EUR / USD

The EUR/USD outlook appears cautious amid shifting monetary policy dynamics between the Federal Reserve and European Central Bank. The Fed's recent 25bps rate cut, while significant, came with hawkish commentary from Chair Powell suggesting December cuts are not guaranteed. The dollar index has found support, albeit remaining below the critical 100 mark as markets scaled back expectations for December Fed easing, with odds dropping from over 90% to around 63%. Looking ahead, key US economic releases, including ISM manufacturing and services data, will be closely watched given the government shutdown's impact on official statistics.

Meanwhile, the ECB held rates steady at 2% for a third consecutive meeting, with President Lagarde indicating policy is "in a good place" after eight quarter-point cuts through June. Recent Eurozone data shows inflation cooling to just above the ECB's 2% target, while Q3 GDP growth exceeded expectations.

The ECB appears content with current policy settings, barring significant changes to the growth and inflation outlook. However, for this policy divergence to have an impact on the currency, the Fed's cut in December must be fully priced in before a meaningful effect is seen on EUR/USD. As a result, we need to see stronger data out of the US to confirm these expectations.

USD / JPY

The Japanese yen continues to face significant pressure against the dollar following divergent central bank policies, with the Federal Reserve maintaining a hawkish stance. Recent comments from BOJ Governor Ueda, indicating a desire for more time to assess wage growth and price movements, have dampened expectations for near-term policy tightening in Japan.

The impact of US tariffs on Japanese businesses has emerged as a key concern for the BOJ, with companies reportedly cutting prices on U.S.-bound goods and slowing wage increases to protect margins. Manufacturing weakness in Japan, evidenced by a PMI reading of 48.3 in October, further supports the BOJ's cautious approach. While Tokyo inflation has shown signs of heating up, broader economic concerns appear to be overshadowing price pressures in the BOJ's policy calculations.

The upcoming week brings critical data, including Japanese PMIs, wage growth figures, and household spending, that could influence the BOJ's December policy decision. Market participants are also closely monitoring potential intervention risks from Japanese authorities as the currency pair approaches the key 155 mark. We expect that despite the overall weakness of the yen, as markets approach this level, the selling pressure may begin to lessen.

GBP / USD

The GBP/USD outlook appears to be finding support at the 1.1310 level, after a previous selloff that was triggered by diverging monetary policy expectations between the Federal Reserve and the Bank of England. The BOE is widely expected to keep rates unchanged at 4.0% at its upcoming meeting on November 6th, with recent weaker-than-expected UK inflation and jobs data increasing speculation about potential rate cuts. Market pricing now shows a 31% probability of a BOE rate cut this week, while the Fed has maintained a more hawkish stance after its recent 25bp cut.

The UK faces significant economic headwinds, with Treasury Secretary Bessent noting that parts of the economy, particularly housing, may already be in recession due to high interest rates. Adding to sterling's challenges is uncertainty around the upcoming UK budget on November 26th, where Chancellor Reeves is expected to announce tax increases and spending cuts to meet fiscal rules. Recent economic data shows the UK economy struggling with slowing growth and sticky core inflation, creating a difficult balancing act for the BOE between recession risks and price pressures.

While the uncertainty around the BOE's cutting path prevails, the yield differential continues to favour the US dollar, while the UK's fiscal challenges continue to weigh on GBP/USD sentiment. This is likely to keep the pair's trading subdued, remaining below the 200-day moving average of 1.1341.

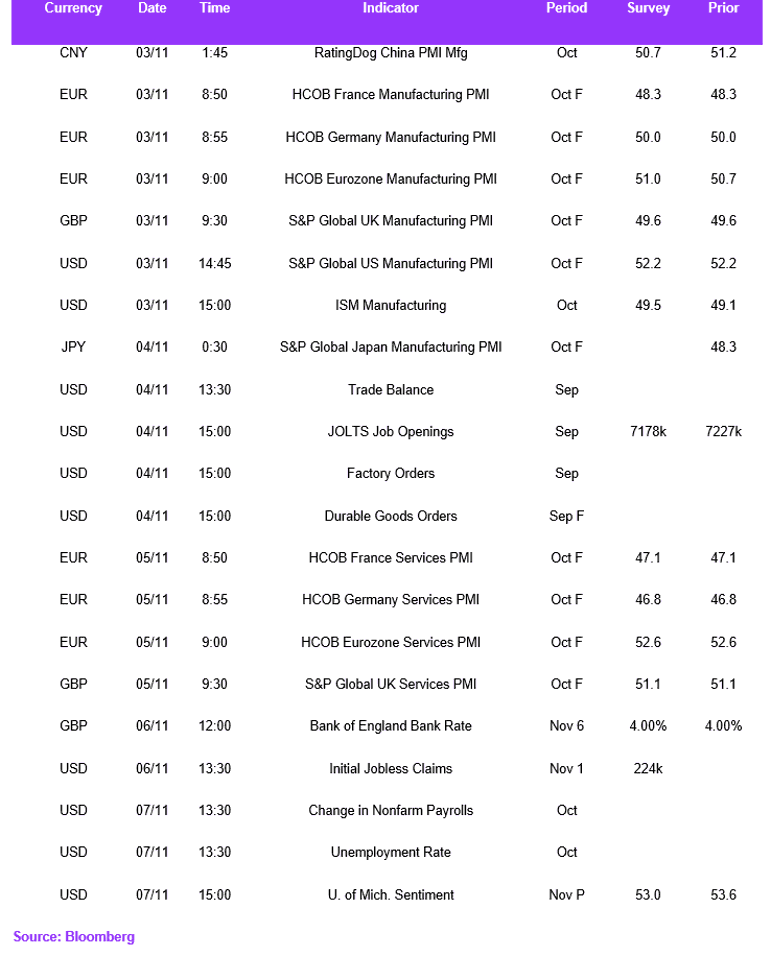

Weekly Economic Calendar