Executive Summary

- Despite high interest rates, the US economy remains strong, driven by robust consumer spending.

- We believe that if the rate cut does not occur in September, the Fed will likely postpone the cuts to December, given that an intervention during the election month is improbable.

- The ECB is expected to cut rates by over 50bps this year, with the first cut already taking place in June, creating headwinds for the euro.

- In the US, significant price increases at major coffee chains are discouraging consumer purchases; high prices, driven by inflation and wage increases, are the main deterrents.

- Southeast Asia, particularly China, has experienced a remarkable increase in coffee consumption and imports.

- Although we believe the underlying market fundamentals have not changed drastically, shifting market perceptions concerning the supply side tightness have driven recent price rallies.

- Producers have been selling into these rallies, preferring to capitalise on price strength rather than sell into market weaknesses.

- While we expect the near term to remain bumpy, our longer-term forecast remains moderately bullish.

- Although this is primarily a Robusta story, Brazil's Arabica market has experienced increased volatility due to weather-related supply concerns, coupled with rising speculative demand linked to cocoa supply issues.

- Our view of Vietnam is cautious but not concerned as of yet. In our view, the weather is the overriding factor in our crop analysis.

- Moreover, growing durian proved significantly more financially rewarding for the farmer than coffee cultivation, leading to the neglect of replanting old trees.

- Although the precise market impact of EUDR remains to be fully assessed, we anticipate that there will be significant attention from investors regarding how this regulation unfolds and its effects on global supply chains.

- It seems unlikely that the existing stockpile will be sufficient to meet the ongoing demand. We expect that all the exports will go to the industry instead.

- Brazil’s ability to keep the exports going will be crucial in determining the Arabica narrative in the coming months.

Our View

The coffee industry has experienced significant volatility in recent months, breaking out of the stagnant price ranges observed since October. Although we believe the underlying market fundamentals have not changed drastically, shifting market perceptions concerning the supply side tightness have driven recent price rallies. This trend has been exacerbated by ongoing dryness in Vietnam, causing Robusta prices to test a new high at $4,338/mt, subsequently affecting Arabica prices as well. Broader volatility in the softs market is also adding to coffee price volatility.

Producers have been selling into these rallies, preferring to capitalise on price strength rather than sell into market weaknesses. Historically low stocks and roaster coverage indicate that roasters are purchasing on a hand-to-mouth basis. While we expect the near term to remain bumpy, our longer-term forecast remains moderately bullish. In our view, the weather is the overriding factor in our crop analysis. Brazil’s ability to keep the exports going will be crucial in determining the Arabica narrative in the coming months.

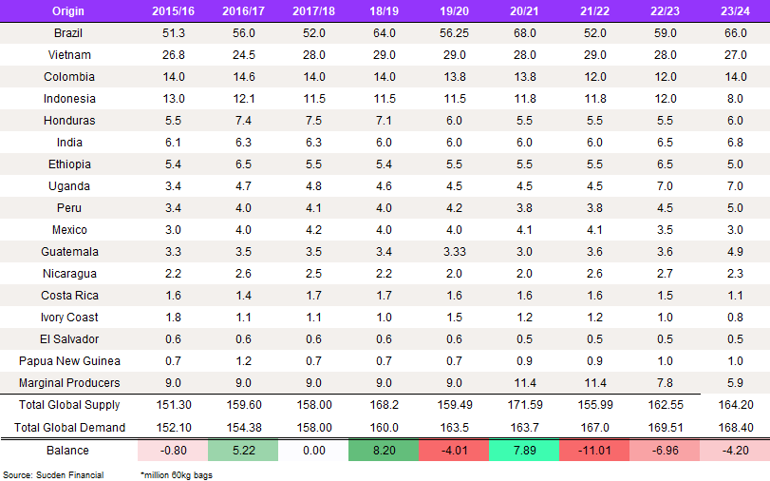

Analysing the recent Brazilian export data, we estimate Brazil will ship 45m bags in the 2023/24 crop year. Our production number of 66m remains unchanged, and we estimate 22m bags for internal consumption, which would leave a deficit of 2m bags. For 2024/25, we expect 69m bags; early indications suggest a lower yield and smaller bean size; however, at this time, we would caution that only 10 to 15% of the crop has been harvested. We are also paying attention to the logistical situation in Brazil and the demand for containers.

Assessing the overall damage to Vietnams 2024/25 crop remains challenging, as we enter the traditional rainy season, but the impact on 2023/24 is clear, with an estimated 2m bag reduction to our crop number from 29m to 27m. Some reports estimate a 20% damage to the 23/24 crop, however, we feel currently that number seems on the high side at this point of time.

Macro Overview

US

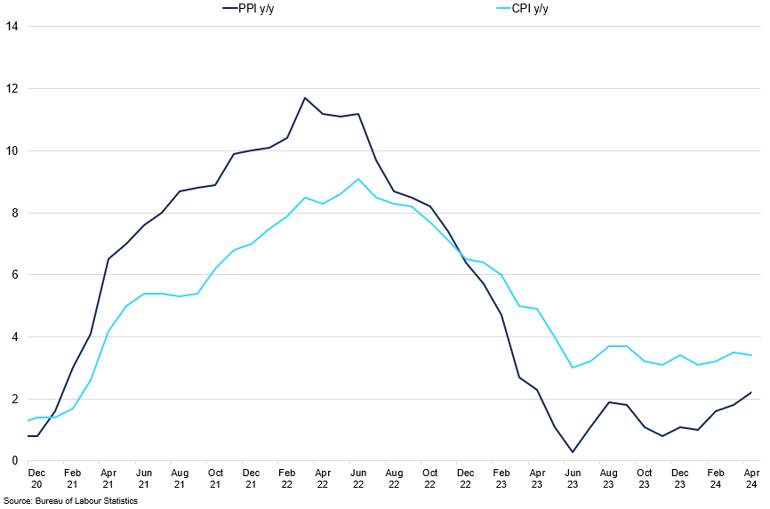

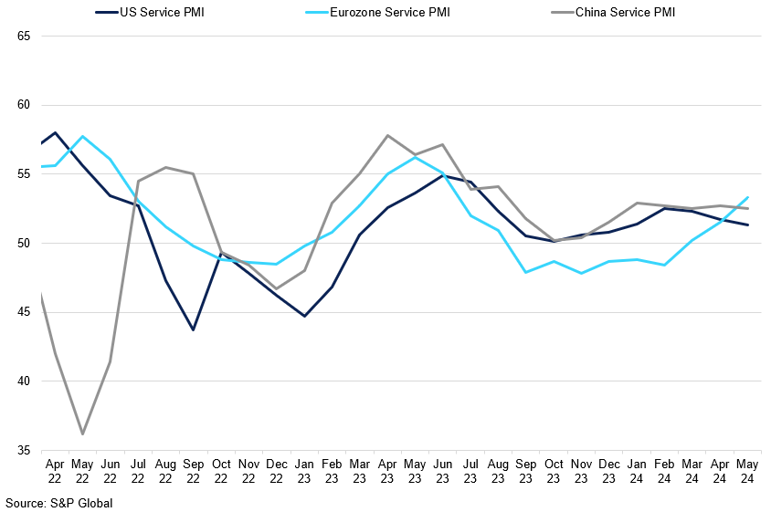

Despite high interest rates, the US economy remains strong, driven by robust consumer spending. Although final GDP growth in Q1 2024 came in lower than expected at 1.6% QoQ, this was largely due to a surge in imports to meet strong domestic demand. May's PMI data showed the highest business activity since April 2022, led by the service sector. Rising input costs and output prices indicate businesses are passing higher costs to consumers, complicating efforts to reduce inflation to 2%. Sticky CPI prints and rising shelter costs, up 5.5% YoY in April, challenge the Fed's inflation targets. Positive economic data and persistent inflation delay expected rate cuts to Q4 2024. We believe that if this rate cut does not occur in September, the Federal Reserve will likely postpone the initiation of monetary easing until December, given that an intervention during the election month is improbable. Considering these factors, maintaining a careful balance between fostering economic growth and managing inflation will remain a crucial challenge for policymakers in the coming months.

US PPI vs CPI

Inflation remains sticky at the current levels.

Europe

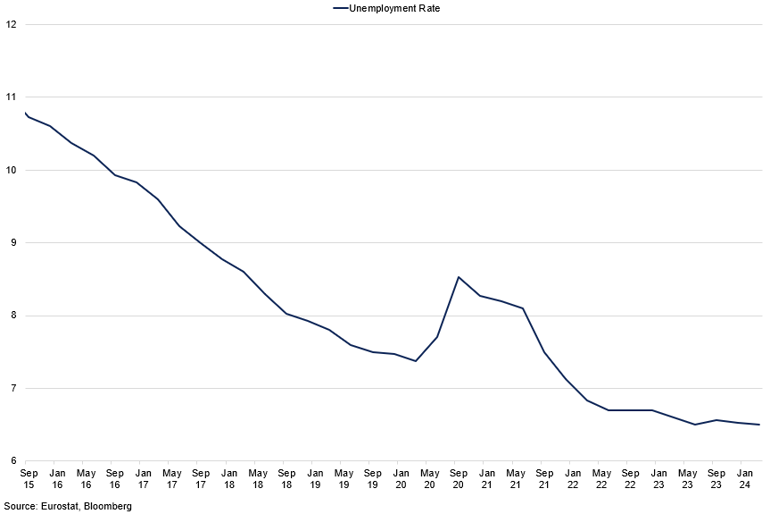

The Eurozone's outlook is improving, with Q1 2024 GDP growth at 0.3% QoQ and 0.5% YoY, driven by Germany’s return to growth and a strong expansion in Spain. Retail sales, a key indicator of consumer's propensity to spend, rebounded 0.8% MoM in March following an upwardly revised decline of 0.3% in February. It was the largest increase since September 2022, showing encouraging signs of recovery in household consumption. Similarly, in line with the US, private sector activity in the Eurozone demonstrated promising growth in May, fuelled by strong expansion in the services sector and a reduced contraction in manufacturing. Inflation remained flat in April at 2.4% YoY, with conflicting pressures from wage deceleration and high service costs. The ECB is expected to cut rates by over 50bps this year, with the first cut already taking place in June, creating headwinds for the euro.

Eurozone Unemployment

Eurozone unemployment hovers at a historically low level.

China

While last year everyone was waiting for China to rebound from the post pandemic slump, reduced expectations regarding the world’s second-largest economy have now became the norm. Sluggish domestic demand, reflected in weak retail sales and a struggling property sector, drags growth. In Q1 2024, a decline of real estate development investment widened to 9.5% YoY, suggesting continued weakness in the sector. In April 2024, new home prices fell 3.5% YoY, with existing home prices down nearly 7% YoY. Premier Li set a 5% growth target for 2024, with measures to support property and local governments. The latest measures will enable local governments to direct state-owned enterprises (SOEs) to purchase completed but unsold apartments from property developers and convert them into social housing. However, SOEs may be hesitant to participate in the program due to the vacancy risks associated with repurposing units for social housing and the resale risks if they attempt to sell them later. Local governments, which own the SOEs, already carry $9 trillion in debt and would prefer to avoid acquiring additional underperforming assets. Government stimulus has so far been insufficient to boost growth, making the 5% target challenging.

S&P Services PMI

Eurozone services have rebounded recently.

Brazil

Brazil's economy likely grew by 0.7% QoQ in Q1 2024, with manufacturing and services PMIs in expansion. Retail sales exceeded expectations, with a 5.7% YoY increase. Unemployment is at its lowest since 2015, at 7.9%, with strong wage growth. April's headline inflation dropped to 3.69% YoY, allowing the central bank to cut the Selic rate to 10.50%. The recent rate cuts have weakened the Brazilian real, which was almost 4% lower against the US dollar by late May compared to a year earlier. This depreciation is partly due to expectations that the US central bank will not cut rates as quickly as anticipated, potentially slowing the BCB's rate-cutting pace. Steady growth, a strong labour market, and controlled inflation suggest a positive outlook for Brazil's economy.

Corporate Results

Starbucks

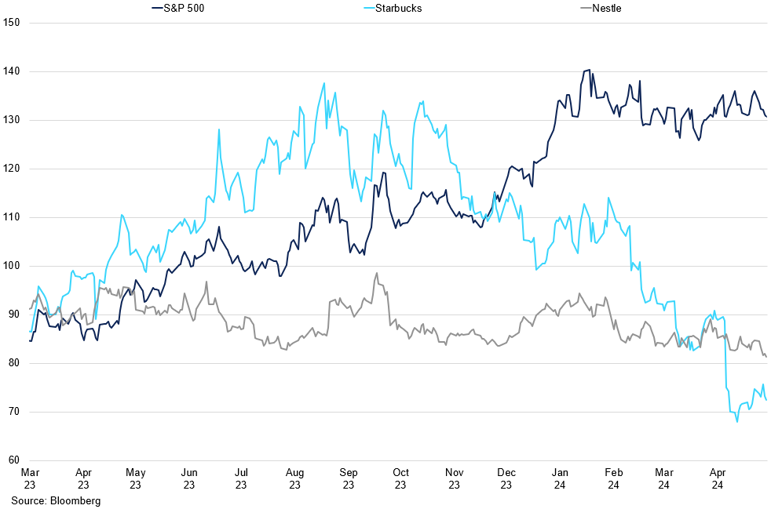

Starbucks' recent earnings report caused a market stir, with shares falling 15% to their lowest since 2022. The company reported its first drop in same-store sales in nearly three years despite higher prices. Same-store sales, crucial for measuring growth, fell by 4% in the first quarter of 2024. Average spending per transaction rose 2%, but the number of transactions dropped 6%. Consequently, Starbucks revised its full-year guidance, expecting flat or single-digit declines in same-store sales and low single-digit revenue growth. New CEO Laxman Narasimhan cited price-conscious consumers in the US and China for these declines. Intense competition from specialty coffee chains and local cafes also contributed. Despite plans to streamline drink preparation and introduce new menu items, significant sales rebound is not expected next quarter.

Starbucks vs Nestle vs S&P 500 Performance

Starbucks recent earnings report led the shares to fall to the lowest level in 2 years.

Nestle

Nestle’s organic growth was up by 1.4% in Q1 2024, much lower than 9.3% recorded in the same time last year. At the same time Real Internal Growth (RIG), which specifically measures the change in the volume of goods sold excluding any effect from price changes, was -2.0%. The company states that these lower numbers were impacted by soft consumer demand. Coffee sales saw growth at low-single digit growth, with continued momentum for Nescafe, Starbucks, and Nespresso. The latter saw organic growth at 1% with sales in North America growing at a mid-single-digit rate, with market share gains. This growth was primarily driven by the more expensive Vertuo system encompassing high tech coffee machines and a range of accessories which allow for a more personalised brewing experience. Nestle expects organic sales growth of around 4% in 2024 and a moderate increase in the underlying trading operating profit margin. However, achieving these targets might be difficult given the current market conditions and consumer demand trends.

Supply

Arabica

Although this is primarily a Robusta story, Brazil's Arabica market has experienced increased volatility due to weather-related supply concerns, coupled with rising speculative demand linked to cocoa supply issues. Although the situation for Arabica is less critical than for cocoa, weather impacts on crop yields in Vietnam and Brazil, especially recent dryness , have affected the quality and quantity of the coffee produced. While Vietnamese producers can redirect their profits towards durian, Brazil is in a tighter spot to ensure sufficient coffee yield is achieved.

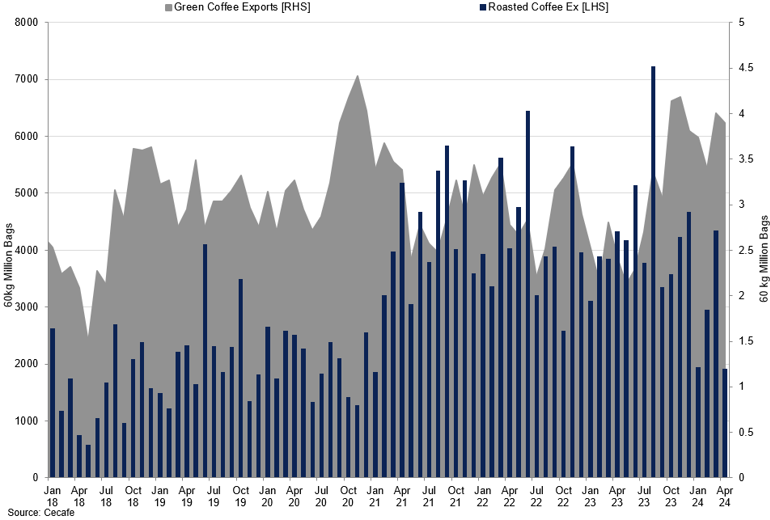

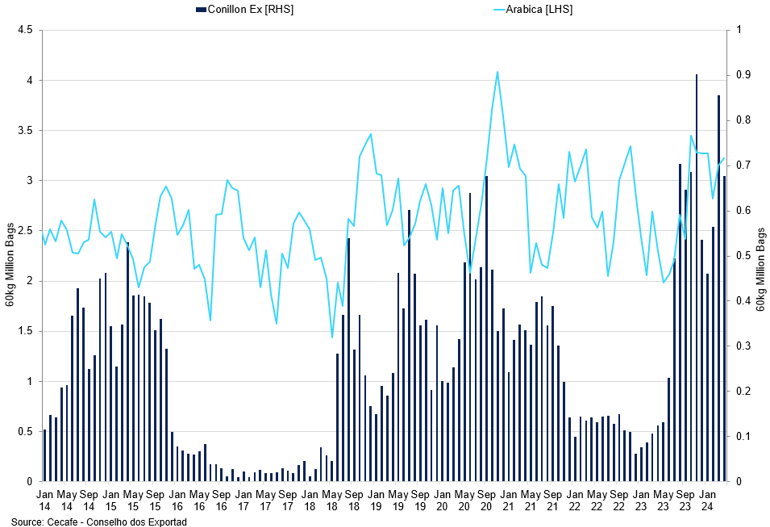

Ahead of the 24/25 crop, farmer selling has been robust, capitalising on the price gains. Brazil has shipped 39.3m bags so far this crop year, up 28.5% from the 2022/23 crop. With an internal consumption rate of 1.8m bags per month, Brazil is likely to export 45m bags by the end of June, surpassing the three-year average of 40.3m. Currently, exporters are actively seeking the most favourable hedging opportunities.

Brazil Roaster Coffee vs Green Coffee Exports

Brazil’s green coffee exports continue to remain robust.

With 22m bags used for internal consumption, we expect the 2023/24 crop to yield 66m bags, with a 44m and 22m split for Arabica and Conillon, respectively. However, Vietnam's Robusta remains crucial in guiding the Arabica narrative, and we must watch out for developments in the region to gauge the picture clearly.

Brazil is projected to produce 69 million bags in the 24/25 crop year, driven by continued tree recovery from the frost a couple of years back. Still, current weather conditions are capping the yield potential for the next crop year. With only 10 to 15% of the crop harvested, there's much progress to be made, making a 66m yield forecast, as mentioned by some analysts, appear low to us now. Moreover, farmers would probably retain some coffee if they anticipated such a low output.

Robusta

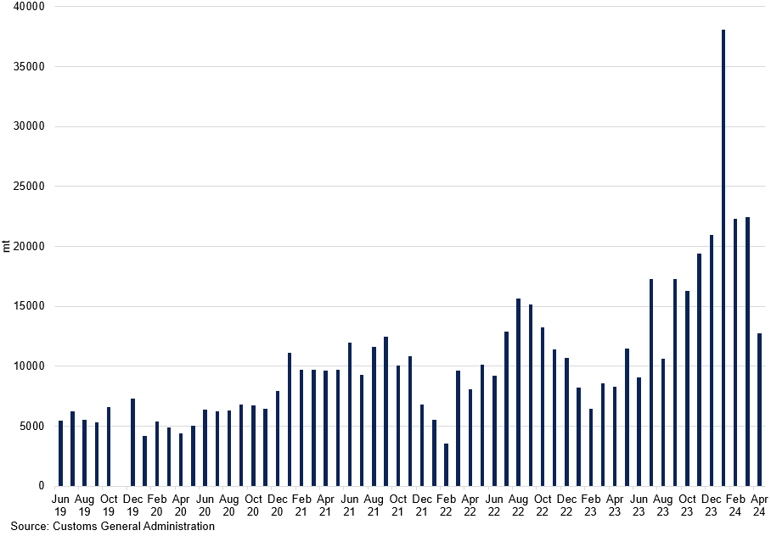

Vietnam plays a crucial role in shaping the coffee prospects in the coming months as the planting season begins. Weather conditions, especially abnormal temperatures and insufficient rain before the monsoon, have adversely affected Robusta crops, causing prices to spike. As stocks are insufficient to satisfy current demand patterns, producers charged a higher physical premium, prompting differentials to trade at $800 over the futures. Some price pressures have eased with the onset of the rainy season, though concerns remain due to inadequate rainfall. Moreover, growing durian proved significantly more financially rewarding for the farmer than coffee cultivation. This further strained coffee cultivation, leading to the neglect of replanting old trees.

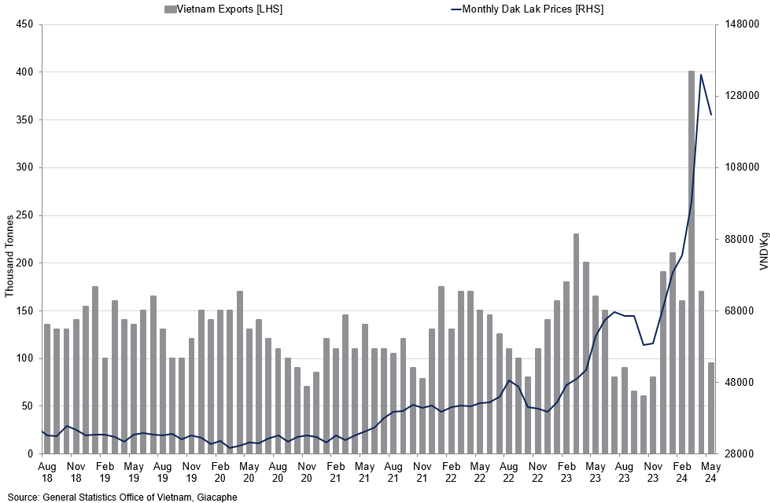

Vietnam Exports vs Dak Lak Prices

Elevated price levels prompted exports to reach new highs; the level should soften in line with cyclical performance.

Despite this, the resilience of Robusta trees and individual irrigation systems on most privately owned farms offer a glimmer of hope for yield recovery if the monsoon strengthens. Our projected loss for the 23/24 crop year is under 10%, adjusting Vietnam's production forecast to 27.0m bags, slightly below the historical average. With the last harvest completed, exports have reached 18.8m bags, and with internal consumption of 1.7m bags, that leaves 7.2m bags over the coming five months of the crop year. This indicates a tight supply until the next harvest season. Currently, only 10% of Vietnam's coffee stocks are available, with half consumed domestically. This scarcity and a weaker 2023/24 harvest prompt farmers and middlemen to hold out for higher selling prices, complicating sourcing for exporters.

Overall, our view of Vietnam is cautious but not concerned as of yet. Weather conditions in later months will be crucial to watch out for. What we have seen in recent days might be more speculative selling than any fundamental change, and our outlook remains on the cautious upside. For the 24/25 crop, we estimate 24.0m bags, meaning that around 3-4m bags are left to be shipped. With Vietnam's crop at 24.0m bags, we expect Brazil to fill the gap.

Conillon

Last year, expectations were high for a significant increase in the Conillon crop for the 24/25 season, following a recovery from several years of adverse weather conditions affecting coffee producers. However, the persistent hot and dry weather has raised concerns about the impact on the current crop's yield projections. The weather, particularly in the Espirito Santo regions, remains a concern despite some potential for rain, as temperatures are still higher than typical for this time of year. Additionally, reports of insect disease have also been noted.

As a result, our number for the 23/24 crop remains at 22m bags, unchanged from the last report. However, with Brazil's internal consumption of 12m bags and 3m bags used for soluble production, export levels will likely soften until the end of the crop year. So far, Conillon shipments from July 2023 to May 2024 are estimated at 7.2m bags. This would total a disappearance of 22.2m bags. Moreover, with shipments from April 2023 to March 2024 at 51.5m bags from Vietnam, the total availability of Robusta coffee remains in question. Hence, demand for Conillon has been partially reinstated due to potential Vietnam shortages, prompting a 2.5m additional demand as part of the replacement from milds.

Brazil Conillon vs Arabica Exports

Conillon exports remain elevated in the face of additional demand for Robusta blend.

With last year's Conillon stock mostly sold, the local market remains firm, with exporters focusing on securing offers for intermediate deliveries. A potential 5m bag shortfall in Robusta due to bad weather could significantly strain the Robusta/Conillon market, particularly as we anticipate a 69m bag Brazilian production in the 2024/25 season. Reduced production from Central America could tighten the market further. We'll closely monitor weather changes as we progress through the current crop cycle.

Consumption

In our view, the global consumption landscape for coffee remains largely stable, with notable regional variations. In the US, significant price increases at major coffee chains are discouraging consumer purchases, impacting companies like Nestle and Starbucks. High prices, driven by inflation and wage increases, are the main deterrents. In contrast, Europe shows resilience to these increases, with a notable 8% year-on-year growth in coffee consumption among the Big 5 European nations, surpassing the global average of 5%, according to Circana.

Southeast Asia, particularly China, has experienced a remarkable increase in coffee consumption and imports. In the last three months of last year, shipments into China stood at 1.5m bags from Brazil. While this trend slowed down slightly in the first four months of the year, the year-on-year trend remains robust, with 3.76m registrations, up 76% y/y, indicating a potential shift in Chinese demand trend. Meanwhile, Vietnam and Indonesia continue their steady consumption patterns despite the challenges posed by high interest rates, which discourage stockpiling by roasters, thus putting pressure on supply.

China Coffee Imports Total

The trend for higher coffee demand in China is now becoming more prevalent.

Our global coffee consumption forecast stands at 168.4m bags for the 2023/24 period, highlighting that coffee is going to the industry. Differentials at a premium underscore this. However, with a lack of capacity to sell at these levels, we expect slight tightness in the market balance in the near term.

Weather

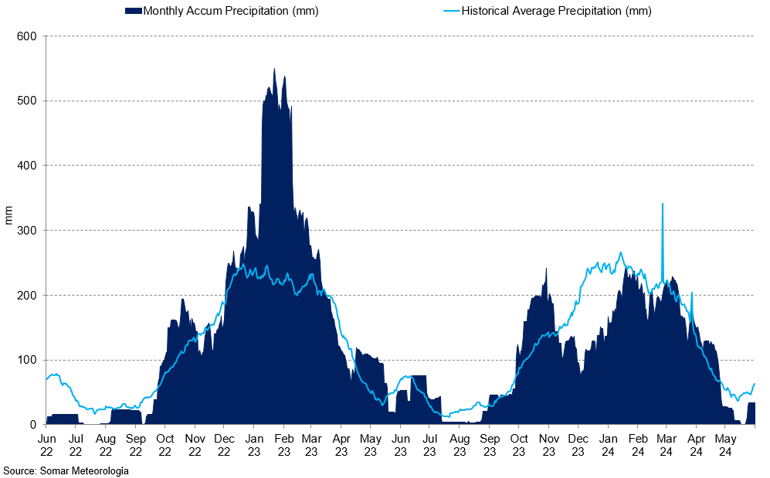

While at the start of the year, rumours about possible lower consumption generated headwinds for both Arabica and Robusta, ongoing weather issues are now creating strong upward pressure on coffee prices. We have seen strong fund buying of coffee futures due to concerns that excessive dryness in Brazil and Vietnam will damage coffee crops. In mid-May, Somar Meteorologia reported that Brazil's Minas Gerais region received no rainfall or 0% of the historical average in the week ending May 17, the fourth consecutive week. Given that the area accounts for 30% of Brazil's Arabica crop, these conditions are likely to significantly impact production levels and further drive up prices at a time when intense heat waves are sweeping through Vietnam.

Espirito Santo Monthly Precipitation vs Historical Average

Precipitation in Brazil remains below historical averages, adding further pressures on the supply side.

According to the Steering Committee for Natural Disaster Prevention and Search and Rescue of Gia Lai Province, drought and water shortages have damaged nearly 380 hectares of crops since the start of this year. On March 26, Vietnam's agriculture department forecasted a 20% decline in coffee production for the 2023/24 crop year, dropping to 1.472 MMT, the smallest harvest in four years, due to drought conditions. However, the situation is likely to improve, and we believe the resilience of the robusta trees will prevent such a significant drop in crop yield. A lot will hinge on weather patterns in the coming months. Hence, we remain cautious about potential heatwaves and heavy rains that could significantly alter Arabica's and Robusta's price narrative.

The European Union has introduced a new regulation known as the EUDR (European Union Deforestation Regulation) to address climate change and biodiversity loss concerns. This regulation is designed to promote environmental sustainability but introduces complexities for global suppliers who may face challenges adapting to Europe's ambitious environmental goals. The regulation mandates that, by the end of the year, suppliers must ensure that their products, including every coffee bean, are not sourced from lands deforested post-2020. Compliance requires detailed tracking and verification of the origin of their goods to avoid substantial penalties from the EU. Although the precise market impact remains to be fully assessed, it is anticipated that there will be significant attention from investors regarding how this regulation unfolds and its effects on global supply chains.

Inventories

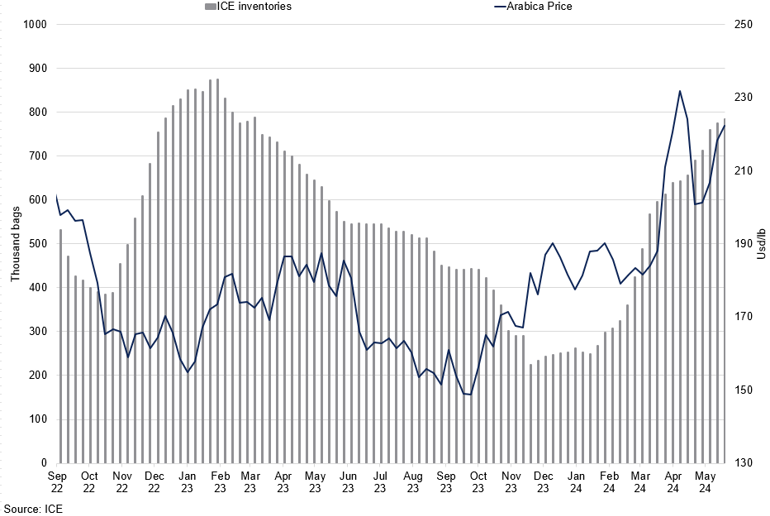

Since the start of this year, there has been a noticeable buildup in inventory levels, jumping from 250,000 to 775,000 bags, in line with 2022 highs. This increase was mainly driven by Brazil coming online and introducing new coffee to the exchange. Traditionally, this influx suggests a potential easing of supply-side pressures, especially since major coffee-producing countries had replenished their inventories from historically low levels. Despite this, prices continued to climb, fuelled by concerns over the direct supply from producing countries being more significantly threatened than the available stocks indicated. It seems unlikely that the existing stockpile will be sufficient to meet the ongoing demand.

ICE Inventory vs Arabica Price

Despite growing stock levels, Arabica prices continued to gain momentum.

Moreover, we expect the coffee currently in certified stocks to be predominantly financed. Considering the current high level of interest rates, only those capable of affording inventory financing will maintain their stocks on hold. Hence, we do not expect the in-stock coffee to be used to meet market demand. We expect that all the exports will go to the industry instead.

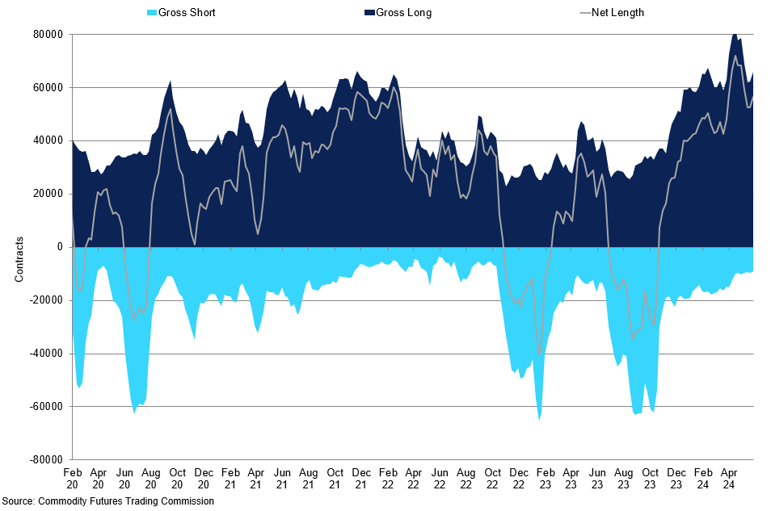

Commitment of Traders

Following the recent rally, the net length of managed money for Arabica strengthened to reflect speculative appetite, prompting the net length to reach 72,706 contracts as of April 16th, a high not seen since 2016. Short contracts remained mostly unchanged at 20,000 contracts, with a slight dip below 15,000 in recent weeks, indicating that bullish investors have taken control of the market in April. As of June 4th, the number of long contracts is in line with January averages at 60,468. We expect that the most recent rally back above 220cts/lb was brought by another round of speculative appetite. From the commercial perspective, longs have gained 10,000 lots in the last ten months, suggesting that roasters might be reluctant to purchase the futures and instead buy coffee outright.

Arabica Managed Money COT

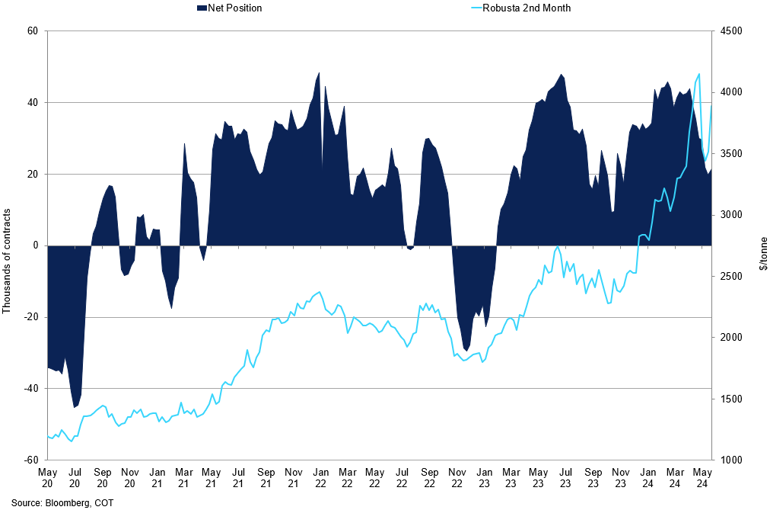

Robusta managed money positions have kept their net long elevated for the majority of this year, at around the 40,000 contract level. However, the recent price weakness, albeit small, prompted net length to contract aggressively, coming back to 20,000 contracts. We believe that the main reason behind the reduction in long positions is investors capturing the profits made from the previous upside. A resurgence of appetite in the softs complex is also contributing to increased interest in coffee.

Robusta Managed Money Net Position vs Robusta Price