EUR / USD

EUR/USD remains range-bound as investors weigh a hawkish ECB against a Federal Reserve preparing for eventual easing. The pair continues to hold within the 1.147–1.167 consolidation band, with clustered moving averages around 1.15–1.16 signalling a potential inflection point.

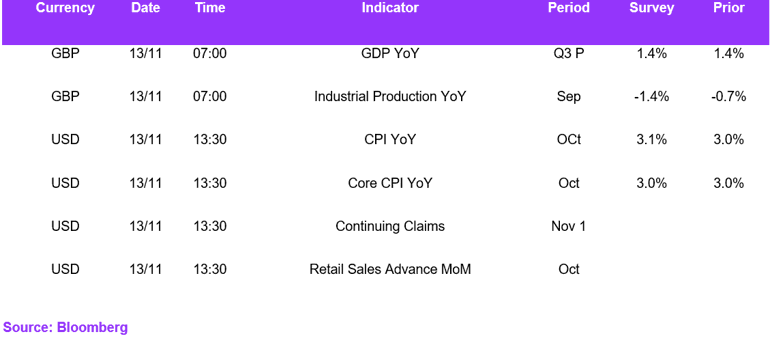

The expected CPI release will no longer provide an immediate catalyst. Despite the government shutdown ending this week, the Bureau of Labor Statistics will need time to process October inflation data, meaning the publication has been delayed until early or mid-December. Our view: with cost pressures in goods persisting and shelter still elevated, we expect a modest upside skew once the data are released. The delay, however, may keep the dollar directionally steady in the near term as markets wait for confirmation.

While yield differentials currently favour the euro, persistent eurozone industrial softness and weak external demand continue to cap upside. Technically, the neutral RSI around 50 and the tight range suggest that a break above 1.167 or below 1.147 will define the next meaningful move.

USD / JPY

USD/JPY retains strong momentum above 155.00, supported by stark Fed–BoJ policy divergence. The pair remains comfortably above its 50-day (151.05) and 200-day (147.29) moving averages, underscoring a well-defined uptrend.

The delay in US CPI removes a near-term volatility trigger. With Japan maintaining expansionary fiscal policy and the BoJ reluctant to rush into tightening, downside pressure on the yen persists. Verbal warnings from officials have produced only limited impact, with the last meaningful intervention occurring near 160.

Markets currently assign a 24% probability of a December BoJ hike and around 46% for January, though political preference for policy patience may push normalisation further out. A firm break above 155.00 would open the path towards 158.55, while a fall through 153.35 could expose a move towards the psychological 150.00 level.

GBP / USD

GBP/USD continues to face selling pressure as UK macro indicators deteriorate. The unemployment rate rising to 5% and a net job loss of 32,000 in October highlight weakening labour-market momentum, contrasting sharply with the resilience of the US economy.

With the CPI release postponed, markets lose a key macro cue this week, leaving sterling more exposed to domestic drivers. The pair trades below all major moving averages, and an RSI of 38.5 signals further downside potential. Expectations of earlier BoE rate cuts relative to the Fed continue to weigh on GBP through the rate-differential channel.

With domestic softness intensifying and broader risk sentiment fragile, GBP/USD remains vulnerable. The 1.301 support level is key; a break lower would open the way to deeper losses.

Economic Calendar