EUR / USD

EUR/USD posted modest moves, with the pair continuing to hover just under the shorter-term moving averages of 1.1660, with the RSI at approximately 40, indicating mildly oversold conditions. A decisive break below the 1.160 support level could accelerate selling toward yearly lows and potentially test the 1.15 handle.

The fundamental backdrop reinforces this technical picture, as robust US economic data, including retail sales outpacing expectations and existing home sales reaching near-three-year highs, contrasts with ECB warnings that markets are underpricing geopolitical risks that pose downside threats to eurozone growth.

Tariff-related cost pressures and persistent inflation risks may further complicate the Fed's rate-cut trajectory, potentially extending the dollar's yield advantage and maintaining structural headwinds for the euro.

USD / JPY

USD/JPY weakened to 158.20 as markets rejected recent highs on the back of overbought conditions and looming fears of potential intervention from the BOJ. Still, the overall macro structure suggests continued headwinds for the yen, driven by the substantial interest rate differential between the Fed's elevated rates and the BOJ's ultra-accommodative stance, which is expected to remain, despite the narrowing of the yield differential further into 2026. Japanese political uncertainty surrounding potential snap elections and speculation about dovish fiscal stimulus have created additional downward pressure on the yen, while the BOJ's structural constraints, stemming from debt exceeding 250% of GDP, limit aggressive policy normalisation.

From a technical perspective, the pair recently pulled back from highs near 159, though price action remains elevated above key moving averages. The daily RSI reading of 64 suggests moderately overbought conditions, while heavily accumulated long dollar positioning creates crowding risks that could amplify moves should sentiment shift. This convergence of narrowing monetary policy spreads, elevated political uncertainty, and stretched positioning creates an asymmetric risk environment where near-term momentum favours the dollar, yet markets are likely to remain cautious around the 160 key threshold in case policymakers make any moves to intervene.

GBP / USD

GBP/USD held its ground above 1.3400, with key support at the 200-day and 50-day moving averages around 1.3405, while resistance sits at the 20-day SMA near 1.35. The BoE is signalling potential acceleration of its easing cycle, with inflation expected to reach the 2% target by mid-2026, while the Fed maintains its restrictive stance with rate cuts pushed into the second half of 2026. Still, with these trends positioned further into 2026, and a lack of general investment into the dollar, with precious metals taking the brunt of speculative and safe-haven qualities, the moves are likely to remain constrained.

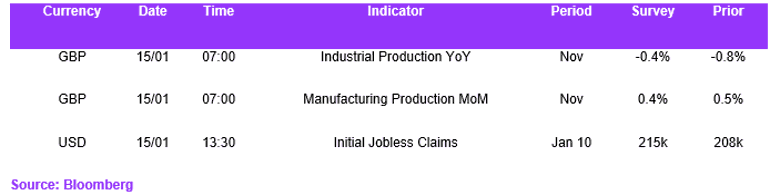

The neutral RSI reading of 52 suggests balanced momentum, with upcoming UK economic data releases, including GDP, employment, and inflation figures, likely to determine the pair's next directional move. A successful defence of the 1.3400 cluster may enable a push toward the 1.3558 weekly high.

Economic Calendar