EUR / USD

EUR/USD stabilised yesterday as the dollar's upside stalled, with a support at 1.14 being defended. The economic divergence between the US and Eurozone becomes increasingly pronounced, with US GDP growth at 3.0% contrasting sharply against the Eurozone's mere 0.1% expansion in Q2. The Federal Reserve's hawkish monetary stance and sticky US core PCE at 2.8% stand in stark contrast to the ECB's more dovish position, particularly as German inflation cools to 1.8% year-over-year.

Technical indicators suggest the pair is experiencing considerable weakness, with RSI readings at 29 indicating oversold conditions, while price action remains constrained below 1.17. The implementation of new US tariffs at 15% is creating additional headwinds for European exporters, further pressuring the euro, while market sentiment has turned notably bearish with significant unwinding of long positions.

The currency pair's immediate outlook appears challenging, with crucial support at 1.14 being tested, and any failure to hold this level could trigger a deeper decline toward 1.13.

USD / JPY

USD/JPY has demonstrated significant strength, breaking above the crucial 150 level amid a combination of fundamental and technical factors. The Bank of Japan's maintained interest rate at 0.5% and upward revision of inflation forecasts to 2.7% have failed to provide substantial support for the yen, while higher US PCE data and the Fed's hawkish stance continue to bolster the dollar's position.

Technical analysis reveals robust momentum in the pair, with successful breaks above key levels including the 200-day moving average at 149.0. The daily RSI's elevation above 70 suggests overbought conditions, potentially setting the stage for a technical correction toward the psychological 150.0 mark as support.

The yen faces additional pressure from domestic concerns about fiscal deterioration following recent ruling party election losses, while the reduction in US-Japan trade tensions through their recent agreement has not been sufficient to stem the currency's weakness. Market participants are now pricing in increased probability of another BOJ rate hike later this year, though Governor Ueda's cautious approach and inflation remaining below the 2% target suggest any policy tightening may be gradual.

GBP / USD

GBP/USD experienced moderate downward pressure, primarily driven by diverging economic fundamentals between the UZ and the United Kingdom. Recent US economic data has been particularly robust, with Q2 GDP growth of 3.0% exceeding expectations, while the UK faces more modest growth prospects of 1.2% for 2025 according to IMF projections.

The technical outlook appears bearish, with the currency pair trading below all major moving averages, but an oversold RSI of 28 suggests potential for a technical rebound in the near term. The interest rate differential between the two economies is likely to widen, as markets anticipate UK rates dropping from 4.25% to 3.75% while expectations for Fed rate cuts have diminished substantially.

The combination of UK political uncertainty, weak economic momentum, and declining real yields continues to weigh heavily on sterling, while the dollar benefits from strong employment data and PCE inflation readings that reinforce US economic outperformance. The immediate technical support lies at 1.31, with a potential further decline to the psychological level of 1.30.

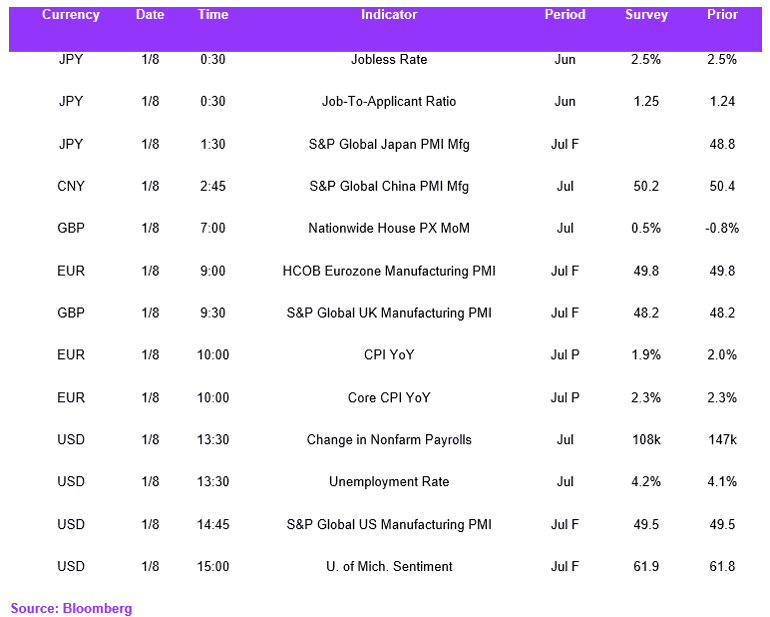

Economic Calendar