EUR / USD

EUR/USD is trading near 1.1781, positioned just above converging 20-day, 50-day, and 200-day moving averages around 1.17, with the pair's broader uptrend having added roughly 5% over the past year. The technical structure shows price approaching established resistance near 1.1800, with a decisive break above this level potentially targeting January highs near 1.2040, while failure here could trigger a pullback toward 1.1720 support.

The fundamental backdrop presents a tug-of-war between dollar safe-haven demand—driven by the US-Iran conflict and elevated crude oil near $103-104 per barrel—and forced ECB hawkishness, with markets pricing an 84-85% probability of a June rate hike to combat energy-led inflation. The eurozone faces a stagflationary dilemma as manufacturing PMIs signal contraction while the prolonged Strait of Hormuz closure threatens sustained energy cost pressures, yet the euro finds support from the ECB's tightening stance and Friday's disappointing US non-farm payrolls print of 115,000.

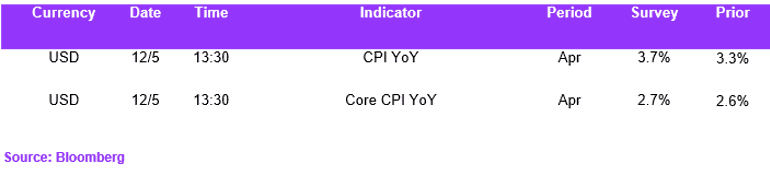

Key catalysts this week include Tuesday's US CPI report, expected around 3.7-3.8%, and the Trump-Xi summit in Beijing, where diplomatic progress on Iran could materially shift the energy premium currently weighing on the eurozone. The resolution of whether EUR/USD breaks above 1.1835 resistance or retreats will likely hinge on the interplay between geopolitical de-escalation prospects, the dollar's inflation narrative, and the ECB's willingness to tighten into economic weakness.

USD / JPY

The USD/JPY pair remains fundamentally driven by the substantial interest rate differential between the Federal Reserve's 3.50%–3.75% policy rate and the Bank of Japan's 0.75%, a gap that continues to fuel carry trade activity and persistent yen selling pressure. Compounding this structural weakness, the surge in crude oil prices past $100 per barrel following the collapse of US-Iran peace talks disproportionately burdens Japan's energy-import-dependent economy, amplifying the yen's vulnerability.

Despite Japanese authorities having deployed an estimated $35 billion in late April and potentially another $30 billion in early May to defend the yen after the pair breached 160, the currency has only partially recovered to trade around 157, highlighting the limitations of intervention absent a fundamental monetary policy shift. Notably, a growing hawkish undercurrent within the BOJ—with three board members now advocating an immediate rate hike and the core inflation forecast for 2026 raised to 2.8%—suggests the conditions for eventual policy normalisation are building.

From a technical perspective, USD/JPY faces significant overhead resistance at the 20-day SMA (158.30), and 100-day SMA (157.37), while the daily RSI at 43.70 confirms bearish intermediate-term momentum. The upcoming US CPI release represents a critical near-term catalyst: a hotter print would reinforce the higher-for-longer Fed narrative and likely push the pair toward those resistance levels, while a softer reading could see a retest of the 155.75 support area.

GBP / USD

GBP/USD is currently trading at 1.3612, well above key moving averages, including the 50-day and 200-day SMAs at 1.34, confirming a sustained bullish posture underpinned by favourable fundamentals. The Bank of England's hawkish hold at 3.75% on an 8-1 vote has shifted market expectations toward approximately 60 basis points of additional tightening before year-end, creating a supportive interest rate differential for sterling against a broadly weakening US dollar.

The pair faces immediate resistance at the 1.3626–1.3650 zone, which has been tested multiple times without a decisive breakout, while broad dollar weakness — with the DXY consolidating near multi-month lows around 98 — provides a tailwind for further gains. A daily close above 1.3650 could open the path toward the January highs near 1.3848, supported by the strong uptrend from late-March lows.

However, meaningful headwinds persist from elevated UK political risk following Labour's local election losses and surging gilt yields approaching 5.79%, alongside intermittent safe-haven dollar demand driven by the ongoing US-Iran conflict and Strait of Hormuz disruption. This week's US CPI data, with consensus near 3.8–3.9% year-over-year, will be critical in determining whether dollar weakness extends or reverses, making the 1.3650 resistance level a key inflection point for near-term directional conviction.

Economic Calendar