EUR / USD

Source: Massive (polygon.io)

EUR/USD remains structurally constrained, trading near 1.1638 within a broader bearish framework. The pair continues to struggle beneath a significant resistance cluster around 1.1700, where the 200 day SMA, 50 day SMA and 30 day VWAP converge. Daily RSI at 46.5 and the pair's decline from the April high above 1.1835 suggest momentum remains tilted to the downside, while support around 1.1553 remains the key level to watch should selling pressure intensify.

The fundamental backdrop continues to favour the dollar. The roughly 175 basis point policy rate differential between the Federal Reserve and the ECB remains a powerful driver of capital flows into dollar denominated assets. US economic data continues to outperform, with manufacturing activity at a four year high and inflation remaining elevated, while markets continue to assign a meaningful probability to further Federal Reserve tightening. In contrast, eurozone growth remains subdued, with weaker German demand indicators and elevated energy costs continuing to weigh on the outlook.

Attention now turns to the ECB meeting on 5 June. A more hawkish tone could support a move back towards the 1.1700 resistance area, although we expect any gains to remain limited unless accompanied by a material improvement in growth expectations. Conversely, a cautious ECB outcome would likely reinforce the recent downward bias and keep pressure on support levels. Until either geopolitical tensions ease materially or the Federal Reserve signals a clear shift in policy direction, the balance of risks remains tilted modestly to the downside.

USD / JPY

Source: Massive (polygon.io)

USD/JPY continues to test resistance near the psychologically important 160 level, trading around 159.73 after a steady advance. The pair remains comfortably above its key moving averages, with the 20 day and 50 day SMAs clustered near 159 and the 30 day VWAP around 158. Daily RSI at 62 points to firm momentum, although conditions are becoming increasingly stretched as the market approaches intervention territory.

The interest rate differential remains the dominant driver. While expectations for a Bank of Japan rate increase have strengthened, markets continue to focus on the sizeable yield advantage offered by US assets. Recent positioning data also highlights persistent speculative pressure against the yen, with short yen positions reaching their highest levels since mid 2024.

Governor Ueda's remarks later this week will be closely monitored for any signals on the timing of further policy normalisation. At the same time, intervention risks remain elevated near 160, although Japanese authorities have so far adopted a more measured tone than earlier in the year. We expect the market to remain cautious as it approaches this threshold.

A sustained move above 160 could open the way towards 161 and potentially higher, while failure to break resistance may encourage profit taking towards the 159 support area. Elevated energy prices and the Federal Reserve's restrictive policy stance continue to favour the upside, although intervention risk should limit enthusiasm for aggressive long positions.

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains range bound around 1.3450, trading between support at the 200 day SMA near 1.3400 and resistance from the 50 day SMA and 30 day VWAP near 1.3500. Daily RSI at 50.5 reflects the absence of strong directional momentum, with the market waiting for fresh catalysts before committing to a clearer trend.

The Bank of England's recent decision to maintain rates at 3.75%, supported by a narrow voting split, has provided some support for sterling and reinforced expectations that policy will remain restrictive for longer. This has helped the pound outperform several major peers, particularly given that the policy gap with the Federal Reserve is relatively narrow compared with the eurozone.

However, weaker UK growth expectations and fragile consumer confidence continue to cap upside potential. Meanwhile, elevated US inflation and ongoing geopolitical uncertainty continue to underpin the dollar through both higher yields and safe haven demand.

The focus this week will be on US payrolls data and broader risk sentiment. A stronger labour market report would reinforce the higher for longer narrative for US rates and could trigger renewed pressure on sterling. Conversely, softer data could support a move through the 1.3500 resistance zone and open the way towards 1.3548.

For now, we expect GBP/USD to remain broadly range bound, with support around 1.3400 and resistance around 1.3500 likely to define near term price action. While the longer term outlook remains constructive, the pair may require a softer dollar backdrop before a more sustained move higher can develop.

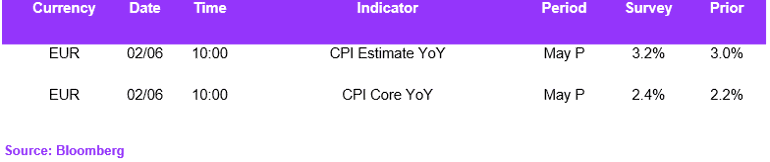

Economic Calendar