The latest episode of our fundamental coffee market outlook looks at whether or not the recent rally will last and gives some trading strategies to help navigate the market.

Executive Summary

- The ‘Phase 1’ trade deal continues to hit obstacles following the U.S. signing the bill which supports Hong Kong protestors

- The trend highlighted in our previous report regarding central bank remains constant, and we question the ammunition central banks will have in the case of a recession

- We believe that President Trump will look for a trade deal in 2020 and carry this positive momentum into his election campaign

- In Brazil, the pension reform will not help the economy in the immediate term, and foreign investor sentiment for the Brazilian real is weak

- The oil auction in November was disastrous for the real and highlighted weak appetite for Brazilian assets reducing future currency flows

- Moderate changes made to our S&D balance due to a reduction in inputs and political unrest in C. America increases our market deficit for the 19/20 season to 5.01m bags

- Strong local prices have favoured Brazilian producers who can hedge far forward, however, those who sold at 105cts/lb will not be so happy. At the time of writing, March 2021 trades at R$5.60/lb

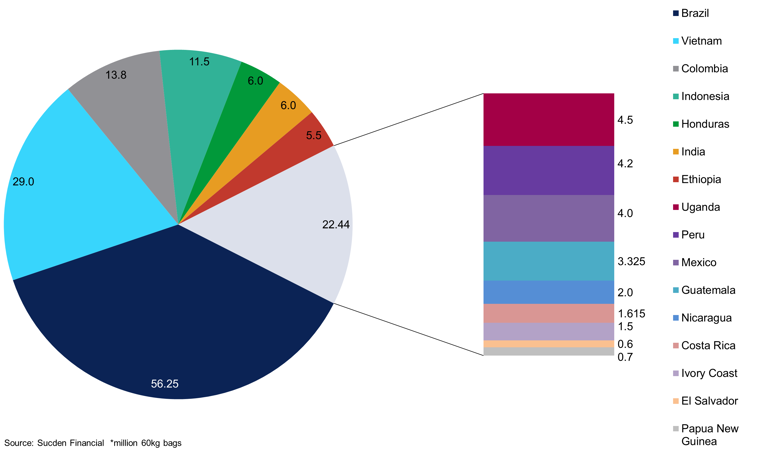

- We maintain our Brazilian figure for 2019/2020 at 56.25m bags and indicate that due to stress on trees the 2020/21 season does not look likely to be 65-70m bags

We see the deficit in fine cup coffee, due to the quality issues in Brazil, C. America, and Colombia - Colombian shipments have remained strong throughout 2019 averaging 1,101,655 bags per month through to the end of September

Canada has emerged as a large importer of Colombian coffee in recent years, importing 727,941 bags through to the end of September and could break 1m bags for the first time - We still believe that certified stocks is the cheapest coffee around and therefore we anticipate certified stocks will continue to drawdown in the coming months

- Analysing Arabica certified stocks, we see that total stocks continue to drawdown, but coffee waiting to be graded continues to flow in

- Favourable Brazilian prices will likely keep the flow of Conillons steady, putting pressure on the London contract and this should, in theory, put pressure on the spreads; we know, in practice, this may be different

- The one year spread between January 2020 to January 2021 has tightened into -$103/t as of December 12th, from -$163/t from October 15th

- TET is early this year and there is a lot of producer selling still to be done, which will put downward pressure on the London contract

Trade Ideas

- For some time we have been in favour of the arbitrage, and in our last report we favoured buying the arb at 38cts/lb and when the March/March arb is trading at 60cts/lb, the trade looks fruitful. A small trade of 10 lots would have yielded $123,750

- However, we would not buy the arbitrage at 70.5cts/lb

- Our apprehension in the market is increasing as prices approach 135-140cts/lb, and in the near term we believe KC would benefit from a correction to the downside

- In the immediate term, margin calls from local producers could facilitate the rally as they are force to cover shorts. Making it a moving target, with some of the physical traders playing catch-up

- Our strategy has shifted from selling rallies to buying dips

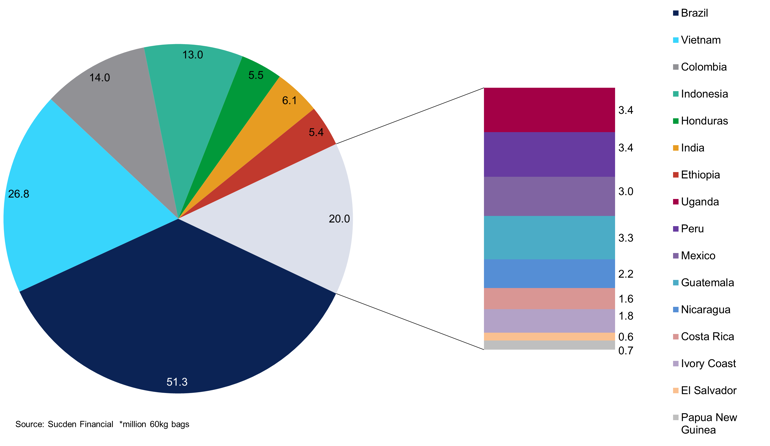

Sucden Financial's Coffee Balance

Global Coffee Balance

Macro Overview

The U.S. consumer spending has continued to show some resilience to the trend of the global slowdown as it continues to support growth. In Q3 2019, US GDP grew at a slower pace of 1.9% q/q as softness in trade and investment manifested economic weakness. Consumer spending, a key driver of growth, grew at 2.9% annualised rate in Q3, supporting a weaker economy. For H2 2019, Bloomberg Economic forecast growth to decline to 1.7% vs the 2.6% GDP growth in H1 2019. Wage pressures, however, have accelerated in response to tightness in the labour market, which shows no signs of relaxing, remaining at 50-year lows. Meanwhile, the sharp increases in bond yields are pushing up borrowing costs up, which will be a headwind for the consumer more in the long-term. Personal savings also are edging higher to 5-year highs, a telltale sign of consumer being cautious of the future.

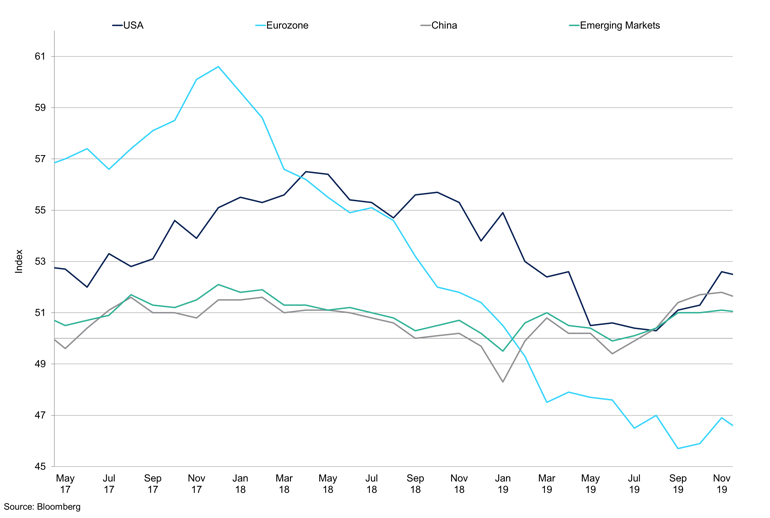

Apprehension is also evident in the manufacturing and factory sectors. Lower corporate investment and hiring drags on the economy as small companies, in particular, are hesitant to expand their operations in 2019 / 2020. Particularly poor performance was coming from manufacturing, utilities and mining sectors. Phase one of the trade deal with China has not seemed to lift the gloom of the manufacturing sector and might not do so until further substantial steps are taken to secure the deal. A caveat is the time lag of sentiment to filter into the underlying data, however with surveys being filled out by a decreasing number of participants they there can be a disconnect between surveys and economic data. Overall, weak external growth and the impacts of the trade spat have hurt demand for manufactured goods. This, accompanied with the headwinds from a stronger dollar, intensified the difficulties for US manufacturers’ performance.

Manufacturing PMIs

Eurozone manufacturing continues to underperform other major economic in 2019.

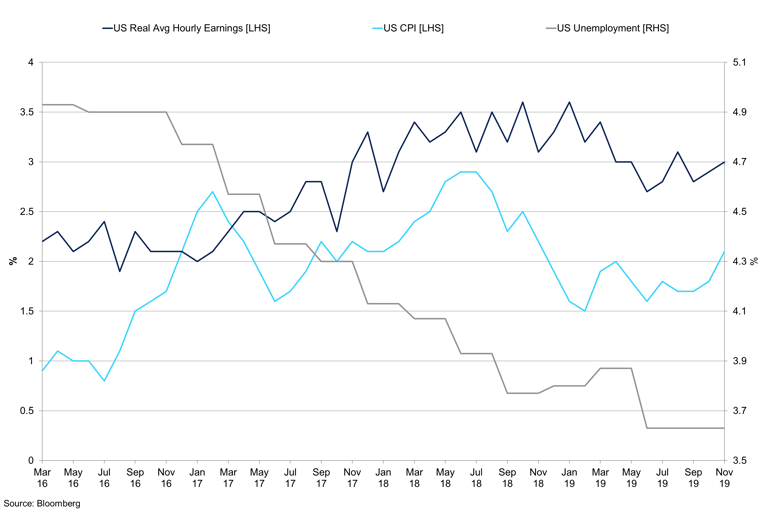

The October nonfarm payrolls remain resilient at 128k, above expectation, suggesting that declining manufacturing performance woes are not yet dragging the broader economy. While factory hiring posted a modest contraction, goods sector employment continues to rise, signalling yet again the impact of the trade war on factory output. The markets responded well despite lower figures on-trend, as the October GM strikes were forecast to impact the labour market data. The strikes, however, have dampened the initial jobless claims performance up to 225k from 211k a month prior. We believe that with the November payrolls report set to be lifted by 40-45k after the end of the GM workers strike, the data should stay consistent with steady monetary policy in December.

US CPI vs Unemployment vs Real Hourly Earnings

US labour market continues to show resilience to global shocks.

This quarter’s sharp rise in overnight repo rate took place as reserves became scarce and, as a result, the central bank is now purchasing $60b in Treasury bills each month to maintain the level of the balance sheet. Despite calming the market nerves, no fundamental adjustments have been made to address the liquidity issue, raising the possibility of another bubble emerging as companies require higher level of financing than before. The Fed’s balance sheet has increased by 7.14% since the start of September outlining the need to provide liquidity and support the market.

China and the US continue the talks with some signs of progress being made, and further breakthroughs might support the slowing economy into 2020. However, as of now, Trump’s impeachment process increases uncertainty and reduces the likelihood of additional fiscal stimuli measures needed for his 2020 re-election success. Worldwide, fiscal and monetary stimulus measures will prevent a sharp slowdown but may increase financial vulnerabilities against a recession threat that is foreseen by many into late 2020-2021.

Origin Focus

The Brazilian economy saw a clear breakthrough on October 22nd as the Senate approved a sweeping overhaul of the country’s pension system. The pension reform in Brazil is seen as a crucial tool to stabilise the nation’s public finances and to restore business confidence. The bills passed aim to save the Treasury around $195 billion over the next decade, plus $68b of ancillary savings, via measures that include raising the minimum retirement age and increasing worker’s pension contribution.

The pension reform is seen as key to restoring confidence in Brazil’s sluggish economy, which grew 0.4% q/q in Q2 2019 up from contracting in Q1 where the mining disaster halted the growth. The service sector that accounts for 70% of Brazil’s economy fell by 1.4% y/y in August, indicating that exports and manufacturing sector are feeding through to the broader economy. Weak 2019 growth has also contributed to widening the deficit, as declining household income impacted tax revenues. This would contribute to an already high level of debt that the country has accumulated over the years, which is forecast to hit 90% of GDP by the end of 2019.

Markets responded positively on the optimism of the long-awaited pension reform; however, this confidence channel might be short-lasting given that the nation does show prominent signs of recovery in 2020. Ultimately, the goal is to establish several measures to close a fiscal deficit that cost Brazil its investment-grade credit rating. The next big reform on the way is to simplify the nation’s tax system, which should make it more manageable for mid-size companies to pay taxes. The agenda also includes efforts to attract more private sector investment to infrastructure projects, to trigger automatic austerity measures when fiscal limits are breached and to decentralise public spending. These measures still need to go through the approval stages later in the 2020s. So far in 2019, the government has announced spending freezes totalling R34b to attain its primary budget deficit target of R139b. The September value for the primary budget deficit amounted to R20.37b, narrowing by 11.5% y/y.

According to the IMF, Brazil is forecast to grow by 0.9% in 2019 and 2.0% in 2020, on the back of accommodative monetary policy and weaker inflation. According to government new estimates, projections for 2019 consumer prices, current account balance (as a % of GDP) and unemployment stand at 3.6%, -1.2% and 11.8% respectively. With inflation under control, we would expect the Brazil Central Bank to further cut rates to 4.75% in 2020.

Brazil’s recent oil auction disappointed the markets as high prices and complex and non-transparent governance kept foreign investors’ interest muted. Only one of the four blocks was bid for, and thus, with limited financing gathered, hopes of easing a tight federal budget have faded. The government officials have since called for a more straightforward concession model in the upcoming oil rounds. This auction took place weeks after Bolsonaro announced his intent to meet the OPEC leaders in hopes of re-joining the biggest oil and natural gas producer and grasping the benefits of the cartel. If it were to join, Brazil would be one of the most significant producers in years, as its oil contribution reaches a record 3.1mbpd in August, in line with UAE production, according to the IEA.

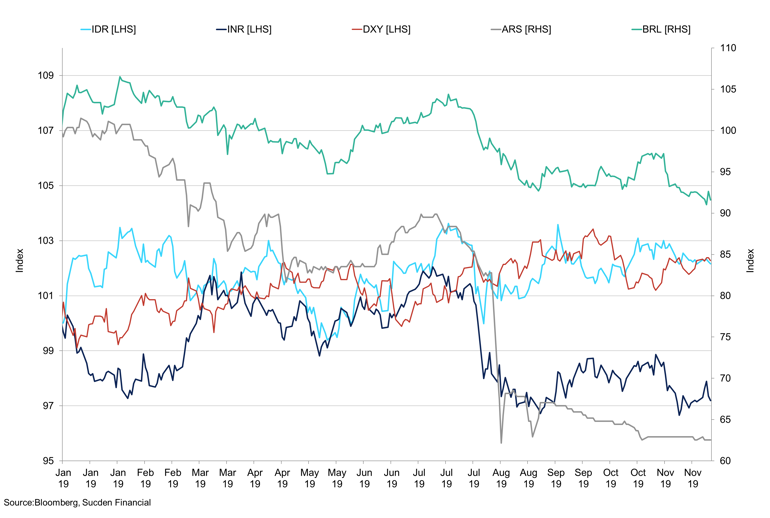

Emerging Market Currencies vs Dollar

Argentine Peso has seen the worst performance amongst other EM currencies since the beginning of 2019.

In the week of the auction, the USDBRL gained 4.8% and has broken through the 4.20 level for the first time since September 2015. We should see some temporary appreciation in the Real given the US and China trade deal shows further progress past Phase one as risk appetite for emerging markets returns. However, the long-term sentiment remains moderately bearish until substantial signs of recovery are seen in the nation’s growth performance.

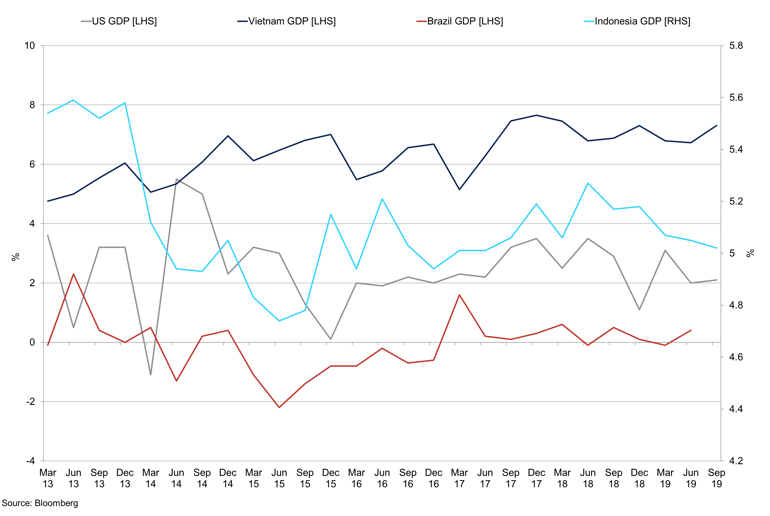

Vietnam is showing some signs of a slowdown in 2019 as the nation is forecast to grow below 2018 growth; however, it remains the clear ‘winner’ in the outcomes of the US-Sino trade war. Vietnam’s economy is forecast to grow by 6.7% in 2019, supporting South-East Asian compound growth. For 2020 and 2021, the World Bank estimates growth to remain robust at 6.5%, yet, some deceleration is felt amid weaker external global growth and tightening of credit and fiscal policies. Nevertheless, with inflation at low levels of 2.24%, Vietnam will most likely not follow through with the easing cycle in 2019.

Manufacturing PMI level has declined to record lows of 50.0 since 2016, as customers are reducing the size of their orders. A similar pattern was seen with regards to new export orders, with the rate of expansion softening to a slower pace of growth.

Unlike what has happened globally, Vietnam’s exports have been growing faster than its GDP and rising as a share of GDP. Moreover, exports to the US were up 40% y/y, whereas overall exports declined by 0.8% y/y. In export revenues, Q3 figures reached $71.76b, 10% increase y/y, largely attributed to outflows into the US. In response to Trump’s tariffs on Vietnamese steel exports, the nation pledged to import more US goods to appease Washington over its expanding trade surplus and damp down perceptions that it is profiting unfairly from the US-China trade war. Indeed, steel exports, the biggest Vietnamese commodity, showed a minor decline in August. This downturn, however, was short-lasting and export levels made a swift recovery to 480k tonnes in October as a result of no further action employed by President Trump. Nevertheless, according to Vietnamese authorities, some logistical bottlenecks have emerged, limiting how much the country could accommodate those additional flows from China into the US. Indeed, money flowing into new plants in Vietnam is straining the country’s roads and docks, with complaints rising about port congestion.

US vs Vietnam vs Brazil vs Indonesia GDP Performance

While Brazil and Vietnam have seen consistent GDP growth, the US and Indonesia have lost some of their strength in 2019.

Indonesia’s GDP declined marginally to 5.02% in Q3 from 5.05% a quarter prior despite weak global demand affecting trade and low commodity prices impacting the manufacturing output. Low investment inflows and low government spending dragged the economy into the slowest performance in more than two years. According to the Finance Minister Sri Mulyani Indrawati, 2019 GDP growth is estimated at 5.08%.

Investment growth slumped to 4.21% y/y in Q3 from 6.96% a year prior. Household spending, which accounts for more than half of GDP, increased 5.01% y/y, marginally higher than 5% in 2018, supporting the target growth. The increase, however, was driven by spending tuition fees so the effect could only be short-lasting and the nation might show some signs of further deterioration if the trade relations do not improve.

Indonesia’s central bank has cut interest rates four times this year to support growth, reversing some of the 175bps of tightening in 2018. October exports contracted by 6.13% and imports plunged 8.6% y/y as the impacts of the trade war have particularly taken the South East Asian economies by storm. As revenues come under pressure, the government has widened its budget deficit to more than 2% of GDP in 2019 and proposed a $180b budget to parliament for 2020, 3% greater than 2019’s plans. With the government’s mandate to defer capital intensive projects to limit the current account deficit, the imports have been contracting January to September. Indonesia achieved a trade surplus in October but at the cost of a pullback in capital machinery and raw material imports. Indonesian bond yields have been notably responsive to the progress of the US-Sino trade war, and have posted substantial losses amid the trade talk progress.

Corporate Earnings

Luckin’s quarterly results showed net revenues from products reaching RMB1.5b (US$213m), as it continues to expand new stores in China. The chain is seeking to overtake Starbucks, which has about 3,700 outlets and aims to have 10,000 stores operating by 2021. However, as it continues to expand, Luckin is facing problems targeting its goods a big share of the Chinese population. According to the FT Research, only those living in the first-tier cities in China, i.e. richest consumers, are increasing their intake markedly, whereas, those that live in remote areas have little preference for caffeinated drinks. Luckin’s goal is to open more stores in those remote areas to create demand for coffee, providing convenient locations across the country as well as low prices for coffee. Given the success in these areas, we would expect to see Luckin monopolising the caffeinated drinks industry in remote China.

According to Luckin financial results, 5.9m new customers were gained q/q in Q2 2019, yielding a total of 22.8m. Average total items sold increased 589.7% y/y, and 593 net new stores opened q/q, where most of the growth came from the pick-up location rather than relax stores and delivery kitchens. Luckin’s strategy revolves around pick-up stores rather than traditional coffee shops like Starbucks and Costa, keeping renting costs at a minimum and ensuring steady customer flow.

Since its inception, Luckin’s losses had inflated to $231m in 2018 from just $8m in 2017. The release of coupons and discounts has helped the company cut losses by over Rmb100m (US$14m) in Q1 2019. LCD (Luckin Coffee) claims to have substantially reduced their store operating losses as a percentage of net revenues and is on track to reach level break-even point during Q3 2019. While the absolute value of the operating costs keeps increasing, as a percentage of net revenues, it decreased to 175.9% from 382.7% in Q1 2019. Luckin Coffee has agreed to establish a joint venture with Louis Dreyfus (LDC) to develop a juice brand in China, the production and bottling of which will be controlled by Margarita Louis-Dreyfus. It is worth bearing in mind that juice beverages are one of the most popular types of beverage consumed in China per annum.

In Q3 2019, Nestle posted organic growth of 3.7% q/q with Strong Real Internal Growth (RIG) at 3.0%; growth was mostly supported by ‘strong momentum in the United States’. The company stated that lower coffee prices weighed on RIG performance; their coffee products posted positive growth. The beverage category saw mid-single-digit growth, and Starbucks creamers generated strong demand. The roll-out of Starbucks products continued, now reaching 34 countries and net acquisitions increased sales by 5.5% in the Americas, largely related to the acquisition of the Starbucks license. In Latin America, growth for coffee was in high single-digits, and America contributed most of the new growth. Nespresso has also maintained solid mid-single-digit organic growth, while North America and emerging markets grew at strong double-digit rates. In China, coffee performed ‘well’. From other news, Nestle announced that it would launch a buyback plan to boost the company’s value to shareholders.

Starbuck’s 4th 13-week quarter posted revenue growth of 6-8% with the US businesses delivering 6% comparable-store sales growth, while China grew by 5% despite growing competition from Luckin coffee. Alibaba accounted for 7% of sales through its partnership with Starbucks. In the corporate earnings segment, the chain mentioned enrolling its new program to personalise orders according to customers’ previous orders, to optimise store labour allocations and drive inventory management in stores as it continues to provide service for 17.6m online loyalty program customers. Iced coffee beverages and improved revenues and sales from China prompted Starbucks quarterly earnings above expectations. The net income reached $802.9m, up from $755.8m in 2018.

Dunkin’s latest quarterly report indicates that the US comparable-store sales increased 1.5%, over the period analysed. Baskin-Robbins, the subsidiary of Dunkin’s Brands, posted its best quarterly sales results in the US since the Q4 2017, with cold drinks leading most of the growth. CEO David Hoffmann mentioned that 40% of Dunkin’s Q3 sales growth came from the espresso drinks, led by strong performance in new Signature Lattes line extensions. In Q3, the Dunkin’ brand opened 122 net new restaurants globally. In the US, 3rd quarter revenues represented an increase of 5.8% y/y. Sales in South Korea, Latin America and Europe were negatively impacted by unfavourable foreign exchange rates. Dunkin expects comparable store sales to continue at a lower-single-digit growth in Q4.

Changes in Supply and Demand

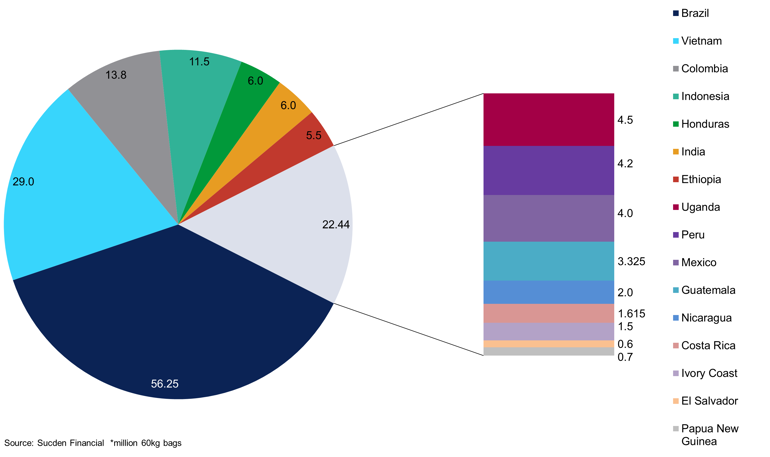

Global Coffee Supply 2019/20

The S&D balance from our previous report was a deficit of 4.14m bags. However, recent revisions have increased the deficit to 5.01m bags due to a significant reduction in the Honduran crop to 6m bags from 6.75m bags. This is due to lack of second fertilisation which has prompted yields to decline and also the political unrest in recent months which has prompted unrest in the industry. The second revision is also in Central America, we have revised lower our Nicaragua crop figure for the 19/20 season to 2m bags from 2.125m bags. The unrest in Nicaragua has been re-affirmed by President Trump extending the national emergency for Nicaragua over attacks on anti-democratic policies. Since the 2015/2016 season, our average balance is a 1.70m bag surplus over the period analysed, the total is an 8.46m bags surplus.

The revisions to the supply side have caused the global deficit to decrease to 5.01m bags, as we maintain our demand figure for the 19/20 season at 164.5m bags. Looking ahead to the 20/21 season, we have a provisional consumption increase of 1.2% from 164.50m bags to 166.47m bags. While 2% growth may have been applicable to the market five or so years ago, as total consumption increases, obviously 2% of 164.5m is significantly larger than 2% of 150m bags. We still see the Chinese market behind the curve but, with strong investment into this region, we would anticipate this to start to take off in the coming years, putting significant pressure on the supply side and inventories. Other growth areas remain in origin countries: S.E.Asia, Canada, the US and also Middle Eastern countries.

We do not anticipate a 70m bag crop in Brazil next year, and this will put further pressure on inventories and Colombian production. In our opinion, the market psyche has changed from the one of selling rallies to buying dips. Our weekly coffee matrix has shown the macro variables are weighing on the matrix and have done so for some time. Furthermore, the real reached an all-time low on November 26th at R$4.2770 to the $, but the NY contract has remained firm. While we see little support for the BRL outside the Brazilian Central Bank, a rally in 2020 in unison with bullish fundamentals could provide a strong platform for the Arabica contract to rally. Indeed, we see value in the flat price around USd105/lb and expect larger Conillon crops and inventories to weigh on the London contract, favouring the arbitrage.

With the global export figure of 129.40m bags globally, this outlines that demand is improving. Despite the year-on-year growth of 8.1% y/y, inventories have not increased a proportionate amount. We continue to see consumption increasing with pockets of strong growth in the US, Canada and S. E. Asian countries. European demand is stable, and we do not see an exponential increase in European consumption in the 18/19 season nor 19/20 for that matter. While a minor part can be attributed to the weak economic performance in the euro area and the upwardly stickiness of prices, despite the decline in the exchange price, we see this region as relatively saturated in the near term. We see a lot of product going straight to industry, and some of the decoupling between the exports and inventories could be explained by the market being efficient and processing coffee when it is cheap and storing the product as the finished product.

Canadian demand continues to go from strength to strength; Canada imports the majority of its coffee from Colombia, as outlined below. The second-largest exporter is Brazil, $197.58m and $132.5m is the value of coffee imported into Canada from Colombia and Brazil respectively, according to Statista. Indeed, consumption is expected to reach 5m bags in the coming year up from 4.68m bags in the 18/19 season.

Canada’s appetite for coffee can be outlined by the increase of coffee shops; domestically owned Tim Hortons has 4,000 stores countrywide and if you use Starbucks as a loose barometer for coffee demand, you see that there are 1,607 stores in Canada, 1,175 of which are company-operated stores with 432 of them licensed, in 2019 according to Statista. This is up from 1,460 stores in 2017, not quite the pace of growth of Luckin coffee but constructive for demand none the less, and during a survey in 2018, 72% of respondents had consumed coffee the day before the survey.

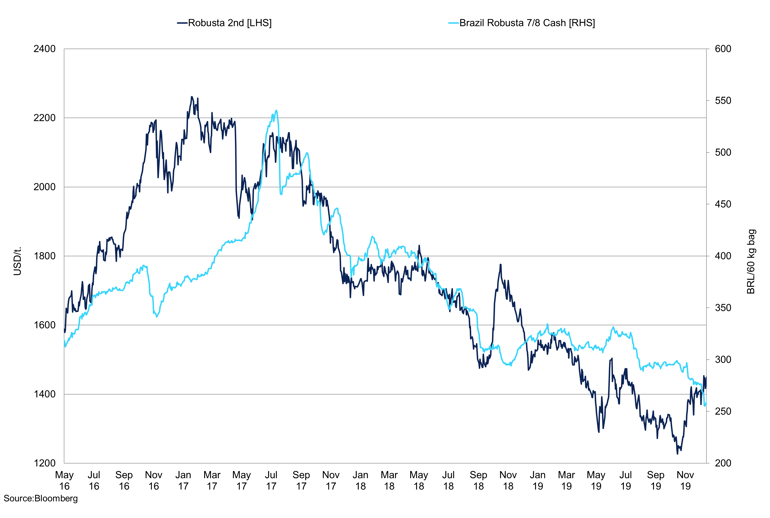

Brazil Robusta 2nd Month vs Brazil Robusta 7/8 Cash

Brazil

We maintain our crop figure for the 19/20 season at 56.25m bags with a split of 18m bags for the Conillon crop and 38.25m bags for the Arabica crop. We note that just before our last report, there was a cold snap which likely caused some stress to the trees. Indeed, we thought it was 1°C away from significantly damaging the crop. The recent hot and very dry weather that we saw in September compounded pressure on the trees, however, the rain arrived and fears abated somewhat. If the rain triggered flowering and then the weather became hot and dry once more, this could have been incredibly damaging for coffee trees; which would have been detrimental to yields and in turn our crop figure. The weather issues this year have reduced the probabilities of a 65-70m bag crop in 20/21. As mentioned above, flowering issues could prevent another monster crop, if Central America and Colombia are unable to respond and fill the void in the Arabica market, we would anticipate further drawdowns in stocks, and traders may look at 100-105cts/lb with regret. Indeed, we maintain our view that Brazilian consumption is 21.5m bags, and a smaller Conillon crop next year may mean more coffee is held back for domestic consumption. Carry-over would be minimal going into an on-year of 21/22. While we believe it is too early for an accurate crop estimate for 20/21, we believe market sentiment is changing and favour buying dips; we believe 115-118cts/lb is what 100cts/lb was at the time of our last report. The recent rally has clearly taken its prisoners with the market, with rumours of another exporter blowing, making it the 3rd this year, causing investors to lift their hedges. This may have caused the commitment of traders to go to a net long.

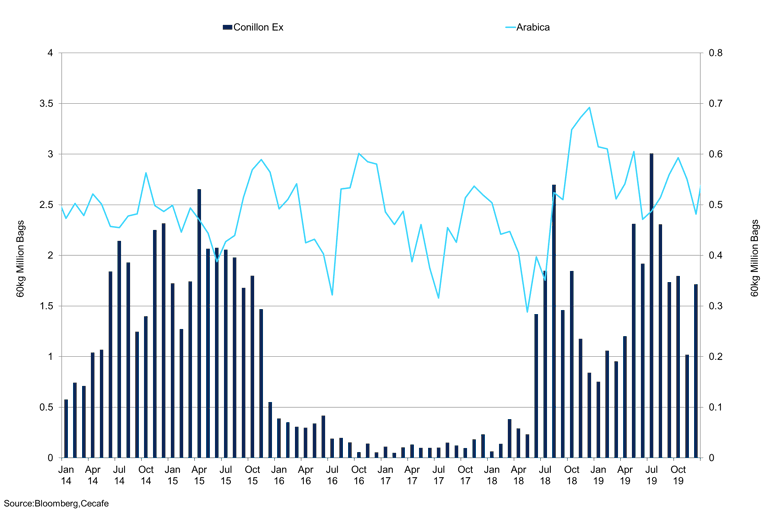

Brazil Conillon vs Arabica Exports

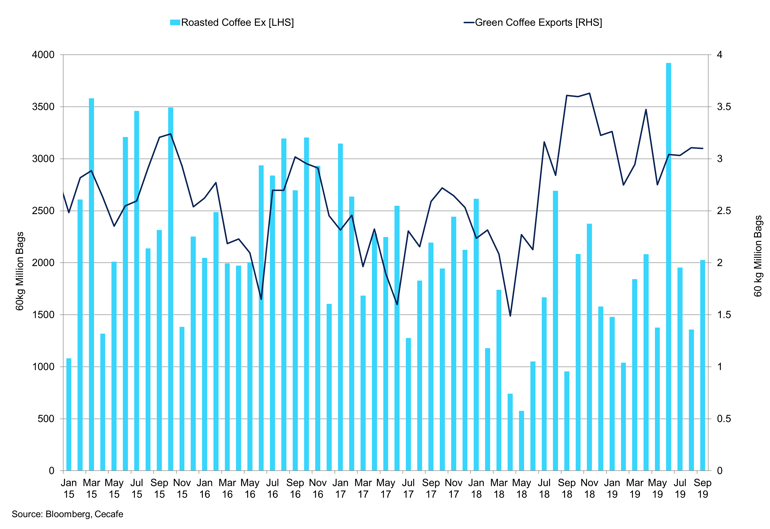

Brazil Roasted Coffee vs Green Coffee

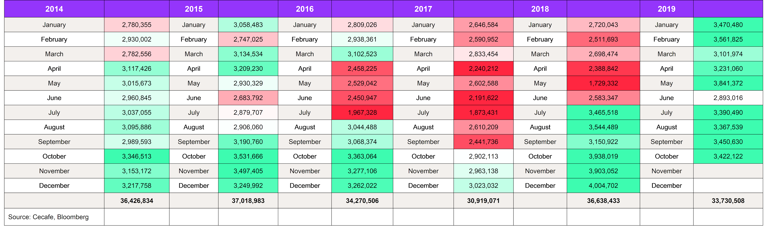

Brazilian shipments have remained strong, averaging 3.4m bags a month, according to Cecafe data, which is the same as the ten months average. Conillon shipments have softened in recent months, below the ten-month average of 328,812 bags a month. We expect this to remain the case in the coming months despite the favourable currency levels. Another rally in the flat price would really twist the knife into those who hedged around USd105/lb. Early estimates for the 20/21 crop suggest another large crop is on the horizon, but again, weather conditions need to be incredibly favourable, especially after the stress the trees have seen. 20/21 is an on-crop year, and even though the cost of production is low in Brazil, a reduction in husbandry and inputs will clearly have an impact on next year’s crop; in addition to the above reasons. Therefore the probability of a 65-70m bag crop is diminishing significantly.

November Certificates of Origin show a total of 1.4m bags set ready for shipment. At the time of writing, 1.2m bags of Arabica, 94,159 bags of Conillon and 139,215 bags of soluble coffee are set to be shipped in November 2019, totalling 1.438m bags. The Brazilian Real has traded a range of 4-4.20 to $1 since August, making coffee cheaper for importers. The Real has weakened by 7.56% against the USD at the time of writing, increasing the cost of inputs which in theory should keep the coffee flowing. With Vietnamese farmers holding back their coffee which is likely to cause high carry-over into next year, ceteris paribus. The flow of Conillon this year has, in theory, landed in the wrong locations for the market. There was 5,117 lots of coffee in London exchange warehouses, as of November 27th, this coffee is expensive to transport, and the differential is at level money.

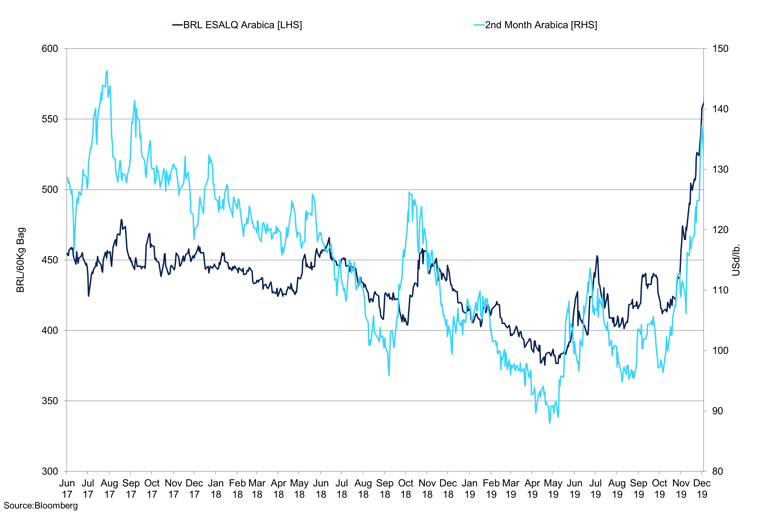

Brazil Local Price vs KC 2nd Month Continuation

Local Arabica prices have strengthened in recent weeks as exchange prices have rallied and the Real has weakened. The CEPEA ESALQ Arabica coffee price indicator has gained 37.8% YTD, and since our last report, the local price has gained 37.35% to 562.1 centavos/60kg bag, as of December 12th. The ESALQ type 6 prices for Cerrado Minas is marginally lower than the indicators at 554.5 as of December 12th. Conversely, type 7 Rio Cup Sul Monas is up 10.5% YTD to 378.27 centavos/60kg; the muted price action outlines the weaker demand for Rio Minas coffee. Differentials remain strong, suggesting physical demand is strong, inventories are drawing for Arabica as certified stocks and GCA stocks are falling. We don’t see a story fully developing unless GCA stocks fall to 5m bags. We maintain our view that the cheapest coffee in the market is certified coffee.

Vietnam

Weather in Vietnam hindered the harvest, due to poor weather but is only marginally behind last year’s figure through the same period. The recent rains and winds could damage the crop that has been harvested. Already picked coffee that is drying and then rained on increases the probability of OTA; we often get this threat, but in the last few years, it has not materialised. Some of the coffee that has been knocked off the trees may be picked up and dried along with the cherries that are picked from the trees. We maintain our view that the Vietnam crop will be 29m bags, local producers have held out for higher prices which they are getting now, but they were stopped out earlier on in the season which caused significant unrest. There is no doubt that there is strong demand for Vietnam coffee, especially from S.E. Asia and the differentials remain strong at $140/160 over for grade 2 Robusta. This helps the Vietnamese farmers achieve their goal of 35,000VND/60kg bag. Robusta prices in Dak Lak have averaged 32,904VND/kg in 2019 and prices are marginally above this level at 33,600VND/kg, at the time of writing.

Vietnam Exports

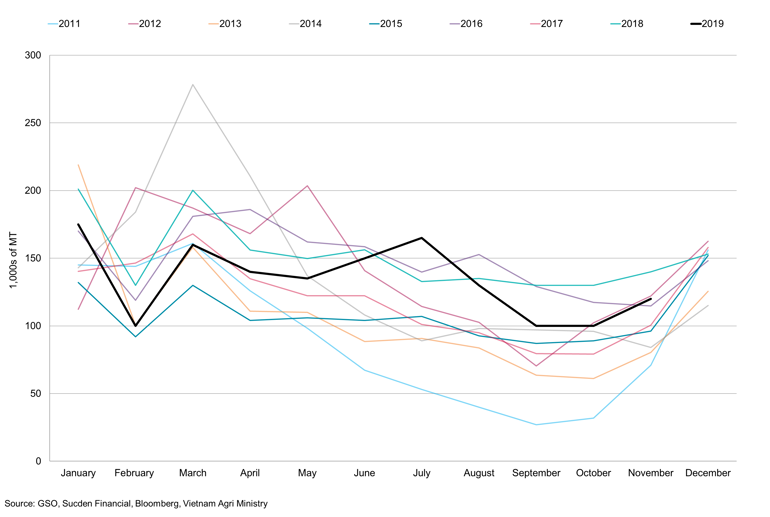

Despite this improvement in income, farmers still hold back product. Carry-over into the 19/20 crop was minimal as Vietnam shipped the old crop at the beginning of this year. We see Ho Chi Minh at 2,030k bags as of the end of November 2019; this is a year-on-year fall of 730,000. On a month-on-month basis, Ho Chi Minh inventories have increased by 375,000 bags, up 22.6% m/m. Our crop figure remains at 29m bags for Vietnam despite the recent wet weather as the majority of the coffee is still on the trees. We expect most of this coffee has already been hedged. With prices at current levels, there is no real incentive for farmers to produce more coffee.

With the Vietnamese farmers keeping their coffee close to their chests, exports have been weak in recent months. We do not expect a rebound in exports in the coming months. The 8-year average for exports in the final three months of the year is 111.9 tons vs an average for the preceding nine months at 130.35 tons. We do not expect a significant increase in exports as farmers continue to hold back coffee. Demand for Vietnam coffee is robust, and those roasters who cannot use Conillon coffee will likely have to pay up.

Colombian Local Prices

Colombia

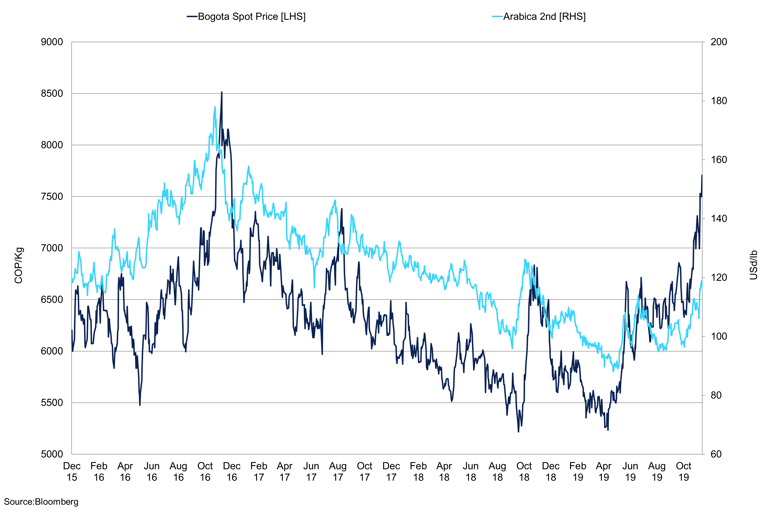

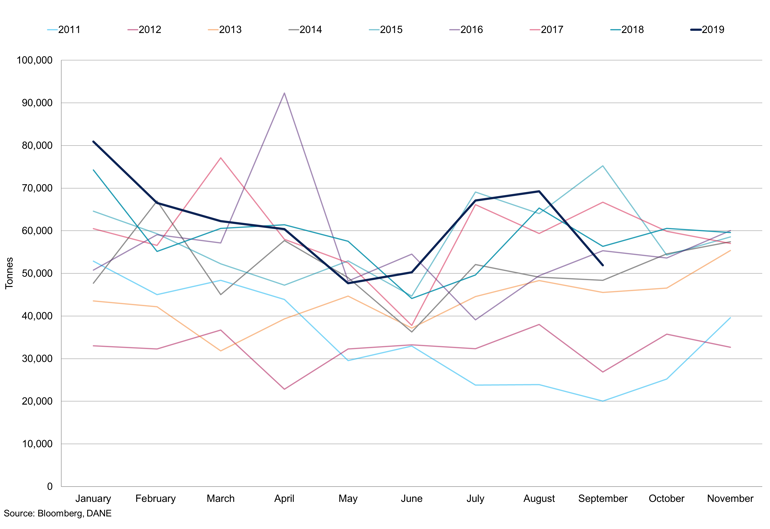

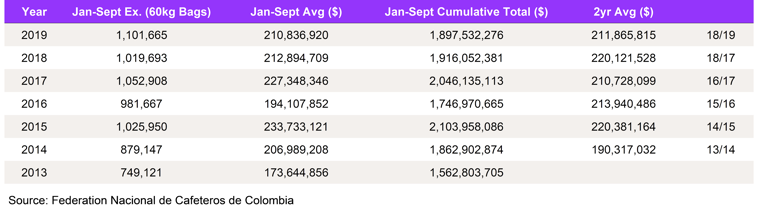

Data from the Colombian Coffee Confederation shows total exports at 9.90m bags from January to the end of August, the most recent data. This gives a monthly average of 1,101,665 60kg bags of coffee; an improvement 10% y/y. According to Colombian data, this year is expected to experience the largest export levels on record despite our S&D numbers suggesting that the 18/19 crop is flat on the 17/18 season of 14m bags. The 18/19 crop is also 800,000 bags lower than a production figure for the 2016/17 season. According to the ICO, U.S. Colombian Milds have averaged USd134.57/lb in 2019, as of December 5th, compared to 2018 when prices averaged USd140.31/lb to December 5th 2018. Intuition suggests that farmer’s income is lower for the19/20 season, and that may be true as input costs have increased due to the relentless strength of the greenback. However, a closer look at the provisional value of the exported coffee from Colombia outlines that over the first nine months of 2019, the average provisional value is $210,836,920 vs $212,894,709 in 2018. We attribute this to strong differentials, which, as of November 22nd 2019, were seen at +31. At the time of writing, differentials show little sign of letting up, and, as mentioned above, we see a deficit in fine cup Arabica suggesting we could see these differentials remain firm.

Since 2013, the average provisional value of Colombia coffee exports through the first nine months of the calendar year has only exceeded 2019s tally three times, and that was last year, 2017, and 2015 at $212,894,709, $227,348,346, and $233,773,120 respectively. The same applies to cumulative provisional value of coffee exports; through to the end of September the cumulative provisional value of Colombia coffee shipments have reached $1,897,532,276 with 2018, 2017 and 2015 at $1,916,052,381, $2,046,135,113 and $2,103,958,086.16 respectively. The two-year averages for the years 2013-2019 show that year average for the 2018 & 2019 is ranked 4th with 2014 & 2015 ranked 1st at $219,840,023, only $8.5m ahead. Spot prices in Colombia have firmed this year with Medellin gaining 43% through to December 4th 2019. The Colombian peso has weakened 6.81% YTD at the time of writing which increases the cost of inputs from fertilizer to transportation; from the beginning of 2018, the peso has weakened 17.7% as of December 2nd. While Colombia’s cost of production is one of the highest in the coffee market, we remember that Colombia’s President promised farmers $32m in subsidies and tree replacement aid. In Q1 2019, the government agreed on a subsidy of 30,000 pesos/125kg per shipment of coffee if prices fall below 715,000pesos/shipment. This, according to the coffee growers’ federation, only just covers production costs estimated at $240 per 125kgs. We firmly believe that farmers should be paid a proportionate share of the price of coffee, but the above analysis suggests that earnings over the last 18 months may not have been as bad as first thought on a historical basis. Clearly, the caveat is that farmers need to receive a fair proportion of these earnings.

Colombian Exports

The export market for washed Arabica has improved in recent years as consumption of high quality strengthens, playing into Colombia’s hands. The shift in receivers over the last couple of years of Colombian coffee is intriguing. Since 2013, there is one constant, which is that the EU imports most of Colombian coffee. YTD exports to the EU is the highest of the analysed period, and we would expect Colombian shipments to increase in this final quarter of 2019, as on average since 2013 for Q4 shipments have been higher than the previous three quarters. We do not see exponential growth in Europe’s coffee demand, but the drive for higher quality Arabica beans may support Colombian shipments. Indeed, Federation Nacional de Cafeteros de Colombia’s data outlines that Germany is in the top 5 for Colombian imports over the period analysed with imports rising from an average of 51,096 bags in 2013 to 95,769 bags in the first nine months of 2019. Indeed, total German imports through to the end of September 2018 of Colombian coffee were 768,809 bags, an average of 85,423 bags versus 861,925 bags for 2019.

Supply and Demand Numbers

Another mainstay is Japan which oscillates within the top 5; however, it is the Canada that is worth having a closer look at. Canada’s true value of imported coffee from Colombia was $197.58m, according to Statista; this figure is slightly different to the figure Federation Nacional de Cafeteros de Colombia have, which was $176,552,018 for 2018, YTD Canada have imports worth $131,319,891 of Colombian coffee. What we look to highlight is Canada’s increasing demand for Colombian coffee. In 2013, total imports reached 605,470 bags, averaging 50,456 bags a month. In 2019, average monthly shipments through to the end of September are 80,882 bags, and thus far, the exports to Canada have surpassed the total amount for 2013 at 658,629; 2018’s total was 928,591 bags with an average of 77,383 bags. Colombian coffee exports to Canada could surpass 1m bags for the first time. This helps accentuate that demand in Canada has strengthened in recent years.

We anticipate the Colombian crop to decline in the 19/20 crop year to 13.8m bags from 14m bags the year before. We attribute this to a drop off in inputs, reducing yields in coffee regions. Even though prices have been declining since 2017 and below the cost of production in Colombia for nearly two years, we do not believe farmers have decided to grow other crops. However, workers are more flexible, and if producers of other crops offer them a higher wage, they are more likely to favour a change. Indeed, having cleaned up its act, the Colombian economy is set to grow at 3.4%y/y in 2019, according to the IMF. Last year’s election provided a springboard for optimism and investment is starting to improve. The weakness in the peso is a concern, but the decline in government deficit provides hope. Such optimism makes big cities exciting and vibrant places for young citizens and is causing would-be farmers to migrate to urban areas. The Colombian peso has been dragged lower by uncertainty and political turmoil in the rest of Latin America, but if risk appetite returns, the peso could shine.

Commitment of Traders

Total open interest increased throughout October from 314,876 contracts to 374,646 as of October 25th. However, October is a tale of two halves, as we saw prices were falling to October 11th and we saw new shorts enter the market. We do not believe this was risk premia traders as the one year yield for KC is 10.55cts/lb. Following October 18th, we saw open interests increase in unison with prices. However, in November, total open interest has declined to 376,077 on November 5th, as investors covered their short positions on the news of more bullish fundamentals and news of a Brazilian exporter defaulting due to margin calls. When focusing on the March open interest, it has increased significantly in November from 80,125 contracts as of October 31st to 122,468 as of November 21st. This is to be expected as the December contract entered into FND, but total open interest is still falling, affirming the short-covering rally.

Arabica Managed Money Commitment of Traders

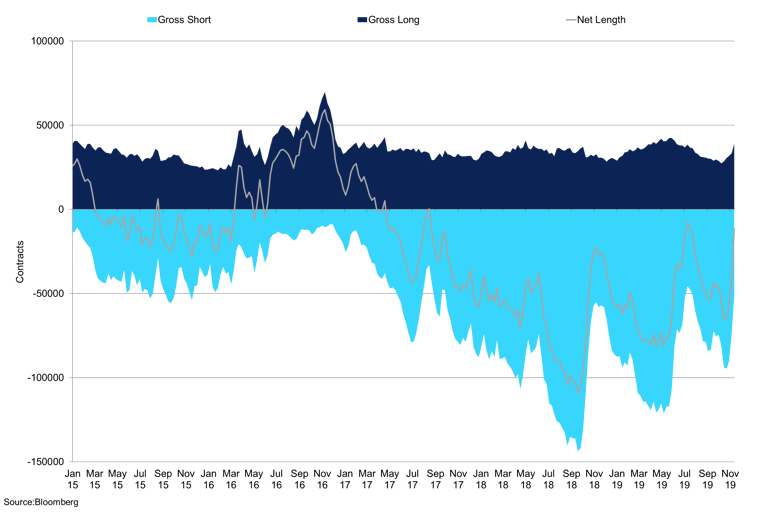

With CFTC data up to date, money managers for the KC contract increased their positions substantially, with the net position at -7,592 as of December 2nd from - 58,278 in on October 15th 2019. This is largely due to the contraction in the short positions, falling from 93,720 to 38,672 contacts in the same time period with longs only increasing from 43,094 contracts to 49,894 in the same period. We believe that the net position will move to a net long, but we could see a significant correction to the downside in the next 5-10cts/lb. The question is, how much do the funds want to buy? Given the market fundamental outlook outlined above, we expect the commitment of traders to move into a net long for the first time since 2017.

Commercials have increased their short positions to 177,816 as of December 2nd contracts from the beginning of September, outlining the strong producer selling that we have seen. We attribute this to the favourable BRL levels on a forward basis, however, for buyers at this level, the risk reward is not in their favour. Roasters still have more room to increase their shorts, after recording 182,000 short contracts in April 2019. The recent rally would have cost roasters who do not have enough cover; however, their margins have been very strong for the last few years, and historically, prices at 115 are still favourable for roasters.

Robusta Commercial/Producer Commitment of Traders

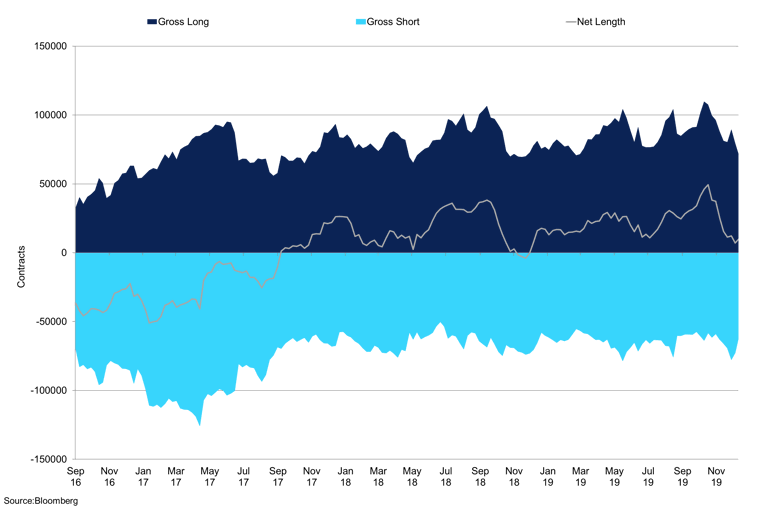

The Robusta producer/merchant disaggregated futures and options net position seesawed since our last report, with the net long peaking at 49,413 as of October 22nd, the first time since March 2016 that the net length was above 40,000. Since October 22nd, producers have reduced their net long to 11,304 contracts as of December 2nd. Taking a proxy that roasters are 80% of the gross long, we see them holding 64,355 contracts as of December 2nd. This could be attributed to significant gains made in the DF contract, with prices rallying 18% in the same time period. The managed money net positions followed a similar trend, as managers covered their short positions, causing a net short of 17,423. We believe that there is much more to cover given the prices continue their upward momentum. The Robusta producer/merchant disaggregated futures and options net position seesawed since our last report, with the net long peaking at 49,413 as of October 22nd, the first time since March 2016 that the net length was above 40,000. Since October 22nd, producers have reduced their net long to 11,304 contracts as of December 2nd. Taking a proxy that roasters are 80% of the gross long, we see them holding 64,355 contracts as of December 2nd. This could be attributed to significant gains made in the DF contract, with prices rallying 18% in the same time period. The managed money net positions followed a similar trend, as managers covered their short positions, causing a net short of 17,423. We believe that there is much more to cover given the prices continue their upward momentum.

Inventories

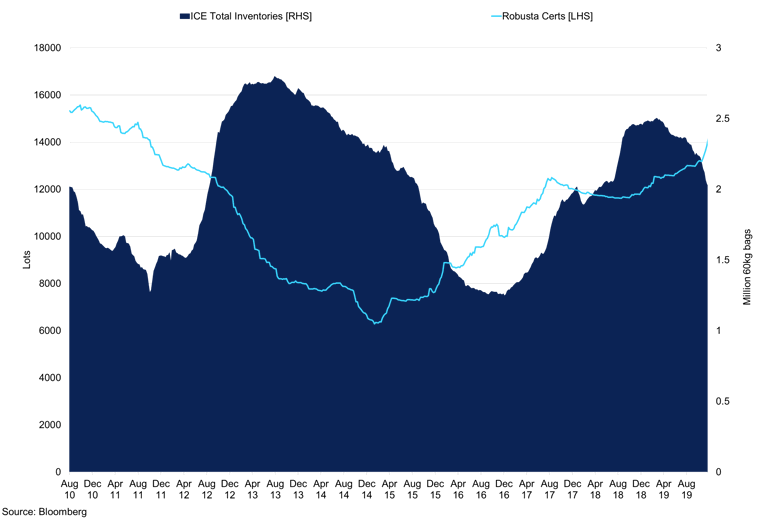

Since the beginning of August, we have seen Robusta certified stocks increase by 6.57%, 959 lots which equate to 159,826 bags of coffee. The majority of these increases are seen in Antwerp where inventories have reached 7,785 lots as of November 26th 2019. This could be attributed to Vietnam holding back their crop and strong differentials making certified stocks the best-valued coffee. Conillon shipments have slowed as outlined below but the favourable exchange rate at R$4.2642 per $ making Conillon cheaper for importers, however, few companies are able to blend the Brazilian derivative of Robusta. However, if the real continues to weaken and Robusta prices suffer, we could see a Conillon shipments increase, putting downward pressure on the flat price and keeping London spreads wide, favouring those who are carrying coffee.

Exchange Inventories

Arabica inventories have declined by 8.78% to 2,148,922 since August 2019, this equates to 793,000 bags of coffee. In our last report, we indicated certified stocks will start to draw, and we maintain this view as the downward revisions to C.America crops and also the expectation of a weaker Arabica crop next year. We believe certified coffee is the cheapest coffee due to strong differentials which show little sign easing up. November has seen outflows speed up, with a 5.6% decline to 2.14m bags as of November 26th.

Consumer stocks may have turned a corner, YTD Green Coffee Association stocks are up 17.04%. However, GCA inventories have fallen from the September high of 7.352m bags to 7.178m bags as of October 31st 2019. Since August, the market GCA inventories are marginally down. Clearly, further drawdowns will indicate stronger fundamentals; however, we do not expect significant prices responses when GCA stocks are at current levels as total consumer stocks remain elevated. If inventories continue to draw and GCA stocks reach 5m bags, then we have a story.

Appendix

Brazil Coffee Exports Calendar Year

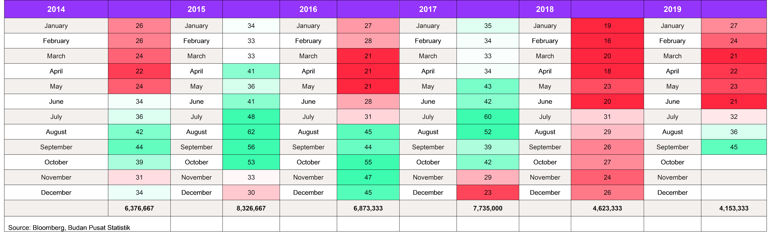

Vietnam Coffee Exports Calendar Year (tonnes)

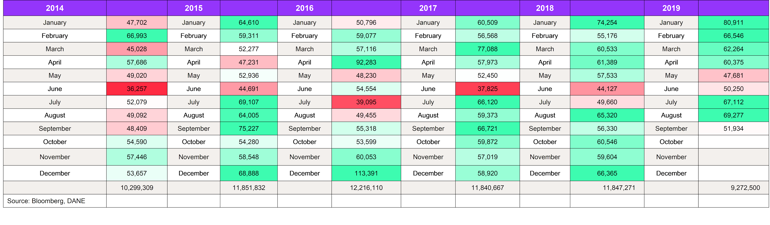

Indonesia Coffee Exports Calendar Year (tonnes)

Colombia Coffee Exports Calendar Year (tonnes)

Global Coffee Supply 2019/20

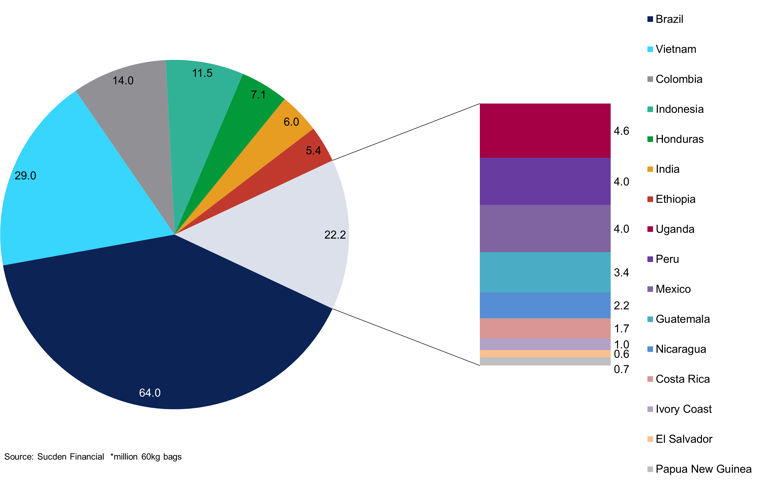

Global Coffee Supply 2018/19

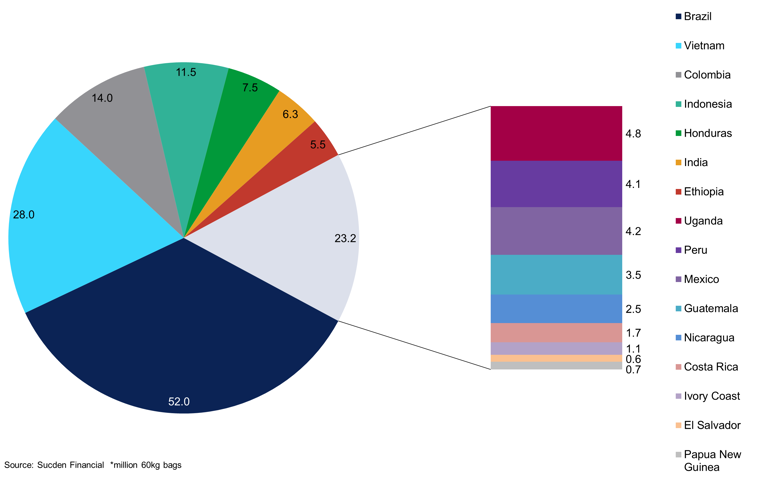

Global Coffee Supply 2017/18

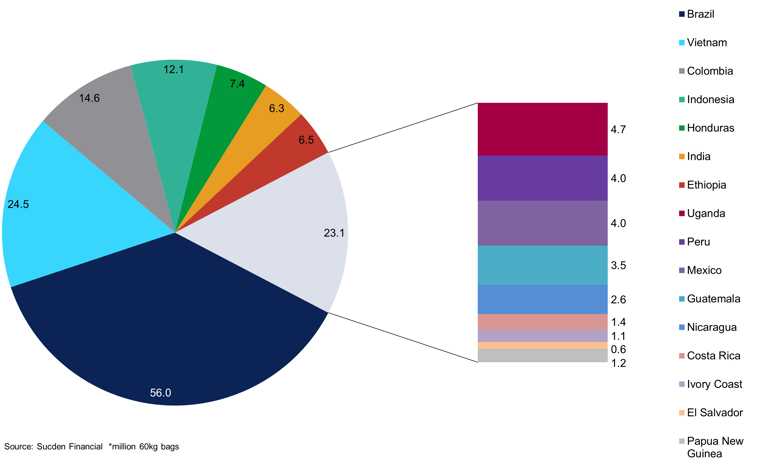

Global Coffee Supply 2016/17

Global Coffee Supply 2015/16