EUR / USD

The euro faces mixed signals heading into December as markets grapple with diverging monetary policy expectations between the Fed and the ECB. Recent comments from Fed officials have been notably divided, with NY Fed President Williams hinting at potential rate cuts while Boston Fed President Collins opposes easing, creating uncertainty around the December FOMC meeting.

However, the US economy continues to demonstrate resilience, with delayed figures indicating that a December cut remains unlikely, as there is a lack of recent data to inform policymakers’ decisions. Still, the probability of a rate cut has surged to over 70% probability following Williams' dovish comments, compared to just 39% odds a day earlier, potentially weighing on the dollar in the near term. Although there are signs of progress in Russia-Ukraine talks, we believe the outlook for the pair will remain primarily driven by central bank yield differentials. With a relatively quiet economic calendar this week, heightened volatility is likely as markets adjust to shifting Fed expectations.

If rates are unexpectedly held steady, as we anticipate, it could trigger a dollar rally and push EUR/USD below the 1.1500 level in the coming weeks. Overall, we see limited downside risk for the pair in the near term.

USD / JPY

The Japanese yen is facing significant pressure amid mounting fiscal concerns and potential shifts in monetary policy. Japan's fiscal outlook has deteriorated following Prime Minister Takaichi's approval of a massive 21.3-trillion-yen economic stimulus package, pushing government debt beyond 260% of GDP.

However, the recent rebound in the yen has been driven by the BOJ’s consideration of a rate hike in December, with board member Masu indicating that they won't wait for spring wage negotiations to conclude. Markets are pricing in a 71% probability of a December rate increase. Moreover, Japanese officials have intensified verbal intervention efforts to stem the currency's decline, with Finance Minister Katayama expressing deep concern over the yen's rapid depreciation and warning of possible intervention.

These underlying factors set the stage for a potential trend reversal in USD/JPY. Friday’s inflation data from Japan will be crucial for shaping monetary policy direction, as economists forecast core inflation to ease slightly to 2.6% from 2.8%.

GBP / USD

The UK autumn budget on Wednesday will be a critical focus for GBP/USD, with Treasury chief Rachel Reeves needing to plug a fiscal hole while maintaining growth prospects. Recent reports suggest Reeves may opt for multiple smaller tax measures rather than major income tax hikes, following improved OBR forecasts. The budget's credibility in addressing fiscal challenges while providing sufficient headroom will be key for sterling.

Meanwhile, uncertainty surrounding the Federal Reserve's December policy stance is creating volatility, with mixed signals from Fed officials. The NY Fed's Williams hinted at potential rate cuts, while the Boston Fed's Collins opposed easing. The compressed pre-Thanksgiving week schedule could amplify market moves. Gilt investors remain nervous about UK fiscal policy, with yields at risk of staying elevated due to increased political uncertainty.

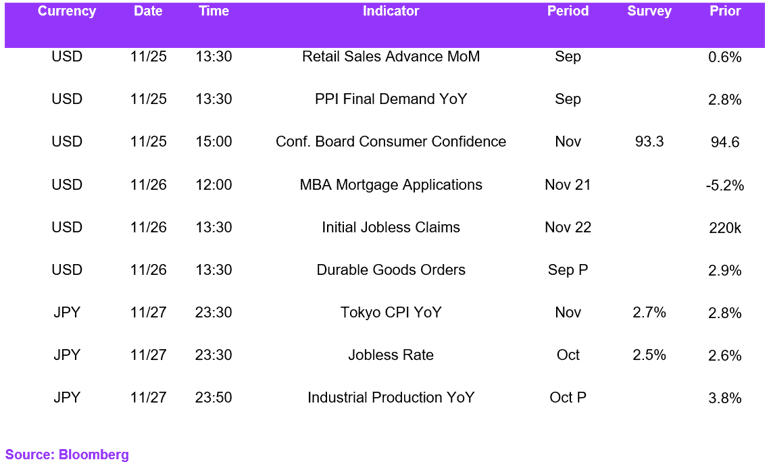

Economic Calendar