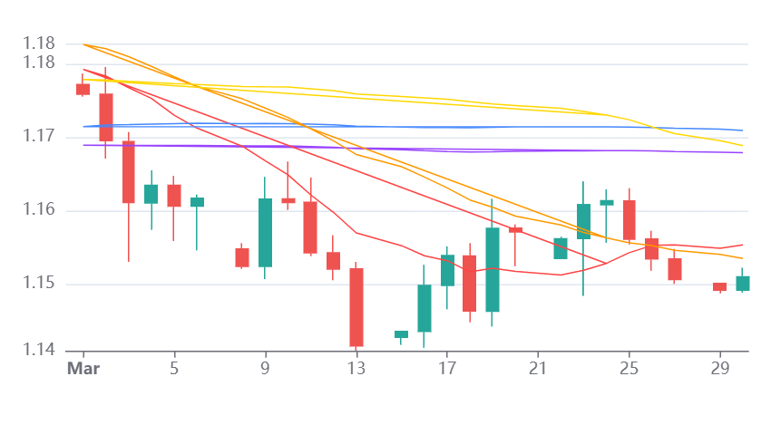

EUR / USD

Source: Massive (polygon.io)

EUR/USD remains under sustained pressure, and we see the dominant driver as the asymmetric impact of the Iran conflict on the two economies. Europe’s dependence on imported energy is translating into a sharper deterioration in growth prospects, while the United States continues to benefit from its position as a net energy exporter and from elevated commodity revenues. We see this divergence increasingly reflected in macro projections, with eurozone growth downgraded and inflation rising, reinforcing a stagflationary backdrop that constrains the ECB.

At the same time, we see a decisive shift in US rate expectations. Markets have effectively priced out rate cuts and are now implying modest tightening, which has widened the dollar’s yield advantage and supported strong institutional demand for USD. This combination of energy dynamics and rate repricing continues to underpin the broader dollar bid.

From a technical perspective, the pair is trading near 1.1510 and remains below all key resistance levels, including the 50 day and 200 day SMAs near 1.17 and the 30 day VWAP around 1.16. The RSI near 42 confirms that bearish momentum remains intact. We expect that the inability to reclaim the 1.16 area would leave the pair vulnerable to a retest of 1.1415, with a break below opening further downside.

Looking ahead, we see the outlook as highly dependent on geopolitical developments. A de escalation in the Middle East would likely trigger a sharp euro recovery through lower energy prices and a repricing of rate expectations. However, in the absence of such a shift, we expect the path of least resistance to remain lower. We also see a secondary scenario where broader global growth concerns begin to weigh on the US outlook, which could eventually stabilise EUR/USD.

USD / JPY

Source: Massive (polygon.io)

USD/JPY continues to be driven by a powerful combination of energy dynamics and policy divergence, and we see the pair remaining sensitive to both factors. Elevated oil prices are particularly negative for Japan, given its reliance on energy imports, and we expect this to continue weighing on the yen through a deterioration in the terms of trade.

At the same time, we see the dollar supported by safe haven demand and a sharp repricing of US rate expectations, with markets shifting from anticipating cuts to considering the possibility of further tightening. This has reinforced the rate differential in favour of the dollar and supported the broader uptrend.

Technically, the pair remains well supported above key moving averages, including the 20 day SMA near 159 and the 50 day SMA around 157. However, we see strong resistance in the 160.20 to 160.45 zone, which has been tested multiple times without a sustained breakout. The RSI near 59 suggests that momentum is moderating, raising the risk of a near term consolidation or pullback.

We expect the outlook to remain a balance between competing forces. On one side, dollar strength and elevated yields continue to support upside, while on the other, intervention risk near 160 and the prospect of gradual Bank of Japan normalisation introduce downside risk. Looking ahead, we expect developments in the Middle East and energy markets to remain the primary driver, alongside key Japanese data and signals from the BOJ.

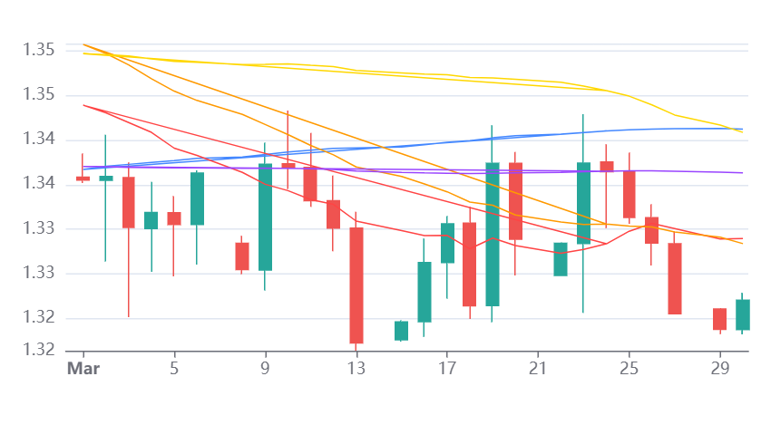

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains under significant pressure, and we see sterling particularly exposed in the current environment. The Iran conflict and associated oil shock are creating a stagflationary backdrop for the UK, where higher energy costs are feeding into inflation while simultaneously weighing on growth. This dynamic limits the Bank of England’s policy flexibility and undermines the currency’s appeal.

We also see a sharp shift in rate expectations reinforcing dollar strength. Markets are increasingly pricing the possibility of Fed tightening rather than easing, while volatility in UK rates markets has increased as positioning around BoE policy is unwound. This divergence continues to drive capital flows towards the dollar.

From a technical perspective, the pair is trading near 1.3272 and remains below both the 50 day SMA near 1.35 and the 200 day SMA around 1.34. The RSI around 43 confirms that bearish momentum remains in place. We expect the 1.3222 area to act as a key near term support, with a break below likely to open the path towards 1.31. Any recovery would require a move back above the 1.33 to 1.34 zone.

Looking ahead, we expect GBP/USD to remain highly sensitive to geopolitical developments and liquidity conditions. Sterling’s vulnerability to risk aversion, combined with widening spreads and fragile market depth, increases the risk of sharp moves. In the absence of a credible de escalation in the Middle East, we expect downside risks to remain dominant.