Executive Summary

- The Brazilian reais has failed to break out of the range in recent months, risk appetite for EM currencies has increased recently, but the state of the government's finances and the slower vaccination administration is a headwind

- Mid-crop Colombia expected to be lower, Colombia bought 135,000 bags of Brazils

- Colombian diffs are +52/55 cents/lb, and the Mitaca crop is expected to be smaller

- Central America coffee production far from clear, the crop should be in full swing, but we still hear labour problems due to COVID-19

- Semi-washed Arabica being graded has surpassed our estimates, but we expect this coffee to start to tail off in the second half of March

- Fine and good cup coffees are trading above R$700/bag, and they have sold over 80% of the current crop and a large chunk of the 21/22 crop

- A strong rally in futures prices will be detrimental to exporters and producers who have sold around due to large margin calls

- Differentials remain high, and we expect this to remain the case as demand for coffee remains strong, but the supply of Arabica coffee falls

- Our estimate for the Conillon crop will remain unchanged, and we still expect this to cap prices on the London market

- Options open interest has been something we have noted, strikes of 150cts/lb with a September expiry have been heavily traded

- Roaster buying comes into play around 120/122cts/lb, of course, there can be spikes lower in this market, but we expect heavy buying below 120cts/lb

- When we look at the data algos process, we do not see a clear signal for them with Brazil shipments high, certified stocks rising or lacking conviction, lack of clarity from C. American production and prices have failed to break upside technical levels

- We remain constructive but believe patience is essential, the options market for us may be preferential, but we do expect prices to break higher with a target of 150cts/lb in Q3

Macroeconomic Update

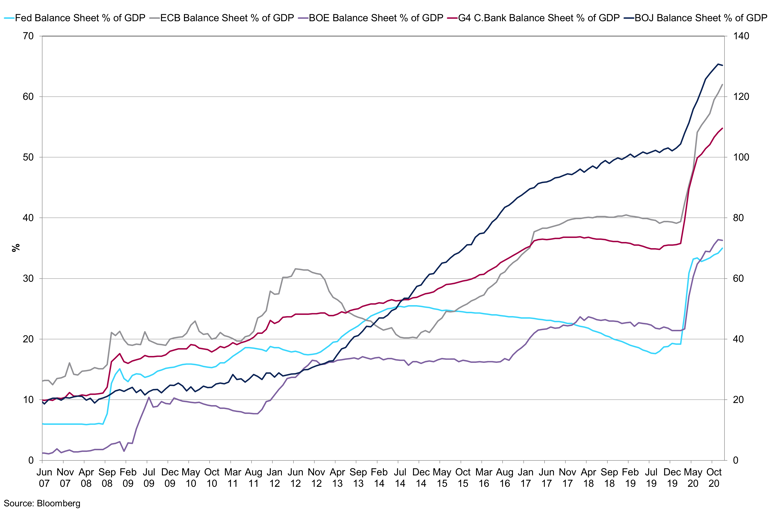

Central Bank Balance Sheets as a Percentage of GDP

The rising balance sheets of Central Banks will continue to support markets but when will it stop?

Stimulus packages supported financial markets in 2020; 2021 markets have acted in a similar vein but with the added dynamic of vaccination rates. Investors have their eyes fixed on global vaccination rates, and any supply chain dynamics a country may experience, underlying economic data has become less important at this moment. For example, the UK is in lockdown, Brexit risks are particularly prevalent, but cable has rallied as their vaccination rate is healthy, and investors are looking to Q2 data. Risk appetite is healthy, and stimulus measures from central banks and governments are unlikely to turn the taps off in the near term. Commodity prices have rallied, and cost-push inflation is poking its head above the parapet. With unemployment high and set to rise when COVID-19 employment schemes turn off, could cause stagflation, conversely, another stimulus cheque could prompt small firms to rehire some employees, but employment growth has lagged significantly behind spending growth. The inequality in the economies and across global economies has increased with higher-income households and countries able to cope with the pandemic better from a fiscal standpoint to low-income households and governments. The latest round of US stimulus from the new administration will ease some of the pressure on families in need, and the unemployed. Lower-income households who receive these cheques will spend it, boosting the economy, whereas higher-income families will save excess cash, and this will not ease until caution subsides. The savings rate in the US in December was 13.7% according to the Fed. Research conducted by Harvard university outlines that stimulus payments did not lead to significant gains for most businesses impacted by the crisis.

Economic policy has been rewritten, and we expect governments to maintain higher levels of debt for longer, this is not an issue if economies run with higher economic growth. However, the dollar trend is firmly intact; we expect this to continue given the amount of stimulus released and the Fed's policy of allowing inflation to be higher for longer with low real interest rates. The gap between real and nominal yields suggests investors expect US inflation to rise, other central banks have not followed the Fed to increase their inflation target, and their minimal support for the dollar indicates there is much further for the dollar to fall. This will help support commodities in 2021, but so far, coffee has failed to follow this trend. With stocks continuing to grind higher, and buybacks back in the fray, we expect capital to remain in cash equities in the near term. However, there is certainly more interest in commodities than in previous years. While the supercycle may be more applicable for metals in the long run due to the green economy, soft commodities will benefit this year.

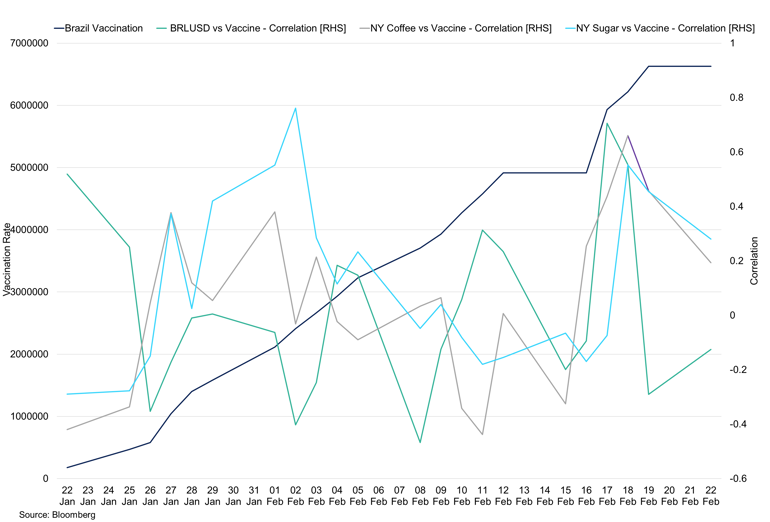

Brazil Vaccination Rate and Asset Correlations

Risk appetite has improved as vaccination rates improve, in the week ending 19th February the correlation between the vaccination rate and NY Coffee reached 0.63.

Vaccination rates in emerging markets are behind the curve, but we have seen large inflows into emerging markets so far in 2021. Higher yields are attracting investors, and this should help support local currencies. The BRL has gained ground this year, and we expect risk appetite to drive gains for the currency, in turn benefiting the New York contract. As we move through 2021, we start to look at Brazil's election, which will certainly impact the currency. Another benefit for the BRL is that US interest rates are likely to remain low in the medium term, which in conjunction with a weaker dollar will ease pressure on countries who hold US dollar-denominated debt. The Brazilian government discusses another round of emergency aid; however, with the government's finances fragile, there are questions over how extensive this stimulus package will be. A proposal is for 3 monthly instalments of 200 reais ($37), directed at those who are not currently receiving Bolsa Familia, the benefit scheme, the estimated cost of the new proposal is 6bn reais. The government's spending gap is set in stone and limits the growth in public spending to the previous year's rate of inflation. A break of this gap would be unnerving for the investors, and we expect this would weaken the real. One bright spot for Brazil is the export orders for their goods and commodities are likely to remain strong in 2021. A short-term policy can only go so far, last year the government provided support up to 12% of GDP with the Banco Central do Brasil (BCB) cut rates by 250 points. The BCB has not cut rates since August 2020, which suggests they have an eye on inflation. The budget deficit was high going into the pandemic and despite positive data in Q3, stood at 17.3% of GDP, government borrowing likely remain high in the coming years with the IMF estimating government debt will rise to 82.8% of GDP over the next 5 years. While risk appetite for EM currencies could benefit the BRL, the economy's long-term fundamentals are vulnerable.

Supply & Demand Update

Since our last report, we have seen significant reductions in Brazil's crop numbers, specifically the arabica numbers. Crop numbers for Arabica 21/22 have converged at a lower level; some estimates are below 30m bags we believe that is too low. Our arabica number was 35m bags in our last report; we are revising that lower in this report by 2m bags to 33m bags, bringing our crop forecast to 53m bags for 21/22. If we believe Brazil produced 50m bags of unwashed Arabica and 3m semi-washed for the current crop, working with this number. As of July 1st, this number will be 17m smaller; we still believe the certified coffee presents the best value. Local prices for top quality coffee are trading above R$700/bag; this includes semi-washed and Cerrado coffee. Semi-washed arabica coffee has continued to be shipped and graded, total shipments of semi-washed Arabica have surpassed our expectations. Forward sales of coffee have been strong, and at this time between 25-30% of the 22/23 crop and 25% of the 23/24 crop have been sold. The 2020/21 crop is approximately 80% sold.

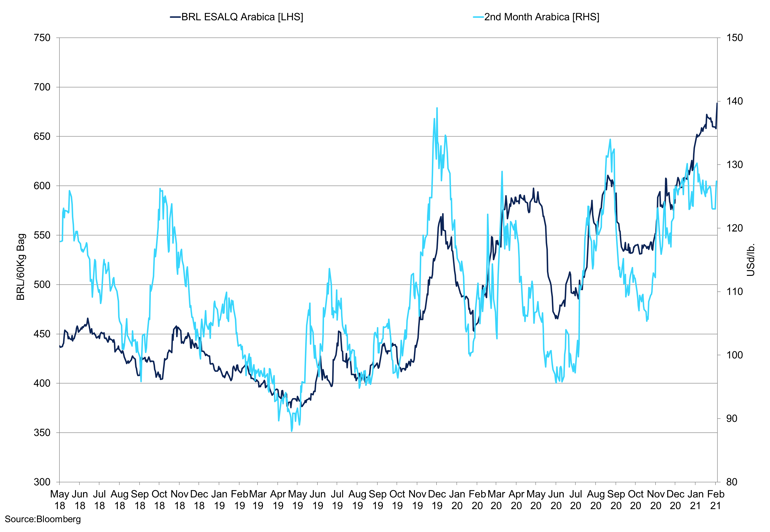

Brazilian ESALQ Arabica vs 2nd Month Arabica Contract

The local price continues to rise due to weak reais, with farmers holding out for R$700.

The market has been rangebound, but more recently prices have traded towards 135cts/lb, we have seen strong producer selling. Forward selling down the curve has capped prices, but we remain bullish on the New York contract and we expect to see short covering above 137cts/lb which will help support the market. Price action has been rangebound, but we expect the market to push through 150cts/lb in Q3 2021, but patience is vital. There is a significant risk to exporters if prices reach this level, and they have sold their coffee at 120-125cts/lb. We believe that even with a larger semi-washed arabica bag count, this coffee is still not a viable substitute for the lack of fine cup and washed Arabica from Colombia and Central America.

Shipments of Brazilian coffee were above 3m bags in January at 3.14m bags; this included 2.65m bags of Arabica, 241,534 bags of Conillon, and soluble exports of 253,577 bags. There are 5 months left of the Brazilian crop year; we need to see if shipments continue to trend lower during this time before we enter the off-cycle year. A reduction in Brazilian exports into July would aid the bulls. Coffee in warehouses from Brazil has increased to 715,781 as of February 12th; this has helped widen the spread and cap prices in the near term. Coffee pending grading has been trending higher in recent months but after reaching 157,000 bags at the beginning of February 2021, pending grading is 86,861 bags as of February 12th. Differentials are substantial, and Brazilian fine cup 17/18, Brazil good cup 14/16, and Brazil semi-washed coffee are at -15, -22., and -12, respectively. We do not believe coffee will be shipped with differentials strong if you do not have a home for it. Between September 2020 and February 8th, we saw 926,389 graded, 257, 367 bags have failed, a pass rate of 72.77%. Some of this may be re-graded on appeal. However, we believe that semi-washed Arabica's volume should tail off in the second half of March.

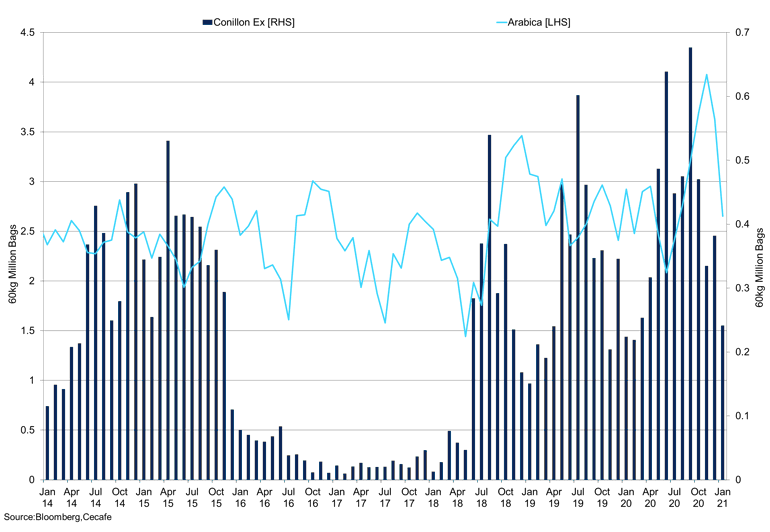

Brazilian Conillon vs Arabica Exports

January shipments for Brazil remained above 3m bags but we expect this to tail off after March.

Washed Arabica

Following the hurricanes in Central America in November or December, output for Central American coffee was revised lower, but the damage could not be quantified with much certainty due to stagnant water and the lack of pickers. Exports for January were 590,281 bags, down from 718,886 bags in 2020. IHCAFE have lowered their forecast for exports for the 2020/21 season to 5.6m bags, down 10.7% from the original estimates. Honduran shipments have been weaker between October and January than the previous years. Honduran differentials have softened marginally to +20, from +22 the last month. Even though futures have rallied in recent months, diffs are still very high, which outlines that lack of physical product in the market. We expect diffs to remain firm in the coming months, but the decline in Honduran coffee in stocks has halted, standing at 800,000 bags. This has prompted some fears of weak demand, but we do not believe this is the case. Honduran coffee will continue to be consumed, and we extract a further drawdown in Honduran coffee in inventory. We continue to see another deficit in washed Arabica and fine cup coffee, and strong differentials outline this. There is little substitute for this coffee, and when you factor in the large decline in Brazil's Arabica, you have a large hole to fill.

Inventory

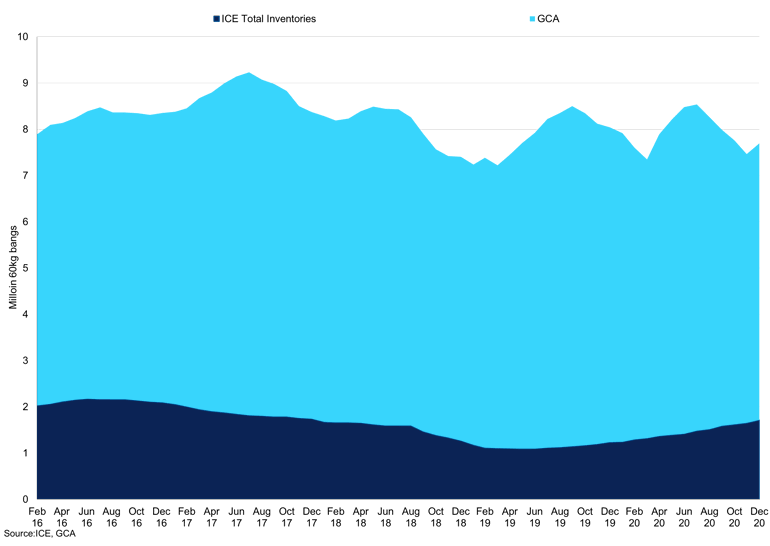

ICE Total Inventories vs GCA

GCA inventories declined in the latest data release but semi-washed arabica clouds the outlook.

GCA inventories declined in January by 135,130 bags to 5.843m bags, bags in Jacksonville declined from 475,000 in December to 275,000, with mild builds of inventory in Savannah, Houston New York. Demand is strong, and we hear from roasters that business has not slowed due to the lockdown in recent weeks. Certified coffee from Brazil has risen significantly, and while the amount of semi-washed coffee being graded has surpassed our expectations, we do believe it is now coming to an end. We do expect inventories of Honduran coffee to decline again. Certified stocks stand at 1.72m bags as of February 15th with 1.421m in Antwerp, 95% of certified coffee is in Europe at destination, and in the week to February 15th 68,960 bags passed grading.

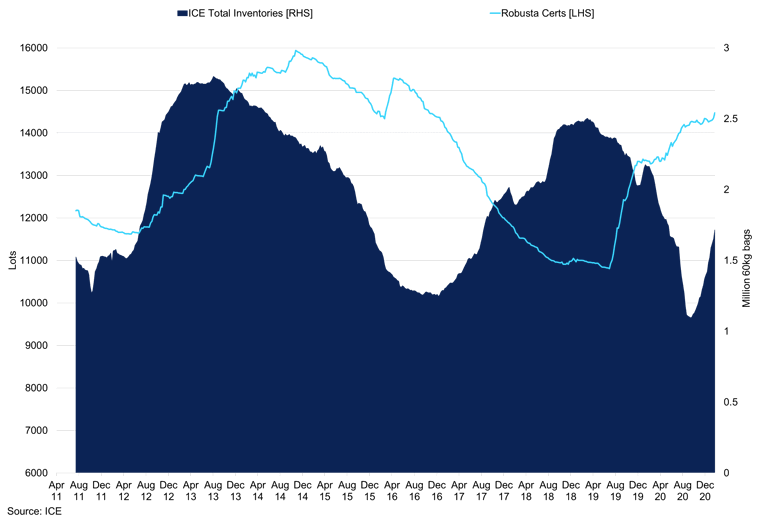

ICE Arabica Certified Stocks vs ICE Robusta Certified

Inventories are rising which is helping to cap prices on the upside.

Robusta inventories have been less active in recent weeks, in the week to February 15th we saw 51 lots withdrawn from stocks. We saw outflows in Amsterdam and Antwerp, but we did see some large inflows into London. Gradings reached 170 this week, non-tenderable lots were 111, with 13 suspended. The large Conillon will cap the Robusta market, but demand continues to be strong according to roasters.

Commitment of Traders’

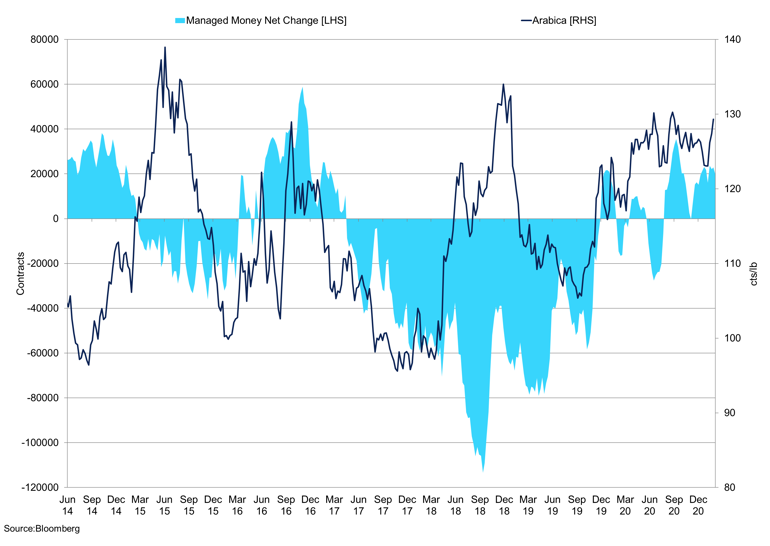

Managed Money Net Position Change vs 2nd Month Arabica

The managed money position has plateaued but price action tested 135cts/lb.

The Arabica managed money net position has increased in recent weeks, reaching 22,804 contracts as of February 9th. This is a slight decrease from the previous week, but the trend is still on the upside. Speculators appetite for coffee has increased, but the remains apprehension above the 130cts/lb as producers start to sell heavily. The z-score for the non-commercial commitment of traders' position once normalised stands at 1.113, which is marginally lower than last week's score at 1.136. The max z-score is 1.79, there is upside capacity to the fund's position, but the semi-washed Arabica shipments and inventory data do not provide a clear signal to specs and algos. We expect the tightness in the market to become more apparent in the coming months. High local prices have prompted heavy selling pressure. As a result, the gross short position of the commercials has reached -162,757. The record gross short is -184,087, so we are near the extremities but as mentioned before the significant amount of forward selling from Brazilian farmers is problematic if we get a significant rally, this could lead to defaults due to margin calls and would trigger some substantial short covering. The net gross short stands at -77,296 and has oscillated around this level for the last few weeks.

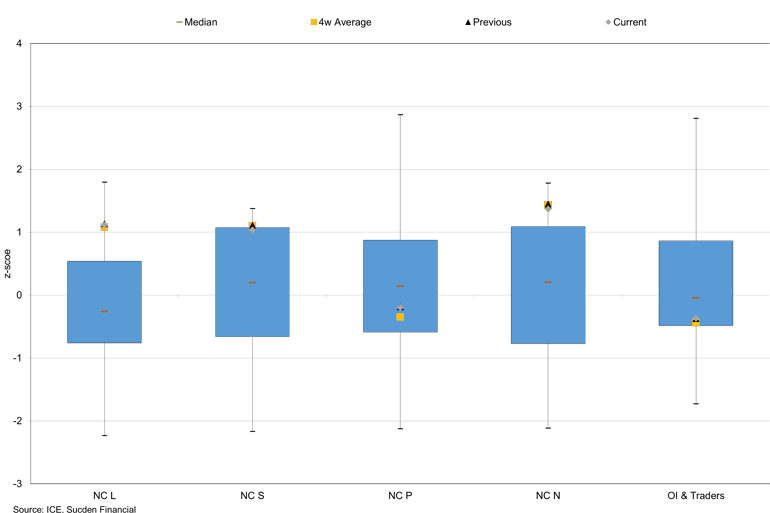

Non-Commercial (NC) Normalised COT

Z-scores suggest that there's excess capacity in the market, we expect this to be fulfilled as shipments from Brazil tail off.

In the Robusta market, the managed money net position stands at -14,378. In the week to February 9th we saw the net position decline as some shorts were liquidated and some new long positions were added. The producer net position is relatively benign at 1,853 contracts as of February 9th. The producer long position stands at 67,415, while the short position has increased to -65, 562 contracts. Producer selling has been strengthening in recent weeks, but the large conillon crop is expected to weigh on the market. As with the arabica market, the favourable local prices will keep selling elevated, with some producers asking for prices above current levels. However, there is limited trading at this level. Local Vietnam prices have declined in recent weeks but are holding above 31,000VND/kg, farmers have previously held out for prices above 33,000VND/kg, but the larger conillon crop has made this less likely.