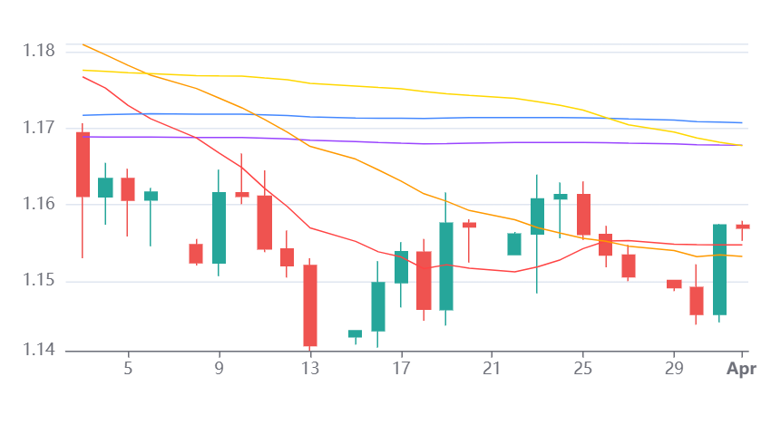

EUR / USD

Source: Massive (polygon.io)

EUR/USD is navigating an exceptionally complex environment, and we see the pair increasingly driven by geopolitical headlines and shifting rate expectations rather than clean macro trends. The recent rebound toward 1.1570 reflects a partial unwind of safe haven dollar demand following signals that the United States could scale back its involvement in Iran, though we expect volatility to remain elevated given conflicting messaging and continued uncertainty around the Strait of Hormuz.

We see weakening United States data beginning to weigh on the dollar at the margin, particularly ahead of the upcoming nonfarm payrolls release, where expectations remain subdued. However, we expect any sustained euro upside to remain constrained by structural headwinds, most notably Europe’s acute energy vulnerability and the stagflationary pressures building within the eurozone economy.

From a policy perspective, we see the European Central Bank facing an increasingly difficult trade off, with inflation rising on energy costs while growth deteriorates. Although markets are pricing further tightening, we expect this to provide only limited and potentially temporary support for the euro. Technically, the pair remains below key resistance near 1.16 to 1.17, and we expect bulls will need a decisive break of this zone to shift the broader trend. Absent a clear de escalation in the geopolitical backdrop, we expect rallies to remain fragile and prone to fading.

USD / JPY

Source: Massive (polygon.io)

USD/JPY is showing signs of near term exhaustion, and we see the recent pullback from the 160 area as an early indication that bullish momentum is beginning to moderate. The pair remains highly sensitive to developments in the Middle East, with energy prices and risk sentiment continuing to dominate direction.

We expect the yen to remain structurally disadvantaged by the energy shock, given Japan’s heavy reliance on imports, though we also see growing pressure on the Bank of Japan to normalise policy as inflation expectations rise. At the same time, we expect intervention risk to increase materially as the pair approaches the 160 threshold, which should act as a soft cap on further upside.

From a technical perspective, the move below the 20 day SMA and the test of the 30 day VWAP suggest a weakening short term structure. We expect that a break below 158 could open the way toward 157 and potentially deeper support near the 50 day SMA. Looking ahead, we expect the nonfarm payrolls release to act as the key catalyst, with a softer print likely to accelerate expectations for Federal Reserve easing and reinforce downside pressure on the pair.

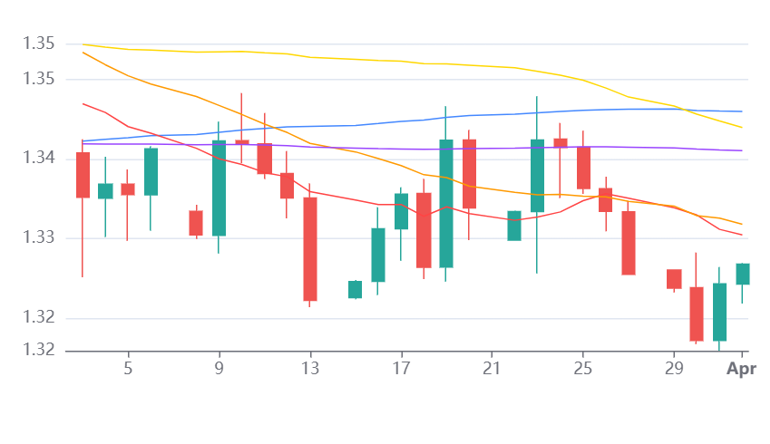

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains under structural pressure, and we see the balance of risks still tilted to the downside despite the recent stabilisation near 1.3266. Sterling continues to be weighed down by a combination of geopolitical risk, stagflation concerns, and fragile domestic fundamentals, all of which leave it particularly exposed in the current environment.

We expect the United Kingdom to remain more vulnerable than the United States to the ongoing energy shock, which continues to erode growth prospects while keeping inflation elevated. This places the Bank of England in a difficult position, and we see current market pricing for rate hikes as vulnerable to repricing should economic data deteriorate further.

From a technical perspective, the pair remains firmly below the key 1.34 resistance cluster, and we expect this level to cap upside in the near term. While short term rebounds may occur on improved risk sentiment, we expect these to be limited in scope. Looking ahead, we expect GBP/USD to remain under pressure, with a break below 1.3170 opening the path toward 1.3015, particularly if dollar strength persists and geopolitical uncertainty remains elevated.