest oil supply disruption on record. Brent crude, near $62/bbl at the start of the year, spiked above $110/bbl in May and was trading near $95/bbl in early June, still roughly one third above pre-war levels. The shock has spread quickly into freight, bunker fuel, fertilisers and wider industrial inputs, with the World Bank projecting overall commodity prices to rise 16% in 2026, led by energy and crop nutrients. For agricultural markets, the transmission is mostly indirect, through logistics and farm inputs rather than direct supply loss, but it has still been enough to restore a macro risk premium across the complex.

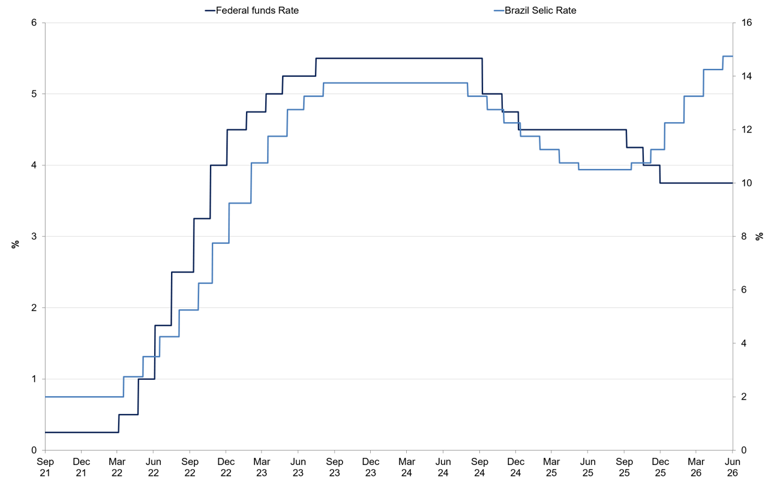

In the United States, that environment has collided with a turning point in monetary policy. Kevin Warsh was sworn in as Fed chair on 22 May and chairs his first FOMC meeting on 16 and 17 June. The federal funds target range has been unchanged at 3.50% to 3.75% since the Fed's last cut in December 2025. Markets came into 2026 expecting further easing; they have since reversed course. With energy driven price pressure building, fed funds futures now imply at least one quarter point rate hike by year end, while a hold at the June meeting is almost fully priced in. Warsh's first press conference will therefore matter as much as the decision itself, for the tone on inflation, the Fed's communication, and whether the committee is shifting from an easing bias towards a more neutral or hawkish stance. US equities have largely looked through the conflict, but for commodity markets the relevant signal is that the world's largest economy is no longer priced for easier policy.

Federal Funds Rate vs Brazil Selic Rate

Source: FRED

Geopolitical flare-ups in 2026 have added volatility to commodities, but coffee's sensitivity has been indirect and mostly lagged. When the Middle East conflict escalated in late February, the initial move in coffee came mainly through higher freight and energy costs, not through any loss of physical supply. Coffee's supply chain sits largely outside the conflict zone, and the Hormuz route carries minimal coffee volumes. The risk premium therefore worked mainly through fuel costs and shipping delays rather than direct disruption to origin supply.

Markets were quick to fade that premium once it became clear the disruptions were manageable for coffee, and focus shifted back to fundamentals, notably improving forward supply from Brazil, which has contributed to softer prices.

Another channel of geopolitical risk is trade policy. For example, the US briefly imposed a steep 40% tariff on Brazilian coffee in 2025 (later rescinded), illustrating how coffee can be pulled into international disputes. This showed that, even absent a true "trade war," tariffs can be used as bargaining tools for non-trade issues, with Brazil structurally exposed to such measures.

For now, these remain tail risks: markets generally treat isolated flashpoints as transitory. That said, any renewed escalation, whether military or policy driven, could quickly reverse this complacency, especially if freight or input costs surge again and reintroduce a macro risk premium into coffee.

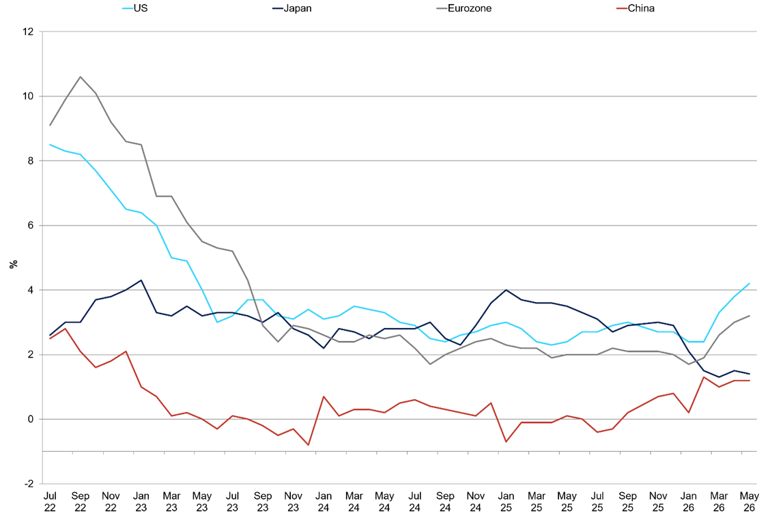

Inflation

In early 2026, the energy and freight shock described above reawakened inflation concerns across commodities, including coffee. That macro bump proved short-lived. With sizeable global coffee supplies in 2026, the market's focus returned quickly to fundamentals.

Major Economies’ Inflation

Source: FRED

Corporate results underscore coffee's resilience in this environment. In 2025, roasters like JDE Peet's saw average coffee prices jump nearly 20% to offset a surge in input costs, with only a modest ~4% drop in volume, indicating that consumers largely absorbed higher costs. On balance, at-home coffee consumption in Europe and North America has held up despite inflation, while out-of-home demand is gradually recovering as consumers adjust to new price levels.

We believe that current inflation pressure poses less of a headwind for coffee than it did a year ago. If broad inflation re-accelerates or persists well into 2027, we could eventually see some renewed demand headwinds, such as consumers trading down to cheaper blends or brewing more at home. But for now, inflation has shifted from an acute threat to a manageable factor: with roaster price rises largely behind us, coffee consumption should remain on a relatively firm footing through late 2026.

Shipments

The Hormuz disruption described above has fed through to coffee mainly via shipping rather than lost cargoes. At a time when supply chains are already stretched, that channel has become one of the most important links between politics and coffee prices.

The Strait of Hormuz is one of the world's most important maritime chokepoints, typically handling around 138 commercial vessel transits per day and underpinning roughly 3 to 4% of global container trade. It is also central to energy flows, carrying around 25 to 27% of global seaborne oil trade and close to 20% of LNG volumes, which makes any disruption immediately inflationary for freight and fuel markets. In early 2026, heightened security risks and periods of effective closure sharply reduced traffic through the strait. Major container lines suspended Gulf calls, while over 130 container vessels were temporarily stranded in or around the Persian Gulf, tightening vessel availability across global routes.

Coffee rarely transits Hormuz directly, but the indirect effects have been meaningful. Higher oil prices pushed bunker fuel costs higher, while war risk insurance premiums and emergency surcharges added hundreds to several thousand dollars per container on affected routes. At the same time, vessel diversion and redeployment lengthened transit times on key intercontinental lanes, in some cases by 10 to 20 days, and contributed to congestion elsewhere. As a lower priority agricultural cargo relative to energy and strategic goods, coffee has been more exposed to these delays.

The result has been higher landed costs, longer lead times and a more cautious, hand to mouth buying approach from roasters, particularly for nearby delivery. While these disruptions have not altered the underlying supply balance, they have reinforced short term tightness and volatility, underlining how global coffee logistics remain highly sensitive to shipping stress at critical chokepoints.

Asia Impact

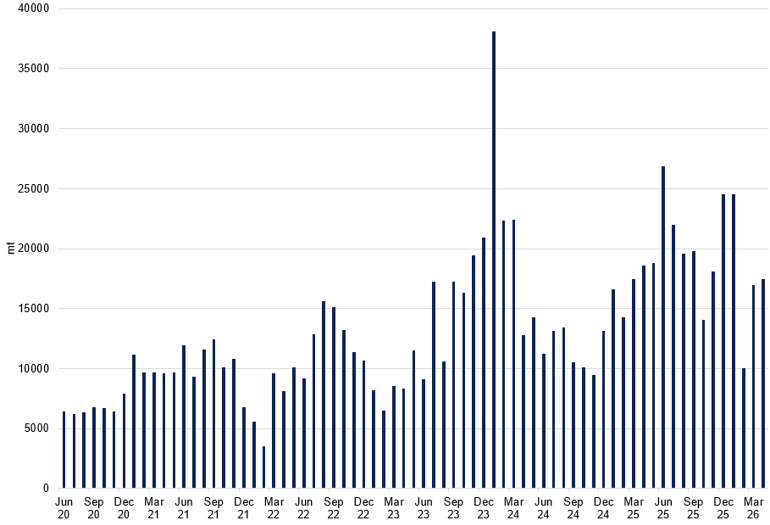

Asia’s thirst for coffee continues to grow in 2026, supporting the global demand base. Emerging Asian consumption – particularly in Southeast Asia and China – has accelerated, increasingly offsetting stagnation elsewhere. Vietnam and Indonesia now allocate significant shares of their output to satisfy their own domestic markets, estimated around 3.2m and 4.8m bags per year each. China and India, for instance, are consuming more coffee than ever before, mostly via affordable robusta-based brews and instant mixes. Major Chinese coffee chains such as Luckin continue rapid expansion, contributing to a sharp rise in import demand. In 2025, China approved 180+ Brazilian coffee firms for export, reinforcing a trend of closer Asia–Latin America trade links as Chinese buyers seek reliable green coffee supplies.

The net effect: China, India and Southeast Asia combined now account for an increasing share of global coffee demand – by our estimates, nearly 10% of world consumption. Even after adjusting for double-counted inter-origin shipments, robusta exports rose by 4–5 million bags year-on-year, reflecting a genuine switch in global usage patterns toward robusta – a shift largely fuelled by Asia’s burgeoning soluble coffee market.

China Coffee Imports

Source: Customs General Administration

Looking ahead to H2 2026, Asian coffee consumption growth appears more structural than cyclical. We anticipate further steady gains, particularly in price-sensitive segments like instant coffee. This demand growth, though not enough to create a runaway market on its own, bolsters the overall balance at a time when traditional consumer markets are plateauing, reinforcing Asia’s importance as a key engine of future coffee demand.

Weather

A potent El Niño appears to be taking shape in 2026, posing a material weather related risk to the global coffee market. Climate centres place the probability of El Niño conditions at around 80% by mid 2026, rising to above 90% later in the year. Sea surface temperatures have accelerated sharply, with roughly a 2% rise in April alone, pointing to rapid Pacific warming. Some models even raise the prospect of a ‘super’ El Niño, comparable to the extreme 1982–83 or 1997–98 events, although confidence in such an outcome remains limited at this stage.

If a strong El Niño materialises, Southeast Asia is likely to be most exposed. Vietnam and Indonesia typically experience reduced rainfall and higher temperatures during El Niño phases, increasing drought stress and curtailing yields. The timing is particularly sensitive: Vietnam’s next crop enters a critical development phase in September–October, meaning prolonged dryness through mid 2026 could directly impair the upcoming Robusta harvest. Indonesia, where production has expanded in recent years, remains similarly vulnerable given its high sensitivity to short term weather conditions.

Elsewhere, impacts are more nuanced. Colombia and parts of Central America face the risk of erratic rainfall, which can disrupt flowering and complicate arabica crop cycles. In contrast, Brazil’s near term outlook remains relatively constructive, supporting expectations for a near record 2026/27 crop of around 75–77m bags. This provides an important buffer for the global balance. That said, attention is already shifting to the August–October flowering window. Irregular rainfall or excessive heat during this period would matter less for the current crop, but could undermine yield potential and quality in 2027/28, extending weather risk beyond the immediate horizon.

Overall, we believe that Robusta appears more exposed to El Niño driven disruption than arabica, reflecting the geographic concentration of supply in climate sensitive regions. While producers are gradually expanding into new areas and higher altitudes to diversify climate risk, these adjustments will take time to materially reduce volatility. One under appreciated implication is that even modest weather shocks could have an outsized impact on differentials and nearby spreads, given already low inventories and limited spare capacity in Robusta heavy origins. As a result, the remainder of 2026 and early 2027 will require close monitoring of weather developments across Vietnam, Indonesia and Colombia, with El Niño intensity likely to be the key driver of supply risk and market volatility by the end of the year.

Fertiliser

A precarious global fertiliser backdrop has emerged in 2026, but any major impact on coffee yields is likely to be felt in 2027 rather than this year. Disruptions to Middle East output and logistics – from a region that normally supplies around one-third of the world’s nitrogen fertilizers – have already driven urea prices roughly 50% higher. With nitrogen an essential input that cannot be skipped without eroding yields, coffee farmers have been reluctant to cut application rates for the current season. Major producers like Brazil reportedly moved early to secure their needs, so immediate production in 2026 is not expected to suffer even as margins tighten.

However, if fertiliser supply remains constrained or costs stay elevated into late 2026, the risk of under-application grows, particularly among smaller growers. Any broad pullback in nitrogen use would likely curtail the 2027 harvest, given the lagged impact of nutrient shortfalls on coffee yields. In the clearest escalation scenario, a prolonged Gulf shipping blockade or prolonged export restrictions could prevent replenishment of global stocks, forcing deeper cutbacks in farm inputs. Under that scenario, the market would likely start pricing in a 2027 supply shortfall well in advance – for instance via wider robusta and new-crop differentials – as participants anticipate fertilizer-driven yield loss before it is fully visible in production data.

Corporate Earnings

Nestle

Nestlé posted better-than-expected first-quarter 2026 sales growth, with organic sales up 3.5% vs 2.4% consensus. Crucially, coffee remains a pillar: coffee was the primary growth driver in Q1, with organic sales surging ~9.3% (3.5% volume growth, 5.7% pricing). Management again described coffee demand as “resilient”, noting broad-based momentum across brands, particularly Nescafé. Despite lingering cost pressures (energy, freight), Nestlé maintained its full-year outlook of 3-4% as consumers continue to absorb higher prices. The company is leaning on coffee as a steady growth and pricing engine but acknowledges that commodity costs and pricing headroom are key watchpoints for sustaining volume growth.

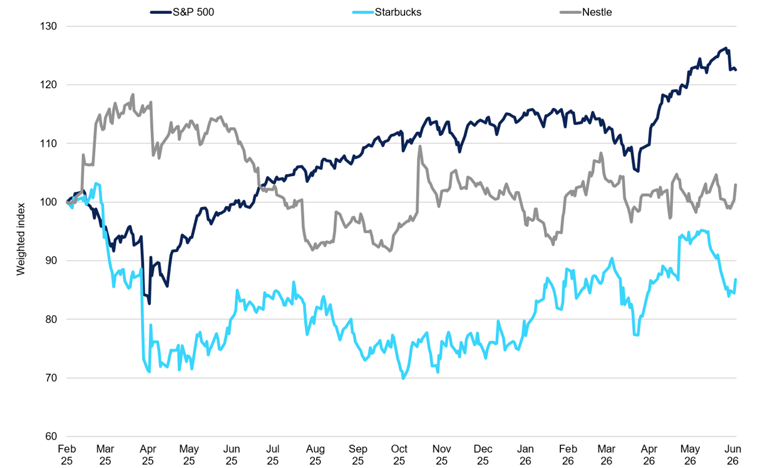

Starbucks

Starbucks delivered a solid turnaround in its latest quarter (Q2 FY2026). Global same-store sales rose 6.2%, fuelled by a second straight quarter of higher customer traffic. North America led the improvement: US comps jumped +7.1%, marking the best traffic growth in years. Encouragingly, Starbucks raised its FY2026 outlook for comp sales and EPS following these gains. The story outside the US was more mixed: international comps rose 2.6%, as China’s performance remained subdued (same-store sales just +0.5%). The chain has relied on heavy discounting in China to boost footfall, yielding +2.1% higher transactions but a –1.6% dip in average ticket. That helped return China to positive comps, but at the expense of margins. Overall, Starbucks’ results indicate that out-of-home coffee demand is rebounding, especially in its core US market, even as cost controls and competitive pressures, particularly in China, keep profit growth in check.

Normalised S&P vs Nestle vs Starbucks Relative Performance

Source: S&P Global

Luckin

Luckin Coffee continues to report breakneck growth. Q4 2025 revenues climbed 33% YoY to RMB 12.8 billion, capping a full-year sales increase of 43%. Luckin added 8,700 net new stores in 2025, ending the year with 31,048 stores (roughly triple Starbucks’ China store count). Average monthly customers grew by 26% YoY, underscoring how successfully Luckin has popularised coffee as a high-frequency, mass-market beverage in China. This expansion has come with intense competition and margin trade-offs. Luckin’s same-store sales returned to modest growth of +1.2% in Q4, but store-level margins compressed amid promotional activity. The firm’s strategy prioritises scale and market share: it has even locked in long-term procurement deals for Brazilian coffee to secure supply for its growing footprint. In short, Luckin’s rapid rise highlights structurally strong demand in China’s coffee market, albeit driven by aggressive pricing and expansion as it squares off against global rivals on home turf.

Supply

Brazil

Brazil is moving into the centre of the coffee balance for 2026/27. The 2025/26 crop is still estimated at around 64m bags, with exports for July to April at 32.234m bags. May exports are expected to finish close to 3.0m bags, with June also estimated at around 3.0m bags, taking total 2025/26 exports to about 38.2m bags. This would be below both the three-year average of 43.2m bags and the six-year average of 42.4m bags, highlighting how tight nearby availability has remained despite the size of Brazil’s underlying crop.

Internal consumption is estimated at 21m bags, leaving carryover at the end of June 2026 at around 4.8m bags. While this is not a large figure, it provides some cushion ahead of the new crop. The focus has now shifted to 2026/27, where production estimates have been revised higher. Earlier expectations of 72–73m bags have moved towards 76–77m bags, with some estimates circulating closer to 79m bags. Weather has been supportive for crop development, and the producing area has expanded by around 3%. On this basis, a 76–77m bag crop looks reasonable at this stage.

If Brazil produces around 77m bags in 2026/27 and carries in 4.8m bags, total availability would be close to 81.8m bags. Assuming exports recover to around 43m bags and internal consumption remains at 21m bags, carryover by the end of June 2027 could rise to around 17.8m bags. This would mark a significant improvement in Brazil’s balance sheet and would leave the country in a much stronger position than in recent years. The projected increase in availability should help cushion the market against some weather risk, although it does not remove the risk entirely.

Brazil Exports MoM

Source: ICE

The more important question is how Brazilian farmers behave in this environment. They are in a much stronger financial position than in previous cycles. Fine cup Arabica was quoted around BRL390 per 60kg bag in March 2019; over the past two years, good cup prices have averaged around BRL1,700. At those levels, farmers are under little pressure to sell aggressively.

This makes farmer selling the key variable for the second half of the year. If the Brazilian farmer chooses to sell steadily, the market should be able to absorb the new crop without severe disruption. If farmers panic and sell more aggressively, the pressure on Arabica could build quickly and the Arabica/Robusta arbitrage could narrow further. For now, Brazil looks more comfortable than it did last year, but the flow of coffee into the market will matter as much as the size of the crop itself.

There is still a timing issue. The new crop comes on stream from early July, but it takes time for coffee to ripen, be harvested, prepared and shipped. Roasters also tend to avoid the very first pickings, as the coffee is often too fresh and needs time to mature. As a result, the nearby tightness could last through July and into August before the market starts to feel the full benefit of the larger Brazilian crop. After August, availability should begin to ease for the industry.

Weather remains the main risk. The potential for El Niño-related disruption has not disappeared, and the next three to four months will be important for crop development. That said, Brazil’s larger crop and improving carryover mean the market is better placed to deal with adverse weather than it was in previous tight years. If weather remains favourable and farmer selling increases, coffee could continue to move slowly lower. If weather turns adverse, the market could quickly recover from lower levels.

Other Arabica Origins

Other Arabica origins have helped ease some of the pressure on the market, although the picture is mixed. Central America shipped well during the 2025/26 season. Honduras exports increased by around 989,000 bags in the six months from October to March, while overall regional exports rose by around 1.312m bags. This provided useful additional supply at a time when Brazil’s export flow was running below average.

Colombia has been weaker. The 2025/26 crop is estimated at around 12.5m bags, with exports from October to April at 6.492m bags. Internal consumption is estimated at 2.6m bags, or around 216,666 bags per month. On this basis, around 4.5m bags are left for the final five months of the crop year. Weather issues have slowed exports, with shipments around 1.194m bags lower in the first six months of the 2025/26 crop year.

Colombia Coffee Monthly Exports

Source: Federal Naccional Cafetero, Banco Central de la Republica

The slower Colombian flow matters because it limits the amount of Arabica supply available outside Brazil. While Central America has performed well, there does not appear to be much carryover from other Arabica origins. Most of the available coffee has already moved or has been committed to the industry. As a result, the market remains dependent on Brazil’s new crop arriving smoothly and on farmers releasing coffee at a steady pace.

Overall, the Arabica balance is improving, but the improvement is heavily concentrated in Brazil. Other origins have provided some support, especially Honduras, but they are unlikely to generate enough surplus to materially change the broader balance. This leaves Brazil as the main driver of Arabica availability through the second half of 2026.

Robusta

Robusta supply has played a crucial role in covering the tightness in Arabica. ICO shipment data show Robusta exports from April 2025 to March 2026 at 59.845m bags, compared with 51.918m bags in 2024/25. Some of this increase may reflect double counting, with coffee moving from Indonesia to Vietnam and from Brazil to Colombia, possibly accounting for around 2–3m bags. Even allowing for that, around 4–5m bags appear to reflect a genuine switch by the industry from Arabica to Robusta.

This switch has been driven by both price and demand. The Arabica/Robusta arbitrage moved as wide as around 190 cents last year, compared with a more normal range of 35–45 cents. It remains elevated, with the September/September arbitrage around 93 cents and the July-September Arabica spread trading at around a 100-point premium. This has encouraged the industry to use more Robusta where possible, particularly for soluble coffee. Demand from China and India remains focused on soluble, and around 70–80% of Vietnam’s Robusta is linked to this market.

Arabica Robusta Active Arbitrage Price

Source: Bloomberg

Vietnam has filled part of the supply gap, but availability is now more limited. The 2025/26 crop is estimated at 29.5m bags, with exports from October to April at 21.095m bags. Internal consumption is estimated at 3.2m bags. A large share of the crop has already been sold, leaving around 4.5m bags for the final months of the crop year and the region is now entering the quieter part of the cycle ahead of the new crop in September–October.

Brazilian Conillon also remains important. The 2026/27 Conillon crop is estimated at around 25m bags. Brazil’s Robusta availability should improve with the new crop, but the market still needs to see how much coffee farmers are willing to release and how quickly it moves into export channels.

Indonesia is unlikely to keep shipping at the same pace. Production has previously moved from around 6m bags to as high as 9–10m bags, but output is expected to be lower this time. This limits the scope for Indonesia to repeat the strong contribution it made to Robusta availability in the previous cycle.

The Robusta market is therefore better supplied than it was, but not loose. Vietnam has already front-loaded a large share of its crop, Indonesia is expected to slow, and Brazil’s larger Conillon flow still needs to come through. The arbitrage should continue to narrow, potentially towards 70–80 cents, if Robusta demand remains strong and Brazil’s Arabica crop moves smoothly. A sharper narrowing would likely require more aggressive Brazilian farmer selling, as discussed above.

Consumption

Global coffee consumption remains firm, but the composition of demand has changed. Total production is estimated at 172.189m bags, while consumption is estimated at around 176m bags. This implies that the global balance remains tight, even though Brazil’s next crop should improve the forward supply picture.

The main shift has been increased Robusta usage by the industry. The wide Arabica/Robusta arbitrage outlined above has encouraged substitution, especially in soluble coffee, with an estimated 4–5m bags switching from Arabica into Robusta after adjusting for possible double counting in trade flows. Demand from China and India has helped absorb a larger volume of Robusta exports from Vietnam and other origins.

This substitution has helped manage high Arabica prices, but it also means that Robusta demand is now more structurally important. If the arbitrage remains wide, the industry is likely to continue favouring Robusta where quality and product mix allow. If the arbitrage narrows further, the pace of substitution may slow, but it is unlikely to reverse quickly given the strength of soluble demand.

Consumer demand has not shown clear signs of collapse. The market has absorbed strong shipments without building meaningful certified stocks, which suggests coffee continues to move into consumption. Wholesale prices have eased from earlier peaks, so the pressure on demand from very high coffee costs looks less acute than it did during the tightest phase of the market. For now, the more visible change is not weaker overall demand, but a shift in the type of coffee being used.

Inventories

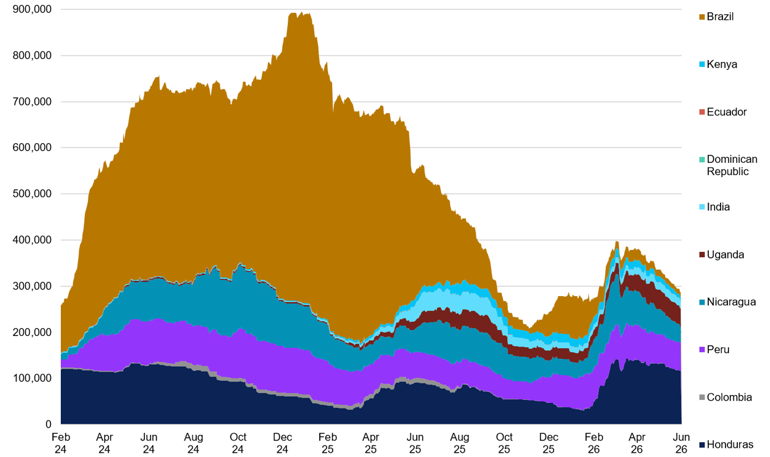

Coffee Inventory Levels per Location

Source: ICE

Certified stocks remain tight. Arabica certified stocks started 2026 at 452,906 bags, while Robusta certified stocks started the year at 4,210 lots. As of 10th June, certified stock levels are 409,897 bags and 3,713 lots. Grading activity increased in March, but there is now little additional coffee in the grading pipeline. Much of the coffee that was available has already been sold to the industry, leaving limited scope for a meaningful nearby rebuild.

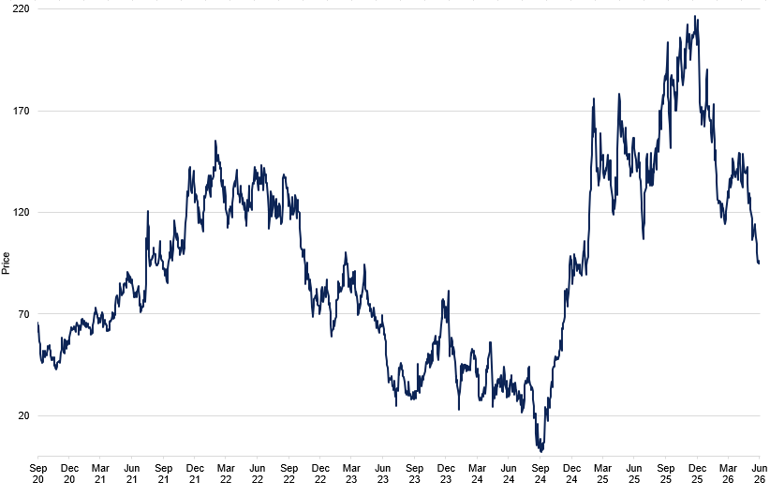

The first half of 2026 was defined by tight supply and very wide arbitrage levels. The second-month arbitrage was around 192.10 at the start of the year, reflecting concern over limited availability. Vietnam, Central America and substitution into Robusta have helped ease pressure on the physical market, but certified stocks are unlikely to rebuild meaningfully until Brazilian coffee arrives in volume after the usual July–August lag.

The key inventory question is whether Brazil’s larger 2026/27 crop can translate into working stocks and certified supply. On paper, the forward Brazilian balance improves sharply, as set out above, but the rebuild depends on execution: favourable weather, a smooth harvest, and sufficient farmer selling into the market. If weather dries up or El Niño concerns intensify, prices could fall towards 200 cents/lb and then recover quickly. If the crop moves smoothly and farmer selling increases, the market should remain under gradual downside pressure.

Overall, inventories are still tight today, but the forward picture is improving. Brazil is no longer in the same vulnerable position as last year, and the 2026/27 crop should ease the market once coffee begins to arrive in volume. Until that point, the transition period through August remains the main inventory risk for the industry.

COT

Softs

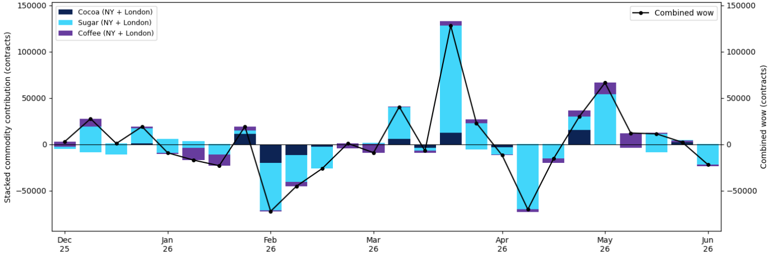

Futures positioning has become more important as the market moves from tight nearby supply towards a potentially larger Brazilian crop. The COT data capture how speculators and commercials are responding to that transition across softs, not just in coffee.

Across cocoa, coffee and sugar, NY and London combined, non-commercial positioning has been volatile but directionally informative. Non-commercials remain net short on a combined basis, at around 72,264 contracts as of the week ending 2 June, but that is a much less extended short than the 172,821 contracts recorded in mid-April. Much of the improvement came through May, when non-commercials reduced shorts in four consecutive weeks, with combined short covering of 66,515, 12,238, 11,354 and 2,298 contracts respectively. That pattern was consistent with a market gradually adjusting to better forward supply rather than continuing to build bullish exposure at elevated levels.

The latest report interrupted that trend. In the week ending 2 June, combined non-commercial positioning moved back towards a larger net short, with a 21,881-contract increase in net short exposure. Commercials moved in the opposite direction, adding 23,154 contracts of net length on a combined basis. Coffee played only a modest part in that reversal. The move was dominated by NY sugar, where non-commercials added around 27,413 contracts of net short and commercials added around 28,407 contracts of net length. Cocoa and coffee non-commercial changes were comparatively small.

Softs Combined Speculative Positioning Weekly Change

Source: Commodity Futures Trading Commission

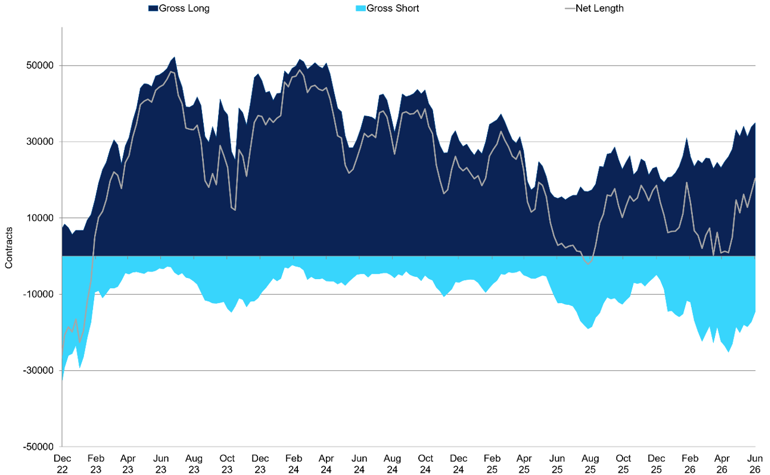

Arabica

In Arabica, non-commercials remain net short 17,312 contracts. That is not a particularly extreme position in itself, but the recent path matters. Through May, specs covered part of that short as the market began to price a larger Brazilian crop and less immediate tightness. Non-commercial net shorts narrowed from around 20,234 contracts in early May to roughly 12,981 contracts by mid-May. Since then, the tone has shifted slightly the other way. In the two weeks to 2 June, non-commercials added back around 1,824 contracts of net short, leaving them modestly more bearish than at the May low.

Arabica Specs Positioning

Source: Commodity Futures Trading Commission

That fits the broader supply narrative. The market is not positioned for an aggressive bullish squeeze on Arabica, but neither has it fully committed to a sustained bear trend. Specs appear to be trading the transition: some short covering when the forward balance improved, followed by cautious re-building of shorts as prices eased and as the July–August arrival window still lies ahead. Arabica positioning therefore looks more neutral-to-cautious than outright bullish, which is broadly consistent with a market waiting to see how much coffee Brazilian farmers actually release.

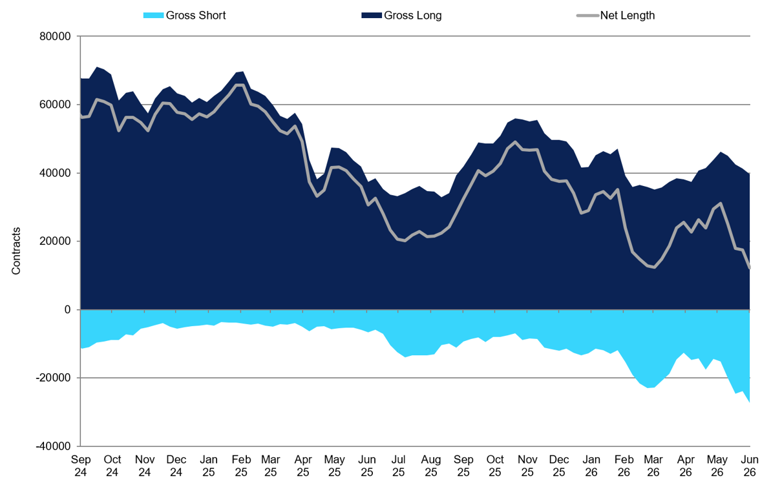

Robusta

Robusta positioning has shown a clearer adjustment. Non-commercial net exposure on London Robusta stood at 8,401 contracts short as of 2 June, compared with around 29,132 contracts short at the end of April. That is a meaningful reduction in bearish spec exposure over a period when the industry was switching towards Robusta and when Vietnam, Central America and Brazilian Conillon helped cover Arabica tightness. In the latest week alone, non-commercials covered a further 2,792 contracts, continuing the recent pattern of short reduction rather than fresh speculative buying.

Robusta Positioning

Source: Commodity Futures Trading Commission

This is the more decisive coffee-specific message in the COT data. Robusta specs have been unwinding bearish bets as the substitution story has played out and as Robusta exports remained strong. The position is still net short, so the market is not positioned for a sharp Robusta squeeze, but the trend in non-commercial positioning supports the view that much of the bearish Robusta trade had already been expressed. That aligns with the narrowing Arabica/Robusta arbitrage discussed above.

Commercials

Commercial positioning tends to move as the mirror image of non-commercial flows, and that has been visible again in coffee. On NY Arabica, commercials remain net long 17,227 contracts, with a 1,936-contract increase in the latest week. That is a relatively stable band, suggesting commercials have not been aggressively lifting hedges despite the improving forward supply picture. On London Robusta, commercials, proxied by Producer/Merchant accounts, remain net short 25,281 contracts, and that short has become more extended over recent months as non-commercials have covered. In the latest week, London Robusta commercials added a further 597 contracts of net short.

Taken together, the commercial side of coffee positioning supports the physical-market story more than the speculative one. NY commercials have maintained a steady net long position, while London commercials have remained structurally short, consistent with origin and trade hedging remaining active even as specs have reduced bearish bets in Robusta. The sharp commercial lengthening in the latest combined softs report was again mainly a sugar story rather than a coffee one.

Overall, positioning does not yet suggest that the market has fully bought into a smooth, bearish transition in Arabica. Robusta non-commercials have adjusted more clearly, which fits the substitution and export flow seen in the physical market. Commercials remain more willing to sell or hedge into the market than specs are to chase rallies. For the second half of the year, the more important variable remains the same as in the physical balance: not just how large Brazil’s crop is, but how quickly that coffee, and how much of it, actually reaches the market. The COT data suggest specs remain cautious about execution risk, without positioning for a sharp move lower.