EUR / USD

EUR/USD exhibits some volatility during the day, drifting lower through the Asian and European sessions before hitting a session low around 1.1805 during the mid-afternoon New York hours, where the heaviest volume concentration occurred. The pair subsequently staged a sharp recovery, reclaiming nearly all losses to settle near 1.1849, effectively unchanged on the day. This pressure persists amid a firmer dollar, as markets continue to delay their bets on a Fed cut.

Eurozone economic indicators paint a concerning picture, with industrial production decelerating to 1.2% YoY in January, German ZEW expectations unexpectedly deteriorating to 58.3, and the Euro Area Economic Sentiment Index falling significantly to 39.4, well below forecasts of 45.2. Upcoming macroeconomic releases, including FOMC minutes, fourth-quarter GDP estimates, and personal consumption expenditures data, represent critical catalysts that could either validate current dollar positioning or trigger mean reversion if inflation continues normalising.

While elevated euro short interest creates some technical risk of a squeeze, the combination of sluggish Eurozone growth dynamics, superior US economic resilience, and structurally entrenched fundamental headwinds for the pair suggest that downside risks for EUR/USD remain predominant in the near term.

USD / JPY

The USD/JPY pair is consolidating within a bearish structure, trading near 153.28 as divergent macroeconomic trajectories between the US and Japan increasingly favour yen strength. Japan's disappointing fourth-quarter GDP growth of just 0.2% annualised has paradoxically supported the yen, as real money investors reduce dollar-yen overweight positions and rebalance toward yen purchases, while the new Takaichi administration's fiscal caution removes a key yen-negative factor. Meanwhile, US economic resilience continues to provide a floor for the dollar, though below-expectation CPI data and approximately 59bps of Fed easing priced for 2026 temper the greenback's upside potential.

From a technical perspective, the pair remains firmly below a key resistance cluster formed by the 20-day SMA at 154.90, and the 50-day SMA at 156.05, while the 200-day SMA near 150.60 serves as critical support. The daily RSI, hovering around 39, reflects persistent bearish momentum accumulated during the 2.5% decline from early February highs above 157.

Market participants are now focused on upcoming U.S. data releases, including Federal Reserve minutes and preliminary fourth-quarter GDP figures, which will clarify the trajectory of U.S. monetary policy and likely determine whether USD/JPY defends the 152 support zone or breaks decisively lower.

GBP / USD

GBP/USD pair came under significant selling pressure, declining roughly 0.5% over the past 24 hours to approximately 1.3562, driven by disappointing UK labour market data that revealed unemployment rising to 5.2%, its highest level in nearly five years, while wage growth decelerated more than anticipated. This deterioration in employment conditions has fundamentally shifted monetary policy expectations, with market pricing now reflecting approximately 74% probability of a Bank of England rate cut by March and a full 25bps reduction by June. The Bank of England's recent 5-4 vote to maintain rates at 3.75% underscores deep internal divisions, yet the incoming labour data appears to have decisively tilted the balance toward the dovish faction favouring near-term easing.

From a technical perspective, the sell-off drove the daily RSI down to around 46, well below its recent baseline of 59, positioning the pair beneath the 20-day SMA at 1.3650, while still holding above the critical 50-day SMA at 1.3525. Peak volume coincided with the session low near 1.3497, suggesting aggressive selling that was subsequently absorbed as buyers defended the 1.3500 level. The concurrent strength of the US dollar, reinforced by robust American economic data and safe-haven demand amid geopolitical tensions, has created an asymmetric headwind for sterling that compounds the domestic weakness narrative.

Looking ahead, the pair's trajectory will depend critically on whether the UK's disinflation trend persists and whether additional economic data validates the dovish repricing already embedded in sterling, with a sustained hold above the 50-day SMA needed to prevent a deeper move toward the 200-day SMA at 1.3443.

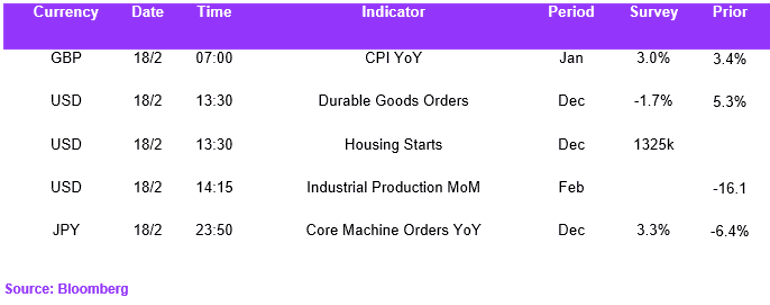

Economic Calendar