EUR / USD

EUR/USD weakened toward 1.1570, primarily driven by the widening monetary policy divergence between the Fed and ECB as well as the extended trade truce between China and the US. Recent Fed decisions maintaining higher rates, coupled with Chair Powell's hawkish stance on December cuts, have strengthened the dollar's position against the euro. Technical analysis reveals a bearish momentum with the pair trading below critical moving averages, notably the 50-day MA at 1.1680.

Meanwhile, the eurozone's economic indicators, including Q3 GDP growth of 1.3% and moderating inflation at 2.3%, while showing signs of stabilisation, remain relatively weak compared to US metrics. This data only supported the ECB's decisions to keep rates on hold, suggesting the effective pause in its rate-cutting cycle. Despite the recent repricing for fewer Fed cuts by year-end, forward swaps indicate that markets have not ruled out another cut altogether. This suggests that further remarks from Fed Chair Powell may be needed to keep market pricing consistent with the Fed's intended policy path.

Heavy trading volume around 1.1570 suggests this level could be crucial for determining future price direction, with potential support at 1.1550 and resistance at 1.1870. The combination of institutional investors reducing euro exposure and the ECB's cautious monetary stance amid mixed economic signals suggests continued vulnerability for the EUR/USD pair in the near term.

USD / JPY

USD/JPY has demonstrated remarkable strength, climbing to 153.80, primarily driven by the widening policy divergence between the Fed and the BOJ. The BOJ's decision to maintain interest rates at 0.5%, coupled with Governor Ueda's ambiguous signals regarding a potential December rate hike, has contributed significantly to the yen's weakness. The Fed's hawkish stance and Chair Powell's dampening of December easing expectations have further amplified this monetary policy disparity.

The new Takaichi administration's apparent preference for accommodative policy has increased scepticism regarding potential BOJ tightening, with forward swaps pricing no hikes until Q1 2026. Market participants are now closely monitoring upcoming wage negotiations and economic data that could influence the BOJ's December policy decision, as these factors may impact the currency pair's trajectory.

Meanwhile, the sustained yen weakness may trigger intervention concerns from Japanese authorities if USD/JPY approaches 155. The pair's technical structure suggests potential for further upside movement toward this level, although market caution surrounding potential intervention might taper the yen's bearish sentiment around this level, creating a strong resistance for the USD/JPY pair.

GBP / USD

GBP/USD continued to weaken, breaking below the 1.3200 level and reaching a concerning low of 1.3130, reflecting broader challenges in the UK economy. The technical landscape appears particularly challenging, with the currency pair trading below all major moving averages, including the critical 200-day SMAs at 1.3250, forming a substantial resistance cluster. The upcoming November budget has created additional market anxiety, as Chancellor Rachel Reeves is expected to maintain strict fiscal discipline, potentially implementing greater fiscal tightening measures that could further pressure the pound.

Despite a persistently elevated inflation level above the BOE's target, markets have begun pricing in earlier interest rate cuts from the Bank of England, with expectations of a terminal rate of 3.25% by summer 2026, contributing to sterling's nearly 4.3% decline since mid-September.

The daily RSI reading of 30 indicates severely oversold conditions, suggesting potential for a technical bounce, though fundamental headwinds remain strong. Key support has emerged at 1.313, while immediate resistance lies at 1.3250, with these levels likely to hold, keeping the pair's direction capped on the upside.

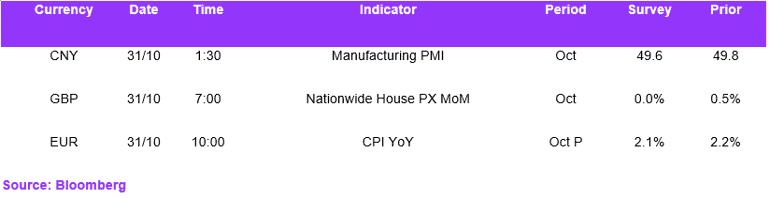

Economic Calendar