Executive Summary

- Globally, the strong recovery in some economic sectors seems to be subsiding, partly due to the resurgence of COVID-19 cases in major economies

- With election results now behind us, the downside risks prevail around the speedy approval of a vaccine, and the scale and scope of policy responses required over the winter

- We believe that Biden will face a significant headwind from Republicans, stalling his plans to unwind most of the projects Donald Trump has put in place

- Nevertheless, we expect a new stimulus package to take place, potentially enacted before his inauguration next January

- Returning to pre-crisis levels will be challenging, and recovery paths will differ significantly between countries, especially in the vulnerable service sectors

- China's output is already back to the pre-pandemic levels, credit is growing rapidly, and fiscal policy remains expansionary

- Corporate earnings results have improved in Q3, however, still declined moderately year-on-year

- Demand for at-home consumption remains strong; despite rising drive-through sales, the out-of-home demand remains muted

- On October 30, Dunkin’s Brands has been acquired by Inspire Brands for $11.3bn

- The producing countries have provided fiscal stimulus measures to support the recovery, however, much will depend on the spread of the COVID-19 infections and deterioration of public finances

- We have seen the Real recover some ground since the results of vaccine, we could see more flows into riskier assets such as EM currencies

- We have re-evaluated our COVID demand model below and continue to present two scenarios

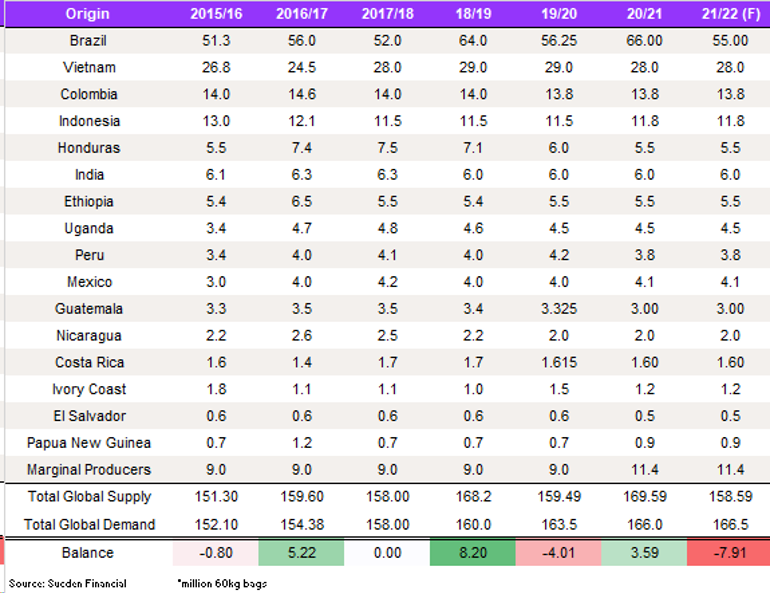

- For the 19/20 season demand took a hit from COVID-19, with demand dropping to 163m bags, reducing the deficit to 3.5m bags.

- The Chinese economy has recovered well, demand in mainland China has been a bright spot this year. China’s consumption conditions remain supportive for coffee and we expect this to continue in 2021

- We expect the U.S. economy to recover before Europe and this will see US demand return to growth before Europe

- Consumption trends this year have changed, we expect more relaxed office hours to increase the at-home consumption going forward

- Consumers want more transparency and sustainable practices; farmers can reduce the impact on biodiversity and ecosystems with improved techniques. However, packaging is a huge part of being more environmental

- Chen, Pelton, and Smith 2016, and other studies, outline that some bioplastics are more impactful than fossil plastics. This highlights the need for companies properly research materials that reduce the impact on the environment and not just adopt a material that may sound better to consumers, to improve sales

- At this period of the crop, rains have not been beneficial, indeed, if this rain pattern continues into February, we expect there to be more damage to crop

- Semi-washed Arabica has gained traction in recent months, as the pass rate has increased inventory levels in exchange warehouses. We expect the quality of the semi-washed coffee to start to fall in the coming months

- It is too early to assess the damage to the Central American crop from the hurricanes

- Brazilian shipments have not disappointed, suppressing any fears of any lack of containers or storage

- For the 2019/20-season between October and September, exports for Central America were down 10.8% on the 2018/19 season with the 2019/20 season total shipments at 16.54m bags vs 18.34m bags for 2018/19

- We expect the Indonesian Robusta crop to be strong in April and May, this could push pressure on Robusta prices

Global Economic Review

Global

Regarding the global outlook, the strong recovery in some economic sectors seems to be subsiding, partly due to the resurgence of COVID-19 cases in major economies. This has the potential to significantly slow down activity in consumer-facing industries that are currently operating below capacity. There is significant uncertainty regarding economic outlook, which will depend on a couple of key factors. The stimulus bill in the US remains gridlocked, and with cases in the country on the rise, the potential for another quarter of economic recovery is limited. With election results now behind us, the downside risks prevail around the speedy approval of a vaccine, Brexit negotiations and the scale and scope of policy responses required over the winter.

It is now clear that the policy response to the outbreak of the pandemic has not just dominated the economic development in 2020 so far, but also set the starting point for 2021. Indeed, countries around the world had to face historic adverse hits to their economies in H1 2020. While the lockdown measures implemented during the first wave of coronavirus infections were unprecedented in most countries, some have succeeded in getting the virus under control. In Q3, we saw some significant rebounds to economic growth as the economies relaxed the lockdown measures across the world.

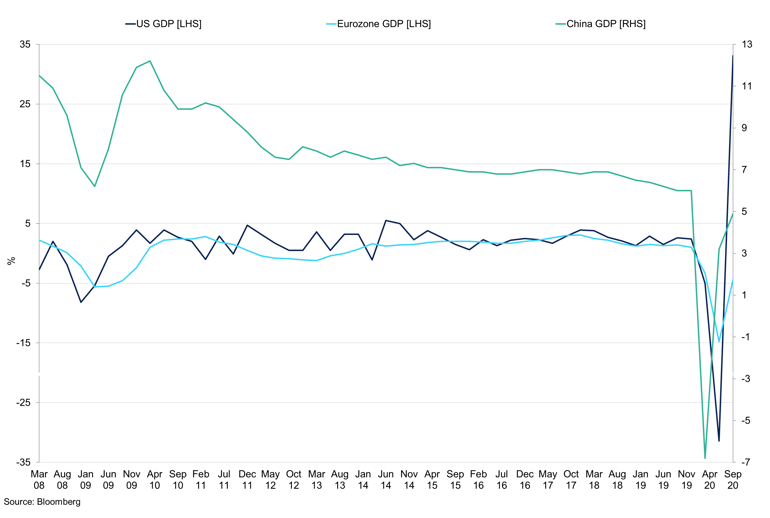

GDP Growth for US, EU, China

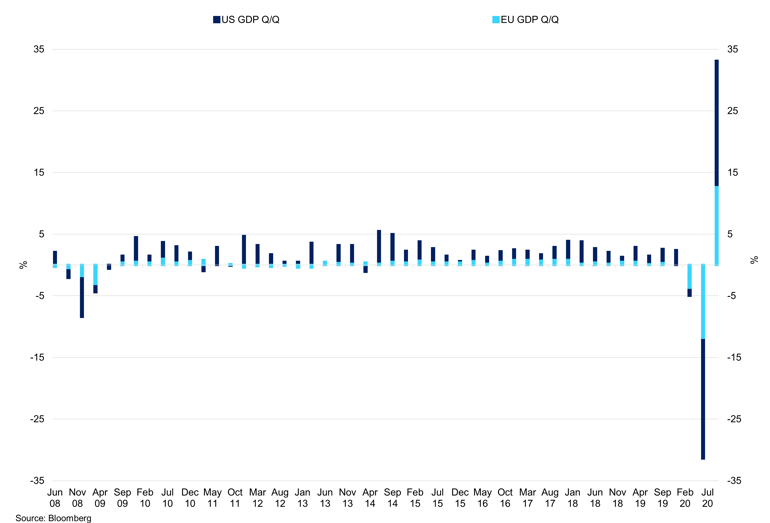

GDP for major economies rebounded sharply in Q3 on the back of easing of lockdown restrictions.

While there is generally a more positive outlook in comparison to Q2 2020, the divergence between sector performance is likely to widen in the last quarter of the year, especially between manufacturing and services. However, even in the most negative scenario, another plunge seen in Q2 is highly unlikely, as the world seems to have adapted to the risk of outbreaks via measures such as social distancing and working from home, allowing for consumer-facing industries to operate, despite lower overall demand. Additionally, with hopes of country-wide use of a vaccine next year, the path to recovery could be more clearly established. If fiscal and monetary policies are to remain focussed on supporting household income and cash flows to businesses during any renewed containment measures, we would expect a bounce back in demand.

The central banks are likely to remain dovish for the next couple of years. Indeed, even under the scenario of a strong growth rebound, labour market conditions would take longer to normalise, and inflation looks set to remain below central bank targets for the long run. A rebound in economic growth in 2021, therefore, could be followed by a renewal in hiring, resulting in temporary acceleration of economic growth and inflation. For 2021, we foresee inflation to be higher than that seen in 2020, however, below of 2019, as consumers will take longer to adjust back to ‘normal’. The risk of long-term inflationary pressures, however, prevails, and we believe that central banks have adequate tools to avoid it. The main focus will remain on fiscal support in the meantime.

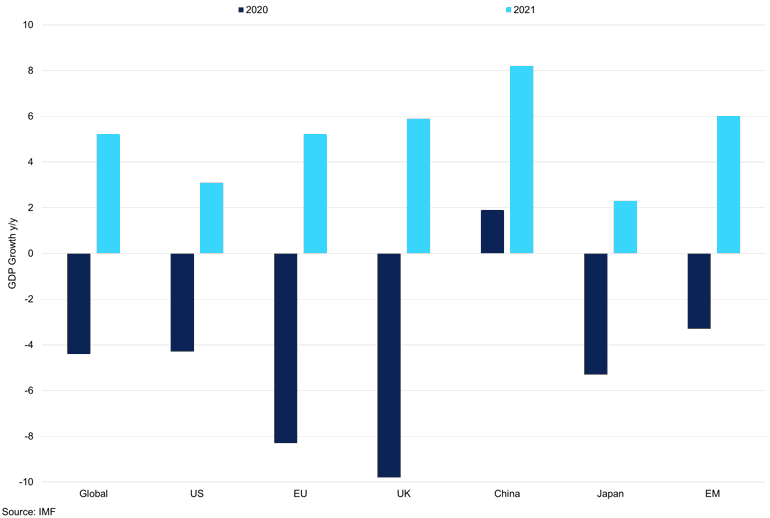

Growth projections 2020 vs 2021

While China is one of the few economies forecast to grow this year, next year the world will grow at 5.2%.

We expect economic output to reach pre-pandemic levels by the end of 2021, enabling economically sensitive markets to catch up. Indeed, the global economy is forecast to grow by 5.2%, with the US, Europe and China recovering faster than other economies, as demand continues to pick up from the recession lows. With policy rates close to record lows in all major developed economies for the long run, the equity market should continue to provide attractive returns. Given continued government support through most of 2021, and the implementation of the vaccine driving the industries back to ‘normal’ activity, we would expect a rebound in the service industry and increased spending on non-durable goods.

US

The US economy is forecasted to rise by 2.2% (annualised rate) in Q4 as it continues to battle the growing number of COVID-19 cases. Indeed, while it seems that the economy has partially rebounded from a deep contraction seen in H1 2020, the spread of infections, unemployment levels, additional fiscal stimulus measures, approval and the country-wide distribution of a number of vaccines will drive the market growth. Just as a GDP rebound seen in Q3, we would expect equally strong growth given a vaccine becomes available. Assuming the FDA approves any of the candidates by 2021 and country-wide implementation starts shortly thereafter, growth should pick up sharply.

Despite the record-breaking growth performance, both negative and positive in 2020, the sector that has been resilient during the downturn, and is most likely to remain strong is housing. Housing permits and starts have returned to the pre-pandemic levels and are likely to keep growing further as a result of a sharp acceleration in home sales. This could be attributed to several factors: low mortgage rates, increased general interest, and supported incomes through government protection schemes. We expect this trend to continue in the long term, driving the housing market. However, given a robust economic recovery in 2021, the housing prices could skyrocket, therefore, diminishing buyer demand.

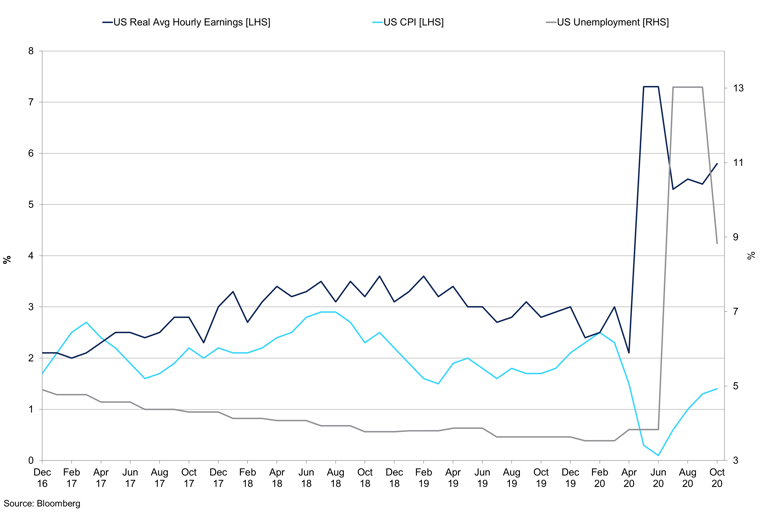

US Real Average Hourly Earnings vs CPI vs Unemployment

The unemployment has fallen from record highs, however, remains above the pre-crisis levels.

When fiscal stimulus expired in the US at the end of July, there was an expectation that it would lead to a rapid decline in consumer spending. This did not happen. Instead, while personal income fell sharply, consumer spending only decelerated. In September, retail sales increased by 1.9% m/m, above expectations, as the nation continued to spend, using their savings and borrowing more at record low rates. When the cases in the US started to rise, the situation reversed, and the retail sales decelerated sharply, yet still growing at 0.3% m/m. While it is reasonable to assume that with the introduction of new lockdown measures in the country, retail sales would fall, we believe that this has been driven by a sudden belief that additional government support might be delayed or not come at all. We believe that sales are likely to continue decelerating through November - December.

With Biden now in the office, we take a look at the way his presidency could shift economic outlook in 2021. Biden suggested that virus suppression will be the first order of business, especially at a time when the virus appears to be spiralling out of control. The number of new daily cases in the US is now about twice the size of the summer peak, with the number of daily deaths at the highest level since May, and public health officials claim that the worst is yet to come. Biden's new plan envisions free testing for all, more spending on medical equipment, enhanced guidance to state and local governments for virus suppression, and obligatory mask wearing. The president-elect also intends to shift the allocation of COVID-related federal funds. His team also wants to divert some of the funds from vaccine research toward improving testing.

Ultimately, his policies include relaxing the immigration policies, re-joining the Paris Accord and the WHO. On the trade front, the reduction of tariffs on China is possible along with changing rules regarding cross-border investment. On the other hand, with a divided government, there are many legislative actions that Biden had proposed that are likely to be stalled or not happen at all. These mostly cover additional fiscal spending, including raising the federal minimum wage, expanding the Affordable Care Act, raising taxes on the top 5%, and increasing the corporate tax rate. The infrastructure investment proposal, however, might have a chance given that there are some Republicans who favour this kind of expenditure. We believe that Biden will face a significant headwind from Republicans, especially in the first year of his term, stalling his plans to unwind most of the projects Donald Trump has put in place. Nevertheless, we expect a new stimulus package to take place, potentially enacted before his inauguration next January.

Europe

Eurozone has experienced tough lockdown measures in summer, and, as a result, economic indices fell to record lows. Indeed, the pandemic, along with the accompanying restrictions hit the bloc extremely hard in Q2. Among countries within the bloc, the difference in economic performance depended on the success of controlling the spread of infections and the length as well as the severity of lockdown. Returning to pre-crisis levels will be challenging, and recovery paths will differ significantly between countries. Indeed, the economies in the bloc are contracting quickly, particularly in the vulnerable service sectors. It is now clear that many economies will keep the lockdown measures in place until December.

A contraction in Q2 was mainly due to consumer spending, which contributed 7pps to an 11.8% decline in GDP. Both private and public consumption fell drastically, 12.4% and 2.6% respectively. The fall in public spending seems to be counterintuitive but could be explained by the fact that most of the fiscal packages came into light and financed in Q3. As for private spending, the reduction in disposable income led to a fall in demand for durable goods. Indeed, accommodation and food, automotive, and transport and storage were the sectors that have been hit the hardest in Q2, with revenues falling by 65%, 50%, and 23% y/y respectively.

Despite a sharp drop in spending, economic policy measures softened the blow on the labour markets. In many countries across the bloc, short-term work schemes have been implemented in order to support activity in order to prevent a massive wave of unemployment. Indeed, the four largest economies have implemented these measures to buffer the impact of the pandemic on household's disposable income. In France and Italy, 40% of those who have been temporarily let off have been covered, in Germany and Spain, this share came to 20% of employees. Employment data shows that the work hours declined by 16% y/y in Q2, while the number of people employed decreased only by 3%, suggesting that people stayed in work, but worked fewer hours met with reduced demand for services.

Even though there are many restrictions in place that are likely to remain until the end of this year, business sentiment has significantly recovered in comparison to the summer period. The EU Commission's economic sentiment indicator is seen rising steadily but remains below pre-crisis levels. The manufacturing PMI, however, continued to strengthen due to increased demand and improving export conditions. Continued uncertainty should weigh on business investments, and the ongoing health crisis in some of the bloc's biggest export markets will likely prevent a fast recovery to pre-crisis levels. The speed at which the economy will recover depends on the consumers and indirectly on the labour markets.

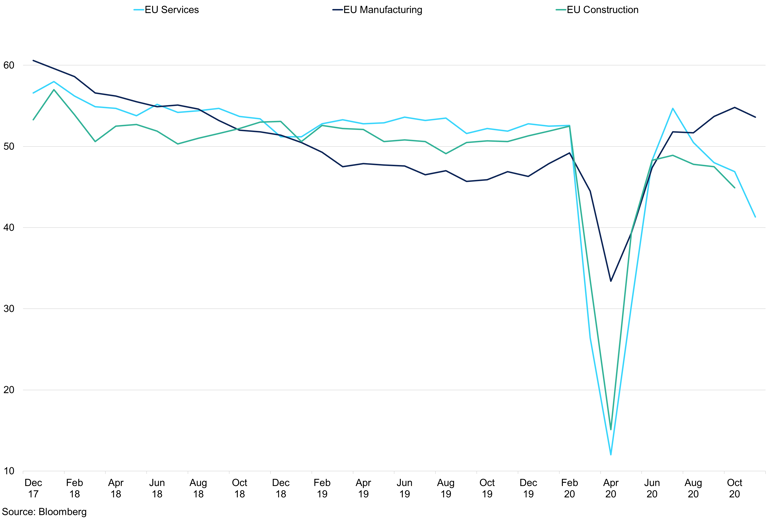

Services PMI vs Manufacturing vs Construction

EU services and manufacturing activity has started to widen since the summer period.

The service sector remains on the back foot, as accommodation, as well as food and beverage service, continue to suffer from restrictions. Mobility in Europe is strongly correlated with the country's PMIs for the service sector. For the October period, the PMIs were already below 50, indicating that the sector is contracting. If mobility indicators remain subdued for the rest of the year, then we will likely see much lower service PMIs for subsequent months and therefore a larger contraction in services. This could raise the probability of GDP falling once again this quarter.

China

China's exports continued to grow in October, up 11.4% y/y from 9.9% y/y growth seen in September, the fastest export growth in more than 18 months. Imports were up 4.7% y/y. Regardless, the strength of China's exports comes at a time when global demand remains relatively weak. Therefore, this strength highlights the continuing competitiveness of Chinese industries. Indeed, China's exports have been supported by strong global demand for medical equipment as well as remote working technologies and consumers demand goods as opposed to experiences, giving Chinese industries an edge during the pandemic. That said, the rally in infection rates in Europe and the US suggests the possibility of a further slowdown in demand, which could adversely impact Chinese exports. China was the best performer in emerging markets in Q3; however, intensifying tensions with the US, highlighted by the US crackdown on China's leading tech firms, pose additional risks to the already-sour relationship.

We believe that Biden might take a tough stance on China-US relationship, especially, on the topics concerning human rights issues and general market practices. However, he is more likely than Trump to seek multilateral partnerships and implement a different approach to their relationship. Biden may still face tensions between reengaging more with other allies on trade while seeking to rebalance the trade negotiations with China.

China's output is already back to the pre-pandemic levels, credit is growing rapidly, and fiscal policy remains expansionary. Policymakers look set to ease off the accelerator, which should result in a modest sequential growth slowdown. Indeed, while the implementation of the vaccine across the globe is likely to contribute to a significant spike in growth in both the US and Europe, China is likely to benefit from it much less given its already-recovered economy. For Q4, high-frequency indicators suggest further solid growth and at least some possibility of a trade easing with the US under the incoming Biden administration. Given this favourable backdrop, Chinese policymakers have started to redirect their attention to the risk of future financial instability from excessively loose lending conditions.

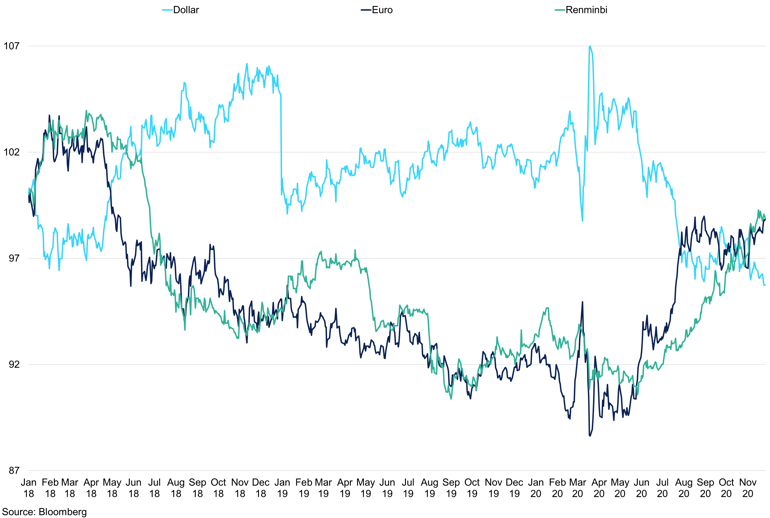

CNH vs DXY vs EUR

Most of the major currencies strengthened this quarter on the back of a weakening dollar.

For the financial markets, the main implication could be higher interest rates, at least relative to the record-low levels seen across the world, and, in turn, leading to currency appreciation. These are key aspects of the broader monetary and fiscal policy normalisation that largely explains why the Chinese economy will finish the year on the front foot.

Brazil

In Q2 2020, Brazil slipped into recession as the spread of the pandemic weighed on economic activity. Consequently, lockdown measures and rising rates of unemployment affected consumer spending significantly. Indeed, private consumption contracted by 13.4% y/y in Q2. Business uncertainty has also increased, and in turn, the gross fixed capital formation fell by 15.2%. While fiscal stimulus measures have supported an economic recovery later in Q3 2020, it is still too early to say whether growth will continue by the end of this year. According to the IMF, Brazil GDP is forecast to fall by 5.8% in 2020, below India and South Africa. We are of the opinion that economic recovery is underway in 2021, however, as with other economies, much will depend on the spread of the COVID-19 infections and deterioration of public finances due to strong fiscal stimulus packages will remain areas of concern.

The Brazilian government, however, expects a fall of GDP of 4.7%. For 2021, the forecasts stand at 3.2% growth. Evidently, the speed of economic recovery will depend largely on the course of the pandemic in Brazil and the rest of the world. With new daily cases currently below its July peak, the incidence is still high, with 35,000 cases per day on average. Even if a vaccine is approved by early 2021, ensuring production and supply will depend on supply chains across the globe, and Brazil may face some major challenges rolling out inoculation programmes in time with other developed economies.

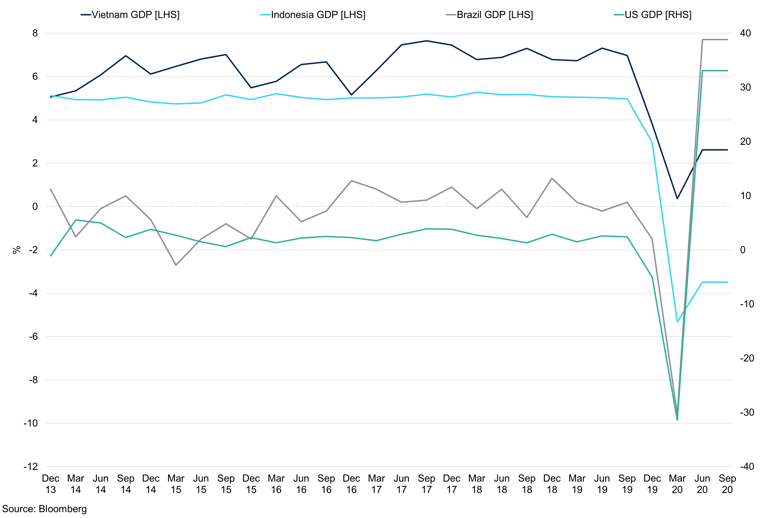

Vietnam vs Indonesia vs Brazil vs US GDP

While the US economy has seen a sharp rebound in economic output, emerging economies are yet to return to pre-crisis levels.

The government officials noted that the services sector, which accounts for 70% of Brazil’s GDP, has been slow to recover from the pandemic shock, but is starting to show signs of improvement in Q4. Sectors more directly affected by social distancing measures remain depressed despite the offsetting effects of the transfer programmes. Prospectively, uncertainty about economic growth remains larger than usual, especially for the period starting at the end of this year, concurrently with the expected unwinding of the emergency transfer programmes.

Consumers also appear to be increasing spending as the economy continues to reopen. Indeed, retail sales volume has been picking up since May, which stood at 12.2% m/m, higher than the pre-crisis levels. Since then, the trend decelerated, yet remained in line with the pre-crisis level. Trends in consumer consumption show that, in line with other economies, customers are spending more on groceries and household items and cutting down on non-essential purchases. Nevertheless, despite a slight recovery in retail sales, consumer spending faces continued risks from a weak labour market. Employment fell by 11.5% in the first six months of 2020, with the 3-month unemployment rising to 14.1% in Q3 from 11.2% at the beginning of the year. This, along with expectations of weak economic activity, will weigh on consumer confidence, and therefore, spending.

The fiscal response to the pandemic crisis has been strong. Alongside additional funds to tackle the pandemic, the government ensured that fiscal support was provided for both household and businesses. Indeed, low-income homes benefitted from cash transfers and bonus payments were awarded to select people in the labour force. Businesses were supported through tax breaks, expansion of credit lines and partial compensation to workers for reduced working hours. The total fiscal measures should add up to 12% of GDP, according to government officials. At the same time, due to the unprecedented levels of government support needed during the COVID-19 pandemic, Brazil’s debt is forecast to reach $112bn in the first four months of 2021, or 14.1% of the economy’s GDP. Reduction of average length on debt maturities along with low interest rates brought costs down to the record lows, increasing the roll over risk for the Treasury sharply.

However, while these measures supported short-term economic recovery, the sheer size of the package will deteriorate the government's balance sheet. Indeed, in Q1 and Q2, the budget deficit widened significantly from 6.31% in Q3 2019 to 13.73% of GDP in Q3 2020. As borrowing to fund stimulus surged, government debt went up - gross general government debt surged to 90.55% of GDP in September from 76.18% in January. In the long term, this rise in government debt and deficit levels should make it harder for the government to finance spending in the future. We expect that in 2021 bond prices will depend largely on government finance handling and ability to provide more support packages if necessary.

From the monetary policy side, the interest rates were cut by a total of 250bps since January. As the economy is currently within its inflation ranges, the BCB is likely to go for further cuts. Additional measures include reduction of reserve requirements from 25% to 17%, capital conservation buffers, and launch of a credit facility by the central bank.

Indonesia

In Q2, Indonesia's GDP was down 5.32% y/y due to falling household spending and investment. Whilst the contraction in Q3 was weaker, 3.49% y/y, the economy has entered a technical recession. According to IMF, Indonesia's GDP is expected to decline by 1.5% in 2020, more than previously expected 0.3% projection in June, as Southeast Asia's largest economy struggles to contain the spread of the COVID-19 infections. Indeed, as of November 15th, the number of daily new cases stands at above 5,000. The IMF projection is largely in line with the government's estimate of 1.7% decline, down from 5.02% in 2019. The government expects an additional 4m to fall into poverty and 5.5m to lose their jobs during the pandemic.

To cushion the economy next year, the government is said to prepare $186.3bn in-state expenditures to fuel the virus-battered economy. A large chunk of the spending will be allocated to infrastructure, education and healthcare. Therefore, the budget deficit is projected to reach 5.7% of GDP in 2021, especially as the uncertainty surrounding the coronavirus pandemic is expected to further deter the activity and eventually tax revenue. The government collected $81.58bn in taxes in the first half of 2020, down 13.7% y/y, as business activity cooled. In 2021, state income is expected to reach $123bn, down from a previous projection due to lower income from non-oil and gas taxes.

Starting mid-September, the city administration of Jakarta, the capital of Indonesia, implemented new lockdown measures. However, Indonesian consumers seem to be more confident than their peers about the future economic outlook. Indeed, according to the PWC survey, 64% of Indonesian consumers said that they are going to spend more once restrictions are lifted, compared to 33% in global survey results.

The recently approved Omnibus Law on Job Creation in October is designed to enhance the business climate, aiding market flexibility, which should improve the country's international competitiveness. This law should help reduce longstanding hurdles to doing business in Indonesia by reducing red tape, simplifying land acquisition processes, and easing restrictions on foreign investment. Indonesia's current ranking of the ease of doing business remains just above the median, 73rd of 190 countries in 2020, and the inward foreign direct investment in Indonesia averages at 2.0% of GDP, compared to 6.0% in Vietnam.

Many countries are exploring the ideas of diversifying the supply chains away from China, as a result of rising labour costs in that market and the uncertainties created by US-China trade tensions. Many have relocated operations to Indonesia, but the local business environment may have served as a dampener on investor interest. The reforms should put Indonesia in a better position to capitalise on shifts in global manufacturing supply chains and will foster Indonesia's long-term economic growth prospects.

Vietnam

Despite the success so far in containing the spread of infections due to contact tracing and quarantining, the economic performance of Vietnam has, nevertheless, been severely impacted by the pandemic. After annual GDP growth rates of an average of 7% for most of the decade, economic growth is forecast to slow down to 2.3% in 2020, in line with other economies that suffered from the spread of COVID-19. However, despite this decrease, Vietnam is one of the few economies that is not facing a contraction this year. For 2021, Vietnam’s officials have targeted economic growth of 6.5% next year, signalling a return to the pre-pandemic growth pattern, as the manufacturing-led economy emerges from its current slowdown.

Vietnam, population 97 million, has managed to keep its reported Covid-19 cases down to 1,068, allowing work, in-country tourism and services to keep operating after the implementation of lockdown measures in April. Nevertheless, due to lower global demand, investment spending and private consumption growth are expected to slow down to 0.4% and 4.0% in 2020 respectively. Due to the global economic slowdown, export levels are projected to contract by 5.5%, and inflation is expected to increase to above 3% in 2020 and 2021.

Producer FX Rates

To support the economic performance, the central bank has lowered the benchmark interest rate to 4.5%, while supporting banks and facilitating loans. At the same time, government consumption increased by more than 7.0%. The government has initiated tax breaks for businesses and transfers to households. As a result, the fiscal deficit is projected to increase by more than 5% in 2020, with public debt picking up to 49.5% of GDP. In 2021, the fiscal deficit should fall to below 4.5% of GDP, due to rising public debt.

The continued dispute with China over claims in the South China Sea continues to strain the countries' relationship. According to government officials, Vietnam is keen to improve its political and security cooperation with the US and Japan in the meantime. Indeed, since formalising the diplomatic relation with the US, the bilateral trade between the two countries increased from $77bn in 2019. While China is an important trade partner to Vietnam, the US had become its largest export market, with Vietnam becoming the US’ quickest growing market.

Corporate Results

Nestle

Organic growth reached 3.5%, with the pricing of 0.2%. Growth was supported by momentum in the Americas, as well as the acceleration of the coffee business in Q3. For the full year, the sales growth forecasts stand at 3%. Coffee posted mid-single-digit growth, fuelled by strong consumer demand for Starbucks products, Nespresso and Nescafé.

Demand for at-home consumption remains strong. Americas grew by 5.1%, with Latin American growth outpacing the one of North America. The beverages posted double-digit growth, with strong demand for Starbucks at-home products, Coffee mate and Nescafé. EMENA saw growth of 2.9%.

China saw negative growth in Q2, turning positive to 2.9% in the third quarter. Regardless, coffee, culinary and ice cream all delivered positive growth, with sequential quarterly improvements. Oceania reported strong growth across most product categories, particularly in coffee and confectionery.

Starbucks

In Q4, Starbucks experienced comparable store sales growth of -9%, -3% in the US and China, sustained recovery from -40% and -19%, respectively. The company opened 480 net new stores in Q4, up 4% y/y, ending the period with 32,660 stores globally. Stores in the US and China comprised the majority of the company's global portfolio at the end of Q4. For the fiscal year ahead, Starbucks plans to increase the comparable store sales growth of 18% to 23%, introduce 2,150 new store openings.

Starbucks has seen its same-store sales, earnings, and revenue plunge. Adjusted EPS and revenue also fell y/y amid the ongoing COVID-19 pandemic. Revenue was above forecasts, however, still declined by 8% y/y; however, same-store sales declined by more than expected.

Starbucks' same-store sales growth plunged in 2020 as COVID-19 forced store closures, and as many customers have stayed away even as most of the shops have reopened. Rising drive-through sales have failed to offset these declines. Starbucks Rewards loyalty programme members in the US increased to 19.3 million, up 10% y/y.

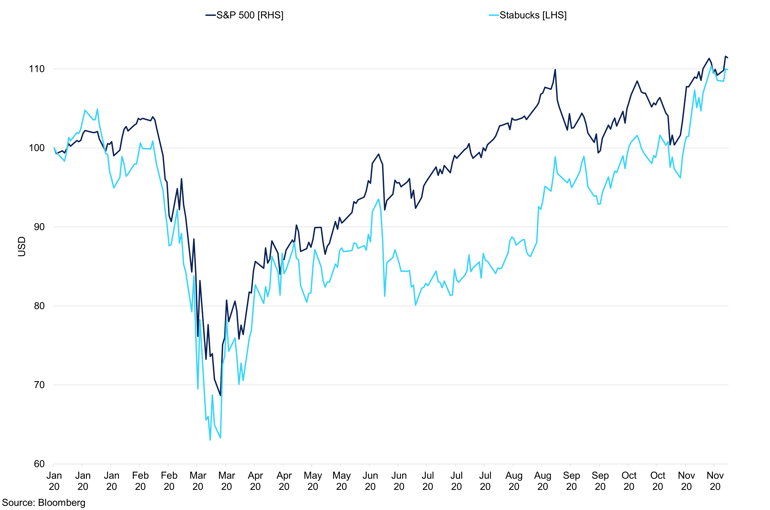

At the beginning of 2020, Starbucks shares were in line with the broader US market. However, as the market crash took place in February, the stock has been underperforming due to the closures of stores across the world. Starbucks' shares are trading 9.5% YTD, a few percentage points lower than the S&P 500's return of 11.9%.

Starbucks vs S&P

Starbucks shares have following the general American market before the pandemic hit, and now are significantly behind.

JDE

JDE Peet’s in-home sales reached record highs for the first half-year of 2020; this growth was primarily driven by developed markets. In H2 2020, total sales decreased by 1.1%, while CPG sales continued to grow. The measures taken by the government to prevent the spread of COVID-19 resulted in a noticeable shift in coffee and tea consumption from away-from-home to in-home purchases, and to a significant increase in sales through e-commerce. The latter grew up by 63% y/y.

Consumer package performance largely offset the away-from-home purchases, which represent 25% of JDE Peet’s total sales. Out-of-home sales have been significantly impacted through H1 2020, as many offices, bars, and cafes were shut down, with volume/mix growth falling by 29.6% y/y. Limited service was maintained where possible in our coffee stores with pick-up and delivery. In June, as lockdown restrictions were partially lifted, the away-from-home sales picked up.

In Europe, reported sales increased by 3.7%, which was driven by the continued success of Beans and Single Serve offerings, as well as increased at-home consumption. LARMEA (Latin America, Russia, Ukraine $ EECA, and MEA) sales fell by 3.1%, and APAC (Australia, New Zealand, and China) also fell by 1.1%, however, strong in-home growth has been felt throughout all the regions.

Dunkin Donuts

Comparable store sales in the US grew by 0.9% in Q3, while improving sequentially for each month of the quarter. This increase was driven by a shift to ‘family-size bulk orders and snacking attachments, as well as premium priced espresso’. This was, however, offset by increasing discounting. Dunkin has closed net 466 locations in the country, in line with the company’s initiative to close low-volume, under-performing locations. This has been done to enable greater reinvestment into the brand, according to a company statement. As of October 24, 98% of Dunkin’s US locations are open; however, the Company expects a total of 800 permanent closures in 2020. Regardless, revenues picked up 1.6%.

Worldwide, sales declined by 1.3% mainly due to permanent and temporary shutdown due to the spread of the coronavirus pandemic. In Q3, globally, there were net closures of 533 restaurants. Dunkin' International Q3 systemwide sales decreased 14.9% y/y driven by sales declines in Latin America, Asia, and South Korea, offset by an increase in the Middle East.

On October 30, Dunkin’s Brand Group has been acquired by Inspire Brands for $11.3bn. The company took Dunkin’s private shares at $106.50, a 20% premium over the closing prices before the deal took place. Inspire has been seen involved in the operation of its portfolio companies, pushing for more changes to the menu and sales. With Dunkin’s fully franchised business model that was doing well during the pandemic, making it a good target to purchase with debt.

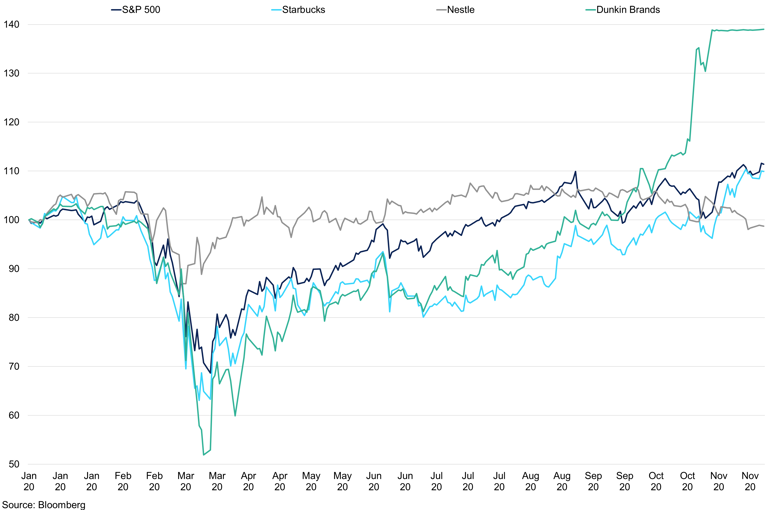

Starbucks & Nestle & Dunkin Share Prices

Supply and Demand Balance

Due to COVID-19, we saw a decline in consumption in the first month of lockdown; and as consumers shifted to consuming at home and coffee shops were closed. As shops re-opened, out of home consumption increased but did not quite reach full capacity across the country. Starbucks earnings reports suggest that sales recovered quickly but remained down, we expect sales to recover and grow in 2021. Our COVID-19 consumption scenario analysis suggested that using a total demand offset of 50% during lockdown and as lockdown restrictions were eased, a total of 3.8m bags of coffee could have been lost, vs 4.829m bags for 30% offset. We expect that the demand during this was higher than this, reducing the total loss for 2020. Conversations with the industry suggest that demand has recovered and could even be flat on the year, we do think that there was a loss of consumption in the first lockdown, and therefore consumption will be slightly lower on year. As mentioned in our previous, consumption in China and S.E. Asia has been strong, this is due to a faster recovery from the pandemic in China, and reduced impact of COVID-19 in some nations. Our demand number for 20/21 has been dropped to 166m bags, this is due to a decline in consumption in Brazil. For the 19/20 season demand took a hit from COVID-19, with demand dropping to 163m bags, reducing the deficit to 3.5m bags. This brings the cumulative balance for 2019/20 and 2020/21 season is flat. As we move into the 2021/22 season preliminary numbers suggest a deficit of 7.9m bags, this excludes our final numbers for Central America, Brazil, Ivory Coast, Colombia, and India for the 2021/22 season. There is downside to these projections, and with demand expected to grow, the fundamental outlook is likely to tighten, once again, we see the deficit in Arabica due to the strong Conilon crop. The cumulative balance for these three seasons is a deficit of 2.78m bags, but as mentioned, it is too early to assess damage to Central America.

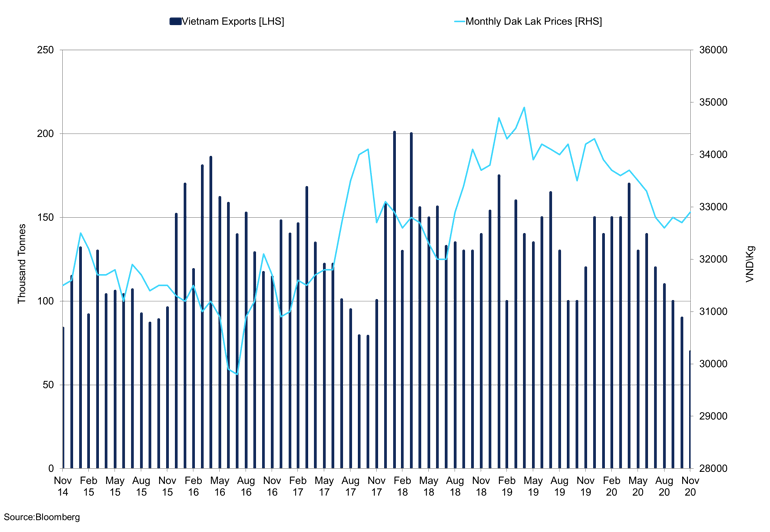

In Vietnam, we expect the crop to be weaker but are keeping our figure at 28m bags. We have seen some softness in the differentials, and we attribute this to an improved off-take in Conilon coffee. The emphasis is off Vietnam now, and while farmers have sold some of their crop, they are not under pressure to sell, right now. The weather was poor in October, but it has been slightly better in November, which has improved harvest conditions. We expect more selling to come towards TET but do not anticipate any aggressive producer selling. Local prices have fallen sharply in line with the London contract, with Dak Lak prices at 32,300VND/kg, with the January 21 London contract at $1,353/t.

Sucden Financial S& D Balance

Demand

2020 has seen significant changes to coffee consumption, this has been outlined in previous reports. The increase in at home consumption due to lockdown restrictions, this caused a significant rise in online coffee sales. Since the end of the first lockdown, we expect demand has taken back some of those early losses in March, and April. As coffee shops opened, we saw a moderate increase in out-of-home consumption, however as coffee shops ran at a reduced capacity due to social distancing. Due to most of the work force still working from home, we saw a shift to coffee consumption in the central business districts to residential areas, and clearly as we have entered Lockdown 2.0 in the UK, and some parts of Europe this trend has remained intact. We do not expect there to be a drop off in demand this time in the UK, Europe or the US as this is now a well-trodden path, in which consumers will revert to their previous lockdown consumption habits. Where we saw pod coffee, and roast and ground coffee demand increase significantly.

Company earnings report show that sales recovered stronger than expected in Q3, specifically in the US and China. This shows us that consumers will revert to previous consumption patterns quickly, when offices re-open and a vaccine is rolled out. Pfizer’s vaccine is reported to have had a 90% success rate, and if further tests prove successful, as things stand, we expect this to be rolled out in 2021, presenting upside to consumption for 2021 and a reversion to out of home consumption as individuals return to their commute. We do believe that at home consumption will increase as there is more flexible working. This could support instant consumption which has been stronger this year, a greater proportion of instant coffee is Robusta. Despite weather problems in Vietnam, we expect the crop to be around 28m bags. Conilon has been taken by the industry, and we expect this trend to continue. Strong Brazilian exports have been strong showing that demand for coffee has improved since the sharp drop in Q2 2020.

We anticipate demand for coffee in major economies to improve and push back to previous 167m bags in 2021. This is on the assumption that a vaccine is rolled out, however, exponential growth will be limited by the high levels of unemployment the US, Europe, and Brazil. The Chinese economy has recovered well in 2020, and this recovery should continue into 2021. According to Starbucks earnings report, they expect comparable store sales to recovery by the end of Q1 2021, and for the full 2021 fiscal year, we expect comparable store sales to grow around 30%. We expect the Chinese economy to continue to grow at a faster pace than the US, and Europe, however, the US is likely to turn around faster than Europe. The recent move from McDonald’s will spend $381m in the next 3 years to expand McCafe in China. Their plan is to have 4,000 McCafe’s in mainland China by the end of 2023. According to Frost & Sullivan, China’s coffee market 56.9bn yuan in 2018 to 180.6bn yuan in 2023, coffee cups consumed in China is expected to reach 15.5bn by 2023. Further indication that consumption is showing signs of improvement.

US GDP Q/Q vs EU GDP Q/Q

The US recovered from a deeper recession in 2009 quicker than Europe.

In our opinion, this will see the US and China coffee consumption return to growth before Europe. The U.S. economy can turn around faster than Europe, exemplified by the GFC recession. While the economies are not entirely comparable, during this period, both economies suffered from 4 months of negative economic growth; however, the U.S. decline was a lot sharper with a contraction of -8.4% Q/Q in Q4 2008 vs -3.10% Q/Q Q1 2009 in Europe. The recession was more profound in the U.S., but by Q3 2009, growth was more substantial at 1.5% Q/Q vs 0.4% Q/Q in Europe; this pattern of higher U.S. growth continued in the following years. From an employment perspective, it increased to 10% in 2009 in the U.S., with Europe rising to 12% but not until 2012. The recovery stage for the U.S. was shorter than the E.U.; it took the U.S. 16 quarters to regain 30% of those unemployed jobs vs 20 months or the E.U.; this suggests we could see the U.S. emerge from the COVID-19 recession sooner than the bloc.

Western economies pandemic packages have been extended into 2021. Whilst this creates a false economy to some extent, coffee consumption will be supported as we have previously stated. Going into 2020, we saw demand in major regions was on the front foot, with the US & Canada and Europe at 34m bags and 52m bags respectively. In Europe, Germany and France had consumption at 11m and 6m bags. We expect demand to hit these levels once again in 2021, at home consumption was 80%, 85%,82%, in the US, Germany, and France respectively. In countries where at home consumption was below 75% for example, the UK and Italy we expect in home demand to rise as people still work from home and offices a more flexible approach. This has changed consumption trends and end-user tastes, while some consumers go for instant coffee, there is a stronger roast and ground consumption which is higher quality arabica. This accentuates the need for Central American coffee, however due to weather disasters washed arabica availability is low with limited in washed coffee in stocks.

Consumption trends have changed this year, some customers will revert to previous habits when they return to the office, while others who will be working from home more often may see their demand shift slightly towards pods or roast and ground. One trend that will only strengthen is the consumers demand for more sustainable practices, before COVID-19 we saw discounts for customers bringing a reusable cup to the coffee shop. While this reduces plastic pollution, and landfill use, it is not enough to help turn back the clock on climate change. A shift to bio-plastics or bio-degradable materials will help reduce plastic pollution, however when you conduct a life-cycle assessment of bio-plastics vs fossil plastics, there is not much difference in damage to the environment. Due to agricultural practices, in some cases bio-plastics are worse than fossil-based plastics, indeed acidification, eutrophication, and climate change impacts are greater for some bio-plastics. The extraction of raw materials, for example, sugarcane or corn, fertilizer production and usage are significant contributors to greenhouse gases. According to Chen, Pelton, and Smith 2016 indicate that of the eight environmental impact categories were analysed. The summary of unit process impact implies from this paper indicates that biomass feedstock extraction and pre-processing are likely more emissions-intensive than the refinery processes for fossil PET due to extra energy required or agriculture and production or application of chemicals. This, in turn, impacts the biodiversity and eco-system at origin and degrades land impacting future yields.

The introduction of coffee pods has increased the efficiency of demand but has increased packaging. In recent months there we have seen the introduction of re-usable and bio-degradable pods. This is because a lot of these pods are unrecyclable, in some cities in the U.S. they are banned, even when rinsed and the plastic is stripped out some pods are not recyclable. As a result, Nestle and JDE Peet are launching a recycling scheme in the UK in partnership with not for profit Podback, the scheme will cover Nespresso, Nescafe Dolce Gusto, and Tassimo, the scheme will see be expanded to cover all aluminium and plastic pods in the UK. Consumers are showing a strong inclination that they want to recycle these pods. YouGov research indicates that 35% of consumers are not aware these pods can be recycled, with 90% suggesting they’d like to be able to. Customers can take used pods to their local Yodel drop off, or in some locations, councils will offer collection.

COVID-19 Demand Trends

Scenario 1

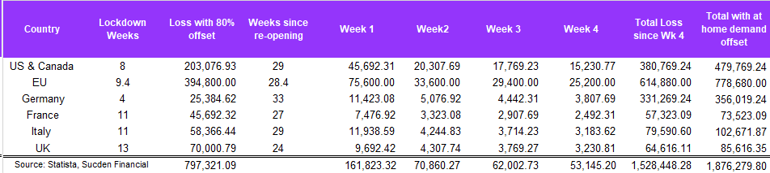

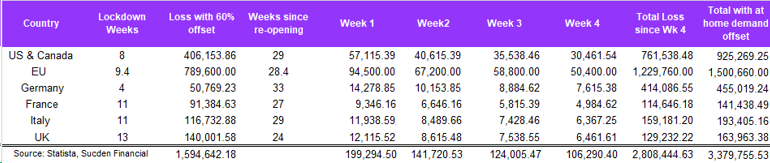

We have revisited our COVID-19 demand model, and have on analyzing new data, there is a strong indication that the drop of in demand is less severe than we first thought. We continue to run two scenarios, however with a higher in-home demand contribution, reducing the decline for this year as a whole. We now run two models. One with an 80% offset in demand, during lockdown, and another with 60%, in scenario 1 we see a drop off in demand during the first lockdown of 797,21 bags in major producing regions. In scenario 2 we see a drop off by 1.594m bags. Thereafter under the different scenarios have a different degree of demand offset from coffee shop traffic and at home consumption. Scenario 1 we see a total demand loss of 2.67m bags this year in major consuming countries, this includes the 797,321 bags during the first lockdown and the total demand since those economies have re-opened at reduced capacity, which amounts to 1.87m bags. Scenario 2 shows indicates a loss of 1.594m bags during the first lockdown and 3.379m bags since the economies have reopened, bringing the total loss for this scenario to 4.974m bags.

Scenario 2

We highlight that demand in Q1 was strong up until COVID-19 hit, and as mentioned above, Chinese consumption recovered quickly and could grow this year. As we move into 2021, we expect to see Brazil consumption start to recover, but also unemployment levels will rise, the inelasticity of demand for coffee suggests we will not see a significant drop off in demand as a result of the rise in unemployment. However, the longer individuals are out of work will clearly have an impact on demand. In the UK, Statista and the Trussell Trust suggests that 1.90m people have been receiving 3 days’ worth of emergency food, the trend is only on the increase. Indeed, in the US, according to Feeding America, between March and October food banks distributed 4.2bn meals and between March and June 4 in 10 people were attending a food bank for the first time, Feeding America estimates that 1 in 6 Americans could face hunger as a result of the pandemic. This highlights the need for a new round of stimulus from the US government.

Supply

Brazil

Brazil Monthly precipitation

Weather in Brazil remains patchy, with soil moisture low due to consistently below average rainfall.

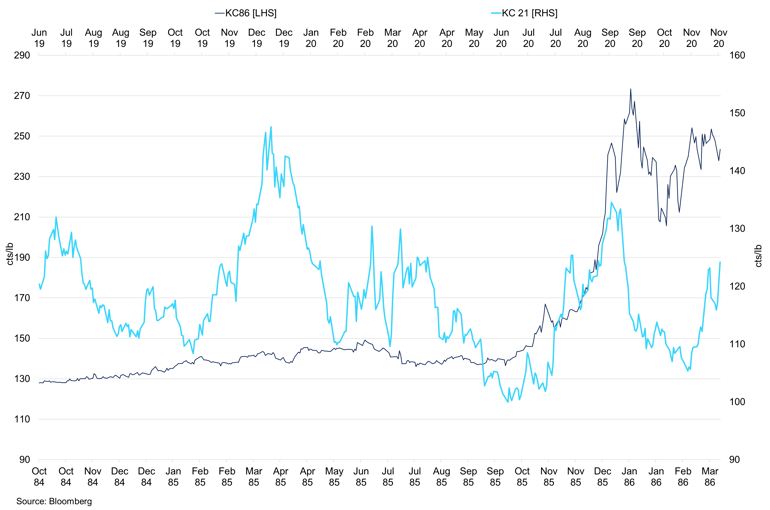

Since our previous report, dry weather in Brazil has caused significant damage to the 2021/22 crop. Severe dryness in Brazil and erratic rains in key regions in some key coffee regions, for example Coromandel and Monte Carmelo. At this period of the crop, rains have not been beneficial, indeed, if this rain pattern continues into February, we expect there to be more damage to crop. It seems that in recent weeks, investors have become more aware of the weather issues in Brazil but are still underestimating the damage. Some farmers are starting to prune trees already. The damage has been to the Arabica crop and we expect the 21/22 number to be 35m bags with the Conilon crop at 20m bags. This would bring the total crop to 55m bags, once we factor in Brazil consumption at 21m bags, the outside world demands around 40m bags, showing a 5m bag deficit in Brazil alone. Lack of rains into January would cause the crop to fall further with our Arabica estimate falling to 34m bags, bringing our total estimate for Brazil in 21/22 to 54m bags, a deficit of 6m bags in Brazil. This will wipe out the 20/21 surplus that we have seen. The picture we see today is very similar to what we saw in 85/86, but the similarities stop because of the size of the production area and crop today. It is worth noting that this year the March contract is coming from a lower base, but there are more traders, more funds with large AUM, and the prospect of a weaker dollar. This will provide support for coffee on the upside.

Arabica March 1986 vs Arabica March 2021

We have drawn similarities between 1986 and the current crop in terms of weather, below we see the price action.

A lot has been made of the semi-washed arabica being graded, while the quality of this product may be good, and is tenderable against the KC contract, the pass rate has been low. The majority of Brazilian is unwashed natural coffee which is not tenderable against the KC contract. The number of arabica bags pending grading is rising and stands at 67,540 bags as of November 16th. The semi-washed grading has caused the spread to weaken significantly but we remain of the view that this coffee fails to act as a viable substitute to the washed arabica coffee. 2020/21 season needs to carry to 2022/23 season. The pass rate has ranged between 38% and 73%, with 534 lots (151,342 bags) as of November 19th, if the desired impact was to widen the spread, then this would have worked. In August, the March21/March22 spread was -1.95cts/lb, and as of November 23rd, the spread trades at 6.85cts/lb.

Brazil Coffee Local Price vs 2nd Month Arabica

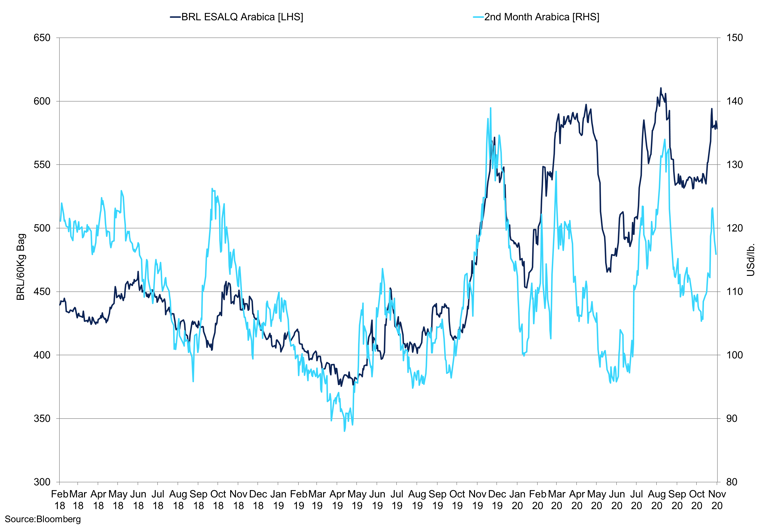

Local prices remain strong compared to exchange prices, and have pushed back to R$600/lb.

Brazilian farmers have taken full advantage of rallies in Q4 2019, and Q3 2020 to market their 2020/21 crop and in part of their 2021/22, and in some degree 2022/23 crop. To our estimation, the 2020/21 crop is 70% sold so far, and as prices have rallied in the last few weeks, we expect more producer selling, especially as the Real stands around 5.50 to the $ at the time of writing. However, the most recent rally to 135cents/lb, using R$600/kg bag as a reference and 5.300 to the $, saw the difference between KC and Brazil at a 44cent discount in respect of Brazil. In recent weeks the discount has tightened to -17/-20, and as of November 16th, 2020 the discount was at -30 with the exchange rate at 5.44. We believe the industry has bought large amounts of cheap Brazils, in dollar terms, and with the crop 70% sold, they are under no pressure to sell on the cheap. Factoring in the dry weather, high temperatures and erratic rainfall, the farmer may wait until late December or even early January 2021 once they’ve seen how the flowering and cherry development stage performs.

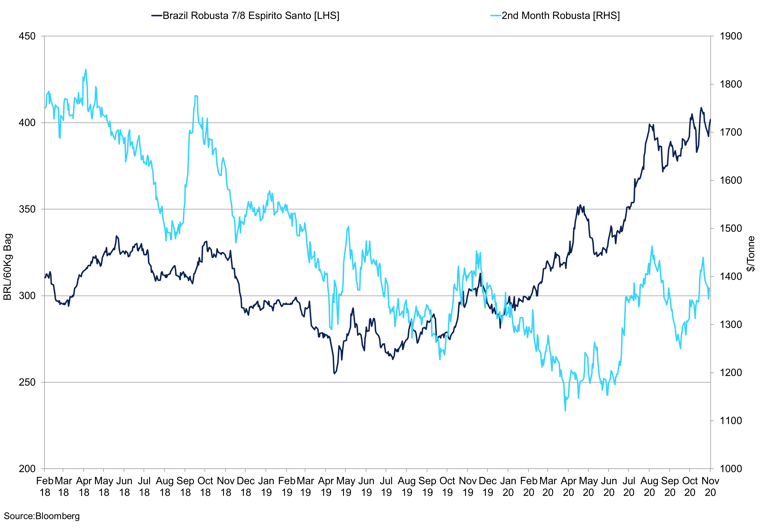

Brazil Robusta 7/8 Espirito Santo Vs 2nd Month Robusta

The spread between local and exchange prices is widening as local prices continue to rise.

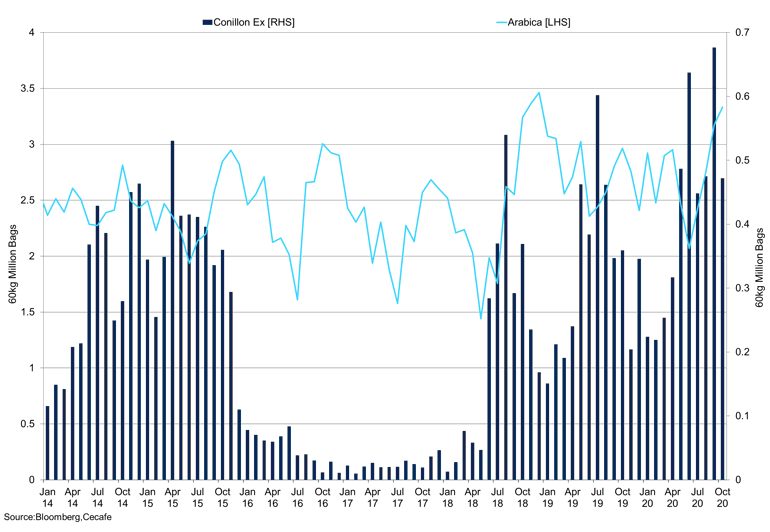

Brazil Conilon vs Brazilian Arabica Exports

Conilon exports have surged in recent months, and we expect them to remain elevated in 2021.

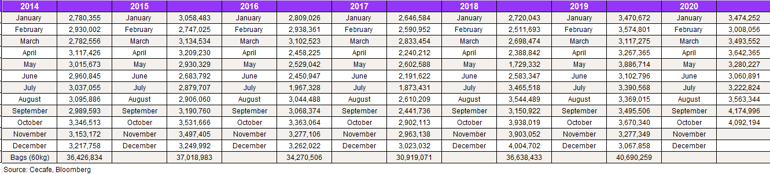

Our 2020/21 crop number for Brazil is 66m bags which is below some participants, this is split as 48m bags for Arabica and 18m bags for Conilon. Internal consumption has dropped to 21m bags from 21.5m bags, external demand stands at 40m bags and this would mean a carry-over of 4m bags. However, with the reduced crop for 2021/22 there is tightness expected in the coming months which may see some roasters start to get nervous. Exports for the calendar year have reach 35.12m bags as of October 2020., according to Cecafe. September and October shipments have been particularly large, both over 4m bags. October shipments were 4.092m bags. The breakdown saw an increase in arabica exports in October from 3.176m bags in September to 3.331m bags in October, Conilon shipments were nearly 200,000 bags lower at 471,793 60kg bags. Exports from July through to October 2020 vs 2019 have seen an increase in all departments except Soluble coffee which is down 78,416 bags y/y at 1,293,127 bags for 2020. In these months, Arabica shipments have increased 908,333 bags, from 10,774,474 bags to 11,682,233 bags. Conilon exports have also improved this year, up 301,628 bags from 1,769,475 bags and 2,071,103 bags.

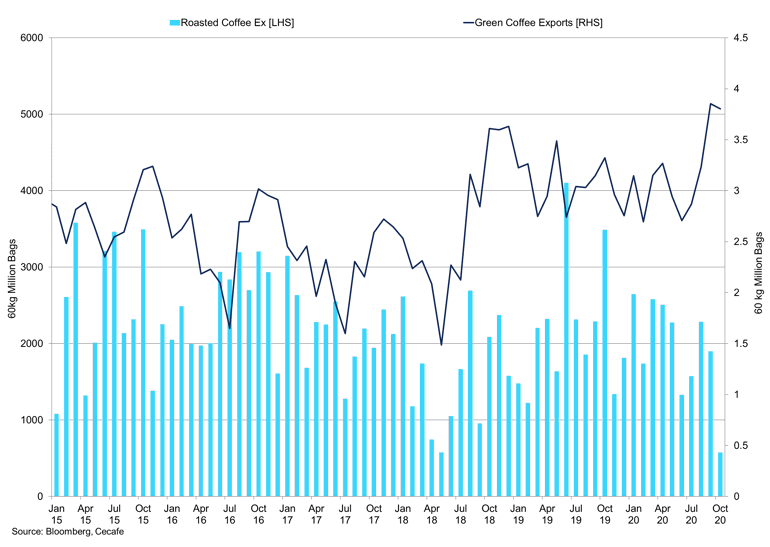

Brazil Roasted Coffee vs Green Coffee Exports

The rise in Conilon and arabica exports have prompted green coffee exports to rise.

Central America

The recent weather disasters in Central America has provided significant tailwinds to the market. Hurricane Eta, and Iota have caused significant destruction, with winds in the latter reaching 160mph and was the first category 5 hurricane of the season. Both hurricanes have caused devastating flooding, in Honduras and Nicaragua, as a result we expect there to be significant damage to both countries coffee crop, as well as other crops such as rice, sugarcane, and corn. Leaders of Central American countries have asked for aid, and requests have been granted but this will not help with crop damage. Surrounding countries such as Guatemala, Belize and El Salvador have also been impacted but not to the same degree as Honduras and Nicaragua. The recovery for these two countries will take a while, and we hope there are not more weather disasters for the rest of the season. The airport will not be up and running for a while. There could be a longer lasting impact on the coffee market because 90% of farmers in Honduras are small scale farmers, and if their crops are destroyed, they will not have any income. This loss of income for these farmers will be devastating, especially after market prices over the last few years, but could also significantly reduce the crop size in the coming years.

As we look at the fundamental backdrop for Central America and washed arabica, we have seen tightness in this coffee type for a while. For the 2019/20-season between October and September, exports for Central America (Mexico, Honduras, Nicaragua, Guatemala, Panama, Dominican Republic, and Costa Rica) were down 10.8% on the 2018/19 season with the 2019/20 season total shipments at 16.54m bags vs 18.34m bags for 2018/19. Following low prices, the lockdown earlier on in the year, and the switch to competitively priced Brazil Arabicas due to the devalued Brazil currency, the last thing farmers needed was a weather disaster. Damage to the crop is unknown at this time because farmers cannot get into the fields to assess the coffee. The final impact may not be known until January. As COVID-19 cases remain high, this has prevented pickers from crossing the borders, we expect larger economies to receive the vaccine first which may mean LEDCs continue to struggle. Our current crop number for Honduras is 5.5m bags for the 20/21 season and we expect this to decline but as mentioned, it is too early to estimate by how much.

Farmer selling has been moderate, and we do not believe coffee that has been damaged was previously sold, we expect around 1m bags worth of coffee to be sold in Honduras. In our opinion, farmers wanted to increase their hedges when prices rallied to 135cts/lb in August, but they struggled to get access to finance. We expect differentials to remain firm, with Honduran differentials are +24, and Guatemala diffs are +45/50, we don’t not see much downside to these levels in the near term. Even with these diffs, you can’t buy the coffee at the moment. We have seen a significant decline in washed Arabica stocks in 2020, with Honduran coffee falling from 1.550m bags in January this year to 853,458 bags as of November 2020. Following the recent weather disasters, we expect stocks of this coffee to fall further, however the competitively prices semi washed that passed do have commercial value, which would tighten up the board. We saw the Central American crop estimates falling into this season, but after the weather damage the losses are likely to be more severe, we expect demand to improve next year, the decline in stocks could be pick up pace in 2021. Brazil has been cupping coffee at R$600-620/60kg (March 124cts/lb and exchange rate at 5.31 to the $), in local currency this remains good, but it remains 33cts/lb under KC futures which is cheap compared to Central America. In our view, this coffee is worth R$700-800 per 60kg bag or 19/20 under.

Inventories

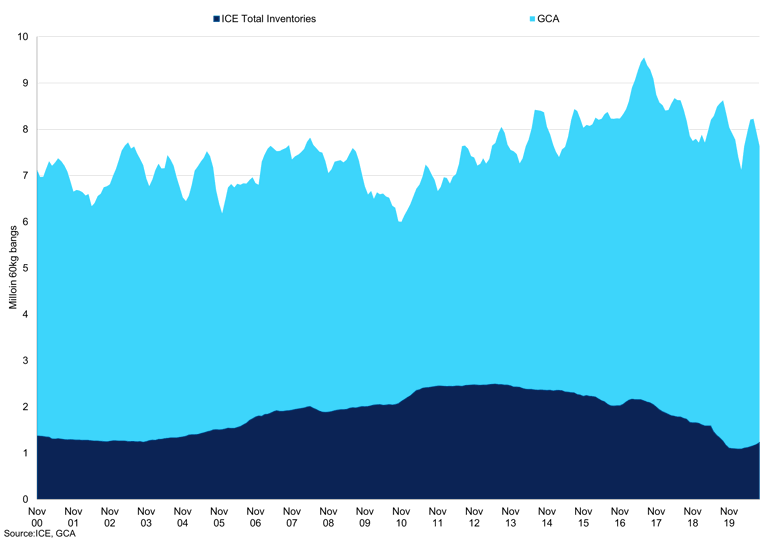

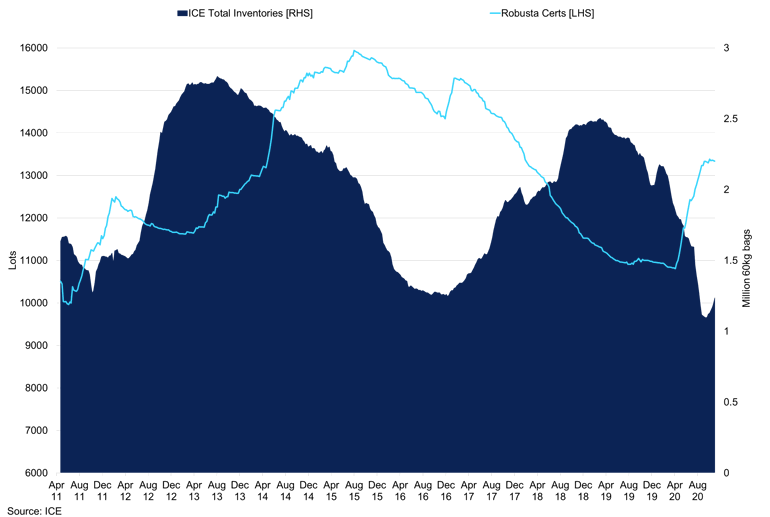

ICE Total Inventories vs Green Coffee Association

GCA stocks have fallen this year, and ICE inventories are also down on the year despite weaker demand conditions.

Certified stocks for the Arabica contract have fallen this year, from 2.032m bags in January to 1.247m bags as of November 24th. We previously expected inventories to fall below 1m bags this year, however, since the start of October we have seen inflows into warehouses rise, with certified stocks rising from 1.099m to 1.246m bags from October 1st to November 24th. We attribute this to the influx of semi washed Arabica from Brazil. Since the beginning of October, Brazilian coffee in exchange warehouses has increase 1,691% to 171,592 bags as of November 24th, this is as a result of the semi washed arabica pass rate increasing. The devalued Brazilian currency has helped the competitiveness of this coffee but as we see risk appetite increasing in financial markets, EM currencies have caught a bid, and this could reduce the attraction of this coffee. However, with dollar weakness and Brazilian real strength, this could give rise to the New York contract. Exchange data shows that coffee pending grading has fallen slightly in recent days to 44,145 bags as of November 2020, and bags passed was 18,905 on the same day. The key to the fall in inventory was the withdrawal of Honduran coffee. The decline has subsided in recent months with stocks holding around 853,000 tonnes. The pass rate for semi washed arabica fluctuates and while we expect more of this coffee to come to the board, as weather issues in Central America and Brazil threaten the crops, and demand returns to normal and grows next year, we expect inventories to continue to draw which will provide tailwinds to the flat price and also see the structure tighten. Total damage is still early to say but Brazil is dry, while Central America has the opposite problem. This year the drop off in Central American coffee was offset by the huge Brazil crop and inventories still fell even when demand was hit in March and April by COVID-19, in the 20/21 season we do not expect this to happen. GCA stocks have fallen by 9.8% this year to 6.137m bags, flows have been volatile but since rising to 7m bags, stocks have declined once again.

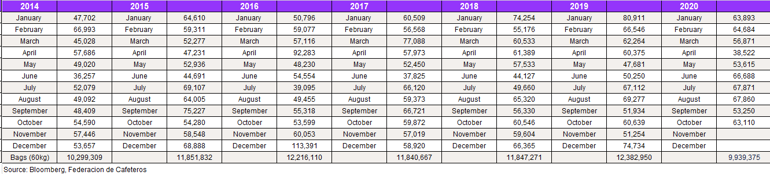

Robusta inventories have been rising since the beginning of October, and have reached 13,334 lots, up form this year’s low at 10,808 lots as of October 23rd. Antwerp has 7,647 lots as of November 30th, we expect the rise in inventories to be due to the strong Conilon shipments. Non-tenderable coffee in stocks has been falling gradually to 153 lots, from 228 as of February 2020. Vietnam coffee exports have been in decline since February 2020 when they reached 2.8m bags. Vietnam exports are usually front loaded to the beginning of the year due to the crop cycle, however, the bad weather in Vietnam which has delayed the harvest, and farmers reluctance to sell could see exports disappoint in the lead up to December. We do expect December exports to show strong improvement, with exports pushing back to 2.5m bags. This may not have huge impacts on stocks, as most of this coffee will go straight to industry.

ICE Coffee Inventories vs Robusta Certified Stocks

Robusta certified stocks increased in recent weeks, and with a large Conilon crop, we do not expect Robusta tightness.

Commitment of Traders

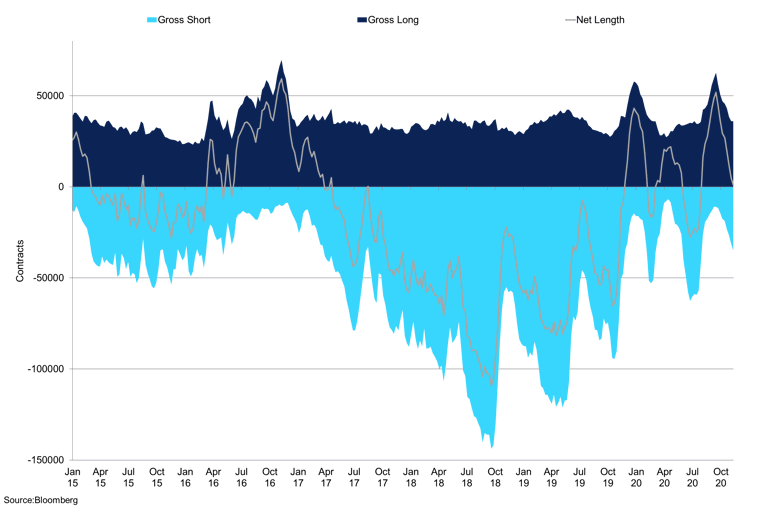

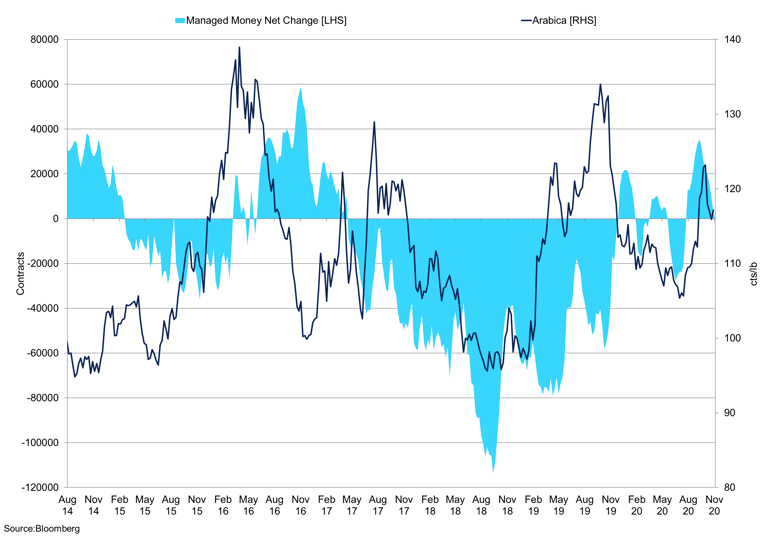

For Arabica, the supplemental non-commercial COT data shows that there was a fall in the net position by 31,821 contracts to the lows of 15,844 contracts so far this quarter. We saw an increase in the short position, up by 21,206, bringing the gross short to 37,306 contracts on November 11th, the highs last seen in August. The drop-in prices saw some new shorts and longs closing out their positions in the market. At the same time, we saw prices falling to 104.73cts/lb. As of November 20th, the net stands at 24,245, and we saw a rally in the KC contract. Spread contracts fell to 62,808, a decrease of 40% since October 1st, and we expect this to be as a result of the spread widening. The Dec-March spread widened into 3.35cts/lb, the contract's low, but has now tightened back up again to 2.70cts/lb, as of November 20th. The normalised supplemental COT data for non-commercial traders for arabica shows that the current position is above the upper quartile range, this outlines the potential for an upside swing. In our view, as things stand there is enough coffee now, tightness will increase in H2 2021, supporting prices and the fund position suggests ammunition on the upside, but also the downside, if crop damage is less than expected. The non-commercial long position is neutral, and holding around the median, even with the recent rally there is further upside potential.

Arabica Managed Money Commitment of traders

Longs have substantially reduced their positions, driving net length closer to net short.

From the commercial perspective, while we did see some buying at higher prices, the net position increased significantly to -23,805 as of November 10th, up from -65,000 contracts at the beginning of September. We saw some reduction in the gross short as prices rallied, falling to 197,390 contracts on November 20th from 204,000 as of November 3rd, as commercials sold into the rally. At the same time, we also saw a significant increase in the number of longs, reaching 179,000 contracts as of November 11th, an increase of over 11,390 contracts from the beginning of November.

Since the market has retreated from the highs of 124cts/lb on November 19th, some of the longs have fallen, while the shorts continued to fall. Ultimately, the non-commercials have moved the market in recent months. The disaggregated commitment of traders, on November 20th, Producer/Merchant gross long and short, were 98,989 and 151,260 respectively; and the managed money stood at 34,402 and 26,985, respectively. Gross shorts combined for disaggregated COT was 207,915, which equates to 58.908m bags.

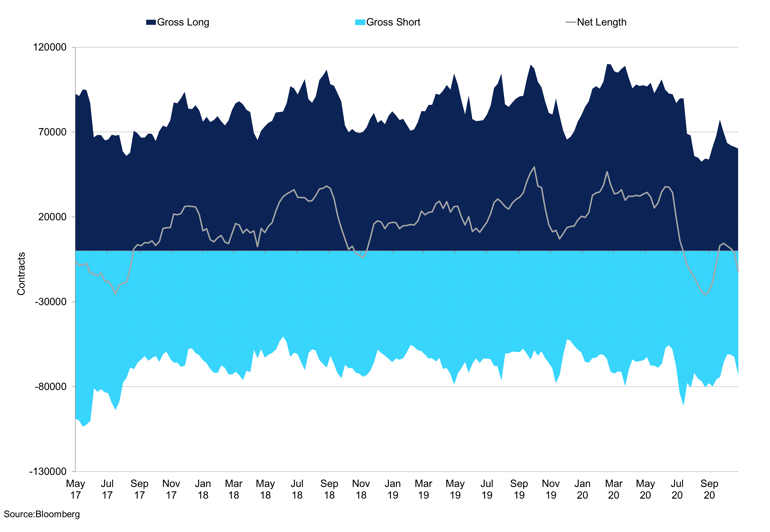

Robusta Producer/Merchant Commitment of Traders

Net length has once again returned to net short in November.

For Robusta, the net producer/merchant position was -15,233 as of November 17th; this was a net change of 3,192 contracts since October 1st. During the period, the net positions picked up by 20,739 contracts to 2,314 contracts on October 20th, before falling to net short a week later. The number of gross shorts fell between October 1st and October 20th, down by 15,125 contracts to 57,773; since then, the number of contracts picked up by 8,541 to 66,315. This shows that producers have started to sell into the rally, during the same period, we have seen longs fall by 14.56% to 51,082. The managed money commitment of traders for futures and options has seen a significant decrease in the long positions from 17,900 to 11,000 contracts. Shorts have seesawed in the same period, picking from 4,585 to 17,854 on October 20th, back to 3,532 on November 17th. As prices rallied at the begging of November, the short closed out some of their positions.

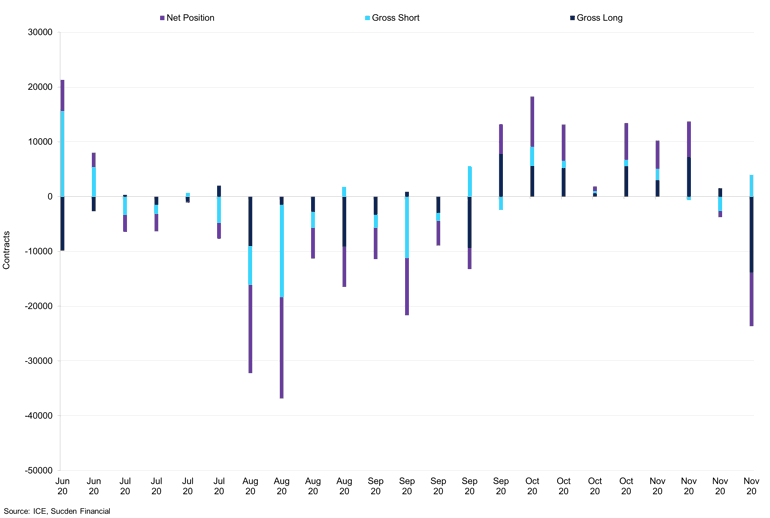

Arabica Commercial COT Week-on-week

Gross longs have reduced their position in the last couple of weeks.

Trade Idea

- Vols are above 40% which shows an increase in Vol appetite, this is expensive but outlies the market skew

- For those wanting to use the options market, we favour buying a March150 call at $2.15 and selling a March 110 put which has a premium of $2.97 at the time of writing

- The Arbitrage has softened as price retreat from 125cts/lb. The market is moving towards 50 which provides an entrance opportunity in our opinion, given the damage to the Arabica crop and strong Conilon and Indonesian crops

- We believe Robusta will struggle to hold above $1600 due to the Conilon crop and we expect this coffee to flow through April 2021

Appendix

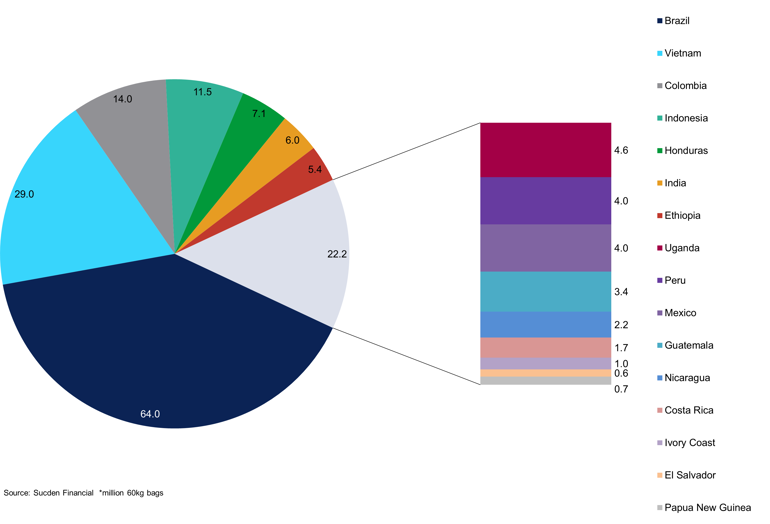

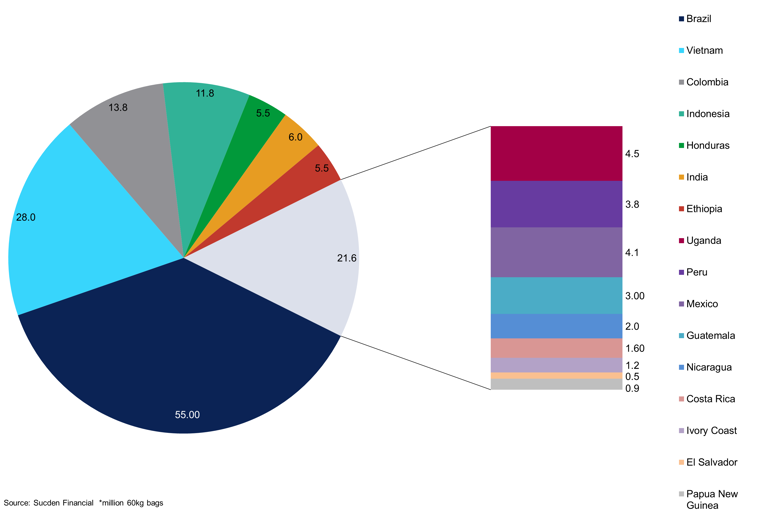

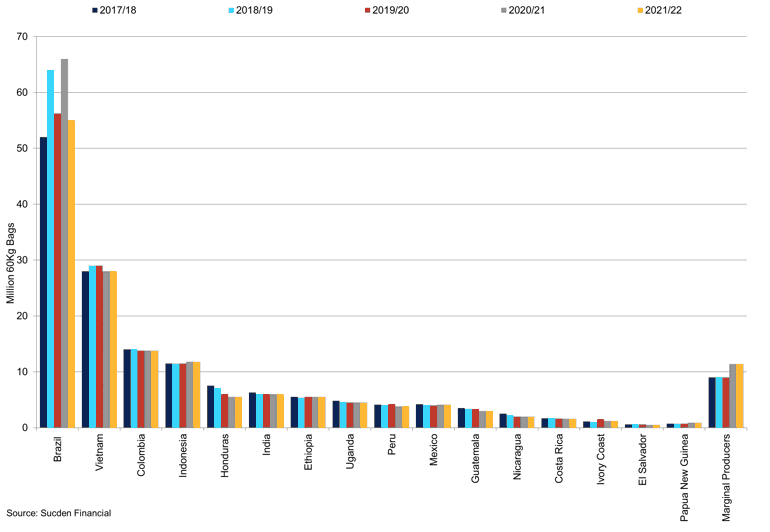

Sucden Production Chart 21/22

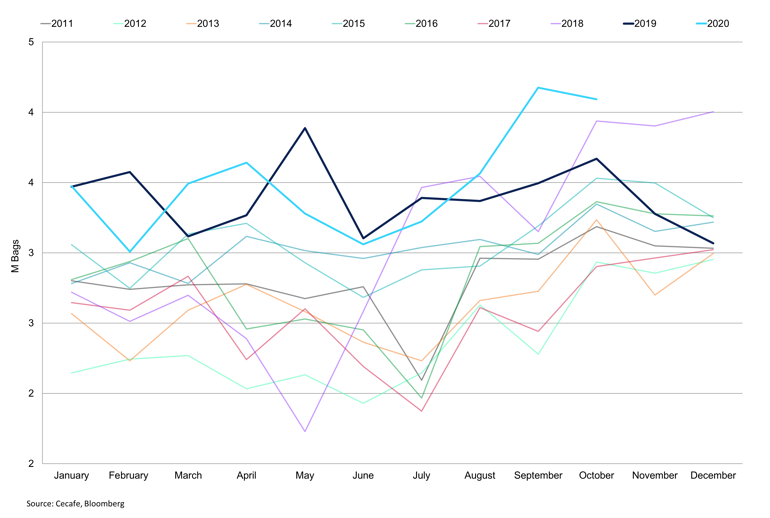

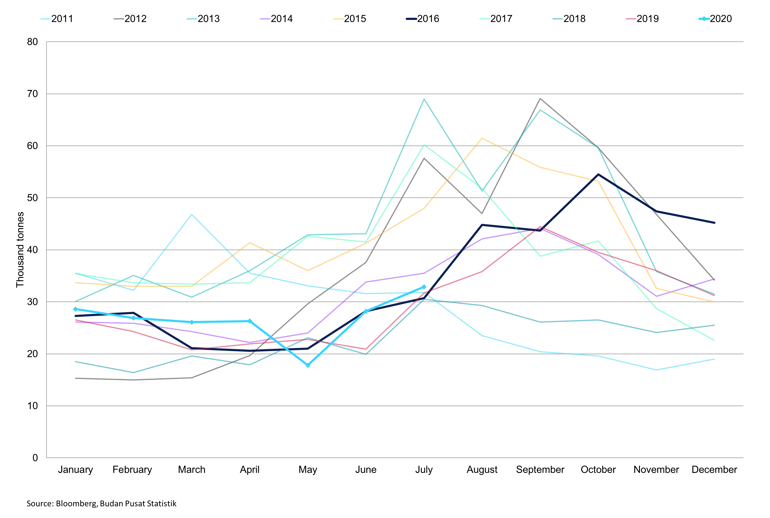

Brazil Coffee Exports

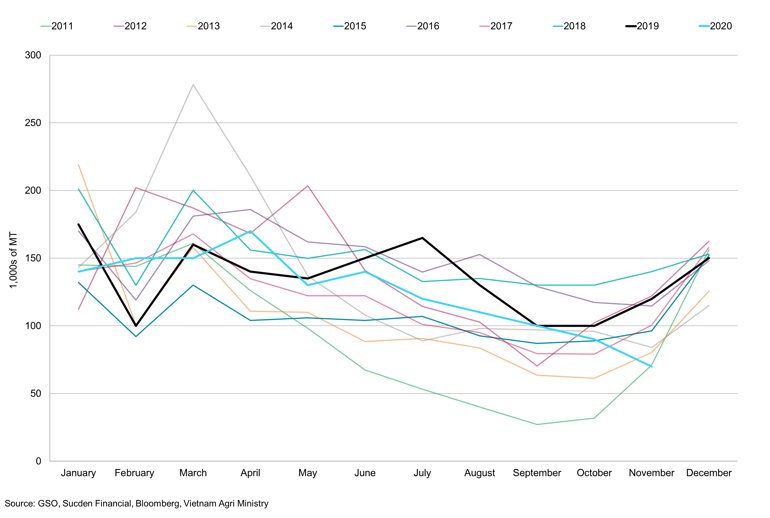

Vietnam Coffee Exports

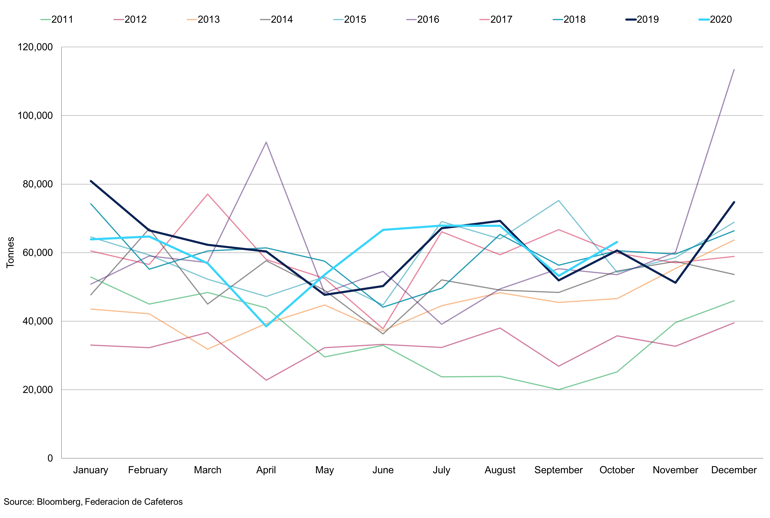

Colombia Exports

Indonesia Coffee Exports

Brazil Coffee Exports

Vietnam Coffee Exports

Indonesia Coffee Exports

Colombia Coffee Exports

Arabica 2nd month price vs Net Change in Managed Money

Vietnam Exports vs Dak Lak Local Price

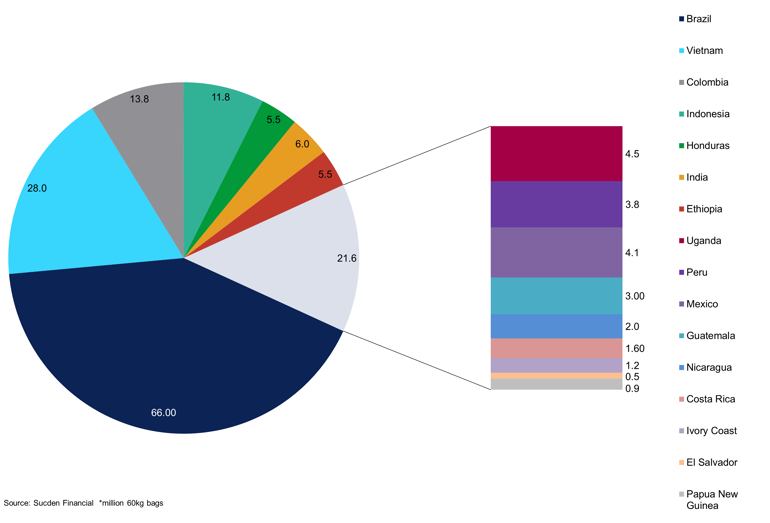

Global Coffee Production 21/22 Bar Chart

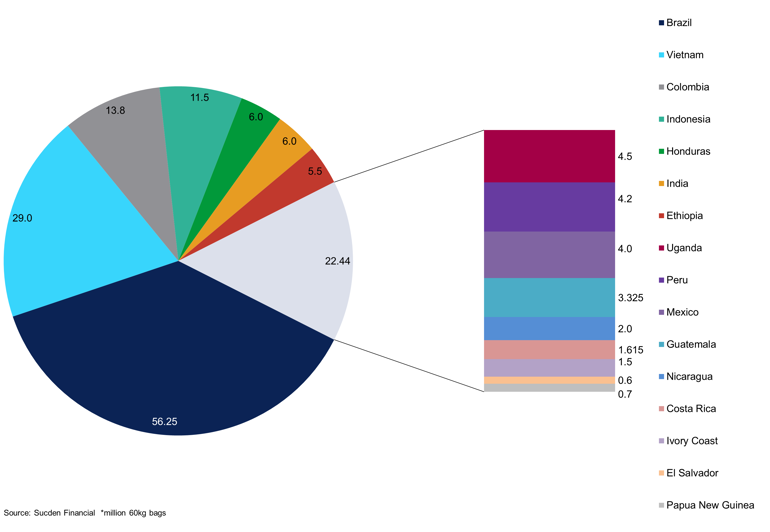

Global Coffee Production 2020/21

Global Coffee Production 2019/20

Global Coffee Production 2018/19