EUR / USD

The euro continues to face mixed pressures following the Federal Reserve's rate cut of 25bps. While the ECB maintains a cautious stance with limited easing plans, the Fed is expected to bring two more rate cuts this year, creating a shifting interest rate differential dynamic. Recent comments from ECB officials, including Governing Council member Stournaras, indicate the central bank will hold off on further rate cuts unless inflation or growth conditions dramatically change.

The softening of the labour market in the US adds another layer of complexity, as it was a key factor behind the Fed's decision to begin easing. Geopolitical tensions and trade uncertainties continue to impact currency movements, with ongoing US-China trade discussions being closely monitored.

The euro's path forward will largely depend on relative economic performance between the regions, with particular focus on inflation trends and growth momentum. Market participants are watching for signs of economic divergence that could drive the next sustained directional move in the currency pair. Currently, the currency pair is likely to find support at the 50-day moving average, which stands at 1.670. Market participants will be closely monitoring the upcoming US core PCE figures later this week, as these will help shape expectations regarding the Federal Reserve's interest rate cuts for the remainder of the year. While two additional cuts are anticipated in the last few Fed meetings, persistent inflation data could reduce the existing interest rate differential with the ECB, potentially causing the pair to decline slightly.

USD / JPY

USD/JPY faces heightened volatility as markets digest evolving monetary policy stances from both the Federal Reserve and Bank of Japan. The BOJ's recent announcement to begin offloading its ETF and JREIT holdings signals a gradual shift away from ultra-loose monetary policy. Under the new approach, the central bank will begin selling roughly ¥620 billion of ETFs annually, using a phased schedule designed to avoid destabilising markets. The sales will likely be executed in small, predictable tranches and may be coordinated with market participants to limit price distortions. While the pace of sales is modest relative to the BOJ's total portfolio, the shift marks an important symbolic step away from ultra-loose policy, potentially preparing for rate adjustments in the future. In particular, while the bank left the rates unchanged at 0.5%, a notable 7-2 vote split at their latest meeting has fuelled speculation about potential near-term rate hikes.

Japanese inflation dynamics remain crucial, with Tokyo's inflation expected to reach 2.8% on Friday, compared to downwardly revised 2.5%, potentially accelerating the timeline for policy normalisation. Rising Japanese Government Bond yields and speculation about policy adjustments are providing underlying support for the yen, while the narrowing interest rate differential between the US and Japan is becoming an increasingly important driver. Markets are pricing in 25bps worth of hikes until the end of the year, which could strengthen the case for higher yen in the coming weeks.

GBP / USD

The British pound faces growing pressures as the UK grapples with growing fiscal concerns due to higher-than-expected government borrowing. The sluggish UK economy, characterised by soft consumer spending and rising business insolvencies, is undermining investor confidence in sterling, pushing it to a crucial level of 1.3470, where a convergence of moving averages exists. The Bank of England remains cautious on rate cuts, while the Federal Reserve has begun its easing cycle with a 25 basis point cut.

The labour market dynamics in both countries are influencing the currency pair, with the US seeing a notable slowdown in hiring while the UK faces disproportionate impacts from government job cutbacks. This has reduced demand for housing in the UK and affected sterling's appeal versus US assets. Technical and sentiment pressures have emerged as GBP/USD broke below key mid-1.35 support levels, with risk aversion and UK fiscal uncertainty driving safe-haven flows into the USD.

Looking ahead, the currency pair's direction will likely be shaped by upcoming manufacturing PMI data and central bank communications, particularly Fed Chair Powell's speech and Bank of England Governor's remarks this week. The differing inflation trends between the two economies suggest that the UK's ongoing price pressures may limit the Bank of England's ability to align its rate cuts with those of the Federal Reserve. As a result, the currency pair may remain historically high, at least until the US PCE figure is released later this week. If the data indicates a reduced likelihood of rate cuts from the Fed, it could provide a fundamental downside boost to the pair, which is currently supported by key technical levels.

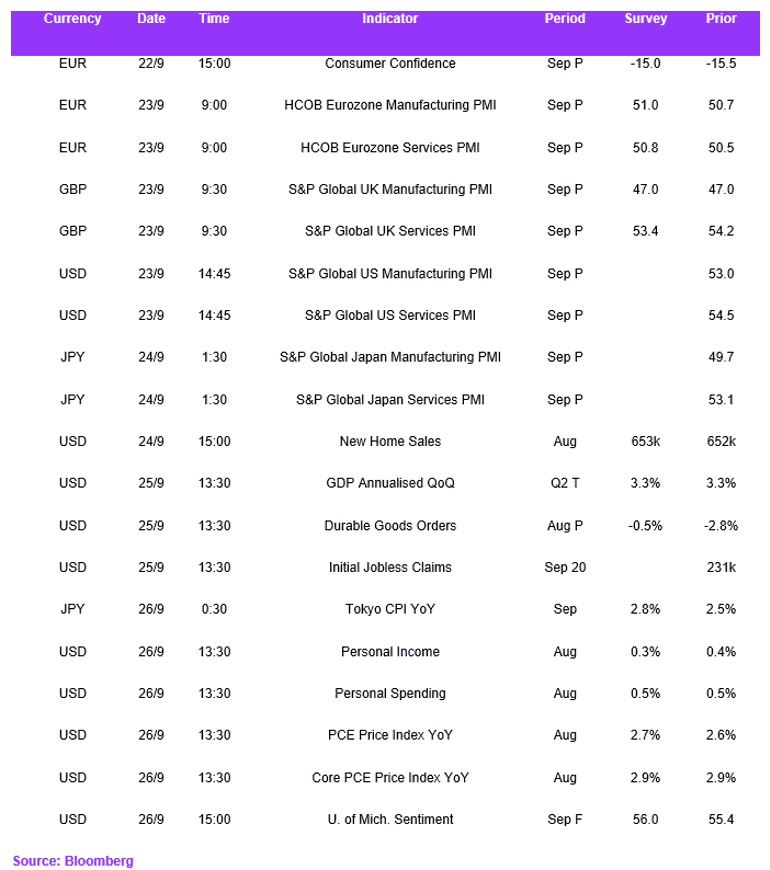

Economic Calendar