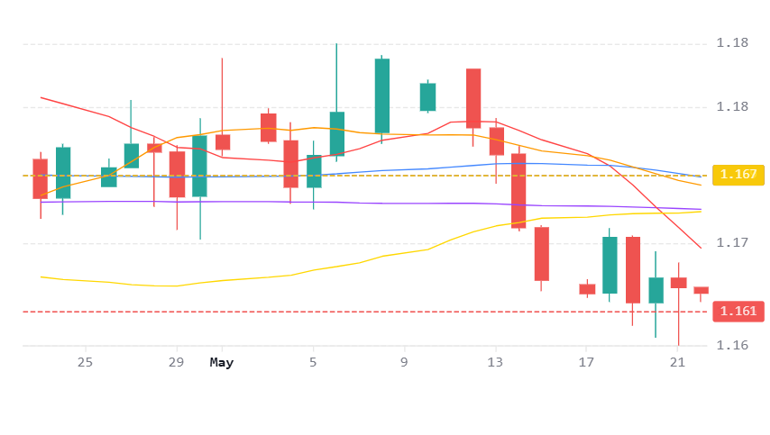

EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair faces a fundamentally hostile environment, with monetary policy divergence continuing to favour the US dollar. The Federal Reserve’s increasingly hawkish stance has effectively closed the door on near term rate cuts, while markets are now pricing a meaningful probability of a rate increase in 2026. In contrast, the eurozone remains trapped in a stagflationary environment, where weakening growth and persistent energy driven inflation continue to constrain the ECB’s flexibility. The ongoing US Iran conflict and disruption to Strait of Hormuz shipping routes remain structurally negative for the euro, as elevated oil prices near USD 100 to 107 per barrel feed imported inflation into Europe while simultaneously supporting US terms of trade.

From a technical perspective, EUR/USD remains below all major moving averages, with the 200 day, 50 day, 20 day SMAs and the 30 day VWAP clustered around the 1.17 region, reinforcing the broader bearish structure. Daily RSI near 42 continues to reflect subdued momentum and a lack of meaningful recovery traction. Although the pair has stabilised near 1.1614, support around 1.1587 appears increasingly vulnerable given the broader macro backdrop, and a sustained move lower could expose the 1.1456 level seen earlier this year.

Looking ahead, the broader outlook remains tilted in favour of continued dollar strength unless geopolitical tensions ease materially or softer US inflation data forces markets to reassess the Federal Reserve’s hawkish trajectory. Until then, we continue to see rallies towards the 1.17 region as corrective rather than trend changing.

USD / JPY

Source: Massive (polygon.io)

USD/JPY continues to consolidate near 159.09, remaining close to the psychologically important 160 level that previously triggered sizeable Japanese intervention earlier this year. The pair remains technically well supported above the 50 day SMA at 158.79, the 20 day SMA near 158.00 and the 30 day VWAP at 158.47, while the daily RSI around 57 suggests moderately constructive momentum without yet signalling overstretched conditions.

The macro backdrop remains finely balanced between persistent dollar support and rising expectations for Bank of Japan tightening. Elevated US Treasury yields and resilient US economic data continue to underpin the dollar, particularly as higher energy prices linked to the Iran conflict keep inflation concerns elevated. At the same time, markets are increasingly pricing the possibility of a Bank of Japan rate increase at the June meeting, which is gradually lending medium term support to the yen.

Intervention risk remains a major factor. Japanese officials continue to signal discomfort with excessive currency volatility, particularly near the 160 threshold, while thinner market liquidity conditions could amplify any sharp moves. A sustained break above 159.32 would likely encourage a retest of the April high near 160.65, while a failure to hold above the 50 day SMA at 158.79 could expose downside towards the 158 area, especially if Bank of Japan rhetoric turns more hawkish or intervention risks intensify.

GBP / USD

Source: Massive (polygon.io)

GBP/USD continues to face a difficult macro environment, with widening US UK policy divergence and elevated geopolitical risks keeping pressure on sterling. The Federal Reserve’s hawkish repricing following stronger inflation data has reinforced dollar strength, while the Bank of England remains constrained by the combination of persistent inflation and weakening domestic growth, highlighted by UK composite PMI slipping into contractionary territory at 48.5.

The Iran conflict and ongoing disruption around the Strait of Hormuz continue to create an asymmetric energy shock that disproportionately affects the UK as a net energy importer. Elevated oil prices are sustaining inflation pressures while simultaneously weakening growth prospects, leaving the Bank of England in an increasingly uncomfortable policy position. Political uncertainty and softer labour market conditions are also weighing on investor sentiment towards sterling.

Technically, GBP/USD remains below both the 20 day SMA and the 30 day VWAP near 1.3500, while the daily RSI at 46.5 reflects modest bearish momentum. However, the converged 200 day and 50 day SMAs near 1.3400 have continued to provide meaningful support across several recent tests. Looking ahead, we continue to see downside risks dominating unless there is a meaningful de escalation in geopolitical tensions or softer US inflation data revives expectations for Federal Reserve easing.