Read our short coffee crop update, with commentary on recent price activity, and coffee market forecasts to take advantage of market movements. The weather in Brazil has improved but that is not enough to help the crop that is to be harvested in May. Shipments were stronger than expected given the use of break-bulk, but is this a sustainable way to ship coffee? Macro events have added a new bound of volatility to the market, and we discuss the key themes for the market next month in our new report.

Macroeconomic Overview

The year started on the back foot, with US stocks falling as much as 12% as omicron spread, and the Fed's tightening cycle dampened the outlook. The IMF has sharply cut its growth forecast for 2022 to 4.4%, down by 0.5pps, as higher-than-expected inflation and omicron variant worsened the outlook for the global economy. Globally, supply chain woes persist, but we expect them to ease this year, with a more prominent easing in the second half of this year as economies continue to go through the backlog at a faster pace and availability of material improves gradually.

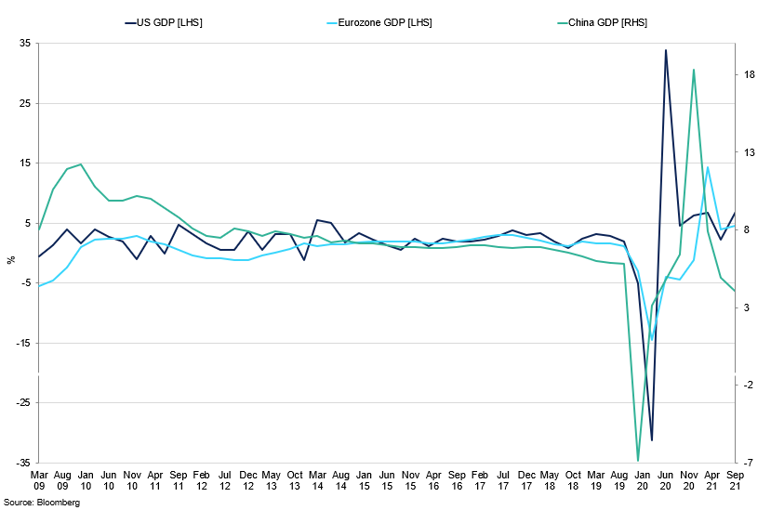

Developed Economies GDP Growth

Both Europe and the US GDP recovered in the last quarter of the year, and are forecast to have continued improving in Q1 2022.

The energy prices saw another wave of strong gains, with the most recent rally driven by the invasion in Ukraine, putting significant pressures on the supply side of the market. The demand remains strong, and the positive outlook has been supporting the market prices from the downside. The halt of the Nord Stream 2 pipeline by Germany is likely to have significant repercussions on Europe's energy usage, as 90% of the country's gas needs rely on Russia; this would mean higher energy prices that trickle through to consumer prices, and this will further impact gas bill payments. This rise in energy remains one of the key drivers behind CPI growth; the core index is also on the rise, as supply chain disruptions are creating shortages in the market, especially vehicles, where chip shortages meant that buyers resolved to buying second-hand vehicles. All eyes are on Russia, and recent moves by the government to move troops into Ukraine will continue to drive volatility higher if the escalation continues.

Emerging market economies have already hiked aggressively in the past quarter and now are seeing ways of slowing down the pace of tightening. Demand is robust, and we should see an additional boost coming from Europe as it emerges from strict lockdown restrictions, and Americans continue to show ample appetite for goods and services. Geopolitical tensions between Russia and Ukraine, however, are adding an unprecedented layer of uncertainty to the global macro picture. Growing tensions, and in turn sanctions, are certainly complicating the global outlook for the next couple of months. Any escalations in the current conflict will continue to drive the market to safety in the form of safe-haven currencies and the Treasury bonds.

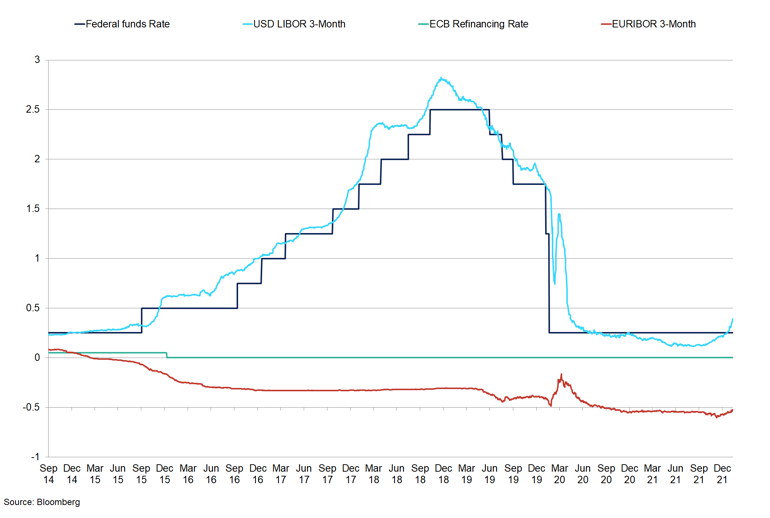

The Fed and ECB Interest Rates and Interbank Rates

Developed nations refinancing rate have all began to price in interest rate hikes this year, with the first scheduled Fed hike in March.

From the monetary policy standpoint, the Fed has confirmed its willingness to do whatever it takes to taper inflation, as it assured that its first interest rate hike would take place in March. The recent crisis in Ukraine has, however, caused markets to reduce their forecasts on the number and scale of interest rate hikes this year. The market response, however, has been mixed, with some debating whether the removal of pandemic support would be less detrimental to the economy than multiple aggressive rate hikes during the year. Indeed, aggressive tightening could significantly undermine economic recovery, thereby eventually slowing inflation. Therefore, the Fed's job will be to find the balance in the pace of tightening that will ensure inflation slowdown as well as keep market expectations under control. In the meantime, inflation continues to outperform, with the January figure at 7.5% y/y, a 40-year high. Month-on-month, however, the growth is seen stalling, with the most recent softness driven by the spread of omicron in January. The economy is now over the peak of its worst COVID-19 wave, and the number of cases has been on the decline. We expect it to provide a boost to performance indicators in February and March.

As expected, the labour market performance has deteriorated during the first month of the year, with job openings jumping to 4.33m and ADP employment falling to 301,000, the levels not seen since the early days of the pandemic. The reports point to the omicron wave being the main reason behind the decline, as pandemic-sensitive leisure and hospitality sectors were hardest hit, meaning that the subsequent months should see improvements in the labour market. The wage growth, the Fed's closely watched indicator, continues to fall, with the January reading down by 1.7% y/y, as employers are hesitant to raise wages in line with current inflation. However, we do not expect this softness in data to deter policymakers from taking aggressive steps to tighten monetary policy this month. The retail sales rose by 3.8% in January, the biggest surge in 10 months, highlighting the resilience of US consumers' appetite for goods and services. Additionally, credit and debit card data pointed to a stable spending pattern around this time of year. We should continue to see robust demand-side performance coming from the US, which should drive GDP performance in Q1 2022, which is forecast to grow by 1.8%, according to the Federal Reserve Bank of Philadelphia. However, given the persistent rise of consumer prices, now coupled with rising energy prices across the world, this puts the cap on consumer willingness to spend in the meantime.

Meanwhile, Europe's performance has been mixed, with regions' performance significantly diverging depending on the scale of the lockdown restrictions. Indeed, Germany is set to relax restrictions in March, while countries such as Spain removed most of the restrictions earlier in February. As a result, according to Bundesbank, Germany's output in Q1 2022 may have declined, making it the second recession since the pandemic began. The ECB has been less reluctant to make any drastic changes to its monetary policy regime, and their sentiment turned less hawkish recently, with the first hike now priced in March next year. The inflation, however, continues to beat multi-year highs, with the latest reading at 5.1% in January despite the spread of omicron across the bloc. The recent halt of the Nord Stream 2 pipeline will begin to trickle through to consumer prices in the near term, putting a massive dent in consumer spending ability, which would give more room for the ECB to respond later this year.

A similar dovish sentiment is present in China, where a deteriorating economic outlook, as well as the most recent outbreak of COVID-19 cases, has stalled the performance during the last couple of months. As a result, there are now shipping delays as shipping containers are sitting in holding areas, sometimes for additional weeks due to lockdown restrictions in docks. We have seen a significant decline in shipping rates in the first couple of weeks of February, which could be explained by the lack of demand given the Lunar New Year celebrations. Overall, the shipping rates have remained at elevated levels and will continue to deter those that cannot afford to ship overseas and increase input costs for those that do.

Emerging Markets

Brazil's central bank signalled that one of the world's aggressive tightening cycles is coming to an end after delivering eight hikes in the last eleven months, pushing the yields to 10.75% in February. The board members see increases to inflation expectations in line with continued rises in CPI, even as the economy struggles through the recession. Indeed, the GDP is likely to have fallen by 4.7% in 2021. The CPI, while slowing month-on-month, grew by more than expected in January, up by 10.20% y/y, on supply chain disruptions and costlier commodities, something tighter monetary policy cannot resolve. Expectations for end of year inflation is now at 5.4%, still above the target range. They will then ease into 3.2% by the end of next year. Heightened inflationary pressures are likely to put a cap on Real performance, despite its recent aggressive hiking cycle, especially as the Fed begins to tighten this month and the rate of hiking by Brazil slows.

Adding to Brazil's economic concerns is the rapid spread of the omicron variant, which disrupted some retail outlets and services. Retail sales have declined by 2.9% in December, and January is likely to see a worsening figure, in line with November's performance. IHS Markit service index continued to decline, falling to 52.8 in January, the May 2021 lows. Even before considering the surge of infections, there are already signs that steep rate hikes are hurting domestic demand. Retail sales, which have been the drive of Brazil's growth in the past, have fallen in three of the past six months, while industrial output rose in December for the first time since May. Therefore, fundamentally, the Brazilian economic environment seems muted, and the near-term outlook is on the downside.

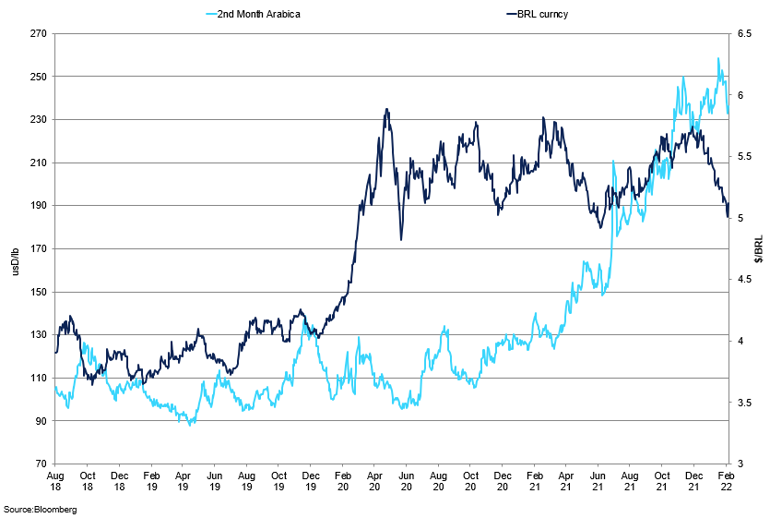

BRL vs 2nd month Arabica

We have seen the divergence between the currency and the 2nd month contract intensify in recent weeks.

The markets are anticipating Lula's comeback as president during the October election, as early polls show a 40% approval rating, vs Bolsonaro at 31%. A candidate needs more than 50% of the votes in Brazil to win a single round. Indeed, the local stocks saw an inflow of $6.2bn from non-residents in January, the second-largest monthly figure since 2008, as investors saw more room for a rebound. Under his proposal, Lula plans to emulate Biden's large infrastructure plan, which could further instil confidence in the country's performance in the longer term.

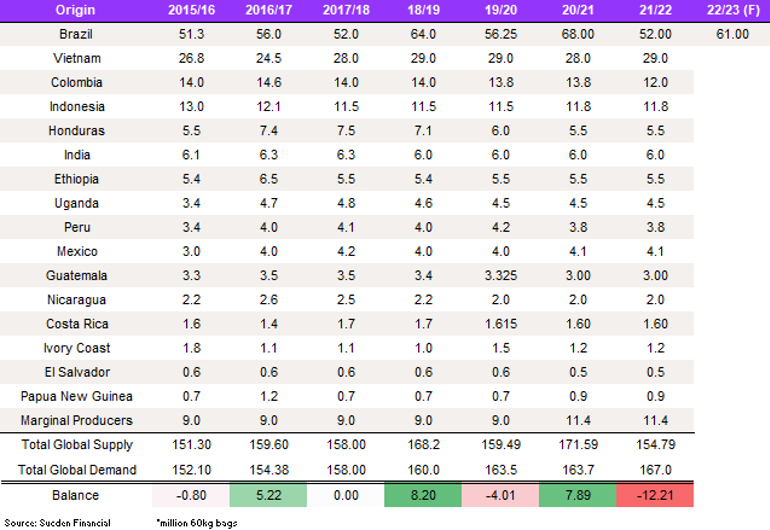

SFL S&D Supply & Demand

Global demand was robust in the last couple of months despite the spread of omicron across the globe at the beginning of the year. Now, the near-term outlook seems brighter as economies that underwent their biggest COVID-19 waves, and even the countries with strict lockdown restrictions, such as Europe, are seeing their restrictions lifted off. In China, where the number of COVID-19 cases is on the rise, separate consumer demand for coffee exists, and demand will continue to be steady there. A blow-up of conflict in Ukraine has clouded the outlook picture from the demand side. In particular, European demand is under threat, and we raise our risks for potential downside demand in the region. From the supply side, we expect lead times to grow as ships will be looking at re-routing their path around Russia or through international waters. At this time, we think that the impact on demand will be limited, but the longer lead times will compound supply chain bottlenecks issues. According to ICO, Russia consumed 4.681m bags of coffee in 2021, taking up a small share of global consumption that year. This will, however, translate into higher longer-term inflation for the US, and especially Europe, through higher gas and oil prices, further capping consumer spending potential in the longer term. The shorter-term impact should be limited in the meantime. The market continued its rally, and Arabica now trades at c250/lb as of February 17th and not far from the September 2011 highs. We have seen moderate softness in February, but the overall tight market picture continues to drive the general bullish trend. Anything that is afloat is bought, and coffee does not sit in the warehouses for too long. As a result, buyers had to accept higher prices. Breakbulk shipments in the last couple of months have taken some short-term steam out of the market, and some repositioning is taking place. We maintain our bullish rhetoric on coffee driven by fundamental market tightness. Therefore, we see no change to our original price ideas, and we still believe that the market has upside potential.

Inflationary pressures continue to strain companies that have had to pass down costs to consumers. And while the month-on-month picture might point to softer levels, the compounded price growth last and this year will mean significant price increases for consumers. Indeed, US consumer prices rose at the biggest annualised rate in 30 years last month, up by 7.5% y/y. As a result, we saw companies raise prices for their products and pledge to raise them again later this year. While the main factor in the increase is coffee, other pricing decisions, such as labour and distribution costs, are also at play in regard to the price hikes. Demand for coffee, however, has maintained its strength, and this can be seen through corporate earnings results in Q4. Nestle, for example, saw organic sales beat forecast, up by 7.5% in 2021, with Q4 growth of 7.2%. Starbucks coffee sales were up by 17%, showing that customers are willing to pay more to drink coffee. More so, these companies are likely hedged a year in advance and so are not worried about short-term price fluctuations but should continue to raise prices through the year to pass down some of the costs.

In 2021, the US imports of coffee grew 3%, and the customs value, excluding import duties, freight, and merchandise, reached $6.8bn, up from $5.6bn a year ago. The import figure suggests that high prices have not deterred the largest importer. On the other hand, this could mean that bulk coffee buyers might be worried about the upcoming even-higher prices and are stock buying ahead. Despite omicron, retail sales continued to grow in January, up by 3.8% m/m, highlighting the persistent appetite for goods and services. Slow wage growth might be capping the potential spending, but as interest rate hikes begin and supply chain bottlenecks ease, we should see easing in consumer prices this year, putting a limited dent on consumer coffee spending this year. Out-of-home consumption increased, with the Pret Index in both the US and Europe pointing to a moderate recovery in coffee purchases across major cities. In the meantime, shipping delays and backlogs will continue to strain the supply side of the market.

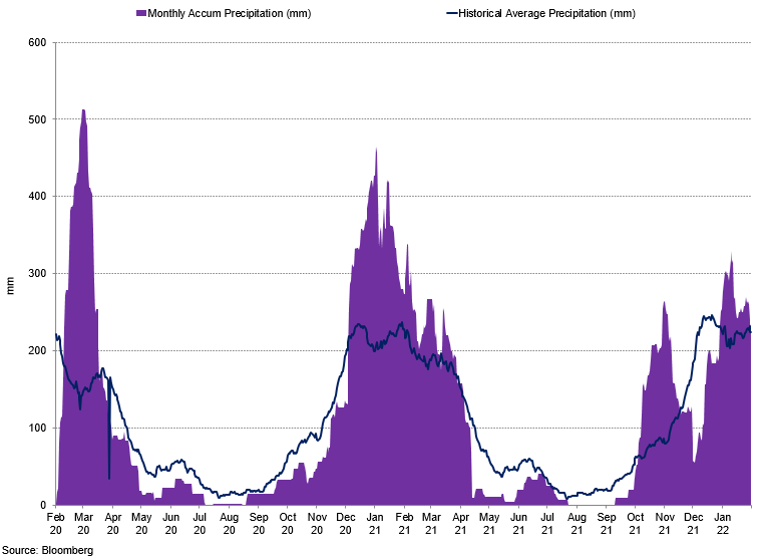

Monthly Precipitation in Brazil

Precipitation has been above average in January and February, not beneficial for the crop.

Battered Brazilian crops, continued supply chain bottlenecks, and falling certified stocks levels mean that there is limited coffee available at origin, and many roasters have to buy coffee on an outright basis. Our demand figure for 21/22 stands at 167m bags. This is the highest level since our time series began in 2015/16. The demand outlook is strong, but we expect price increases to cap the potential of demand that we could have seen this year. The supply picture, however, looks more severe, with our number at for 21/22 crop at 154.79m bags. The current crop is the smallest in 6 years, and this tightness means that anything that is afloat is bought, and coffee does not sit in the warehouses for too long. More supply is coming from other places but not enough to offset the deficit in Brazil. Over the next few months, we would expect Brazil shipments reduced, Colombia shipping less followed by lower shipments from Honduras and Guatemala.

Brazilian Supply

The weather last year, coupled with drought and frosts, decimated the crop. Markets have not seen drought followed by frost and then dry weather, whereas, before, the heavens opened and rain fell. Now, the rain has been so intense that it may not be beneficial for the tree, with the fertiliser being washed away. Therefore, and our Brazil number for 22/23, which was meant to be an on-cycle, is now at 61m, of which 40m is Arabica, 9m higher than 20/21. The downside, however, is more to our conillon number, 21m. We will see the conillon crop and the shipments are behaving in April, after we assess the impact of a lot of rain in key regions. This number, however, is not enough to cover exports and internal consumption of 21m, meaning our number is now 10m bags less than we expected with no stock build up behind it. Parts of Parana and Sao Paulo states saw flooding in January, adding to the stress on the trees. That's kept futures prices near a decade high. About 6/7 months ago, the trees that the farmer felt would not produce were cut back. Therefore, it is very unlikely we see any significant improvements to yields that are to be harvested in May. As a result, the crop is lower than usual, and producers are well sold for the season considering there is a long time till new crop harvest flows and forward supply strongly being reduced. Brazil shipments have been better than expected, but we anticipate shipments to start to fall in the upcoming months. 87% of the 21/22 crop is sold, 34% of the 22/23 crop is also committed, and we still have five months remaining of the 21/22 crop year.

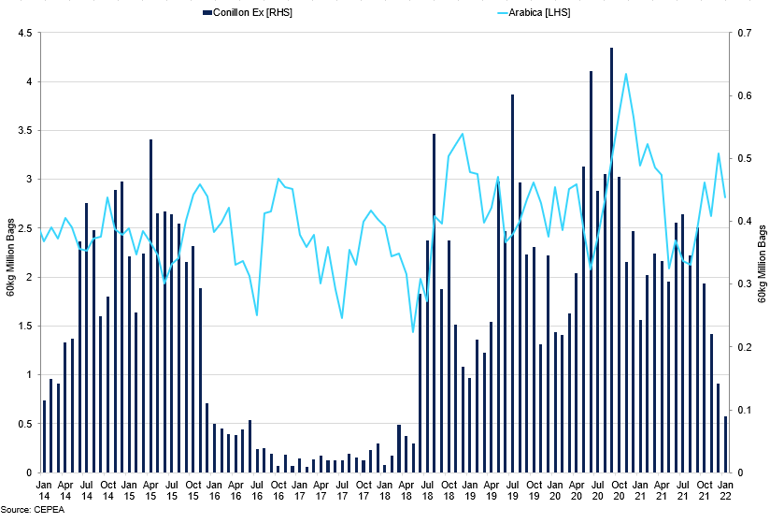

Brazil Conillon and Arabica Exports

Conillon exports continued to decline, as Brazil’s internal consumption increased.

In the period October 2021 to January 2022, Brazil shipped 12.340m of green coffee; Arabica was 11.676m. Soluble was at 1.458m, but it is all conillon. The green shipping number is higher than we expected, and this could be due to the recent switch to shipping break-bulk. In January alone, Brazil exported 3.2m bags, of which 2.8m were Arabica – 8th consecutive month of year-on-year declines in exports but still higher than expected. However, we did not see an increase in stocks as a result, which means that coffee is going straight to the consumer. Brazil currently accounts for 39% of the inventories monitored by ICE, down from as much as 55% last year. While Arabica exports dropped by 10% y/y in January, conillon shipments declined significantly, falling by 63% during the month – the 4th consecutive decline. Brazil is consuming more conillon internally, especially given its price differential to Arabica. Overall, the crop is well down, giving Brazil less to ship, with only some carryover stocks left. We expect the shipments to slow in the coming months, and we have to wait for the new crop to come out. The projections for Brazil's 2022/23 crop indicate that we will continue to see further deterioration to the yields when harvested in May. That will limit the rebuilding of stockpiles needed to weather the typical dip in the following harvest's output.

Washed Arabica

Arabica 2nd month futures gained c95.85 in 2021, closing the year 76% higher at c226/lb. As of February 22nd, the price stands at c250/lb. We believe that any stock of spare coffee has either been shipped or is in the process of being shipped from producer to consumer countries. ICE December 2020-21 total exports totalled 128.92m bags, slightly down from 129.41m in the 2019/20 season. Colombian exports for the 20/21 crop season totalled 12.522m bags vs 12.491m bags in 19/20. Shipments of green coffee from the biggest port of Buenaventura totalled 557,292 bags (down 36%), closing 2021 at 11.828m. Likewise, production in October to January 21/22 was 577,000 bags lower, down 19% y/y, at 4.157m, as too much rain is hurting production. However, given high coffee prices, export value in December reached $329m, the highest monthly reading since March 2011. Imports from Brazil through 2021 stood at 1.162m bags. More recently, Colombia has cut tariffs on agricultural products to help curb inflation, which could mean more imports of coffee from Brazil. Colombian differentials have remained firm throughout 2021 at +60 cents per lb. Over the next five months, we would expect to see Colombian exports remain soft at around 1m bags per month. Indeed, January exports were already at 1.063m, and with production now dropping to 2m, this will come into the exports. As a result, GCE Colombian stocks are continuing to decline, now in line with 2015 lows at 5.795m bags.

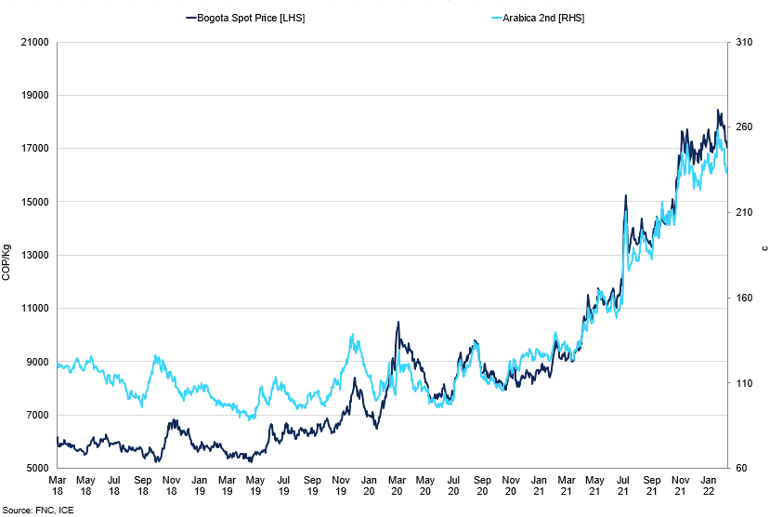

Bogota Local Prices vs Arabica 2nd

The local prices have strengthened, further beating the multi-year highs.

In Central America, where the harvest is peaking, Honduras saw a jump in exports last month. Although January 2022 exports were 522,865 bags vs 465,476 in 2021, they fall short of the 719,000 shipped in January 2020. Honduras Exports October to December 2021 stand at 480,816 bags vs 278,000 in 2020 and slightly behind the 522,000 bags shipped in the October to December period 2019. Central America has been lowering production in the last 20 years, and now there is no extra coffee available coming from Honduras, but demand for centrals has increased. But, over the past couple of weeks, diffs have firmed to +c38/lb on a lower 21/22 crop perspective. Last month, during the elections, the new president Castro took power. Honduras has taken emergency steps to its public finances in order and sought international investment as means of managing its debt issues. Any significant plans are likely to have a lag effect, and in the immediate term, the growth outlook remains thin, hindered by slowing investment and low productivity growth.

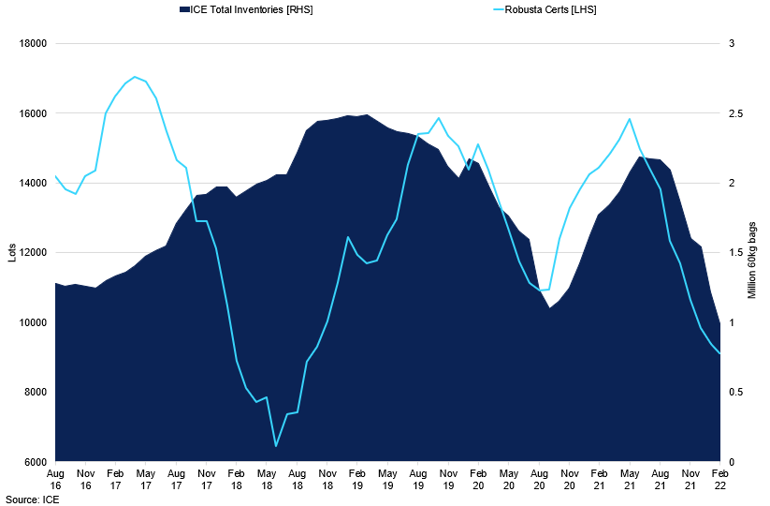

ICE Total Inventories vs Robusta Certs

Inventories continue to draw down, as coffee is being sold straight to the market.

Overall, the market is 100c higher than six months ago, and so the producers will be shipping as much as they can. Coffee reserves certified by ICE have been falling since September due to soaring shipping costs and unfavourable weather that clipped production in Brazil. We continue to see a fall in certified stocks number, with the US ICE now at 1.027m, a 2000 low. The fall below 1m would most likely trigger a reaction in the market, but there is still coffee available in stocks, and we are likely to see a case for significant shortage building in July this year. The supply chain bottlenecks mean that certified stocks will fall further as roasters look to secure products. The GCA stocks came at 5.795m bags, down by 37.8k m/m. Likewise, in Europe, the certs continue to decline, with 889k bags now in Antwerp and 79k in Hamburg, the former has 90% of all available stock. Europe demand could see a push in demand after lockdown measures ease. The US then got 58k bags, which is not much at all, since it is all being shipped straight from Brazil straight to the consumer. Certified stocks at the end of January stood at 1.218m, down 381,022 from 1.599m in November. As of February 18th, the number was at 1.007m, a further 211,302 bags lower, although we do have 100,254 bags pending re-grading. Our thoughts are the same as in past reports, this coffee remains the cheapest for the industry, and in our opinion, unsold certified coffee is between 550,000 and 700,000 bags. We see a structural deficit due to the significant drop in Arabica production in Brazil, and we do not see any other regions that can fill this void. Brazil shipments were above 3m in January, but still certified stocks dropped below 1m bags, in our view this outlines the lack of coffee availability.

Robusta

Elsewhere, Vietnam exports for January were seen at 163,324 tonnes, down 3.6% m/m and up 1.8% y/y, a marginal decline in comparison to Brazil. Customs data for January 2022 indicated 193,377mt green Robusta exports from Vietnam. These numbers are the highest level we have seen since 2019, and we see that Vietnam has plenty of coffee. However, while they are exploring it, we do not see a shift to more Robusta blends on the market as of yet. For the 20/21 crop, Vietnam shipped 25.805m bags vs 25.305 in 19/20. For 21/22, our Vietnam number is at 29m bags. With 26m needed for export, and 2m for internal consumption, the country produces just enough to cover the demand. Local prices have rallied and now stand at VND41,500/kg, the 2017 highs, and we have seen producer short position increase at that time. The higher prices continue to bring steady flow from producers. May-May spread is at $36/t.

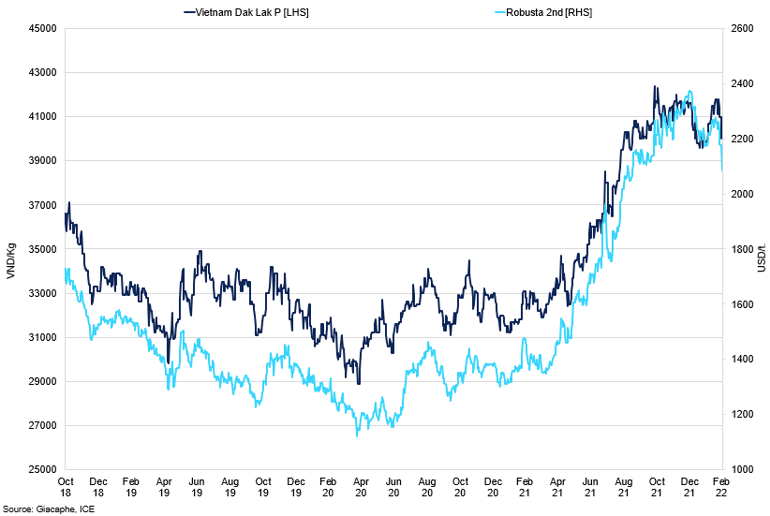

Vietnam Dak Lak prices vs Robusta 2nd contract

Local prices have outperformed the London contract in 2022.

Stocks increased, and there is more Robusta in the market, but this could be attributed to the fact that more conillon have been coming from Brazil. Stocks should start to disappear, especially as Brazil imports more conillon for internal consumption. Robusta has the potential to go to higher, as it follows Arabica. With farmers mostly sold, exporters remain keen buyers on the back of external demand.

Shipping and fertiliser

We have seen some exporters use bulk shipping instead of containers to cut down on costs and ship coffee. However, this transportation process could be quite detrimental to the coffee bean through exposure to changes in temperatures and moisture, and the quality of coffee could suffer significantly as a result. We will wait and see at the grading stage whether the December and January shipments through bulk managed to pass to warehouses. Indeed, if the coffee got mould or other defects, this would be thrown out at the grading stage. While there have been rumours that breakbulk shipping rates might be much cheaper than container rates, we do not think this is true, and break-bulk has been used to move coffee around at a time when it has been hard to secure a container. Time will tell how successful this will be from a cost perspective.

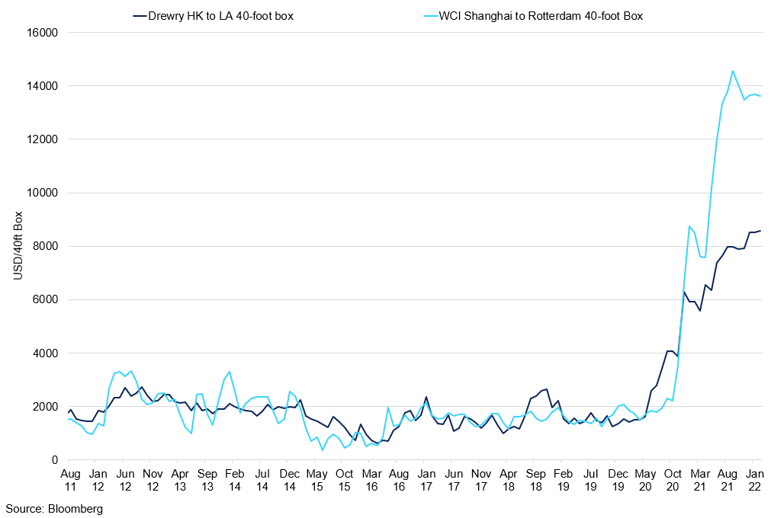

Shipping Rates from Hong Kong and Shanghai to Rotterdam

Shipping rates are past their peak but continue to remain elevated against the robust backlog of orders.

Soaring fertiliser prices are adding to farmers' woes, while elevated freight costs and a lack of container ships hinder exports. That has stalled shipments of millions of bags of coffee out of Brazil. More recently, conflict in Ukraine has led to a wide range of sanctions to be imposed on and by Russia, targeting trade with the rest of the world. This is further coupled with the recent broad ban on fertiliser exports, of which Brazil is a top importer, further reducing the availability of fertiliser supplies coming from Russia. As a result, to cut down on costs, fertiliser is not being used to the same extent at the moment by Brazil. More so, we have seen a slight shift by farmers as they look at other types of crops that require less fertiliser use in farming, which could hamper coffee production in the longer term.

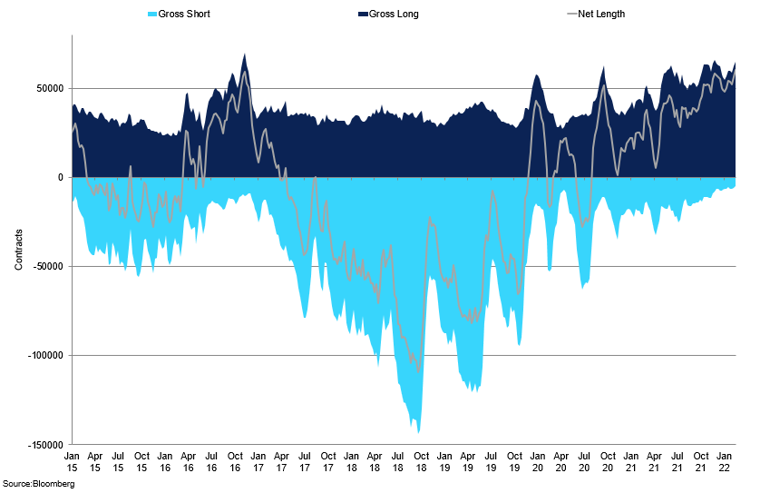

Commitment of Traders'

Supplemental data for Arabica shows an increase in the non-commercial position by 3,882 contracts week-on-week, making an advance of 10,971 contracts since the start of the year. The net position now stands at a length of 50,392 contracts, the highest level since November 2016, as the short position reduced to the levels not seen in November 2014 at 9,834. The longs increased to 58,716. The number of long traders has increased to 169 in February; a similar level was only seen in November, when the price was 100 cents lower. It has since come down to 163, in line with the positioning softening to 58,716 in the week ending February 22nd. This recent softness has been triggered by the built-up of geopolitical tensions in Ukraine.

2nd Month Arabica Managed Money Commitment of Traders

Net short reached the levels not seen since November 2016.

The commercial position also tells an interesting story; we saw a reduction in the net short position in the first two months of the year, falling by 3,716 contracts to a -100,516. The gross short position has declined; however, the total gross short is 183,302 contracts, a decline of 14,935 contracts in the week to February 15th. The industry has done some buying, but they are still behind, and there is still more buying to be expected. Their cover is tight, leaving commercials to buy the physical coffee. The fundamental outlook is robust, and the gross short should increase further.

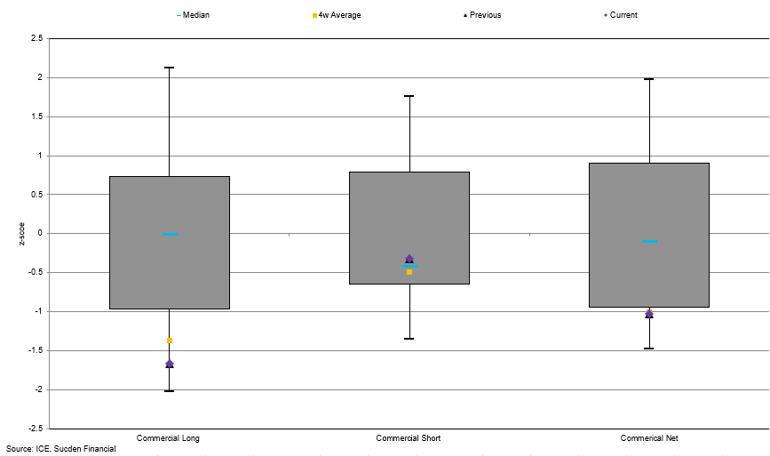

Commercial Supplemental Arabica Normalised Positioning

The 4-week average has fallen below the median level, suggesting lower than expected performance.

The Robusta commitment of traders for managed money shows an increase in the net long by 3,866 contracts to 39,169 in the week ending February 22nd. The gross long for futures stands at 40,477, an increase of 3,881 contracts, which has been driving the net higher, as shorts remained low at 1,308. However, we have seen less managed money traders, falling to 40 in recent weeks, suggesting deteriorating conviction in the market. The producer long traders have plummeted to 36 since the recent peak of 45. The net position has also declined to a net short of 44,573. The gross short has declined to 86,937. In our view, because of the Arabica market, Robusta purchasing has been made an attractive buy, and we anticipate further non-commercial buying as the price rises in line with Arabica.