The latest outlook provides an in-depth analysis of the coffee market. This includes a macroeconomic assessment of consumer and producer economies. We highlight key headwinds to the demand outlook, most notably rising inflation at a faster rate than wage growth. However, it is all about supply and the Brazilian crop, we expect more clarity in January when we can fully assess the flowering but it does not look good. Colombia has also been negatively impacted by weather and we struggle to find a region that will fill this void.

Executive Summary

- The post-lockdown recovery continued in Q3, albeit at a slower rate, as government support was phased out, and there are now talks about regarding the tightening of monetary policy next year to help ease inflationary pressures.

- Although inflation continues to accelerate, the fact that core inflation remains modest suggests tightening of monetary policy from the ECB to be premature at this stage.

- China is in a difficult position as many of its current challenges are coming from the supply side.

- New deficit-boosting plans in Brazil have increased volatility in the domestic markets and one of the most aggressive rate-hiking cycles that have already taken this year.

- In the meantime, Vietnam seems to begin to learn how to live with the virus in hopes of protecting lives as well as economic growth.

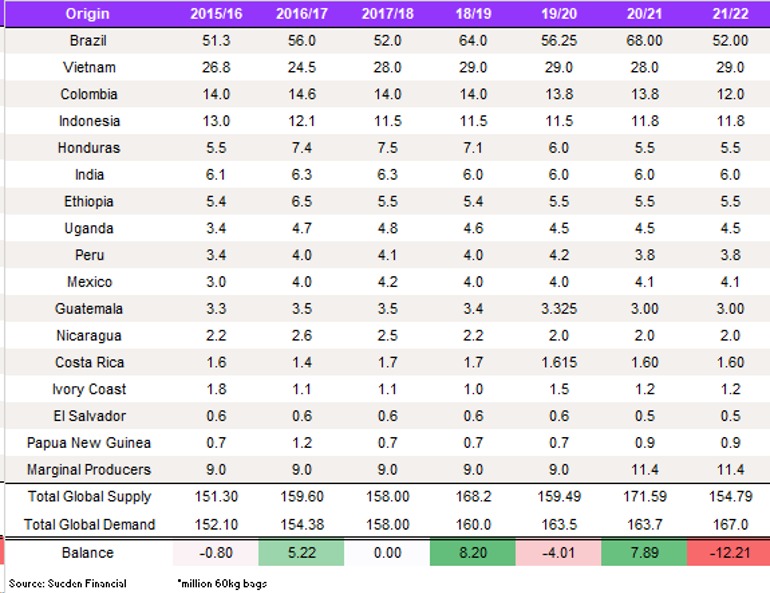

- Current crop exports 2021/July 22nd to October are 12.400m bags, up from 15.553m bags in 2020, you have a deficit of 3.153 mill bags.

- The large gross short has been large for some time, indicating farmers have been forward selling, however, the local price has doubled since the beginning of the year.

- Now the crop is 13m bags lighter, farmers have sold a larger proportion of their crop 130% below the current ESALQ Arabica coffee price index.

- There has been severe damage to the 22/23 crop as well, due to poor husbandry in Arabica areas, young trees notwithstanding the stress of the last 2 years, and mature trees not flowering at all in some regions.

- The next issue for the Arabica market is after 22/23 when we head into an off-cycle year, which is likely to be another deficit.

- We saw excess rain in Colombia this year, causing the crop to weaken.

- Our Vietnam crop number stands 29m bags for the 21/22 season, the crop has been progressing well until recently.

- We do not think the yield will be impacted at this time as the weather is improving, so this should help the harvest progress in the near term.

- However, the main issue is that due to shipping rates, exporting this coffee is expensive and there is a container shortage.

- The gross short is still high, and we expect them to be oversold, which led to traders not being able to honour contracts but also, they sold the coffee at a significantly lower price.

- The fundamental situation was too strong for inventories not to draw, however, the supply-chain dislocation has added to this pressure.

- The structure is at a premium down the curve means you cannot carry coffee; therefore it is being sold to the roasters.

Trade Ideas

- We favour buying the dips in the futures market for the Arabica, or long the Arabica structure.

- When looking at the options market, we favour owning a March 280 Call at 4.65cts as of the December 1st close, and selling a March 220 Put at 8.72cts. You would receive 4.07cts a lot.

- If NY goes to 300 and the arb reaches 180cts, Robusta would need to reach $2,645, which meaning a rally of a $388 per lot.

- Looking at Robusta options, a May 2400 Call is $81 as of December 1st, but you are paying $81 for a $150 move which is a relatively low margin.

Global Economic Review

The post-lockdown recovery continued in Q3, albeit at a slower rate, as government support was phased out, and there are now talks about regarding the tightening of monetary policy next year to help ease inflationary pressures. While inflationary spike has been larger than expected, central banks are of the belief that it is transitory and will subside in 2022, in part, with the help of higher interest rates. Supply chain disruptions have eased somewhat but remain near record highs, and strong consumer spending in the US continues to drive the number of new orders and, in turn, backlogs higher. Regardless, supply disruptions are likely to keep costs elevated. Indeed, the average wait at LA port is now more than 14 days, in comparison to 8 days in April. Will this Christmas be as bad as anticipated? It depends on whether retailers are willing to pay higher prices for bigger ships to hit their targets, significantly hurting their profit margins. We have already seen wholesale inventories in the US jump to a record high as retailers stocked up to fulfil continued demand. The supply chain bottlenecks have been further aggravated by the attempts of supply chain participants to build buffers. The supply chain problem will eventually ease, contributing to lower inflation. However, if persistent high prices boost expectations of further inflation, markets will likely act in a way that strengthens this, especially through the request of higher wages.

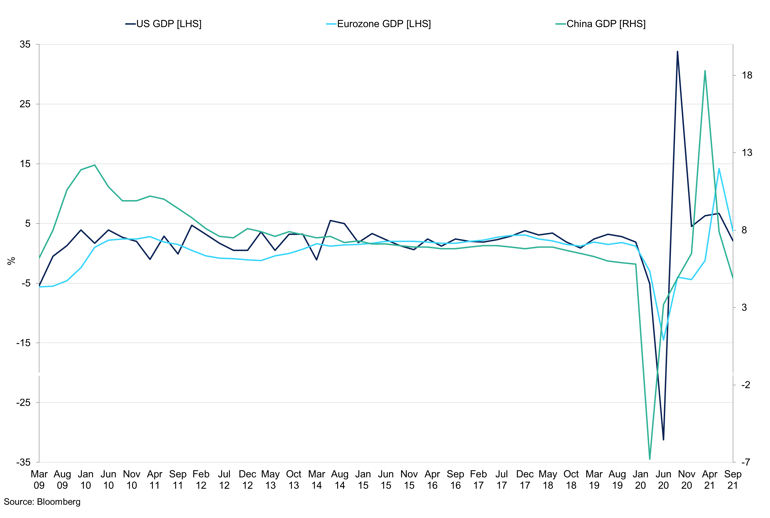

Major Economies GDP Growth

All major economies saw further deceleration in Q3, driven in part by the removal of government support and the rising number of COVID-19 cases.

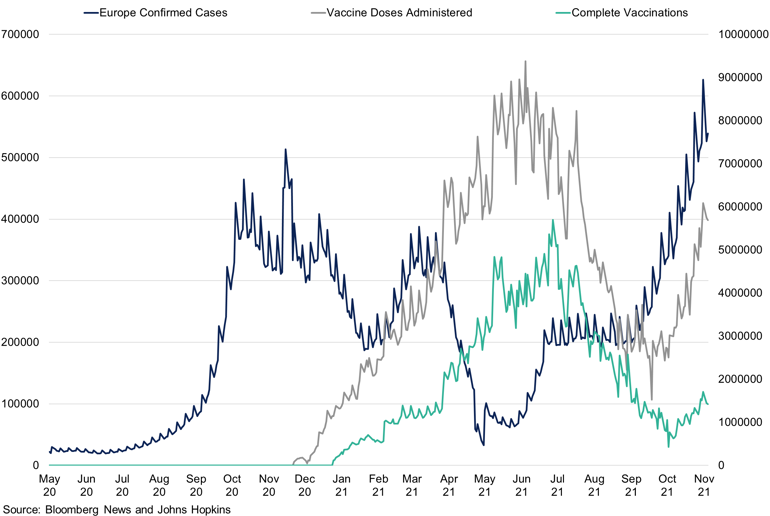

Another concern is the new COVID-19 variant and the spread of infections in Europe, most of which already imposed some level of new restrictions. With vaccination rates now high even in emerging markets, there is a limit on the potential impact that the spread could bring, but government response will be key in how countries decide to deal with the aftermath of another wave of infections.

US

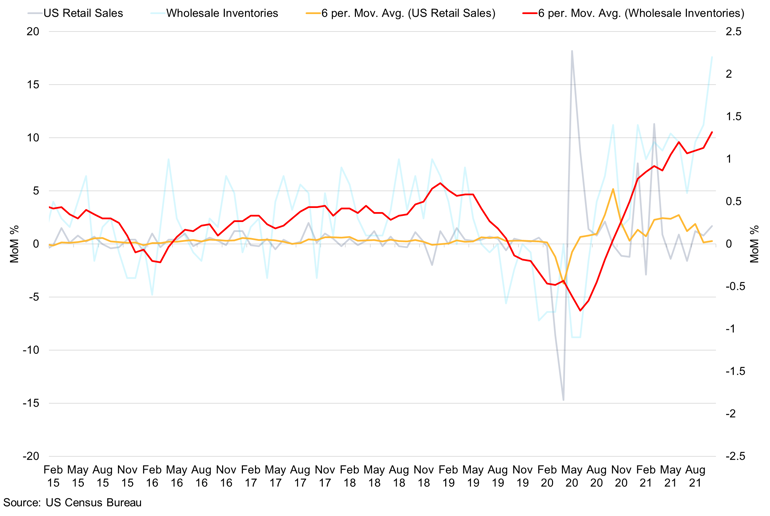

US GDP growth moderated by 2.1% q/q in Q3, in part due to the economy suffering another strong wave of COVID-19 infections in September. For Q4, it would be reasonable to assume that inflationary pressures will be a headwind for economic performance. However, as of October, we have seen a strong appetite from the demand side, a major part of the US economy. Higher income in October has translated into growing consumer spending, which increased by 1.3% m/m, the highest since March, and up by 0.7% when adjusted for inflation – a healthy indication of spending. Retail sales followed suit, growing by 1.7% m/m in October. This was mainly supported through the auto sector, whereas general merchandise continued to fall. Indeed, despite a decline in government support, spending remains strong and savings, as a percentage of disposable income, continued to show significant declines, pointing to a persistent appetite for expenditure. Furthermore, given that the after-tax income adjusted for inflation has been falling for the third straight month, the willingness of an average consumer to spend is evident. As of November, credit card data is already higher than in the last two months, and we expect this to positively impact growth in this quarter. The data for the next couple of months will be key to see if this could be sustained, and we did see wholesale inventories shooting up to record levels as companies sought to stock up to accommodate demand for the holiday season.

Retail Sales vs Wholesale Inventories

Wholesale inventories shot up to record highs as retailers stock up for upcoming Christmas demand.

Industrial production picked up sharply in October, growing by 1.63% m/m, thanks to the waning impact of Hurricane Ida and strong consumer demand continuing to fuel new orders growth. On the other hand, manufacturing performance continued to decline. IHS manufacturing PMI fell to 58.4 in October, a December 2020 low. Although lower overall, expansion of new orders remains historically high, further adding to existing backlogs. A lack of input availability and transportation delays led to a severe deterioration in performance, with input costs rising markedly. At the same time, firms passed higher input prices to their clients, as charges rose at the fastest pace on record. To help build stock, companies purchased more manufacturing goods, indicating that another main component of GDP, orders for business equipment, is in solid shape. At the same time, however, in the longer term, while robust demand is positive for economic growth, it puts additional strains on supply chains which further drives consumer confidence lower.

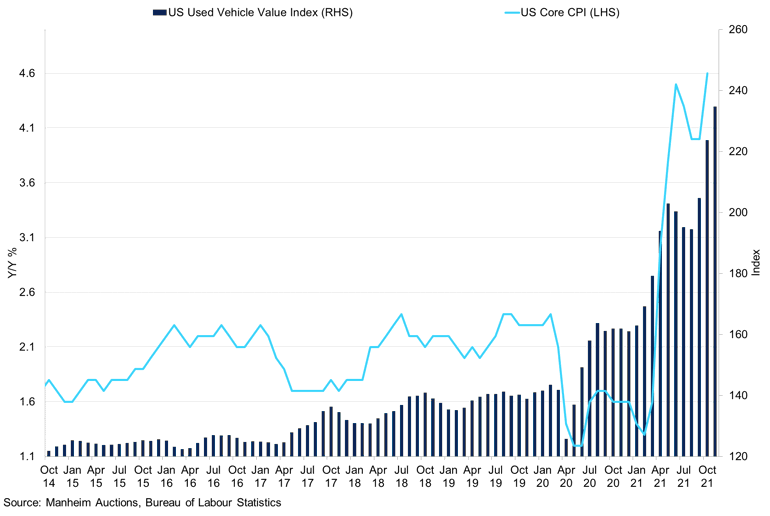

Regardless of growing personal spending, inflation continues to present major headwinds to economic recovery. CPI continues to outperform and remains at 1990 highs of 6.2% with energy, shelter, food, used and new cars among the largest contributors and supply chain disruptions meant that input costs had been passed down to consumers. Indeed, the used car index, which drove a bulk of inflation price increases in spring, is seen picking up sharply once again, suggesting there is still more room for broad inflation measures to grow. Expectations of continued inflationary pressures have adjusted accordingly, with the University of Michigan sentiment superseding the 2010 highs. As a result, outlook sentiment deteriorated, however, not in line with the lows of 2010. This could be explained by the emergence from pandemic restrictions and the hope of inflation being more or less temporary. Indeed, 1yr inflation expectations have diverged from 5-10yr significantly. Higher inflation could also reflect the unprecedented amount of government stimulus that the US has injected into the economy. This could further explain a considerable rise in consumer demand.

US Used Car Index vs Core CPI

Used car index, the part that drove the bulk of core inflation during spring months, is on the rise once again.

As the result of higher-than-expected inflation, the Fed announced it will begin to taper its asset purchases, down from $120bn a month by $15bn until June, unless data points to the need to change the speed of reduction. The markets' response was somewhat muted, a testimony to the Fed's clear management of expectations so far during this monetary policy cycle. Longer-term US yields have continued to edge higher, pricing in sooner-than-expected rate hikes, however, remained on the long-term uptrend. The curve, however, is seen flattening, with shorter-term yields strengthening further after the Fed statement that the target range for the federal funds rate might be raised sooner than market participants expect if the inflation continues to run higher. The officials have also abandoned the description of inflationary pressures as "transitory", confirming that prices have been rising faster and stronger than expected.

The dollar rallied, supported by strong inflationary readings, suggesting that support from the Fed would have to come in the form of stronger interest rates. The dollar is once again is seen as a safe haven, given recent rallies during a time of uncertainty in the global outlook. For 2022, the dollar should continue to strengthen, given further tightening of monetary policy, while Europe's monetary policy outlook is still uncertain, and China is considered to be more dovish.

EU

Eurozone inflation reached 4.1% y/y, the highest since 2008. However, excluding volatile food and energy prices, core inflation remains in line with the ECB target at 2.0%. It is most likely to calm down in 2022, but before then, higher energy prices and supply chain disruptions are going to complicate that recovery.

Although inflation continues to accelerate, the fact that core inflation remains modest suggests tightening of monetary policy from the ECB to be premature at this stage. In line with other economies, its PPI outpaces the CPI index, showing that most of the pricing pressures have fallen on producers. ZEW expectations point to softer growth alongside softer inflation expectations.

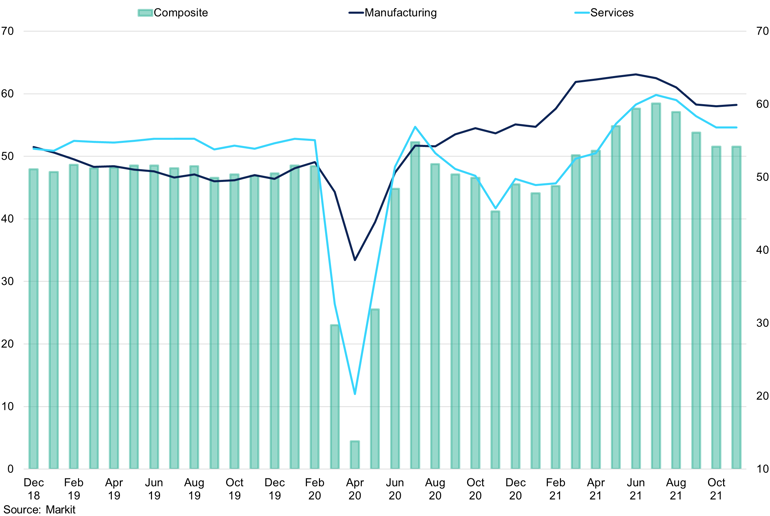

EU composite PMI rose to 55.8 in November, having slipped to a 6-month low in October, as service and manufacturing saw growth improve on the back of slightly stronger inflows of new business. While higher month on month, the average reading remains below the Q3 performance, pointing to a weaker economic environment. The upturn was accompanied by a further increase in inflationary pressures, as firms' costs and, in turn, the prices charged rose at record rates. The service sector continued to outperform manufacturing for a third straight month and is now at the highest levels seen in three months.

EU Composite, Services, and Manufacturing PMI

Manufacturing continues to outperform the service sector, which is likely to deteriorate even further given the spread of the new variant.

Most of the bloc is facing headwinds from the rising number of COVID-19 cases and tough government response that might put countries into tough lockdown measures for Christmas. Given the mix of supply delays, rallying costs and renewed lockdown worries, optimism has fallen to the lowest since the beginning of the year, further adding to near-term downside risks. Retail sales continue to fluctuate month-on-month, in line with the US. Year-on-year, however, is a bit different, and the sales have ticked for the first time since April. Europe seems to lag the US by 1-2 months since it opened much later. The retail sales in the US moderated after the spike seen during summer and now has remained somewhat elevated. Unlike the US, Europe did not receive the cash cheques directly to citizens and therefore had lower disposable income. This, coupled with the worries of upcoming lockdown restrictions, might significantly deter retail sales in the upcoming months.

Already in Q3, Germany, one of the bloc's biggest economies, saw weaker-than-expected growth accompanied by a drop in government spending. Private consumption grew by 6.2%, the highest since Q3 2020. This confirms a similar outlook of one in the US that consumer spending continues to be robust irrespectively of persistent high inflation, but other factors are contributing to a slowdown. However, most of the softness was driven by a lack of government support, which fell by 2.2% in the quarter. Despite mounting headwinds, the EU economy is projected to keep expanding over the forecast horizon, achieving a growth rate of 5% and 4.3% in 2021 and 2022, respectively.

EU COVID-19 and Vaccination Numbers

The number of daily cases is on the rise, and with that, we have seen a great number of individuals getting vaccinated.

From the monetary policy perspective, Lagarde stated that the ECB should not tighten monetary policy too soon and that she does not envisage higher interest rates next year. Indeed, the markets are pricing in lower interest rates as they did a couple of months ago, as EU yields have continued to fall. Policymakers are set to decide in the mid-December meeting whether to allow their pandemic bond-buying plan, PEPP, to end at the end of March and, whether to adjust their regular APP programme, currently running at $23 billion a month. Indeed, the current outbreak of COVID-19 cases will allow the ECB to downplay the need to dwindle down policy support and is most likely let inflation run hot for the time period.

China

Economic indicators suggest a modest acceleration in China after growth bottomed in September. Both retail and industrial performance improved month-on-month, however, private investment continues to fall and is now at 8.5%, the pre-pandemic levels. Retail sales grew by 4.9% y/y in October, given the last big national holiday this year, however, remained relatively low given the pre-pandemic level. Autos and apparel, historically the biggest drivers of growth, declined year on year. Industrial production increased by 3.5% y/y in the same month, with mining and utility components up by 6.0% and 11.1% as China boosted mining of coal to provide more electricity at a time of shortages. Therefore, domestic demand seems to be stabilising as the electricity shortage is easing somewhat through government intervention and virus-related pressure abate for now.

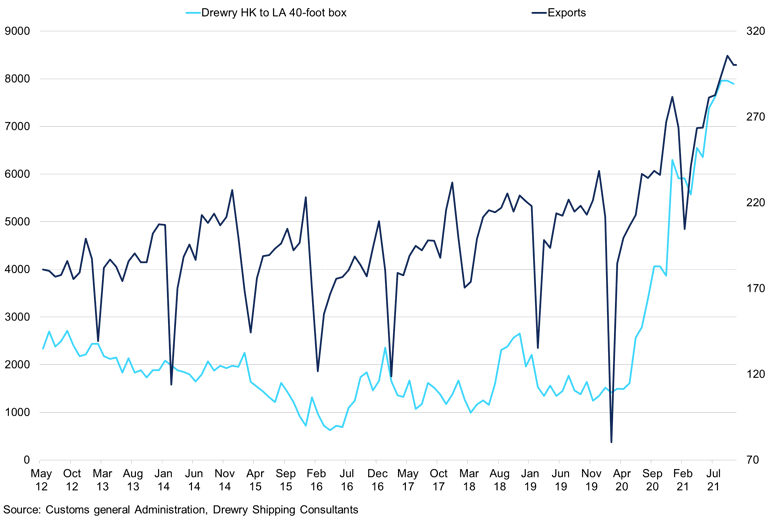

In the latter part of 2021, global supply chain disruptions benefitted China, as its low-cost and efficient manufacturing meant its share of global exports had continued to rise. Additionally, Chinese producers were willing to pay the premiums to load their cargo onto the ships to ship to the US and to optimise the shipping process, more compact and higher valued items were exported. Strong demand meant China's exporters had gained the confidence to raise their prices, partly to offset rising commodity costs. Export growth has exceeded estimates for three straight months, and trade surplus reached $84.5bn in October, as manufacturers continued to export backlog of orders. New export orders ticked up for the first time since March 2021, as softer shipping costs allowed for marginal purchases. However, strong global demand for Chinese-made goods is more likely to recede as the supply chain bottlenecks ease into 2022, softening the level of trade surplus during the year.

Exports vs Drewry Shipping Index

Exports from China rose despite the in-shipping costs, as producers were willing to pay the premium to get the goods delivered.

China's CPI rose by 1.5% y/y in October, while PPI rallied by 13.5% once again, the fastest pace since 1995, due to imported inflation as well as tight domestic supply of energy and raw materials. PPI seem to have taken the brunt of the pressure, whilst CPI has been moderately unchanged. Indeed, retail sales are weak relative to a long-term average, despite a recent uptick month-on-month in October.

Fiscal policy will be a key driver in economic support next year, alongside monetary policy changes. The PBOC has decided to cut the reserve requirement ratio in December, after refraining from using monetary policy tools since the last surprise reduction seen in July. The reduction was unprecedented, given China's limiting ability to loosen the policy, as the US and Europe are managing ways of scaling back policy measures. Indeed, China is in a difficult position as many of its current challenges are coming from the supply side, such as electricity shortages and curbs on travel as the country sticks with its "zero-covid" policy. In the meantime, the government has vowed not to use the property market as a short-term stimulus.

Brazil

In Q3, the economy contracted by 0.1% q/q, the third consecutive decline, despite a sharp rise in the number of vaccinations, as persistent inflation, and in turn, interest rate hikes alongside the drought added to the decline. Agriculture and industry declined by 8.0% and 1.1%, respectively, illustrating the tightening of monetary policy. As for Q4, indicators point to below-expectations data. Exports continued to decline from the peak seen in Q3 and a now in line with a long-term average. On the other hand, the service industry that was hit the hardest by the pandemic continues to recover while the manufacturing side continues to be heavily impacted, supported by the deterioration of global supply chains. According to BCB, continued recovery in the labour market alongside the service sector, as well as the sectors that are less dependent on the business cycle – such as agriculture and livestock, should support, albeit slowing, growth.

In 2021, according to the economy's industry, while forecasts are being downgraded, the economy is expected to grow by 5.1% in 2021 after contracting by 4.1% in 2020 and outperforming other Latin American economies, thanks to its government stimulus packages. New deficit-boosting plans have increased volatility in the domestic markets and one of the most aggressive rate-hiking cycles that have already taken Brazil's base rate 5.75bps higher this year to 7.75%. Growth in 2022 should be lower, with the withdrawal of economic stimulus and advance in the tightening of monetary policy conditions. Markets expect growth of 0.93% in 2022.

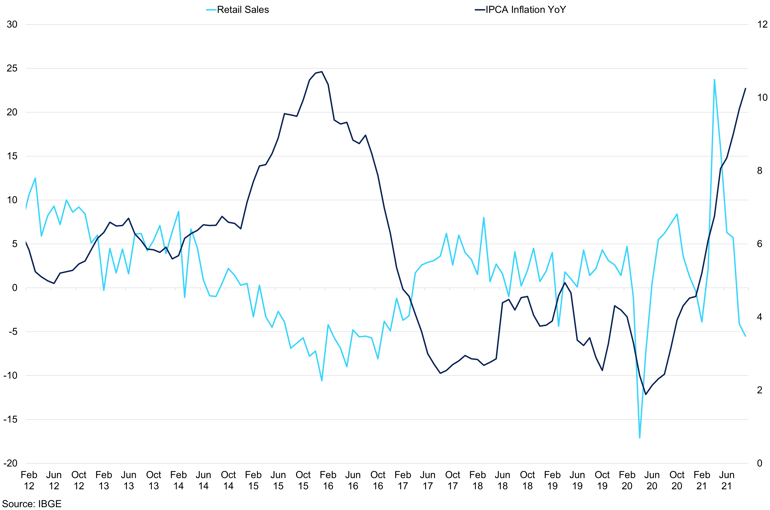

In October, inflation increased by 10.3% y/y, nearly tripling the government target of 3.75%, driven by factors such as high fuel costs, lower exchange rate and a drought that pushed up energy bills. Indeed, inflation remains persistent, and the most recent growth came from the core components of inflation, which means that consumers are experiencing higher prices first-hand. Industrial cost-push inflation also continues to persist and is unlikely to abate any time soon. In 2021, inflation is expected to grow at 9.7%, up from 7.9% in 2020. In 2022, however, inflation is forecast to slow down to 4.7%, given continued tightening of monetary policy conditions and a lack of government support.

Inflation YoY vs Retail Sales

Retail sales continue to soften as high levels of inflation deterred consumers from spending.

BCB raised the Selic rate by 150bps in November, an unprecedented amount, to combat the rising inflationary environment, and is most likely to raise by the same amount in the next meeting. While most economies agree on the need to begin tightening the monetary policy to help combat inflation, Brazil is amongst those that have pushed this narrative to the extreme, with six hikes already underway in just a year. BCB explains its reasoning as necessary means of combating high inflationary pressures to help guide prices to target in 2023. Swap rates in Brazil, with markets pricing in interest rates as high as 12% in 2023, the highest since 2017.

However, higher interest rates, taken together with high inflation, and falling confidence, mean that economic contractions are a clear possibility for economic growth. Inflation expectations have also edged higher as Bolsonaro stated that the fiscal ceiling might be lifted off to fund additional payments to the country's poorest. The increased spending, coupled with a fresh plunge in the currency, are boosting bets that policymakers will have to raise borrowing costs faster. The new cash-transfer programme is partially funded with extraordinary credit, which is not controlled by the federal spending cap, making investors nervous about the trajectory of public deficit. This also creates uncertainty surrounding the integrity of the source of funding, making it more vulnerable to electoral interests, which also means that more over-the-cap spending could be on the way. Brazilian Economy Ministry said a bill on court-ordered payments would open up room for the government to spend 106 billion reais ($18.9 billion) in 2022, higher than the 91.6 billion reais originally expected, following a revision of inflation and GDP forecasts.

Vietnam

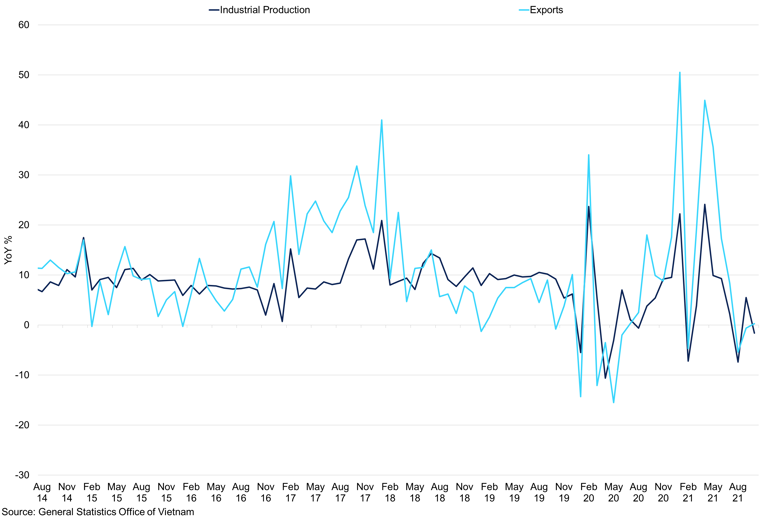

For the first half of 2021, Vietnam's growth averaged about 5.6%, however, in Q3, fell by 6.7% q/q, a series low, as the country got swept by the largest wave of COVID-19 infections since the beginning of the pandemic. As for Q4, the economy is showing signs of recovery, as most of the nation lifted its lockdown restrictions. Manufacturing performance has jumped above 50 for the first time since May in October, pointing to an expansion in the sector. Export levels just recovered y/y in October after two months of decline. However, with the coupling supply chain disruptions worldwide, there are headwinds that could soften the country's performance once again in the last couple of months of the year. Indeed, supply chain disruptions prevail, and while costs have softened to what we saw a month ago, they still remain three times higher on a year-on-year basis. Additionally, labour shortages persist as most of the migrant workers that went back home when lockdown restrictions were imposed are yet to return. These issues remain despite the recent reopening and could further exacerbate the manufacturing performance.

Exports vs Industrial Production

Historically, industrial production has been driving exports from the economy.

In the meantime, inflationary pressures in the economy have been subdued, and therefore, the monetary policy has been mostly untouched since October last year. The governors, however, believe that inflation risks will start to pick up on post-pandemic recovery. As of October, CPI stands at 1.77%, March lows. The central bank policy is to maintain inflation below 4%. Headwinds prevail, as COVID-19 are on the rise again and have beaten highs seen during the latest lockdown. Unlike other nations that have experienced significant waves of infections for the majority of 2020, Vietnam seems to begin to learn how to live with the virus in hopes of protecting lives as well as economic growth. This is despite a sharp growth in fully vaccinated adults seen in the last couple of months. This, coupled with being an export-based economy, supply chain disruptions should further complicate the outlook in the medium term. As a result of lockdown measures, the growth is supposed to reach 2.3% in 2021, marginally lower than 2.9% in 2020, and recover strongly in 2022.

Indonesia

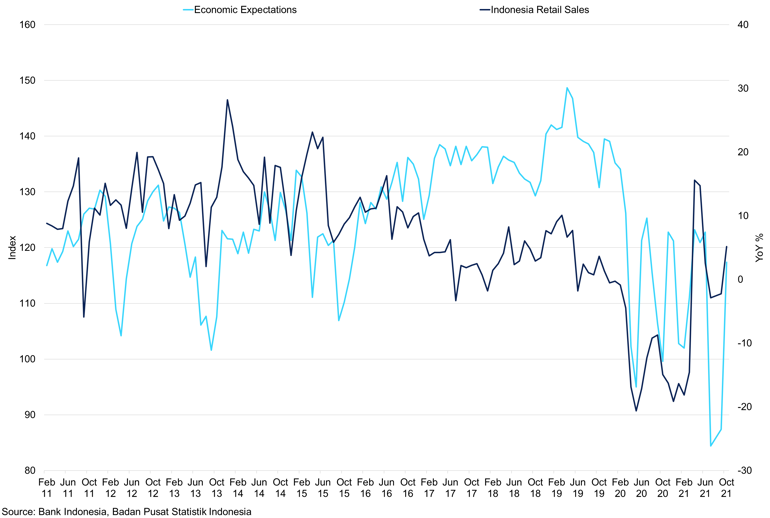

The economy grew by 3.51% in Q3, whilst lower than recovery seen in Q2 and a government projection of 4.5%, still expansionary. Like Vietnam, Indonesia withstood the strongest wave of infections during the summer months but managed to expand quarter-on-quarter, as most of the restrictions have been relaxed in late August, more than a month before Vietnam. Now, cases remain near record lows since the pandemic started, and the mobility data from Google shows increasing movement near supermarkets and malls. Likewise, confidence is recovering sharply, with economic expectations for next year rising sharply in October to the levels not seen since March 2020, and retail sales grew by 5.71%. That should help boost the Q4 performance of the economy that derives more than half of its GDP from private consumption.

While consumption and foreign direct investment slowed during the outbreak, soaring commodity prices have been beneficial for Indonesia, a major exporter. Exports hit an all-time high in August, with the trade surplus surging to more than $4bn in the third quarter. Additionally, consumption picked up higher, which could be explained by pent up demand and would soften in the last couple of months of the year, this should support growth in Q4. Growth in both retail sales and manufacturing performance so far in October should attribute to stronger Q4 growth.

Indonesia Retail Sales vs Economic Expectations in the Next 6 Months

We have seen a sharp rise in both retail sales and economic expectations of the near future, mostly supported through the relaxation of lockdown measures.

Bank of Indonesia injected more than $60n of liquidity into the financial system since last year, including direct purchases of government bonds, and delivered 150bps worth of rate cuts. However, as many economies are experiencing sharp rises in prices, inflation in Indonesia has been mostly rangebound, under 2% so far this year, in line with the BI target. As a result, the central bank involvement has been to a minimum. However, it aims to introduce some unwinding measures in line with other major central banks. BI stated it would adopt a pro-stability monetary policy approach instead of the pro-growth approach taken this year. That is, to reduce the amount of excess liquidity in the banking system next year without disrupting lending, but will keep rates low until it sees higher inflation. This is the first step to unwinding the ultra-loose policy. It may also keep a looser policy on down-payments for home and auto purchases until 2023 to encourage lending.

Corporate Results

Starbucks (Quarter ending October 3rd)

The company finished the last quarter of its fiscal year with a record performance of 17% in global comparable-store sales, given the low base of growth in the previous year as well as the strength of the US store sales. The company has also added an extra week when calculating this quarter's financials. As a result of positive performance, Starbucks announced the commitment to begin doubling down on investments in partners. The company opened 538 net new stores in Q4, a 4% y/y growth to nearly 34,000 stores, 62% of which are comprised of the US and China. Consolidated net revenues as a whole grew by 31% to $8.1bn, thanks to a strong growth of store sales. At the same time, the operating margin nearly doubled, explained by the recovery from the pandemic. This has however been minimised by the impact of increased supply chain costs.

North America and its component, the US, comparable store sales both increased by 22%, the biggest driver to overall performance. Cold beverages reached 75% of total sales, along with benefits from the fall promotion. International store sales, however, increased only by 3%, with a 6% decline seen in China. However, the company claims that 3-4% of those is the adverse impact from value-added tax exemptions, and therefore, are not representative of the true performance during the quarter. The development segment net revenues declined. The decline was primarily driven by a 20% unfavourable impact of Global Coffee Alliance transition-related activities, including a structural change in their single-serve business.

According to the company statement, 200bps of margin dilution took place related to a combination of supply chain pressures, inflation, as well as lapping over government subsidies from the prior year. Past Q4, the company assesses about a 90bps impact from inflationary pressures across the globe, driven by a combination of logistics, labour, as well as commodities. Into Q1 and Q2, these are likely to persist and mostly settle in the second half of 2022. Overall, Starbucks stated that they have a 14-month price-locked on coffee with several months of inventory in the warehouse at the moment.

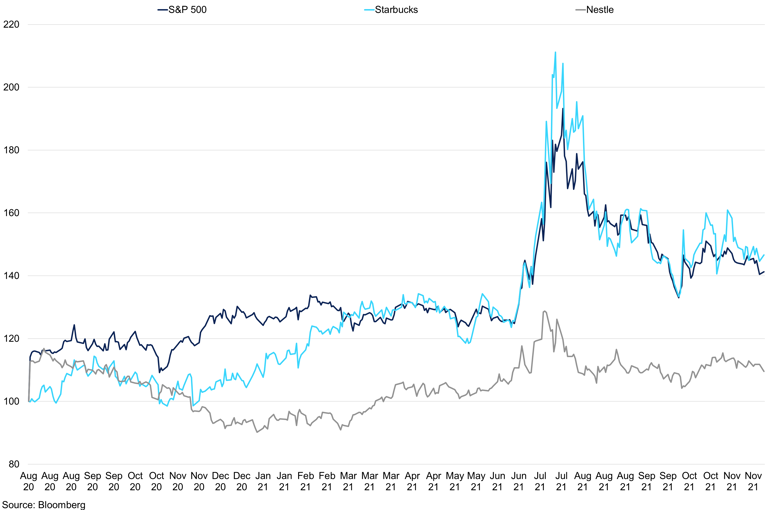

Company Share Price

Starbucks tracks S&P 500 closely, while Nestle gains have been capped.

Nestle

Organic growth reached 7.6% in 9-months for 2021, supported by positive momentum in retail sales, as well as continued recovery in out-of-home channels. Total reported sales increased by 2.2%. For the fiscal year 2021, the company expects organic sales growth of 6-7%. By product category, the largest contributor to organic growth was coffee, fuelled by strong momentum from Nescafé, Nespresso and Starbucks, with the latter posting 15.5% growth. By region, the biggest source of growth was from coming to AMS and EMENA. Out of home sales improved year-on-year, but not enough to offset the losses seen in the first nine months of 2020. Retail sales softened in the same period, down to 6.6% from 7.1%. Pricing increased by 2.1% in Q3 2021, reflecting input cost inflation. As far as coffee is concerned, the company saw less input cost inflation impacting prices, however, they do expect this to change next year.

Nespresso grew by 11% in Q3. Boutique sales have been returning to the pre-pandemic average and are now constitute around 40% of Nespresso sales, vs 10% during the peak of the pandemic. Overall, however, 10-15% of total coffee sales are from out-of-home activities. By geography, the Americas and AOA posted double-digit growth. EMENA saw high single-digit growth.

Luckin

Overall, in H1 2021, the company experienced substantial revenue growth of 106% y/y due to an increase in revenue through self-operating stores, as well as increased customer retention and order frequency. The selling prices have also improved, driving this growth. Furthermore, the company expanded to lower-tier cities in China. The total number of stores increased, through the growth of partnership stores, whereas self-operated decreased by 5.8%. Revenues from product sales were up by 89.3% y/y, with freshly brewed drinks representing 76.1% of total net revenues. The company cautioned that due to the impacts of COVID-19, the financial performance during 2020 was materially affected.

The cost of materials increased by 54.1% y/y. Losses and expenses related to fabricated transactions and restructuring increased by 15.6% y/y up to $24m, which consist primarily of legal fees under indemnification for security holders, underwriters of the company's IPO and follow-on offering, directors and officers. In February, the company filed for Chapter 15 bankruptcy in New York after the company said that more than a quarter's worth of business might have been fabricated. The company agreed to pay $180m in fines.

Demand

Global demand has managed to recover well from a short dip in consumption at the beginning of COVID. Now we are seeing the hybrid work schedules has allowed out of home consumption to return but the pandemic has changed at-home consumption. Consumers are demanding higher quality coffee at home; this presents a problem as this coffee is not as widely produced and there are few substitutes for it. Reduced fine cup and washed Arabica will see more semi-washed Arabica consumed, but what happens when this is gone?

The global economy has recovered well but now we are seeing significant headwinds to the economy now. Inflation has risen significantly as raw material prices, energy and shipping rates have increased and these prices have been passed on to the consumer. Falling unemployment and rising wages will help to counteract this, but CPI has risen faster than wage growth. Nestle indicated that cost inflation has increased 4% and they would keep rising consumer prices through 2022. Demand for coffee has maintained its strength, this can be seen by higher sales targets, Nestle sales across coffee and pet food saw growth of 7.6% for the 9 months through to September. This momentum was continued with Starbucks-branded products as they increased 15.5%. This outlines the strength in the at-home consumption in line with the pandemic and lockdowns.

Our demand figure for 21/22 is 167.3m bags as consumption increased across the globe following the pandemic. This is an increase from 163.7m bags in for the 20/21 season which was 0.2m bags higher than the previous year. The demand outlook remains constructive, but we expect inflation to cap growth in 2022 as consumers struggle. Coffee is an inelastic good but higher prices and limited washed and fine cup coffee may demand growth in 22/23, the limited availability in Washed Arabica and Fine Cup coffee may see more Robusta blends. Demand growth in major economies will be limited, and Brazil will also struggle in East Asia. According to the World Coffee Portal forecasts that there will be 100,000 coffee outlets by 2025, they also did a study over East Asia which concluded that 17 East Asia branded Café markets grew by 3,630 outlets over the last 12 months to reach 74,535. Therefore, we believe that consumption growth will be stronger in Asia but there are concerns over consumer strength in China. Our provisional demand number for 22/23 sees 1% growth to bringing our figure to 169m, this is conservative, but we remain concerned over consumer demand across all sectors, not just coffee, in 2022 and if central banks can keep inflation under control.

Growth in China

We have seen more focus on China with Lavazza Group suggesting targeting 1,000 outlets by 2025. They have opened a flagship store in Shanghai over the last year, they are looking to harness their European luxury style and heritage to appeal to the sophisticated consumers within China. The 1,000 target is ambitious as it took 12 years for Starbucks to get 1,000 stores. However, Lavazza has secured a joint venture with Yum China Holdings Inc., with exclusive rights in mainland China. Yum China Holdings owns 65% of the partnership and Lavazza holds the remaining percentage and are injecting $200m. China's market is growing fast with a 23.2% growth in branded coffee shops between 2018 and 2019. According to Mordor Intelligence estimate, 10% annual growth rate to 2026, with sales of speciality coffee and tea shops surging to $7.7bn in 2020 a significant increase from $551m in 2010, according to Euromonitor. There are now 21,464 coffee outlets in China, and growth will continue at a steady clip, and Starbucks is looking to have more than 6,000 outlets by the end of 2022. China's demand has been based around technology with 86% of Chinese consumers surveyed that they have previously ordered a takeaway coffee 2-3 times a week.

Shipping and Container Availability

The container shortage prevails, this makes shipping products even more challenging. However, the issue is not so severe in Brazil, this can be seen by Cecafe data, which is low because of the lack of coffee availability. Freight rates for containers have softened in recent weeks but remain nearly three times higher than this time last year. The World Container Index assessed by Drewry shows that the cost of a 40ft container stands at $9,146.41, this is down from where the index was $10,377 on September 23rd. This suggests that more containers are becoming available, but there is still a large backlog of orders to fill, and we expect higher-margin products and coffee is unlikely to be top of that list. As an example, as of November 2nd, there were 102 container ships in port around Los Angeles and Long Beach, this is just shy of the record of 108. We are also seeing long waits outside Hamburg, Antwerp, and Rotterdam, this compounds the issue when the product gets to its destination. The new waves of lockdowns in Europe and specifically Germany will increase lead times for products and could reduce trucker availability even further. When products are shipped FOB, the buyer is taking the risk and now freight risk is incredibly high, specifically in Vietnam freight rates are high and diffs are low, with the structure at a premium, all of which are working against you if you want to ship and carry coffee. However, market participants are getting inventive and looking at shipping coffee using bulk instead of containers. The Baltic Index has declined significantly in recent weeks, falling from $5,650 as of October 7th to $2,552 on October 19th, which is still double where the index was this time last year.

The problem with the container shortage is that is it a supply issue, and while higher consumer and producer inflation will likely reduce demand, in the long run, finding a new equilibrium will take time. It is not possible to build more ships and building more containers won't help reduce delays. As a result, we expect the container shortage to continue in the coming months, meaning certified stocks will have to fall further as roasters look to secure product.

Trucker Shortage

Brazil

Trucking in Brazil has been a contentious issue for years, and this year with high gasoline prices the threat remains particularly prevalent. The issue in Brazil is that the fuel tax is set by the state government, but in recent months the central government have been telling states to reduce the tax to keep truckers happy. There are two main problems with this:

- The state government is out of pocket and therefore their expenditure on infrastructure, social care, etc is reduced due to less revenue

- The price of fuel has been increasing faster than the reduction in tax; therefore, truckers are still paying high prices and because the ethanol blend is at 27%, and cannot be increased, governments have little ability to reduce costs.

The government suggested a BRL400 payment to each professional driver, but this was dismissed by the unions, the government also raised minimum cargo transport prices. Following the most recent escalation of the trucker issue, the government have attempted to stop protestors from blocking federal roads, there are now 36 lawsuits with a resulting 24 injunctions. Companies in states where blockages are not allowed will face fines ranging from BRL2,000 – 100,000. Bolsonaro had originally planned to cut the ethanol blend, however, we would advise against this from an environmental perspective and also from a trucker's perspective. In May 2021, the Brazilian Supreme Court ruled that the amount of VAT on sales and services (ICMS) should be excluded when calculating Social Integration Program (PIS) and Contribution for Social Security Funding (COFINS). The court limited the temporal effects of its decision, this could cause the treasury to refund BRL250 of unpaid PIS/COFINS to taxpayers. The taxpayer must deduct the ICMS value from the revenue of the PIS and COFINS.

Europe

Once the coffee has finally arrived at its destination there are still shipping issues due to the lack of drivers, there is a shortage of 400,000 drivers in Europe. This is a combination of COVID and Brexit, for the UK; Poland and Germany are also heavily impacted. The threat of more lockdowns in Europe, and in particular Germany, may worsen the logistical problem. The UK is also battling with Brexit, according to The Road Haulage Association estimate that 16-20,000 drivers have left the UK since Brexit, and 40,000 driving tests were cancelled during COVID. The association says approximately 600,000 registered HGV drivers but the shortage in the UK is about 100,000. New recruits are hard to find due to the limited poor working conditions. In Germany, they are missing between 45,000 -60,000 HGV drivers with this predicted to rise to 185,000 by 2027. France has also got a shortage of around 43,000 drivers since 2019, with Italy missing 15,000 drivers. Poland is the worst affected and the driver shortage is expected to be 124,000, according to the Road Haulage Association.

Fertiliser

We are not of the school of thought that suggests these higher prices will lead to an immediate increase in coffee supply. Firstly, coffee is a tree and planting more trees now would not yield more coffee for 3 years. Secondly, input prices are high, none more so than fertiliser prices. Demand for fertiliser is strong but supply is struggling to keep up, add in the supply-chain bottlenecks and farmers are not receiving delivery of fertiliser and are now looking for organic alternatives. Brazil potash CFR has reached $810/t as of November 11th, a rise of 217% this year, before factoring in currency depreciation. The weekly price assessments for fertiliser in Brazil from Green Markets suggest Brazil MAP CFR Spot has reached $850/t, the price or Rondonopolis MAP FOB increased to $1,050/t, as of November 12th. When you factor in the currency depreciation this year, which stands at 7.5% at 5.53 at the time of writing.

Higher fertiliser, freight, and inputs such as petrol, diesel and oil will keep margins thin, in turn reducing husbandry. Specifically, in Brazil where we have seen truckers threaten to strike due to high gasoline prices. We expect fertiliser prices to remain high in the medium term due to a cut in capacity and reduction of exports of key components by major producers. In Europe, there has been a reduction in capacity because of high gas prices. Nitrogen production in Europe has declined due to the shortage of gas. Fertiliser prices have rallied, this will no doubt squeeze margins, factor in the weaker BRL, supply-chain bottlenecks, and higher fertiliser prices will lead to reduced husbandry in 2022, and 2023. China's urea stock levels have been rising as they look to restrict exports to satisfy domestic demand in the spring. Domestics have increased production by 8% to 71% in October, but it is being held in China and local inventories are high on a historical basis. This continues to tighten the world fertiliser market, especially as demand from the US and India is strong, this is causing prices to rally further; Russia is also capping exports. The higher input costs and delay to input deliveries are likely to reduce husbandry for the next crop, negatively impacting yields. We expect power and energy costs to remain elevated in Europe in the next few months and in China in 2022, which could cap nitrogen, phosphate, ammonia production. Sulphuric acid prices are high which has helped the profitability of smelters, and sulphuric acid is a key component of phosphoric acid. High coal prices, emission regulations, and electricity management in China have caused the production of metals to soften, reducing sulphuric acid production. This will further reduce the availability of fertiliser.

Supply

SFL S&D Balance Sheet

Brazil

All eyes have been on Brazil this year and rightly so, as the weather has decimated the 2021/22 crop and now the 2022/23 crop, which was meant to be an on-cycle. We believe the 2021/22 crop is all but sold, farmers are selling what they have not committed in a disciplined fashion, looking back to the start of 2021 prices were around R$650 per 60kg bag, today we are R$1500 per 60kg a bag and higher. Exports in the 2020/21 crop year totalled 45.6 mill bags, Arabica, Robusta and Soluble July to June. Current crop exports 2021/July 22nd to October are 12.400 mill bags, compare with the similar period in 2020 of 15.553 mill bags, you have a deficit of 3.153 mill bags. November certificates of origin for Arabica, Robusta and Soluble on November 29th are 3.039 mill and exports so far 2.148m l, keep in mind November 2020 total of 4.771m and December 2020 at 4.410m.

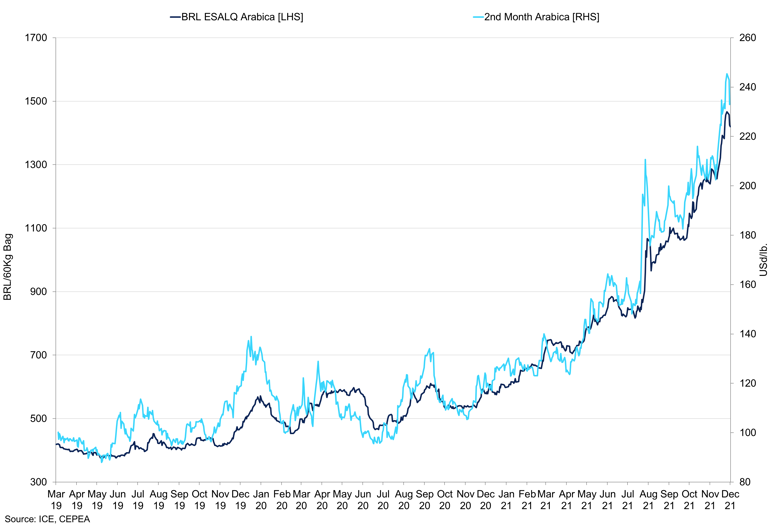

Brazil Arabica Local Price vs 2nd Month Arabica

Due to the lower crop, unless Brazil has a significant amount of stock at origin, exports will not reach 2020/21 levels. Indeed, any inventory in Brazil is likely to appear this year due to high local prices. With prices for Group 1 between R$1,470 and R$1,500 Real per 60 kg bag, group 2 R$1,270 and R$1,300 and Rio Minas at $R1,250 to $R1,270, we expect the tightness to roll into 2022, with these factors in play we work with a 32m bag Arabica 2021/22 crop.

We provisionally set the Arabica crop number at 45m bags for the 21/22 season, which was an off-cycle, however, following the drought and frost, we have reduced our number to 32m. The large gross short has been large for some time shows farmers have been forward selling, however, the local price has doubled since the beginning of the year. A conservative assessment indicates 30% of an originally estimated 45m bag, 13.5m bags, the crop was sold at R$600/bag. Now the crop is 13m bags lighter, farmers have sold a larger proportion of their crop 130% below the current ESALQ Arabica coffee price index. This left them 18.5m bags of coffee to sell at a better price, however, the market has continued to rally. It is our view that this has led to the defaults as they sold coffee well below current prices, we expect the trade to have been caught in this as well with some bearish at $1.80/lb.

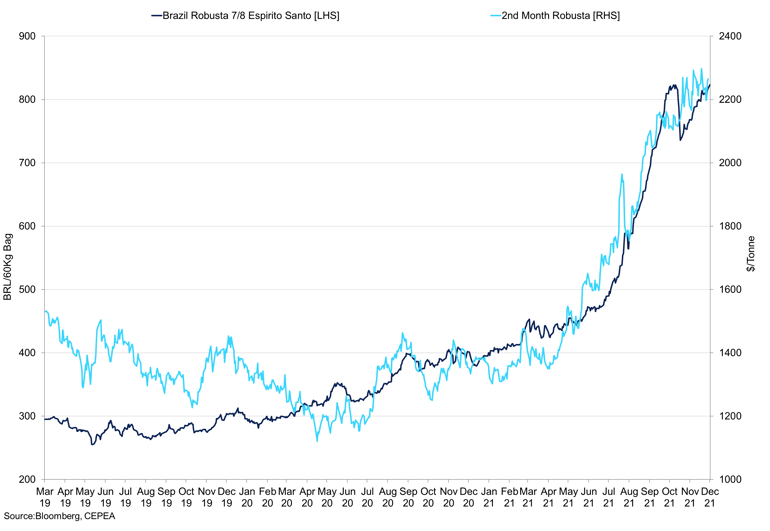

Brazil Robusta 7/8 Espirato Santo vs 2nd Month Robusta

The hope was that farmers would have a bumper crop in 22/23 but the frosts and drought have decimated this crop as well. There has been severe damage to the 22/23 crop as well, due to poor husbandry in Arabica areas, young trees notwithstanding the stress of the last 2 years, and mature trees not flowering at all in some regions. Dryness through flowering was also detrimental to the crop. Our crop number for 22/23 is currently 40m bags but we will know more in January once we can fully digest flowering, which as this stand is not looking good. As a result, there is further downside to this 40m crop number. Earnings for Conillon farmers has been strong and their crop will be the largest proportion of the total Brazil crop. We have the Conillon crop at 21m bags for the 22/23 season, we anticipate 65% of this will be consumed internally alongside low-grade Arabicas, the 21/22 crop is also fully sold. The differential is 17 over for Conillon coffee, which is at a premium to Vietnam. We have seen low-grade Arabica coffee catch up with Conillon coffee and trades for low-grade Arabicas are being done globally as roasters want to receive the product. The next issue for the Arabica market is after 22/23 you head into an off-cycle year, which is likely to be another deficit.

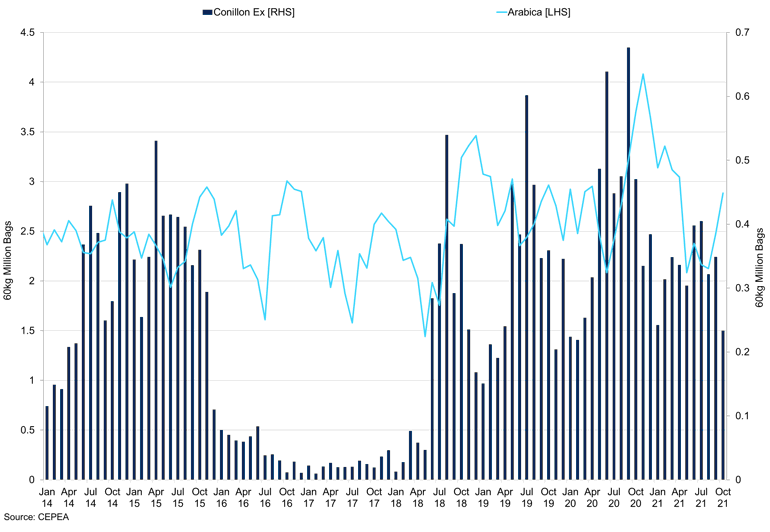

Brazil Conillon vs Arabica Exports

Colombia

We have revised our Colombia crop number lower to 12m bags for the 21/22 season. This is down from 13.8m bags in 20/21 and our original estimate for the 21/22 season. We saw excess rain in Colombia this year, causing the crop to weaken. Differentials for Colombian coffee are still high at 55+ even with the market at $2.41/lb this puts Colombian coffee at $3.00/lb. The issue for Colombian farmers is that they are also short, and the market keeps rallying, with $9,000 margins that are expensive. The internal reference price is $2,070,000 for 125kg, as the exchange rate increased to $3,928.75, as the farmhouse price has increased to $42,500. Coffee production in October declined 13% according to the FNC, output was 1m 60 kg bags which is down from 1.2m for the same period last year. According to FNC production declined by 5% to 13.2m bags, our number remains slightly higher at 13.5m bags for 20/21 but due to too much rain, our crop number is 12m bags for 21/22. The cost of inputs will lead to less husbandry and therefore, worse yields. The worker shortage from neighbouring countries has reduced pickers, increasing labour costs further. We anticipate the cost of production has increased by around 50%, with some regions even higher. This comes at a time when the world really needs that coffee, the reduction in milds creates further issues. We expect Colombian diffs to remain high due to strong demand and limited availability. There is a reduced availability, milds, semi-washed, and washed coffee whilst demand is rising. In our view, the only coffee that isn't in short supply is Robusta, but you can't get this coffee out of Vietnam due to container shortages and shipping costs.

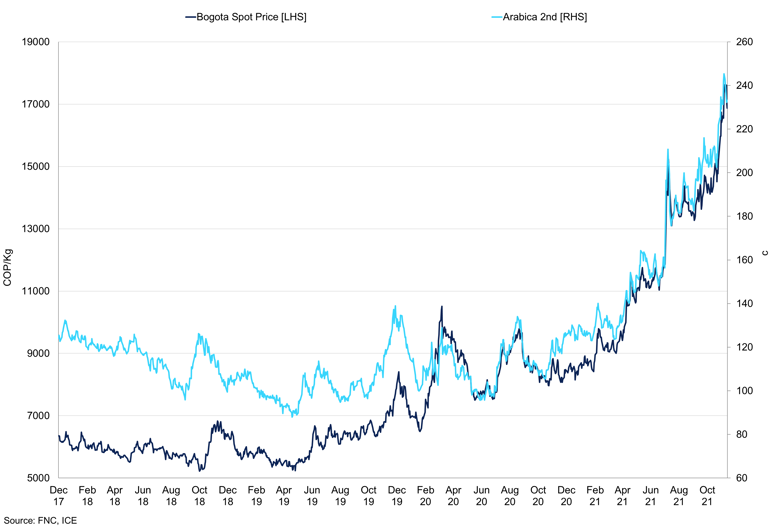

Bogota Spot Price vs Arabica

Domestic prices have pushed towards COP18,000/1kg bag in Bogota, we have seen farmers sell into this, and hedge but the market continues to rally. This creates a similar problem to what we have seen in the Brazilian market. Exports of Colombian coffee are up from November 2020 to October 2021 at 12.7m bags, an increase of 2% Y/Y from 12.5m bags. For the calendar year exports are also 2% higher at 10.1m bags according to the FNC. We expect exports to suffer in the coming months as production declines, indeed, shipments in October were down 6% Y/Y at 986,000 compared to 1.1m bags this time last year. Working with 2m bags of internal consumption, and the imports from Brazil, which between in the 2020 calendar reached 867,911, consisting of 644,210 bags Arabica, Robusta 130,664 bags and 73,037 bags of soluble coffee. So far through the first 10 months of 2021, Brazilian exports to Colombia have reached 945,694 bags, 683,834 bags Arabica, 201,345 bags Robusta, and 60,014 bags of soluble coffee, an increase of 2.84% compared to 2020. With exports for 2020/21 at 12.5m bags, our production number of 13.5m bags leaves 800,000 bags for domestic consumption, when you factor in the 800,000-900,000 bags this leaves around 1.6/7m bags.

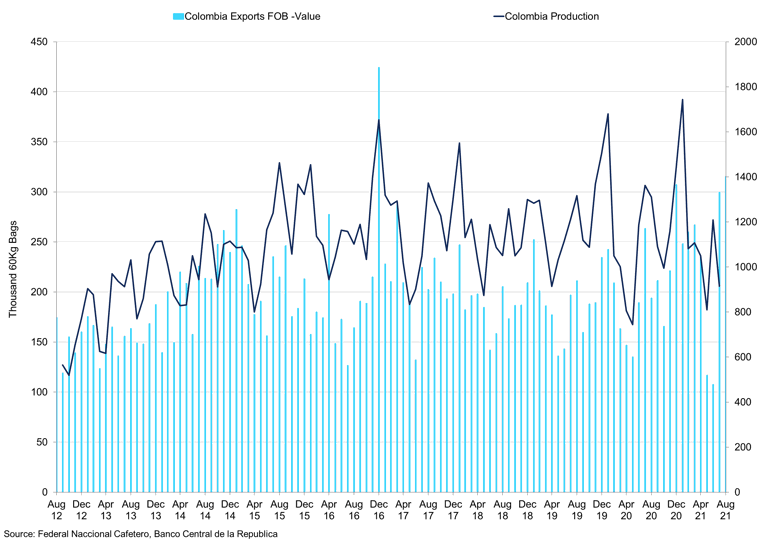

Colombia Exports FOB vs Colombia Production

Ethiopia

Ethiopia is also a contentious region, not just due to the political risk but also because of naturals can act as a substitute for Brazil. However, there is not enough of them, exports between October 2020 and September 2021 reached 3.348m bags, down 465,000 bags, down from the year before. Internal consumption stands around 3.5m bags and we expect the 21/22 crop to be between 6.5-7m bags. The reports of defaults are not to the same extent as we are seeing in Brazil and Colombia. The reason Ethiopia is now so important is because of the defaults and poor crops in Colombia and Brazil. We expect a delay to the current crop as the season is just starting and logistical issues will cause problems, if the rebels block the roads to Djibouti, we expect longer delays. Higher costs and reduced cash flow may lead to more naturals. We expect more defaults as we are bullish on the flat price and exporters will be hit once again. The political situation continues to worsen, as Irish diplomats have been asked to leave, with UK citizens urged to leave ahead of the civil war. We watch closely but the speed at which the conflict is moving indicates further struggles.

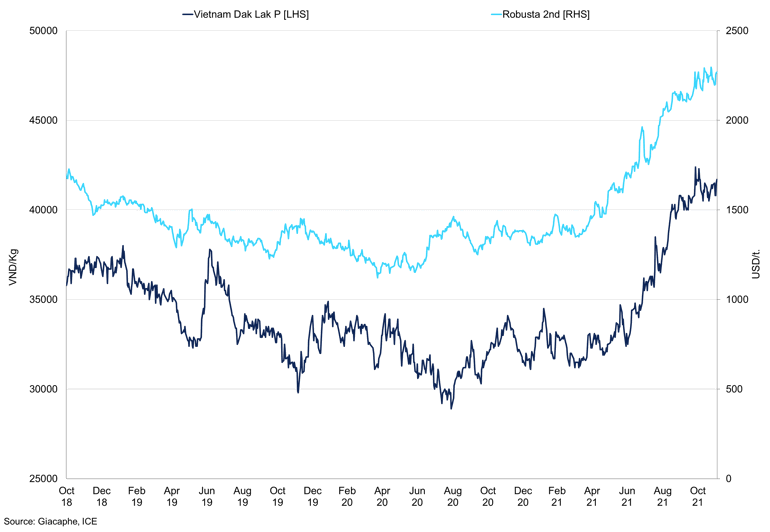

Vietnam Dak Lak Robusta vs 2nd Month Robusta

Vietnam

Our Vietnam crop number stands 29m bags for the 21/22 season, the crop has been progressing well until recently. The weather in Vietnam has been wet recently, and this has delayed the harvest. We do not think the yield will be impacted at this time as the weather is improving so this should help the harvest progress in the near term. Our worries are storing the coffee, Ho Chi Minh stocks stand at 3.043m bags as of the beginning of November, down 1m bags M/M but up 1m bags Y/Y. The lockdown has also meant that coffee could not be dispatched. However, the main issue is that due to shipping rates, exporting this coffee is expensive and there is a container shortage. It is getting easier to secure space on vessels, but the problem remains. If warehouses remain full and as harvest finishes, then this could cause issues as the industry will be unable to store the coffee. If the rain returns, drying the coffee could be challenging. The market structure has moved against those who wanted to carry coffee, as the structure is at a premium, this will cause inventories to draw further, not just at destination. Differentials have reacted to the higher exchange prices, with grade 2s weakening to -250/-290 FOB. These differentials have declined further into -320 and the shipping issue is getting easier rates between $7,000/$8,000. Conillon coffee is at a premium over Vietnam but we expect Vietnam coffee to start to flow more frequently.

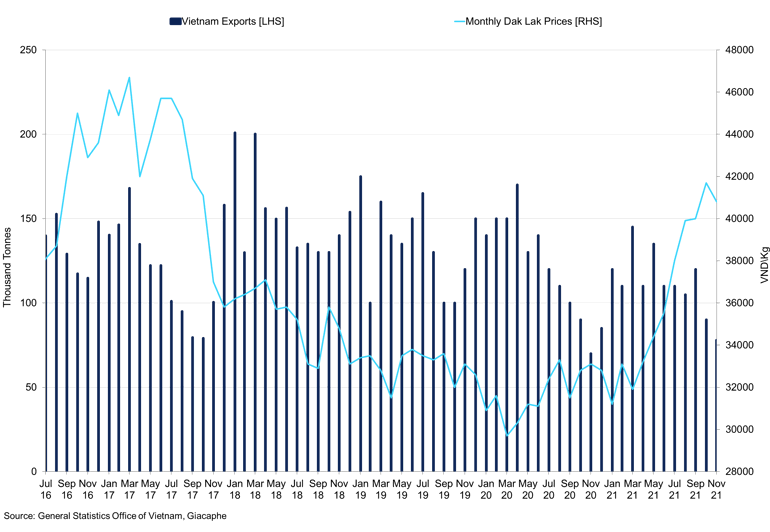

Vietnam Exports vs Monthly Dak Lak Prices

The tightness in the Arabica market, reduced shipping availability, the decline in inventory and now the rain has caused the market to rally. While the fundamentals for Robusta are not tight, the fact that the Arabica market is in such a large deficit, and it is tricky to get the product out of origin, has meant that the market is tight. Robusta coffee will likely go straight to the industry as demand will be strong, also with the current structure you cannot carry the coffee. We considered the prospect of buying Vietnamese coffee outright and holding it in a warehouse waiting for higher prices, which are likely to happen, but costs of storage and limited storage space in Vietnam are likely to mean this strategy struggles. We expect the Robusta market to be tight in the near term but expect the tightness to be greater in the Arabica market. The current wave of infections could lead to more issues with supply chains if more restrictions are put in place, we expect the situation to worsen, making it harder to ship the product. Exports of Vietnam coffee have been adequately low given the shipping issues, exports reached a low in November at 78,000 tons, down from 90,000 tons the previous month. The shipping issues are starting to ease but the new COVID variant is a threat to this. We expect exports to start to rise in the new year but watch the new variant closely. Local prices are still strong trading at 41,500VND/kg, up from 32,000VND/kg in May. This is giving farmers a preferential price and they are managing prices better than their South American counterparts.

What does all this mean?

21/22 Crop

A crop number of 52m bags, 32m Arabica and 20m Conillon and with Brazil, internal consumption at 21m bags suggests there are 31m bags available for export. During the last off-cycle year which was 56.25m bags in 19/20, Brazil exported 37.18m bags between July 2019 and June 2020. The last time the Brazil crop was 52m bags was 2017/18 when exports for that crop year were 30.06m bags. Using the 30.06m bags, there would be a carry-over of around 1m bags. We know that this is not the case, as since then, global demand has increased from 158m bags in 2017/18 to 167m bags for 21/22, as a result, exports need to be around 40m bags from Brazil alone. Therefore, you have a 10m bag deficit in Brazil alone for 21/22. When you factor in Brazilian exports to Colombia of 1m bags, the deficit increases.

As we said in April 2021, certified stocks will draw heavily which they're doing as roasters need product and the supply chain bottlenecks mean that they cannot receive shipments from origin. If there are any stocks leftover in Brazil, they will appear now, the government have said there are no stocks. The reduction of the Brazil crop is not the full story, we are seeing Colombia, India, Ethiopia, and Honduras all lower. This means there are few substitutes, and any coffee in inventory will be drawn. The reduction in other crops outside of Brazil will keep differentials, and the flat price high as inventories draw. We are seeing re-gradings of coffee, some will not pass but this coffee will still be taken by roasters.

22/23 Crop

The frost and drought will also have a large impact on Brazil's 22/23 crop as we are seeing now with reduced flowering, poor husbandry, young trees heavily impacted and stressed mature trees. We will know more about the yield and poor flowering in January, but the crop isn't looking good. This lower Arabica crop will come into effect when there is very little coffee in inventory and crops elsewhere will struggle due to higher prices. The situation will continue to worsen as roasters are behind the curve and will have to pay up, they most likely bought strips around $1.80/lb, but the next clip will be significantly higher, although we have seen many AAs, causing the open interest to decline. The higher prices will squeeze margins and increase the probability of higher consumer prices, but it could get to the situation where there isn't any coffee left to buy.

The issue is compounded when we factor in that 23/24 will be an off-cycle, so it may not be until 24/25 when stocks are able to be replenished as Central America, Ethiopia, and India cannot plug the gap that is due to be left by Brazil. It is not inconceivable that there is a 30m bag loss over the next 3 seasons, we find it hard to see where this will come from given high input costs, a strengthening dollar, and the fact that coffee is a tree, and you can't just turn on a tap and produce significantly more coffee or plant more trees and expect a yield immediately.

Commitment of Traders'

Arabica

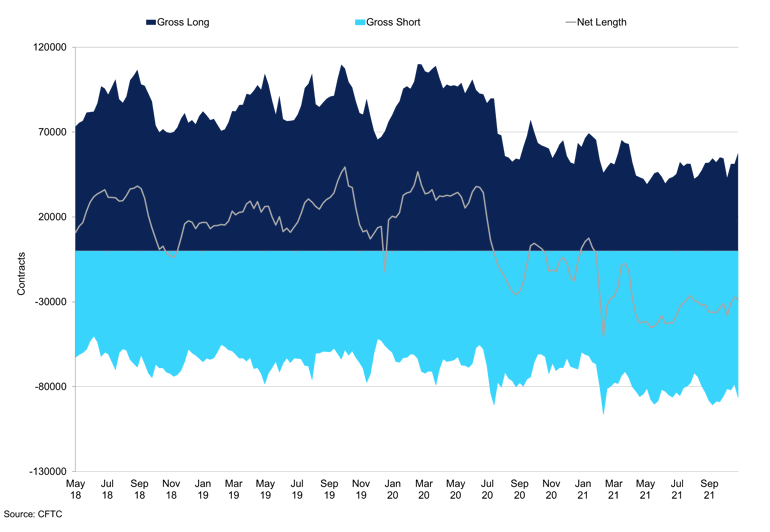

The Non-commercial net long is 46,585 as of November 19th, the position increased by 6,036 contracts, as we saw an increase in the gross long by 4,013 to 56,890. The gross short also declined by 2,023 to 10,305 contracts. The fund positioning has remained high, but the number of traders stands at 170, which is an increase from the September low at 153. The number of traders was over 200 in June this year, this suggests there are significant gains still to be made in the market as there are currently less funds involved in the market. However, the high margin and high prices may mean investors are put off from entering the market, but in our opinion when we know more about the flowering and Brazilian crop in January, we anticipate the market will rally. Spreads saw a large decline by 28,903 to 109,106 contracts. The sentiment is still bullish, and we expect this to remain the case as the fundamentals are strong and could worsen.

Commercials have reduced their gross long by 21,590 lots to 88,157, the gross short has also declined to 198,404 lots, a decline of 9,245. The gross short is still high, and we expect them to be over sold which led to traders not being able to honour contracts but also, they sold the coffee at a significantly lower price. The reduction in gross long indicates that roaster cover is lower than it was last year. Cover in the Arabica market is lower than Robusta, and we think that this will mean certs will draw quickly but also that unsold stocks are around 1.2m bags.

Robusta Producer/Merchant Commitment of Traders

Robusta

Managed money for Robusta has increased by 888 lots in the week to November 23rd to 33,457 lots as the gross long saw a marginal increase to 36,570 lots. The sentiment is bullish and the wet weather and delay to harvest are keeping momentum on the upside in the longer run, and the supply-chain dislocation is still hampering the market and will do for a while longer. The fundamentals for Robusta aren't so tight but we would not want to be short any coffee now. The net producer position has declined marginally by 282 lots to a net short of 33,457 lots, the gross short has reached 72,063 and the length is marginally higher.

Inventories

In April we outlined that certified stocks would draw in Q4, this has proved to be right. The fundamental situation was too strong for inventories not to draw, however, the supply-chain dislocation has added to this pressure. As mentioned, we have seen re-gradings of Brazilian coffee but some of this coffee will not pass, but it will still be taken by roasters. The structure is now at a premium so carrying coffee is not possible, this will cause certified coffee to fall faster as roasters look to secure product. Certified stocks is the cheapest coffee around, and roasters will take this coffee causing stocks to draw below 1m bags before long and then we expect to see sharp declines to 500,000. The certified stocks are at 1.6m bags but unsold coffee is closer to 1.2m bags, in our opinion. We expect coffee to draw quickly from now on due to the structure.

For Robust inventories continue to decline, this has been due to product being stuck in Vietnam. Lockdown in Vietnam, high shipping rates and the container shortage caused the industry to go after the certified stocks. Vietnam differentials are weakening in response to the higher exchange price but the problem the main reason is the structure. The structure is at a premium down the curve means you cannot carry coffee therefore it is being sold to the roasters, whose cover is better than the Arabica market but still isn't good enough, shown by the proxy commercial long in the commitment of traders'. We expect shipments of Vietnam coffee to go straight to industry. This will keep the structure tight and the flat price high.