EUR / USD

Source: Massive (polygon.io)

EUR/USD is currently trading around 1.1536, having rebounded from recent dollar weakness. The daily RSI near 41 signals that technical momentum is improving from an oversold to a more neutral stance.

The fundamental picture is defined by competing macro forces. On the bearish side, the eurozone faces a persistent terms-of-trade deterioration as Brent crude remains above $100 per barrel due to the Strait of Hormuz disruption, disproportionately impacting energy-dependent Europe relative to the more energy-independent United States, while safe-haven flows continue to support the dollar amid elevated geopolitical uncertainty. However, a dramatic repricing in European monetary policy expectations - from a 40% probability of ECB rate cuts to an 85% probability of at least one hike by July - is creating a powerful countervailing force, as the potential narrowing of the ECB-Fed rate differential historically ranks among the most persistent drivers of foreign exchange moves.

The resolution of this tug-of-war likely hinges on the dual central bank meetings approaching in the coming weeks: a hawkish ECB commitment to a concrete tightening timeline on March 19 combined with a slightly more dovish Federal Reserve stance would create optimal conditions for EUR/USD mean reversion toward the 1.16–1.17 zone, supported by purchasing power parity analysis suggesting the euro remains approximately 18% undervalued. While it is expected that ECB policymakers will take a wait-and-see approach to the oil-driven inflation narrative for now, unless a strong narrative is presented, markets are likely to maintain their current interest rate pricing, which should only solidify should the conflict in the Middle East continue.

USD / JPY

Source: Massive (polygon.io)

USD/JPY dipped lower to 159, as the pair's recent price compression into a narrow 0.25% range suggests the market is consolidating ahead of critical meetings, notably the upcoming Fed and BOJ policy announcements scheduled this week.

The fundamental landscape is dominated by the Middle East conflict's impact on energy markets, which creates uniquely asymmetric pressures on the pair. Japan's near-total dependence on Middle Eastern oil imports exposes the yen to stagflationary risks that complicate the Bank of Japan's cautious rate-hiking trajectory, even as Governor Ueda signals that underlying inflation is gradually approaching the 2% target. Meanwhile, reduced Fed rate-cut expectations and safe-haven dollar demand have supported the greenback, though notable profit-taking in long-dollar positions after ten-month highs hints at growing caution among traders.

The approach toward the psychologically critical 160.00 level adds a layer of intervention risk, with Japanese Finance Minister Katayama reiterating readiness for direct currency intervention. The near-term trajectory will likely hinge on whether the pair can consolidate above 159 for a push toward the all-time high near 162, or whether a combination of intervention warnings, central bank guidance, and evolving geopolitical dynamics triggers a retracement toward the 158–156 support zone.

GBP / USD

Source: Massive (polygon.io)

GBP/USD has stabilised around 1.3354 after recovering from its monthly low near 1.3222, though the pair remains firmly trapped beneath a firm cluster of resistance where the 20-day SMA and 100-day SMA all converge near 1.3400 - a ceiling that has consistently capped rallies throughout the multi-week downtrend from the early-February highs near 1.3730. The daily RSI has recovered to approximately 43 from deeply oversold territory, signalling nascent momentum improvement, yet this stabilisation mirrors the broader technical picture of corrective bounces within a persistent falling channel rather than a structural reversal.

The fundamental backdrop heavily favours continued dollar strength over sterling. The UK economy faces a stagflationary trap, with January GDP growth stalling at 0% month-on-month, unemployment expected near a five-year high of 5.2%, and persistent energy-driven inflation constraining the Bank of England's ability to ease policy from its current 3.75% rate. Market expectations have repriced dramatically, compressing from two anticipated rate cuts in 2026 to just one, which fundamentally limits sterling's recovery potential. The projected 7-2 vote split at Thursday's hold decision reveals dovish undercurrents that may prevent the pound from rallying meaningfully even on a hawkish hold, as the announcement would serve as a ceiling rather than a catalyst for sustained strength.

Looking ahead, GBP/USD faces asymmetric downside risk within an expected 1.3225–1.3450 range, as the dollar's structural safe-haven advantage continues to dominate, and meaningful pound recovery depends on catalysts that have not yet materialised, including a dovish Fed surprise, credible energy supply normalisation, or exceptionally hawkish Bank of England forward guidance.

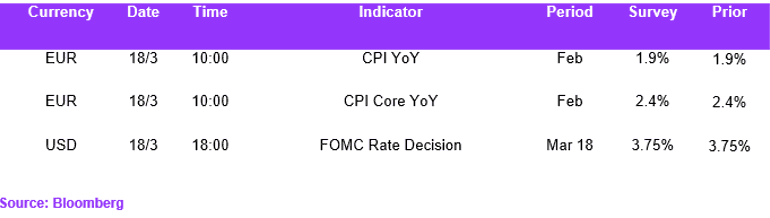

Economic Calendar