EUR / USD

EUR/USD continues to display notable resilience, holding comfortably above key technical benchmarks, including the 200-day simple moving average, and showing particular strength around the 1.174 area on firm trading volumes. The fundamental backdrop remains supportive for the euro, with the ECB maintaining a relatively hawkish stance while the Federal Reserve has already delivered three rate cuts, reinforcing a clear policy divergence in favour of the single currency.

Support for the euro is further underpinned by the ECB’s reluctance to signal aggressive easing, with some policymakers even leaving the door open to further rate increases. This stands in sharp contrast to the Fed’s increasingly dovish trajectory. Technically, an RSI reading near 70 points to overbought conditions, raising the risk of a near-term consolidation or pullback, although strong underlying fundamentals should help to limit downside pressure. A sustained hold above 1.175 keeps September’s high at 1.187 in view, while initial support is seen around 1.156. Beyond domestic drivers, China’s economic slowdown and associated yuan weakness appear to be exerting a more disinflationary influence on the US than on Europe, providing an additional tailwind for the euro.

Looking ahead, attention turns to a heavy US data run, with November nonfarm payrolls and CPI all due before the ECB decision on 18 December. Any further evidence of US labour-market cooling or softer inflation could bring expectations of additional Fed easing, keeping downside pressure on the dollar. By contrast, the ECB is widely expected to leave the deposit rate unchanged at 2.00%, and a steady policy message could further entrench rate-differential support for the euro. Near term, volatility around US CPI and payrolls is likely to be the key catalyst for a break either side of the 1.175–1.187 range.

USD / JPY

USD/JPY remains under pressure ahead of a closely watched Bank of Japan policy meeting, with markets increasingly confident of a 25bp rate hike to 0.75%. Recent Tankan survey data, showing business sentiment among large manufacturers at a four-year high, has strengthened the yen and reinforced expectations that the BOJ will continue to normalise policy.

Japan’s improving domestic backdrop, characterised by inflation holding above the 2% target and solid wage growth, supports the case for tighter policy, even as concerns linger following a 2.3% contraction in GDP in Q3 2023. From a technical standpoint, the pair has been consolidating in a narrow range between 155.68 and 156.09, remaining above its major moving averages and finding support near the 30-day VWAP at 155.74.

A decisive break higher could see USD/JPY retest the yearly high at 158.55 if resistance at 157.73 is cleared. Conversely, a move below the 50-day moving average would increase the risk of a deeper pullback towards the 153.50 area.

USD/JPY faces its most significant risk event of the week with the Bank of Japan policy decision on 19 December, where markets are increasingly positioned for a rate increase to 0.75%. On the US side, payrolls, CPI and PMIs will shape expectations for the Fed’s easing path, potentially amplifying any policy divergence shock. A hawkish BOJ outcome combined with softer US data would heighten downside risks for USD/JPY, while any disappointment from the BOJ could trigger a sharp short-term squeeze higher.

GBP / USD

GBP/USD is facing renewed headwinds as the Bank of England prepares for a widely anticipated 25bp rate cut to 3.75% in December, signalling a notable shift in policy amid a weakening economic backdrop. UK growth momentum appears increasingly fragile, with GDP contracting by 0.1% in October for a second consecutive month, intensifying recession concerns.

Technically, the pair has so far held above the 20-day moving average near 1.33, with elevated volumes suggesting solid near-term interest at these levels. The RSI at 64 points to building bullish momentum, although upside remains capped below the key 1.35 resistance zone. The 200-day moving average around 1.34 continues to act as an important barrier.

Looking ahead, sterling appears vulnerable as markets not only price in December’s expected rate cut but also the prospect of further easing into early 2026. Structural growth challenges, subdued business confidence and the lack of progress on a UK–US trade agreement continue to weigh on sentiment. Ongoing political uncertainty adds another layer of risk, pointing to the potential for continued sterling softness over the medium term.

For sterling, the focus shifts squarely to UK inflation data on 17 December, followed by the Bank of England rate decision the next day. CPI prints will be critical in determining whether the MPC delivers the expected 25bp cut to 3.75% or opts for a more cautious stance. Softer inflation would likely cement expectations for further easing into 2026, weighing on the pound, particularly if US data remain resilient. Conversely, any upside surprise in CPI could delay easing expectations and offer near-term support to GBP/USD, though broader risks remain skewed to the downside amid a fragile growth outlook and elevated global uncertainty.

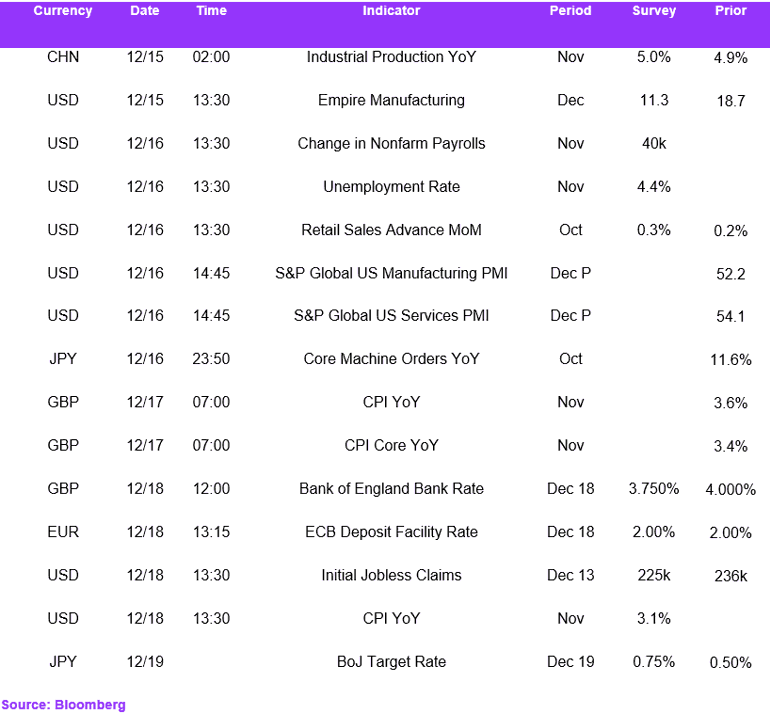

Economic Calendar