EUR / USD

Source: Massive (polygon.io)

EUR/USD continued to weaken on the back of continued dollar strength as markets seek safe havens. Global risk assets slumped sharply as the Middle East conflict broadened far beyond initial expectations, undermining confidence and triggering broad repricing across markets. The conflict is spilling across borders and energy chokepoints, particularly the Strait of Hormuz, which remains effectively closed to commercial traffic.

Expectations of elevated energy prices are widening the central bank policy divergence, as the Federal Reserve reprices toward a more hawkish stance, with rate-cut expectations collapsing from 79 to 57 basis points, while the ECB faces a stagflationary bind, unable to ease policy as eurozone core inflation unexpectedly accelerated to 2.4% even amid deteriorating growth signalled by weak German retail sales. Yield differentials have widened decisively in the dollar's favour, with U.S. ten-year Treasury yields surging to 4.095% against more modest European gains, creating sustained gravitational pull on the pair.

From a technical standpoint, the pair's sharp decline to a low near 1.1530 before a partial recovery to 1.1612 has pushed it just below key moving averages clustered around 1.17–1.18, while the daily RSI has plunged to approximately 33, signalling deeply oversold conditions that could trigger a near-term mean-reversion bounce toward the 100-day SMA at 1.1690. However, unless geopolitical tensions de-escalate rapidly and European energy prices normalise, the fundamental backdrop favours continued euro weakness, with a decisive break below the 1.1570 support zone risking an acceleration toward 1.1470 or lower.

USD / JPY

Source: Massive (polygon.io)

The escalating Middle East conflict and resulting energy market disruption have created a powerful structural tailwind for USD/JPY, as the United States' relative energy security stands in stark contrast to Japan's acute vulnerability as the world's largest energy importer. With Brent crude surging above $85 per barrel and the Strait of Hormuz effectively closed to roughly 20% of global crude flows, Japan's terms of trade have deteriorated sharply, compressing real income and undermining yen valuation. The widening interest rate differential, driven by the Federal Reserve's reduced probability of rate cuts and the Bank of Japan's likely postponement of policy normalisation amid energy-driven economic headwinds, provides additional fundamental support for dollar strength against the yen.

From a technical perspective, USD/JPY reflects this bullish macro backdrop, trading near 157.6 and sitting well above all key moving averages, including more than 500 pips above the 200-day SMA at 151.20. However, the daily RSI at 64 is approaching overbought territory, suggesting that a near-term pullback toward the 50-day SMA at 156 remains possible if profit-taking emerges.

On balance, the combination of persistent energy premiums, structurally wider yield differentials, and elevated inflation expectations points to sustained upside pressure on USD/JPY, with the January resistance near 159.3 representing the next meaningful technical target should buyers defend the 157.5 support zone today.

GBP / USD

Source: Massive (polygon.io)

GBP/USD continued to weaken as escalating US-Israeli military conflict with Iran has triggered a dramatic repricing of macroeconomic risk, disproportionately disadvantaging the UK due to its structural energy dependence, limited gas storage capacity, and heavy reliance on imported LNG, while the US benefits as a net energy exporter, insulated from supply disruptions. Simultaneously, the dollar is capturing safe-haven inflows as the US Dollar Index surged to 99.42, reinforced by hawkish repricing of Federal Reserve policy expectations after ISM Manufacturing Prices Paid surged to 70.5, collapsing rate-cut probabilities from 79% to 57%.

From a technical perspective, GBP/USD suffered a sharp sell-off from around 1.3410 to a low near 1.3251, trading below the critical 100-day SMA at 1.3400, with the daily RSI plunging to approximately 35, signalling oversold conditions. A modest recovery to close near 1.3343 suggests buyers emerged at the 1.3300 level, but the convergence of energy crisis dynamics, monetary policy divergence, and UK political fragility under a weakened Starmer government continues to exert decidedly bearish fundamental pressure. The key levels to watch are a potential mean-reversion rally back toward the 200-day SMA at 1.3445, versus a floor of 1.3300.

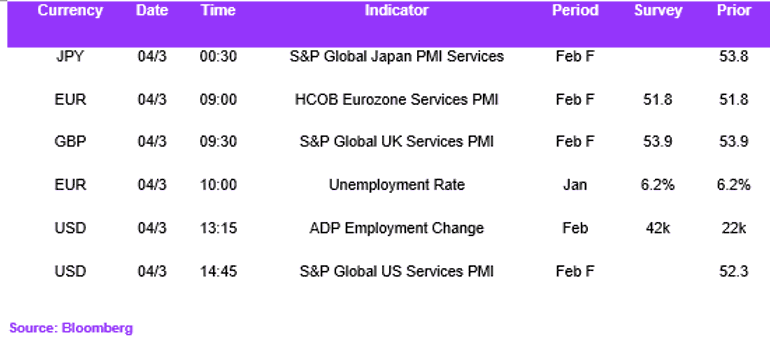

Economic Calendar