EUR / USD

EUR/USD continued to edge higher, primarily driven by the divergent monetary policies between the ECB's hawkish stance and the Fed's easing trajectory, with recent German and French inflation data exceeding expectations and reinforcing the ECB's position. Today's preliminary inflation figures for the Eurozone are expected to support these expectations across the bloc, with a forecast of 2.2% inflation compared to 2.1% in August. Technical analysis reveals a neutral short-term outlook as the price consolidates near the convergence of key moving averages around 1.1700, maintaining a healthy buffer above the 100-day SMA at 1.1601.

The dollar's weakness can be attributed to the Fed's rate cuts and growing concerns about its independence under political pressure, while the euro benefits from the ECB's confidence in the eurozone's resilience to external pressures. A potential breakthrough above 1.1770 could trigger a bullish move toward 1.1870, though structural challenges in the eurozone, including persistent inflation and uneven growth across member states, might temper a significant upside.

The currency pair's immediate trajectory appears contingent on both technical levels and fundamental factors, with support at 1.1650 serving as a crucial threshold that, if breached, could initiate a decline toward 1.155, while the broader trend will likely be influenced by the Fed's ability to navigate political pressures while maintaining its dual mandate. This is likely to result in robust levels, with the pair remaining elevated, although capped on the upside by previous highs.

USD / JPY

USD/JPY weakened due to dual catalysts: mounting concerns over a potential US government shutdown weighing on the dollar and evolving Bank of Japan policy dynamics. Recent market data indicates a decline of 0.48% from 148.64 to 147.94, with the pair encountering notable technical resistance near 148.67 before closing just above the 20-day moving average of 147.90.

The Bank of Japan's September meeting revealed internal divisions regarding monetary policy direction, with some members advocating for rate hikes while others favour maintaining accommodative measures, creating uncertainty in the market. Japanese economic indicators have shown concerning weakness, with August retail sales unexpectedly declining by 1.1% and industrial production falling more than anticipated. Still, forward swaps are pricing in 19bps worth of hikes by the end of the year, and this figure is likely to rise to 25bps given inflation remains upwardly sticky.

The currency pair's immediate trajectory appears increasingly dependent on US political developments and the evolving monetary policy divergence between the Fed and BoJ, with markets pricing in approximately 42bps of Fed easing by December while anticipating potential tightening from the BoJ. Technical analysis suggests that while a bullish scenario could emerge above 149.33, a breach of the 50-day moving average support at 147.79 could trigger a bearish move toward 146.26, particularly if global risk sentiment deteriorates.

GBP / USD

GBP/USD bounced back yesterday, recovering to 1.3442 as a weaker dollar offset concerns about UK growth figures, with Q2 GDP growth decelerating to 0.3% from 0.7% in Q1, albeit the final adjustments remained unchanged. Bank of England Deputy Governor Dave Ramsden's cautionary stance against prolonged high interest rates, coupled with signs of weakness in the UK labour market, suggests a potential shift toward a more dovish monetary policy approach.

The technical outlook remains neutral-bearish, with the pair trading in a tight range and finding support at 1.3420, while the RSI at 46 and prices below key moving averages reinforce the cautious sentiment. The contrasting monetary policy trajectories between the Fed and the BOE will likely drive currency movements, although the looming US government shutdown risk could provide temporary support for sterling.

The pair's immediate trajectory appears contingent on whether buyers can break back above 1.3500, where a cluster of short-term moving averages is positioned at the moment. A weaker dollar, rather than positive UK economic developments, is likely to be a trigger for such a breakthrough.

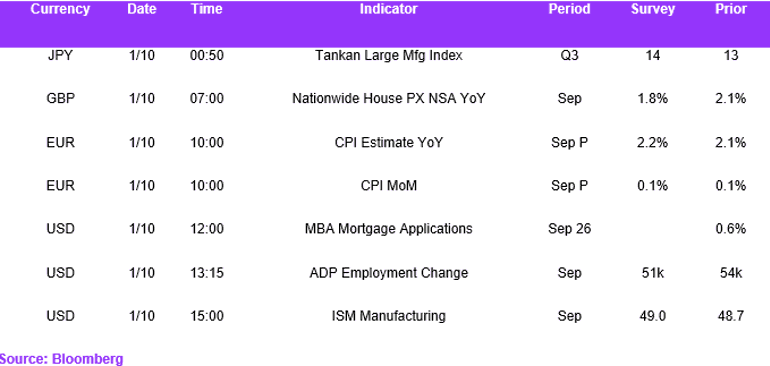

Economic Calendar