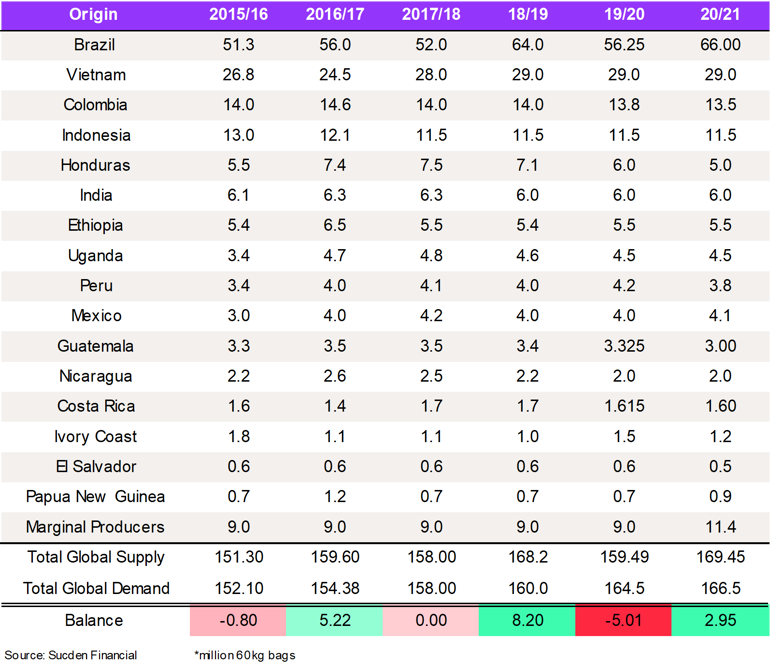

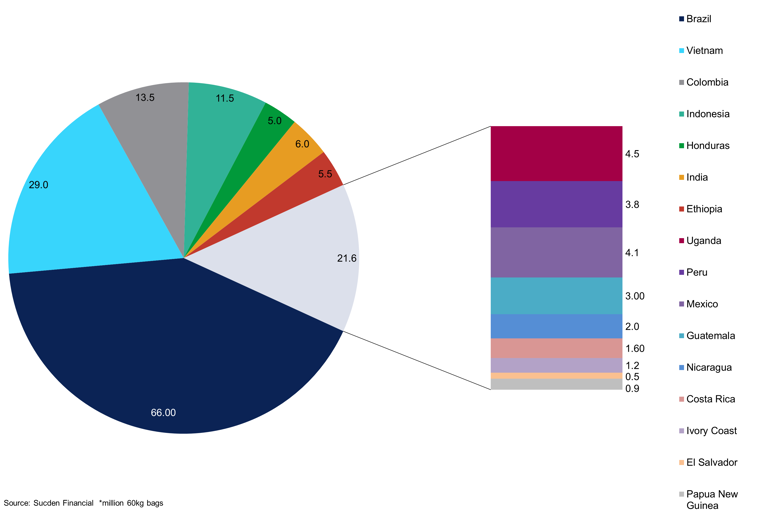

Our final balance for the 2019/20 season showed a 5.5m bag deficit, the 0.5m bag increase is due to a reduction in our Honduras number. For the 2020/21 season, we have a provisional surplus of 2.9m bags. We know there are 1.5m bags of Honduran coffee in certified stock in Antwerp which will not fill the void left of the reduction in the Honduran production over the next 3 years. Our global consumption figure forecast for the 20/21 season has increased to 166.5m bags. In previous years, we have seen our consumption figure relatively conservative to other forecasts. This remains the case for the 20/21, but year-on-year demand growth estimates have moderated. Consumption growth from 19/20 to 20/21 is 1.45%. We see steady demand growth in the U.S. and continued improvement to consumption in S.E.Asia.

Executive Summary

- While the number of cases in China seems to be tailing off, countries such as Europe and the US begin to face the consequences of economic disruption

- Consumers are staying at home, businesses struggle despite injected liquidity, and bond yield spreads widened causing markets to rattle

- The biggest impact will be mostly felt in the US, where the number of cases is growing at an unprecedented rate and the labour force is showing signs of weakness in the economy

- Helicopter money from the U.S. government is unlikely to promote consumer expenditure as uncertainty is very high and they are unsure how long the lockdown will go on for, increasing the saving percentage

- We do not envisage differentials softening in the near term due to consistent demand

- We could see the Brazilian harvest delayed due to lack of labour, reducing the Arabica surplus

- Lockdown at origins, such as Colombia, Brazil, Peru, and C.American countries will delay shipments to consumer destinations due to port queues, labour and or container shortages

- Local prices in Brazil are at record levels, the gross short in the Commitment of Traders’ shows how far forward producers are sold

- A rally towards 135-140cts/lb could see some exporters who hedged at lower prices may be stopped out causing further trouble

- Demand destruction due to the coronavirus depends largely on the ratios of at-home consumption to out of home consumption

- At-home consumption is significantly higher, we have seen at home consumption spike due to panic buying helping to offset the drastic fall in out of home consumption

- Finished products stocks are low at roasters as they work tirelessly to replenish supermarket shelves

- It is clear the revenue split favours out of home consumption, and we expect to see significant losses for multi-national cooperation’s.

- Brazil’s economy is falling further into recession; low saving rates in the economy mean little demand for coffee as it isn’t an essential food item, even if the government give $120 to those most in need

- For the 2020/21 season, we have a surplus of 2.95m bags, consistent with previous reports we see the deficit in washed Arabica coffee

- Exports from Colombia are 9% higher y/y for January and February 2020 according to the FNC, but we expect this to fall due to logistical constraints and will roasters be able to find a substitute?

- The impact on the 2020/21 crop will be significant as the lack of labour on farmers will delay the Mitaca crop. Our crop estimate for 2020/21 is 13.5m bags

- C. America continues to be problematic, and we expect the Honduran crop to be 5m bags for 2020/21, we do not see Honduras increasing their crops to 7m bags in the next few seasons

- We have been saying for a while that certified stocks are the cheapest coffee around, we expect demand for Arabica inventories to increase due to uncertainty about deliveries at consumer destinations

- Conillons are now at tenderable parity, and this could improve the flow of Robusta coffee if the product can get out of Brazil

- Dry weather in Vietnam is becoming a worry, and this could cause downside to our crop number and trigger a rally in London

- We now look to the next Brazilian off-cycle, we believe stocks will fall to 900,000 bags by year-end, but if the off-cycle is particularly low, there will be little coffee available to re-stock

- 1.5m bags of Honduran coffee in Antwerp will be withdrawn but the issues in Honduras in the coming seasons will mean little replacement, keeping diffs firm

Market Activity & Trade Ideas

- Systematic funds have reduced their involvement in the market due to the volatility

- The tightening of the spreads shows that the market is acknowledging the tightness down the curve

- We think arabica spreads will move back to a premium, meaning that the trade cannot carry coffee if the spreads remain at premium funds could get a return on holding a long position

- Optionality is expensive, and this reduces the dynamism of traders, with inability hedge gamma

- The arbitrage is high levels, and the risk-reward for Robusta does not favour the downside.

- The London market looks good value, and we think buying a July $1,300/t call at $45 premium is a good trade in terms of risk-reward given the weather issues in Vietnam

- Buying the arb between 55-60 but we think the chance of rally in London is increasing

- We favour deferring a long position in Arabica down the curve, to help mitigate the volatile swings in the nearby contracts

- The reaffirmation of support at the 200-day MA in the front-month contract should give the market strength, and we continue to favour buying dips

Sucden Financial Coffee Balance Sheet

Macro Overview

China

The Chinese economy has been hit particularly hard by the spread of the coronavirus in Q1 2020. While first cases were registered well in December 2019, the true shock to the nation came in January, when the number of cases doubled every two days. Since then, many developed economies such as Europe, the U.S. and South Korea are in lockdown, and most global travel has been suspended to prevent the spread. The number of cases and deaths in China are seen to be tailing off, but other countries are just starting to face the impact of the virus on public health and safety. This pandemic has forced governments and central banks hands, prompting policies that protect the financial industry. According to the World Health Organisation (WHO), the economic impact of SARS was $40bn. We believe that the impact of coronavirus will be much larger, given the sheer size of the Chinese economy today, and the spread of the virus worldwide.

China 10 Year Yield vs CPI vs GDP

We believe that the Chinese economy will continue to suffer the impacts of the virus throughout 2020.

The small and medium-sized enterprises (SMEs) contribute significantly to the nation's growth. They employ 233m workers and generate more than 2/3rds of the revenue of all business enterprises, accounting for 60% of China's GDP. The impact of the virus has especially affected those companies, not only due to reduced investment participation but the sheer size of the migrant labour force that is yet to be let back into mainland China. As of February, 2/3rds of migrant workers have not returned to work although the return-to-work ratio is seen picking up from around 30% by late February. These companies are especially vulnerable to supply-chain disruptions, and no recovery is expected in the next a couple of months, and we expect this sector to take the hit.

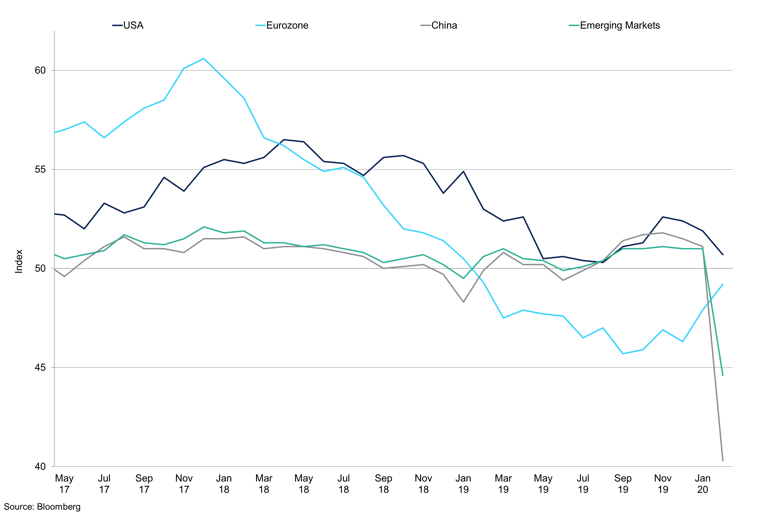

Chinese Caixin manufacturing PMI rebounded sharply from 40.3 in February to 50.1 in March, returning to expansionary territory. Export orders rebounded to 46.4% m/m, demonstrating almost a V-shape recovery in the manufacturing industry. We attribute this to the ease of mandatory quarantines enabling an adequate supply of labour as factories reopen.

Airfreight shipping rates have soared as factories restart production in China, complicating efforts to get their Asian supply chains moving again. All the previous contract prices and discounts have been cancelled, and an urge to ship out of the delayed stock has caused the rates to pick up. At the same time, cargo flights remain limited in and out of China. We believe that once passenger flights are rescheduled, then the situation would go back to normal.

In March, new fiscal relief policies were introduced, starting from a waiver of some fees and taxes for travel agencies to an RMB500bn rise in quotas for special loans to SMEs. The latter was an addition to the increase of RMB300bn in early February. China's CB has also cut its benchmark interest rate by 10bps in an effort to offset the negative economic consequences of the pandemic. Additionally, new bond quotas for new for local authorities as well as $140bn worth of credit to small lenders should prop up the economy. While the US and European stimulus measures included handouts to households and individuals, China has instead focused on credit provision to banks and local governments.

Europe

The virus has been particularly ruthless in Italy, where country-wide quarantine has been implemented; however, no permanent border controls have been applied by the EU council to stop the spread within the bloc. We expect Italian GDP in Q1 2020 to suffer significantly, especially after already weak growth in Q4 2019.

In Q4 2019, Eurozone barely grew, up only 0.1% q/q, the slowest rate of growth since 2013. In 2020, the Euro-area looks to be headed for its first recession in 11 years as the coronavirus reshapes businesses and consumer confidence. The manufacturing PMI showed signs of industry weakness as it fell from 49.2 in February to 44.5 in March, a 92-month low. In the medium-term, however, we expect both services and manufacturing PMI data to see some signs of recovery, especially as China starts to emerge from the crisis.

Manufacturing PMIs

While China and emerging markets manufacturing sectors deteriorated to record low, the US and the EU still have more room for the downside.

ECB left the deposit rate unchanged at historic lows of -0.500% and kept its marginal lending facility at 0.25% opting not to follow the Fed and BoE decisions. Instead, the ECB shook off limits on its new expanded asset purchase program worth €750bn to cushion the economic fallout from the coronavirus pandemic. It also said it would offer new loans to banks and offer liquidity facilities at more favourable rates.

In Germany, household spending fell as well as business investment; exports also experienced a decline. However, construction activity offset weakness in other indicators, and Germany GDP was flat q/q. We expect significant implications from subdued exports to China, but the weaker euro and low oil prices should support the oil-consuming and export-dependent economy, at least in the medium term.

Germany has already promised to spend billions to cushion the economy. The economic package worth $800bn will set no limit on the credit for the companies. This is an addition to a promised $650bn rescue fund to provide companies affected with loans. The discrepancies between Germany and the bloc about the implementation of fiscal measures have always been a caveat to Eurozone economic recovery, however, now, with countries acting in unison to support the economy, we expect to see a U-shaped recovery once the number of cases starts to subside.

US

The US economy has been hit particularly hard in Q1 2020. Equity prices, bond yields, and oil prices have plummeted in the final weeks of February. The yields on the US 10-year bond fell to a record low of 0.54%. The price of WTI fell to $20.09/brl. The manufacturing IHS PMI index declined from 50.8 to 48.5 in March, while broad services declined sharply from 49.4 to 39.8, indicating the impact being mostly felt by the service sector.

Meanwhile, the decline in the US bond yields reflects investors' reaction to multiple emergency Fed rate cuts, by 50bps and 100bps respectively. While the moves were intended to support the economy, we believe that the disruption of supply chains, lower tourism levels as well as subdued external and domestic demand that will continue to keep the growth subdued.

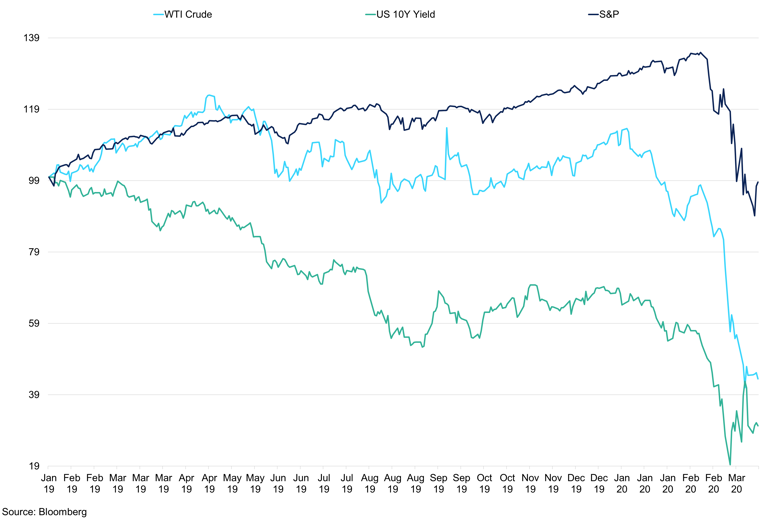

WTI Crude vs US 10 Year Yield vs S&P

After a massive sell-off in February, we see a slight recovery in the medium-term on the back of the US emergency stimulus.

At the beginning of 2020, the underlying economic indicators show signs of weakness to the outside shocks; however, we expect to see a more pronounced decline in the medium-term. February retail sales fell by 0.5% m/m. Industrial production remained weak, down 0.3% m/m and 0.8% y/y. Production of capital goods was particularly hit, as it fell sharply by 2.6% m/m. in January. In the medium-term, we would expect to see a spike in consumer spending as there has been a surge in shopping for household essentials.

Brent crude plunged more than 65%, while bonds surged, sending the entire Treasury yield curve below 1% for the first time in history. The Fed has cut interest rates twice in March and boosted the size of the week's overnight and term purchase operations to help add liquidity to the markets. After announcing the state of emergency, additional measures came through to support the economy. As the economy continues to struggle, the Fed first launched a $700b worth of quantitative easing programme to curb borrowing costs. Later, the level was set to an unlimited bond-buying. Additionally, Congress approved an $8.3bn spending package to provide extra funding to healthcare agencies. Another relief package worth $2tr, the biggest rescue deal on record, has been released to curb the pandemic’s toll. We do not expect this to improve spending at this time as consumers are scared and are unlikely to spend.

Origin Focus

Brazil

The tense political environment, lack of progress on reforms, subdued growth, and challenges facing the central bank as investors turn away from nation's fixed market and currency set the scene for risks to remain to the downside in 2020.

Goldman Sachs slashed Brazil 2020 economic forecast to 1.5%, well below the targeted 2% threshold. Brazil's government, however, remains more optimistic for the year ahead as it slashed its growth forecast to 2.1% from 2.4% growth in 2019. In 2019, industrial output and services were positive; however, they were unable to offset business investment, which saw the biggest drop in 3 years. Private consumption growth slowed to 0.5% from 0.7% in Q3. This confirms that even before the outbreak of the virus, economic indicators were muted, and we would expect this to reflect negatively on Q1 performance.

Brazil is likely to feel a significant negative impact from the economic slowdown in China, given that 27.6% of its exports go to that single market. As of April 6th, the number of cases in Brazil is rising pretty sharply, to 11,130 from 4,630 just a week ago. El Salvador was one of the first countries in Central America to declare a 21-day quarantine. Now, countries, including Brazil, Argentina, and Colombia have imposed similar measures to slow the spread of the virus.

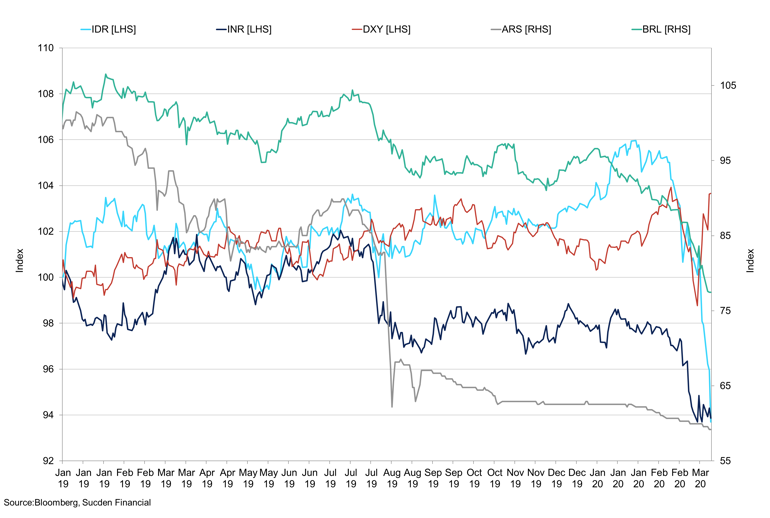

Emerging Market Currencies

Brazilian Real suffered the biggest losses in 2020 in comparison to other emerging market currencies.

From the monetary policy perspective, the US Federal Reserve's emergency rate cuts highlighted the economic damage to the Brazilian economy. A combination of the Fed cut along with coronavirus and oil price wars sent IBOVESPA tumbling 45% since the beginning of March, reaching the lows last seen in June 2017. Indicating the scale of investor's risk aversion, the 10-year yields sky-rocketed 45% in the same period. To support the faltering economy, the central bank cut Selic rate down to 3.75% on March 18th, a record low. In its statement, the CB said the blow to the Brazilian economy will be mostly felt through supply chains, inflation, and demand-side. Additional $10bn scheme launched on April 1st should allow companies affected to reduce salaries and hours, or temporarily suspend contracts, to preserve employment. To protect the currency, we believe that the CB will come in with a currency intervention to support the real. The effectiveness of such intervention, however, remains limited when looking at the market response to the previous attempts.

Indeed, the real continued its decline despite the BCB's announcement to conduct an intervention in the FX market, by selling swaps valued at $1b. The real has declined 25% YTD as record low rates diminish its carry appeal and as disappointing economic data cast doubt on Brazil's recovery. As of April 6th, the BRL is a 5.35 to the dollar.

Vietnam

The Vietnamese market, along with other Southeast Asian economies, faced an unexpected crisis due to the COVID-19 pandemic, reflected in Vietnam Ho Chi Minh Index losing 23.3% since the beginning of February. Faltering manufacturing sector, along with restrictions on travel and tourism, negatively impacted the nation's growth forecasts for Q1 2020. According to government advisers, the virus could cause Vietnam's GDP growth rate to drop around 1% for 2020, a more conservative forecast, and those industries that depend on exports to China would be the first to feel the impact. The analysts believe that the nation's GDP growth rate target should be lowered to 5.9-6.0% despite the government's refusal to do so.

Vietnam's CPI fell from 5.4% to 4.8% y/y in March. Exports, however, jumped 34% y/y in February as Samsung boosted shipments of phones. Imports rose 26% y/y, with shipments from the US surging 13.6% m/m. The manufacturing PMI, however, declined to 41.9 in March from 49.0 a month prior. This is the first time the nation's manufacturing performance fell into the contractionary territory since 2017.

Despite China seeing signs of economic recovery, the Vietnamese trade sector is seen declining in the medium-term, especially as $10bn worth of exports come from China, its largest trading partner. To combat that, Vietnam has eased its restrictions on trade with China. Custom clearance should take some time to ensure safety; however, we would expect cross-border trade to accelerate between two countries. Additionally, there is potential for some Chinese companies to follow Samsung in moving their supply chains to Vietnam. This would attribute to a faster than expected recovery in Vietnam in Q2 2020.

To combat the impacts of the virus, the government offered a credit package worth $12.3b, and commercial banks have been told to reduce interest rates for firms directly impacted by the virus. Indeed, according to a Department of Private Economic Development survey, 60% of businesses would lose at least 50% of their revenue if no measures are undertaken. The State also has extended payment deadlines for taxes and fees to support businesses, including VAT, income tax, corporate tax and land rent. As of March 18th, Vietnam registered 67 cases and 0 deaths.

Indonesia

The momentum in Indonesia's economy ebbed in 2019, with growth edging down to 4.97% in Q4 2019, the lowest in three years. While we see slower growth in Q1 2020, it should remain stable throughout 2020. The nation's inflation remained subdued at 2.98% y/y in February, and the local currency declined by 16% since the beginning of February. Supply-chain disruption will put upward pressures on the prices; however, softer domestic demand should dissipate those pressures. While tourism and foreign investment will feel the pinch from the pandemic, Indonesia's manufacturing is less entangled in global supply chains and therefore should be less prone to external disruptions. However, while Indonesian manufacturing PMI remained the highest among other Asian economies in the first two months of 2020, however, it came to 45.3 in March. As of April 6th, Indonesia has 2,273 confirmed cases and 164 reported deaths.

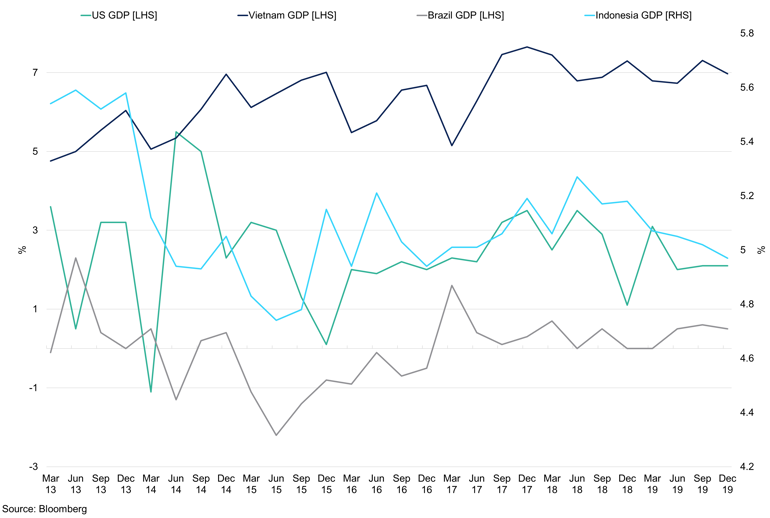

The US and Exporting Economies GDP Growth

Some exporting countries have already lost some of the strength in 2019 before the outbreak of the coronavirus.

Indonesia has committed to combating the impacts of the virus on the economy. The Bank Indonesia (BI) announced an $8.1bn stimulus package on March 13th covering the manufacturing sector and including a reduction in corporate and personal income tax. The stimulus, representing 0.8% of GDP, will exempt some workers in manufacturing from income tax and will give manufacturing companies a discount on corporate tax payment. Additionally, the central bank has been buying government bonds to help curb losses in the rupiah currency, as virus fears triggered a global market rout.

Last time the BI cut rates was in February, the fifth 25bps cut in its easing cycle. BI lowered its deposit facility rate to 4% and its lending facility rate to 5.5%. However, the central bank is under pressure again to cut as the Fed announced its second emergency rate cut in March. According to a Reuters poll, the Bank Indonesia is forecast to cut its key policy rate again to 4.50%. However, in a similar vein to Brazil, concerns about capital outflows and loss in rupiah would present some challenges to this decision. On the other hand, last year's election gave the government a mandate to accelerate reforms. This should make it easier to impose regulations to improve the business climate and attract foreign direct investment.

Corporate Earnings

Starbucks: 13-week quarter ending December 29th, 2019

Starbucks performed "very well" throughout the quarter and had one of the strongest holiday seasons in the history of the company. The growth was fuelled by comparable sales growth, new store development and continued expansion of Global Coffee Alliance with Nestle. Continued investment into beverage innovation and digital customer relationship continues to add value to sales growth.

In Q1, Starbucks delivered global revenue growth of 9%, led by strong net new store growth of 6% y/y. Due to partnerships with Nestle and Pepsi, channel development revenue grew 5% in Q1. The U.S. and China continued to be the key growth markets. The U.S. grew by 9% in Q1, where customer connection scores reached an all-time high in Q1. Sales of the extended line of Cold Brew and Cold Foam options, with seasonal drinks such as pumpkin and Irish cream flavours, have been performing well, especially in the U.S.

To combat the spread of the virus, Starbucks is removing seats from stores and shutting down busy locations in the U.S. and Canada for at least two weeks. Customers can still order at the counter and the drive-thru window, as well as through the Starbucks app. The company will provide "catastrophe pay" for those employees that were diagnosed with the virus.

China grew by 15%, fuelled by a 16% increase in net new stores. Starbuck's research shows that the brand remains the top choice for away-from-home coffee for Chinese customers. In Q1, sales from China's mobile orders jumped to 15% of total revenue, up from 10% in the previous quarter. The continued growth of China's rewards members supported sales, as they reached 10.2 million customers in Q1, 40% y/y growth. In the U.S., this number reached 18.9m, with 16% y/y growth.

In China, sales are getting back to normal after a steep fall. According to Starbuck’s statement, sales in China will fall by about 50% in Q2 2020, and China's revenues this quarter could be hit by $430m. Starbucks closed about 80% of its 4,300 locations in China in early February; however, store operating rate will reach about 95% by the end of the quarter, according to company statements.

Luckin Coffee

In just two and a half years since its launch, Luckin Coffee outpaced Starbucks in China's store count, reflecting the chain's shift in focus to remote areas. Luckin is currently operating 4,500 stores in 53 Chinese cities, with 90% of locations being delivery stores rather than casual coffee shops. Its location placing strategy depends heavily on the location of consumers that have downloaded the app, whereas Starbucks is based on chain location and 'feel at home' atmosphere. As of Q3 2019, Luckin's store growth was more than 200% y/y, and its customer base grew by 413%, with the number of returning customers rising by 398%. The number of stores tripled in 2019, from 1,189 to 3,680 as of October. By the end of 2021, it has plans to reach 10,000 stores.

Luckin shares plummeted by 83% in April on the back of investigation finding Luckin fabricating transactions totalling $310m from second to last quarter of 2019. In their financial result, the company would state growth in net revenues of over 500% y/y, mainly coming from a growing number of online customers. At the beginning of February 2020, the company successfully disputed similar allegations, stating the impact of the virus as not "significant". As a result, Louis Dreyfus, a crop trading giant, could face collateral damage from the scandal, as it invested about $50m in the company in 2019. Starbucks stocks declined by 47% since the virus outbreak.

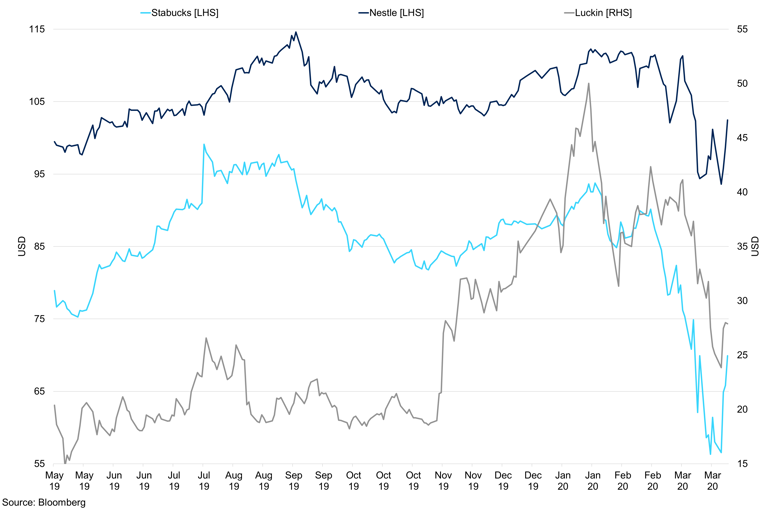

Coffee Companies Share Prices

Luckin Coffee suffers larger share losses than Starbucks amid allegations on fabricating sales figures.

With present concerns about social distancing, Luckin could face bigger losses than its rival, Starbucks, despite Luckin's convenient 'coffee to-go' strategy. The additional burden of a heavily discounted model and stagnating number of online users could add to already-existing virus pressures. China is not a coffee-drinking country, and while Luckin has been targeting younger generations to market their product, the demand remains low.

Nestle

In 2019, Nestle experienced organic growth of 3.5%, with strong momentum coming from the US and Brazil, as well as improving momentum from Western Europe. Profitability improved, and the company reached the guided range one year ahead of the plan. According to Nestlé’s statement, the Greater China region is its second-largest market, representing about 8% of global sales. However, as of now, there were no mentions of the potential impact of the spread of the virus could have on company earnings.

In their annual statement, coffee had momentum, supported by strong demand for Starbucks products, generating more than $313m in incremental sales in 2019. The beverages category saw "high single-digit" growth helped by strong demand for Starbucks, Coffee mate and Nescafe products. China showed "slightly positive growth", with some benefit coming from the Q4 stock up ahead of the Chinese New Year. With more people staying at home in the US and Europe, we estimate that the soluble coffee sales will experience a spike, whereas roasted coffee sales to coffee shops will slow down.

SFL Global Coffee Balance Sheet

Our balance sheet shows a 2.95m bags surplus for 20/21 going into an off-cycle in 21/22.

Supply and Demand

Our final balance for the 2019/20 season showed a 5.5m bag deficit, the 0.5m bag increase is due to a reduction in our Honduras number. For the 2020/21 season, we have a provisional surplus of 2.95m bags. The deficit will be in washed Arabica, and in our opinion, the deficit could amount to 2m bags; keeping the differentials firm, especially given significant troubles in Central America. We know there are 1.5m bags of Honduran coffee in certified stock in Antwerp which will not fill the void left of the reduction in the Honduran production over the next 3 years. Differentials for Honduras are at +28 at the time of writing, but there are no offers, we do not believe you can get Honduras coffee in meaningful size until the new crop.

Our global consumption figure forecast for the 20/21 season has increased to 166.5m bags. Previous years, we have seen our consumption figure relatively conservative to other forecasts. This remains the case for the 20/21, but year-on-year demand growth estimates have moderated. Consumption growth from 19/20 to 20/21 is 1.45%. We see steady demand growth in the U.S. and continued improvement to consumption in S.E.Asia.

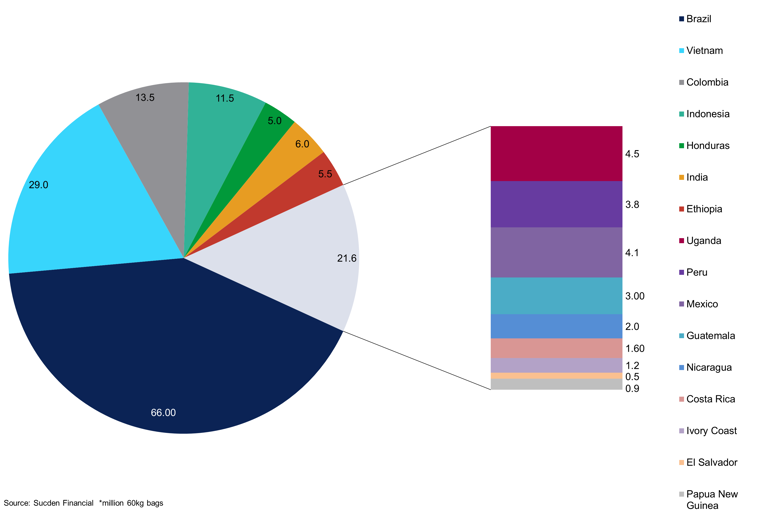

Global Coffee Supply 2020/21

Central American crop has declined, and we see the deficit in Washed Arabica.

Origin consumption has improved but it is very tricky to keep track of on-farm consumption. This is expected to change slightly in accordance with production. Brazilian consumption has remained relatively steady around 21.5m bags in recent years. Indeed, Vietnamese demand is a smaller percentage of total production at 2m bags. Indonesian demand remains strong, pushing towards 7m bags, and we note that we believe Chinese demand is close to 5m bags. There is significant upside to Chinese demand, and we expect this will have a considerable impact on the global balance sheet. This is dependent on what type of coffee China consumes, whether it is soluble, 3 in 1 or Roast & Ground. In our opinion, China has no preference for coffee type between Robusta and Arabica.

Consumption Outlook

COVID-19 Impact

Clearly, the virus has had a huge impact on the global economy and supply-chains. The impact on supply is tricky to show at this time. Labour force constraints will likely impact the harvest period at various origin; however, we expect this to be the case in Central America anyway. The impact on supply-side disruptions will delay the flow of coffee to consumer destinations; the closure of ports will aid the recovery of prices as traders target stocks. These challenging times are obviously testing, and Garrett Hardin’s theory on ‘The Tragedy of the Commons’ comes to mind, as an explanation of recent consumer behaviour. As civilians self-isolate and coffee shops close their doors, this will impact out of home consumption. However, consumer behaviour has shown that demand for soluble, roast & ground and pod coffee has surged to increase stockpiles. Below we try to give some colour to consumption in countries in Europe and the U.S.

The United States & Canada

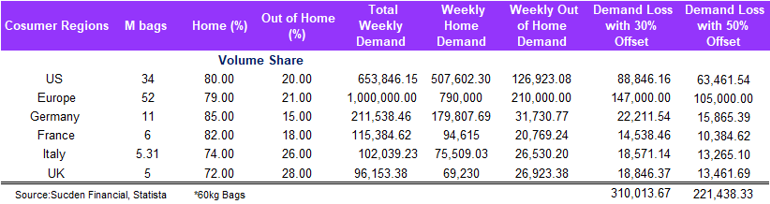

According, Statista the average revenue per person in the coffee market in the U.S. will amount to $260.44 in 2020; this is expected to rise to $269.43m in 2021. The key to the impact on demand is in understanding where the majority of consumption takes place. Out of home consumption creates the highest revenue; 88% of total revenue vs 12% for in-home consumption. The average revenue per capita is $260.44bn for the US, but revenue for the market as a whole is $86,207m.

Statista data suggests that 80% of America & Canada coffee demand is at home. Using our total consumption figure of 34m bags, we see weekly demand at 653,846 bags and the vast majority of that, 507,602.3 bags, is consumed at home. Accordingly, weekly out of home consumption is 126,923 bags. Statista shows that per capita 3.5kg of roasted coffee per year in the U.S. compared to 0.3kg per capita per year for instant coffee. The balance of this is expected to change if 30% of out of home consumption is offset by the increase in at home demand. This would mean 38,076 bags of offset consumption, a loss of demand of 88,847 per week in the United States. Judging by our conversations and consumer observations, we think 30% is too low and at the time of writing 50% is more likely, a loss of demand for 63,461 bags in the U.S.

Europe

In our opinion, the bloc’s demand is 52m bags as a total, however, certain countries are more impacted than others. The region’s, weekly demand is 961,538.46 bags with out of home and home consumption at 759,615 and 201,923 bags, respectively. Again, due to stockpiling, we do not see a total loss of demand of 201,923 bags, the worst-case scenario at the time of writing is 50% of out of home consumption (100,961.5 bags). The largest revenue sector within the coffee market is roasted coffee at $112,091m in 2020, with the coffee market $136,094m in 2020.

Germany

German consumption is 11m bags a year, weekly demand is 211,538.46 bags. The country's demand construction highlights that 85% of demand is at home, with only 15% taking place in coffee shops, restaurants and bars. German consumption considerably favours of roasted coffee, per capita consumption is 4.7kg per year in comparison to 0.9kg for instant coffee. According to Statista, revenue for roasted coffee in 2020 is $19,615m, and per capita revenue is $269.71. Out of home revenue is 75% of the market revenue. Total out of home demand is 31,730.77 bags, using our 50% estimate for the extra at home consumption offset this would leave a demand loss of 15,865 bags. The caveat is that Germany is not yet in lockdown, and this assumes the virus is equally spread.

France

At the time of writing, France has announced a nationwide lockdown of 15 days. Using the same model, and 6m bags of yearly consumption, total weekly demand is 115, 384 bags. The at home and out of home consumption is vastly skewed in favour of at-home consumption. 18% of demand is out of home; we believe that in worst-case France would lose demand of 20,769.24 bags (the lockdown is 2 weeks long, and our base case is for 50% of demand to be offset by stockpiling). On a per-capita basis, roasted coffee in France is 3kg compared to 0.5kg of instant coffee, according to Statista roast per capita consumption has fallen from 4kg in 2014. The coffee market revenue for 2020 is $13,237m, 84% in favour of the out of home segment.

Italy

Italian demand is 5.31m bags, with home consumption at 74% compared to 26% for out of home demand. Originally, we calculated that the worst-case demand loss for Italy was 18,826 bags, assuming there was no stockpiling. We now know this not to be true. This was calculated by taking a % of the total Italian population of the originally infected areas, which is 60% of the total Italian population. Now the whole country is in lockdown, the worst-case scenario is 26,530.20 bags. We know that stockpiling has offset the loss of out of home consumption; using 30% and 50% total demand offset can vary from 7,959 bags to 13,265 bags; in our opinion, 50% offset is more likely. Like Germany, Italy’s per capita consumption is significantly in favour of roasted coffee, 5kg compared to 0.31kg instant.

Impact of COVID-19 on Demand

Estimates to demand loss during the global lockdown hinge on-at-home consumption.

Total Impact

Using our base case of a large spike in at-home consumption offsetting 50% of the decline in restaurant and bars consumption, we see a demand loss of 217,400 bags per week in major regions. Shelves are permanently empty, and we expect roaster inventory of finished products to be low. Any finished product will likely be shipped straight out to supermarkets. Logistics are starting to slow, and this will cause delays to containers finding their way to consumer destinations. Once household inventories have been drawn down there will be a steady stream of coffee consumption. The rise in coffee demand purchased in supermarkets will prompt a reduction of finished product consumption when isolations and regional lockdowns are over if the household still has inventory. A greater threat is also becoming a loss in supply due to worker illnesses and price action. With the KC KN spread switching from a premium to -1.50cts/lb due to the roll; hedges below the current flat price, a large rally would cause producers and exporters to go liquidation.

Supply Outlook

Brazil

Our Brazil number for 19/20 stays at 56.25m bags, with the split 38.25m bags for Arabica and 18m bags for Robusta. We have seen the reduction in crop size play out in Brazil’s exports; however, the reduction in Conillon exports is due to other factors as the crop size is largely the same for the 2018/19 season and the 2019/20 season. Brazil’s domestic consumption is at 21.5m bags and, the on-farm consumption is very tricky to predict. The Brazilians consume lower quality Conillon and the reduction in shipments could benefit Brazilian demand. However, economic woes and Brazil's propensity to stockpile coffee, in conjunction with a favourable local price due to the weak Real may curtail domestic consumption somewhat.

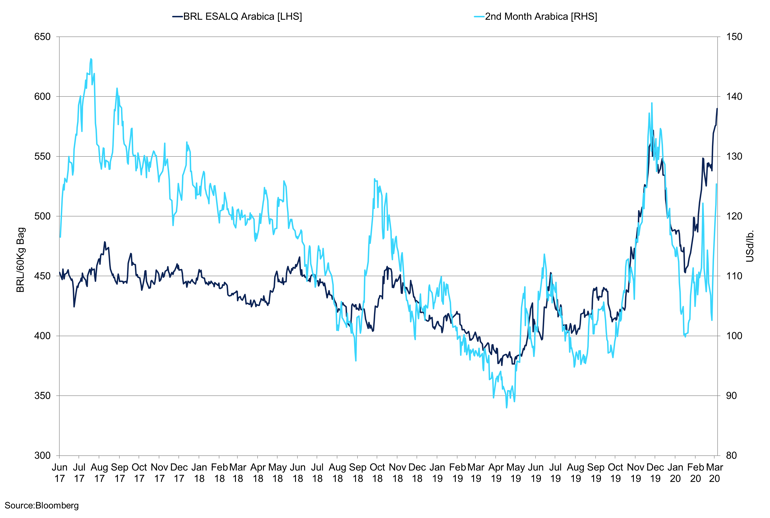

Brazil Coffee Local Price vs 2nd Month Arabica

Real weakness triggers vast producer forward selling due to favourable local prices.

For the 2020/21 season, we have a provisional Brazil crop of 66m bags; total availability is 67m due to the 1m bag carry-over. The split as 48m bags for Arabica and 18m bags for Conillon. The Brazilian crop needs to be 61.5m bags in order to satisfy global and domestic consumption, 40m outside world and 21.5m internally. This is a large Arabica crop, however with the Real holding above R$5.00 to the $ we have seen Brazilian forward selling reach record levels, prompting the commercial gross short reaching a record 214,594 contracts as of February 4th. We do not see the deficit in Brazilian coffee, but there is a downside to our 66m number, more specifically the Arabica crop due to lack of labour during the harvest. Notwithstanding tree stress, in July 2019 cold weather significantly damaged the crop, and in our view, the temperature was 1 degree above severely harmful to the crop. Dry weather in September and October caused further stress to the trees; wet weather in Santos and neighbouring regions has been catastrophic, and landslides destroyed coffee acreage and deaths to civilians.

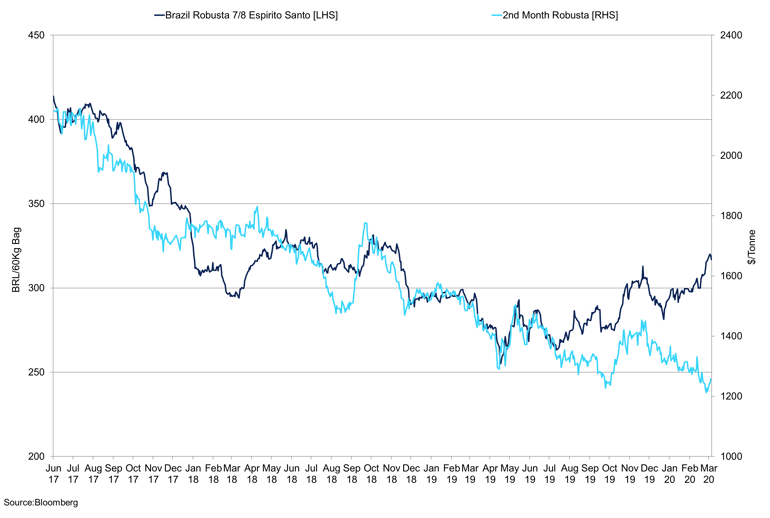

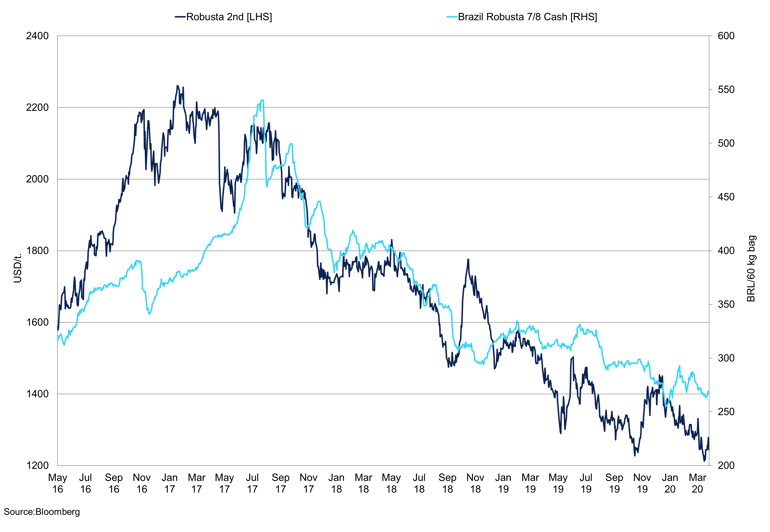

Brazil Robusta 7/8 Espirito Santo vs 2nd Month Robusta

The divergence in local prices and the London contract is intriguing.

As of April 6th, Brazil had sold 85% for 19/20, 50% of the 20/21 season, and 30% of the 21/22 season. We see this as bullish in the long run due to a lack of selling further down the curve, even as the futures curve for Arabica has flattened. Given the slide in the Brazilian Real, we believe farmers will start to hold back selling until the local price reaches R$600/bag at the time of writing local prices are R$575/bag; this will have a downward impact on Brazilian exports until we see the new crop. Inputs such as fertilisers are bought in the greenback, a headwind to profitability. We expect differentials to remain strong as a result, with demand increasing for untenderable stocks. Roasters will cup this coffee and realise it is usable, this coffee could be available for -10, but it is unclear how much of this coffee is available. Traders have withdrawn certified stocks, and we expect this to pick up pace now there are delays to shipments. The tightness in the market is highlighted by the tightening of the structure further down the curve, the March 21/March 22 spread stands at -5cts/lb, in from -8cts/lb. At the time of writing, NY KN spread is at 1.50cts/lb under and we believe this level is attractive for the trade.

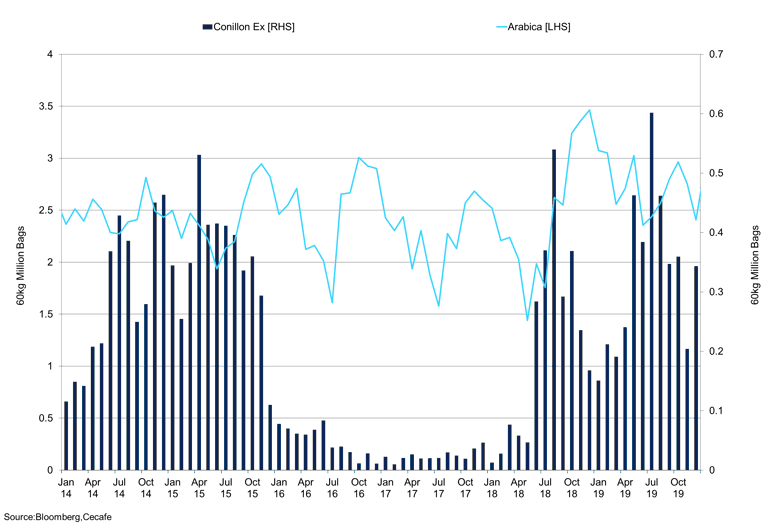

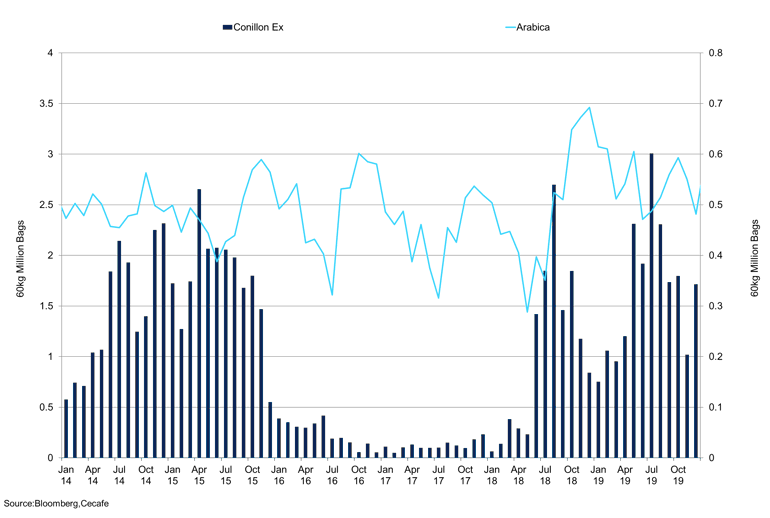

Brazil Conillon vs Arabica Exports

Conillon exports have tailed off in 2020 due to less appetite for delivering into London.

Vietnam

The Vietnam crop stands at 29m bags for the 19/20 season; production has remained steady in recent years. Dry weather in S.E. Asia could trigger some downside to this crop. Yes, the trees are old, but they are also high yielding but the temptation of growing durian fruit of pepper maybe a longer-term threat to coffee. We do not believe this will be the case due to strengthening coffee demand from China.

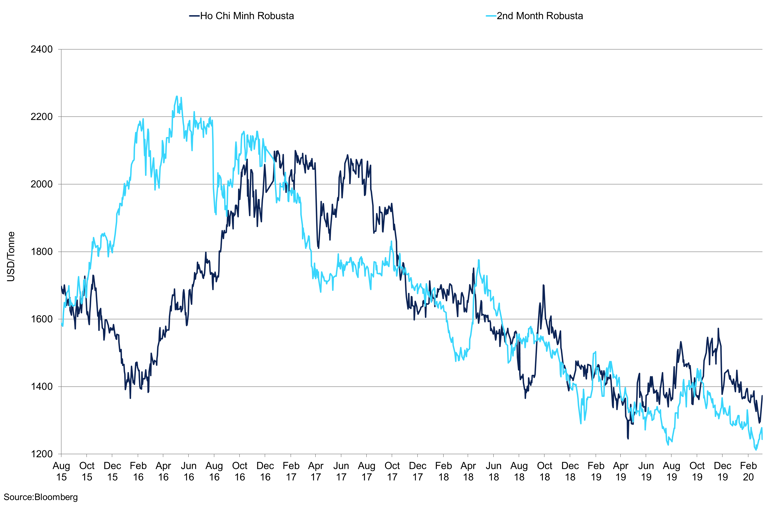

Vietnam Ho Chi Minh Robusta vs 2nd Month Robusta

Robusta prices continue to decline, and Vietnam farmers slightly drop their asking price.

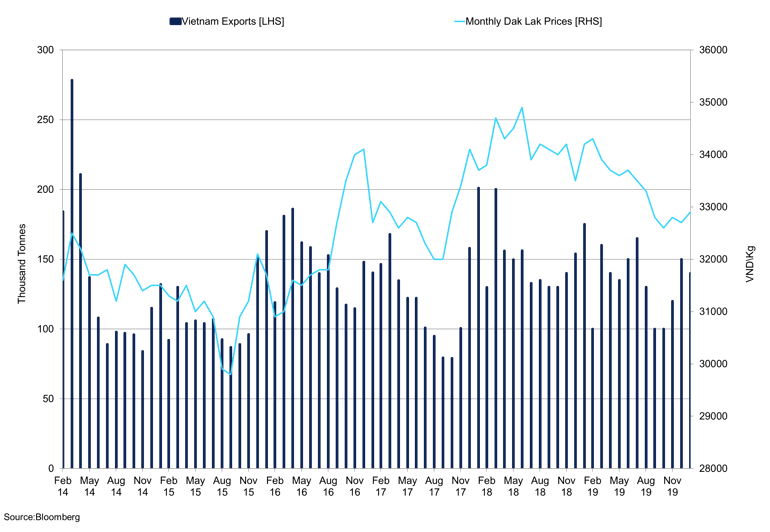

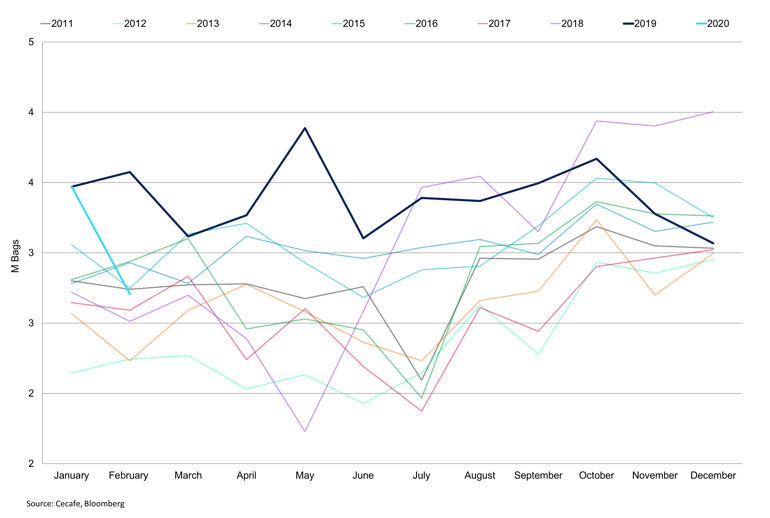

Exports cooled between September to November 2019 as farmers held back sales as they waited for higher prices. However, as prices improved and hit the local target of 35,000VND/kg, exports started to flow with November and December 120,000 and 150,000 tons respectively, up from 100,000 for September and October 2019. This brought total exports for Vietnam for the 2019 calendar year to 27.08m bags. The first two months of 2020 have seen exports rise to 140,000 and 150,000 tons in January and February respectively in 2020. February shipments may be on the rise as the trade attempts to get the product out of Vietnam before the coronavirus impacts logistics and prompts delays in shipping. We did see some vessels diverted to Vietnam from China during the height of the Chinese outbreak of the virus. While we accept that there are different types of freight, congestion in the ports may cause delays to shipments. However, we expect a lack of labour to be the main constraint to ports and there is container congestion in Ho Chi Minh City.

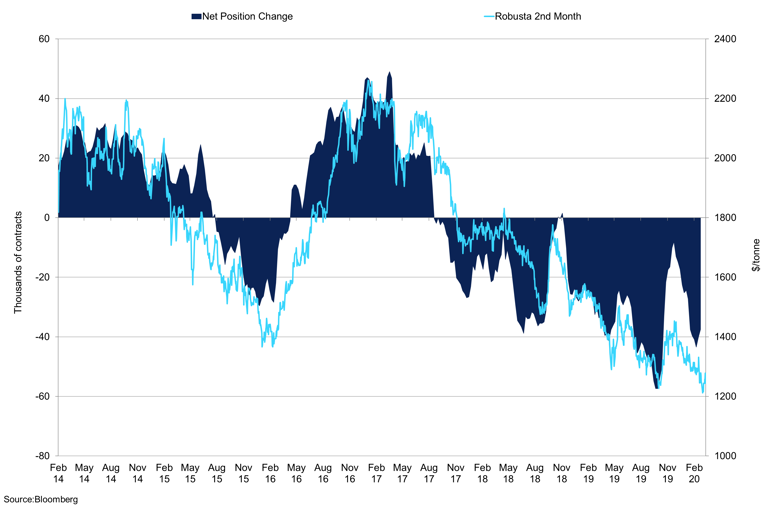

2nd Month Robusta vs Managed Money Net Position

Speculator short net position shows bearish bets on Robusta.

Looking ahead to 2020/21, the recent dry weather is not a huge worry currently. However, like Brazil in September and October 2019, if dry weather continues, we expect this to damage the yield for the 2020/21 crop. We see no reason to reduce our number for 2020/21, if prices start to improve, we’d expect to see more coffee in Vietnam. Our base case is for a modest reduction in shipments due to logistical constraints. If shipments remain slow, then carry-over into the new crop will be higher than expected. However, option 2 is that shipments are subdued while the virus curtails economic activity and then spike as traders and roasters replenish inventories. Differentials remain high with grade 2 Vietnams at +170; we expect them to stay steady at current levels. Farmers have slightly dropped their local price expectation from 35,000VND/kg to a range of 30-33,000VND/kg. We saw strong selling from farmers in recent months as prices remained favourable. Ho Chi Minh inventory increased to 5.9m bags in February 2020, up from 5.7m bags the previous month, arrivals have been strong and depending on the coronavirus and worker shortages reducing loading capacity, we expect shipments to remain strong as European traders and roaster attempt to get the product out of origin into consumer countries.

Colombia

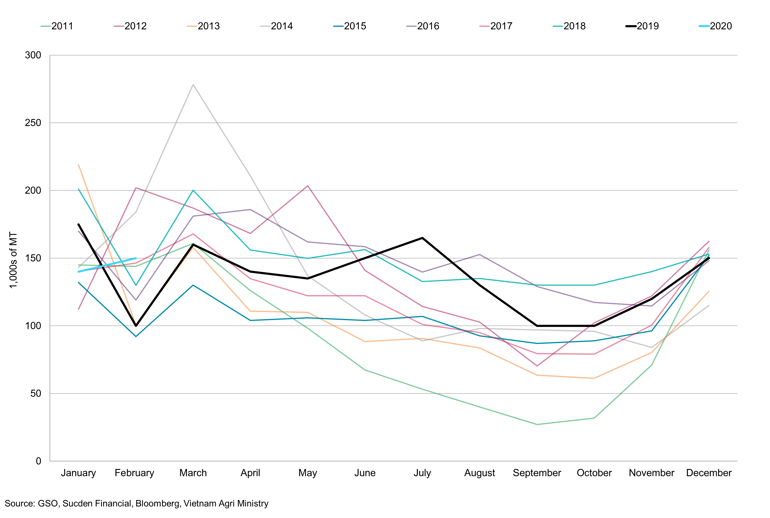

Our Colombian production number for 2019/20 has been reduced to 13.8m bags from 14m bags earlier on in the year. Data from the Federation Nacional de Caeteros de Colombia (FNC) has shown production in January and February down 19% and 9% on year on year basis respectively. Combined production is down 15% to 2.05m bags. The FNC suggests that for the calendar year production was 14.8m bags, at an average differential of 26.7cts/lbs. The confederation suggests that exports are up 9% to 6.606m bags, from 6.071m bags.

Our previous report outlined strong demand Colombian coffee from various destinations such as Canada, the U.S. and Europe. We are now seeing no Colombian coffee offered; differentials continue to remain high at +50 over. The government has enforced a countrywide quarantine, including coffee mills. Incoming flights have been cancelled; shipments will be delayed as well as the harvest of the mid-crop. However, all the ports remain open as exports are the driving force for their economy.

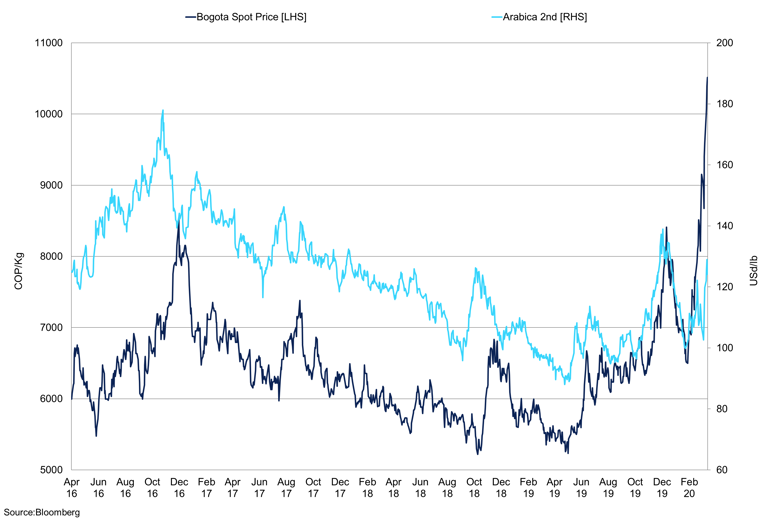

Colombian Bogota Spot Price vs 2nd Month Arabica

A weak local currency has caused the slide in the Bogota spot price.

There are funding issues between Colombia and the U.S. due to the production of illicit drugs; this is causing crops to be sprayed with chemicals in order to kill the crops. There is a risk that this finds its way onto coffee crops. This could reduce certified organic coffee. While it is not clear the outcome of this scenario, it is a situation worth watching. The government has identified revenue issues for farmers; in February, the FNC introduced a new fund of $64.4m in order to protect farmers against volatile prices.

Central America & Marginal Producers

In Honduras, we continue to see issues. We have reduced our estimate for the 19/20 crop to 5.5m bags, and we have the 20/21 crop at 5m bags. This is due to low NY prices, reducing the incentive to grow coffee. Yes, the differential has been strong, but prices are still low on a historical basis. Furthermore, the strength of the dollar has been a headwind to input costs. This has been a headwind for most coffee origins however, more so for higher-cost producers.

The issue with Honduran crops is the lack of washed Arabica coffee, and this is where we see the deficit. The Brazilian on-cycle is expected to see a bumper crop, however, there is little substitute for Honduran coffee. We believe that Honduran differential will stay firm. Once the certified stocks of Honduran coffee have been drawn, there isn’t much replacement due to the low Honduras crop in 20/21 and likely the season after that. Honduran coffee in inventory is subject to a time penalty and compared to physical prices is cheap; we see this coffee at 10-15 under the board as this coffee has a time penalty. If you are delivered coffee that is 1-2 years old, you may sell this coffee at level money to 2 over.

In Africa, we are also seeing problems, in Ethiopia especially there have been issues with locusts. This has caused crops to be sprayed with pesticides reducing the organic and fair trade coffee. This could also impact quality and therefore revenue to the country. According to reports, Ethiopia has earned $407m from coffee exports during the past 7 months, less than the same period last year due to low exchange prices. The decline in prices has a significant impact on the Ethiopian economy which relies on coffee. There have been suggestions to increase origin roasting, therefore adding value in Ethiopia, increasing the price that the farmers receive which can then be spent in the community boosting the multiplier effect. The price of roasted Arabica is significantly higher than green coffee and if Ethiopia can receive a higher price, this would benefit them. Amending the supply chain is not tricky but there are benefits to origin countries.

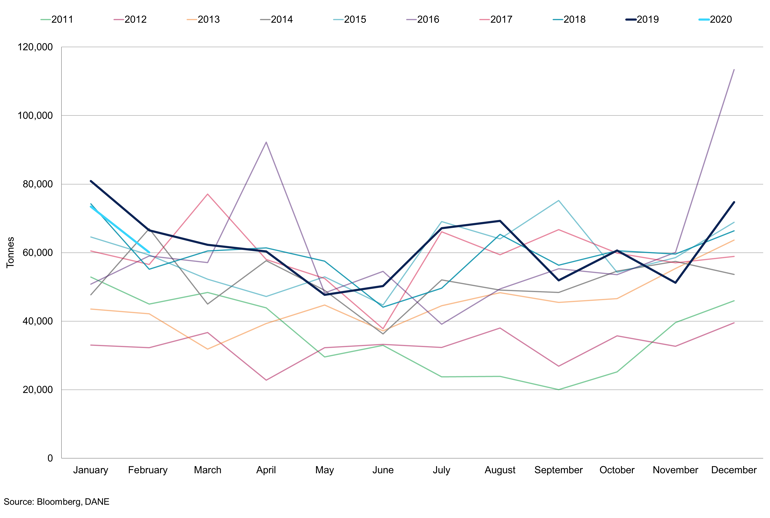

Looking at the Ivory Coast, we forecast the next crop at 1.2m bags at this time. There is a downside to this number but at this time problems are yet to materialise fully. We continue to track shipments avidly to assess if our crop figure needs to fall towards 1m bags.

Inventories

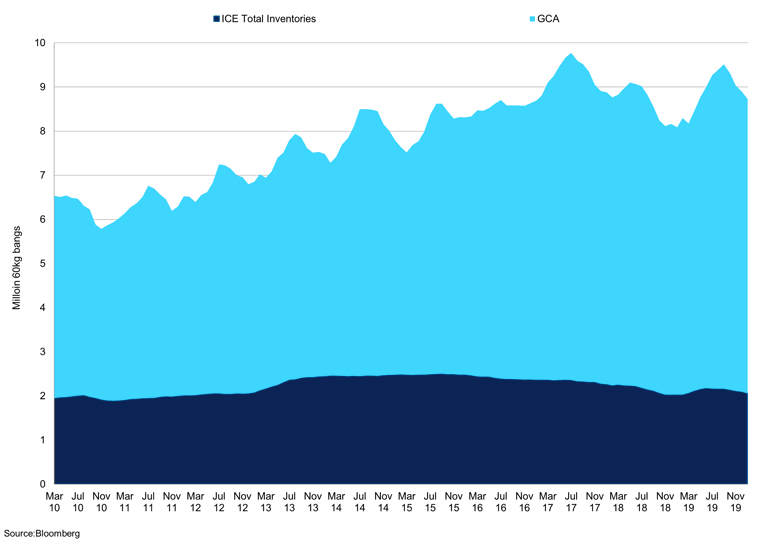

ICE Total Inventories & GCA Stocks

Stocks are starting to draw and we expect this to continue at a steady clip.

The latest GCA stock figures show that inventories are down 357,247 bags to 6.312m bags. The majority of this product is in New York. This includes exchange and non-exchange stocks, in our previous reports we have highlighted that we feel stocks will be drawn and this is clearly the case now. We expect this to continue in 2020 despite the recent outbreak of the COVID-19. It is worth noting that this is only in U.S. ports. We expect to see a similar amount in European ports. We anticipate this coffee to be predominately Honduran origin. As mentioned above, we see little replacement for Honduran coffee in the long run due to poor production. Differentials remain firm standing at +28 as March 13th. The certified stocks for NY show that there are 1.538m bags of Honduran coffee with the majority still in Antwerp. This coffee is priced between 10 and 15 under and has a time penalty. NY certified stocks stand at 2.139m bags and we expect there to be significant withdrawals in the coming months. If the strikes at Port Santos are action and the ICE exchange cannot grade enough coffee in time for the May delivery, we expect roasters to come for the certified stocks. This would see the flat price strengthen; the structure KC KN has weakened slightly from a premium of +1.80ts/lb to -1.50cts/lb as of April 6th; as a result of the roll.

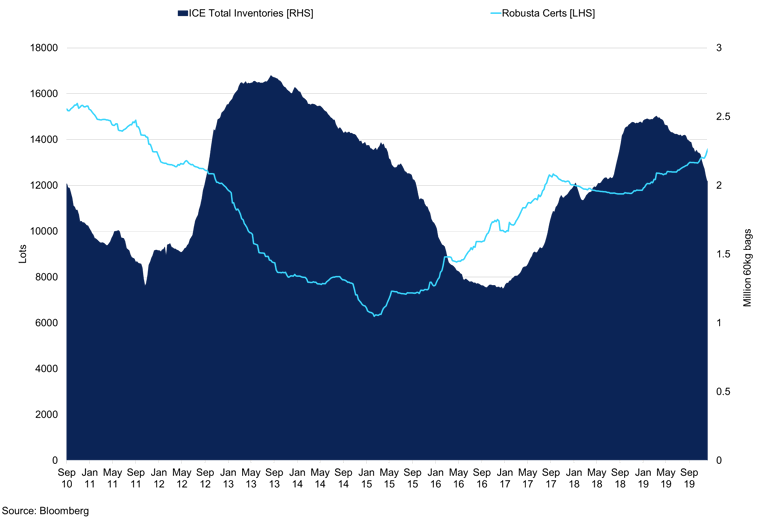

For Robusta, the certified stocks have also started to fall to 14,560 lots as of March 18th; we expect the market will continue to see drawdowns despite Vietnam exports remaining strong through to the beginning of March. We logistical difficulties as a result of the coronavirus, we are seeing the delays to shipments and deliveries. We expect these to continue in the next month or so as the labour force is encouraged to work from home and teams are split between A and B.

ICE Total Inventories vs Robusta Certified Stocks

Certified stocks for Arabica and Robusta are diverging. We expect the trade to start going for the certs.

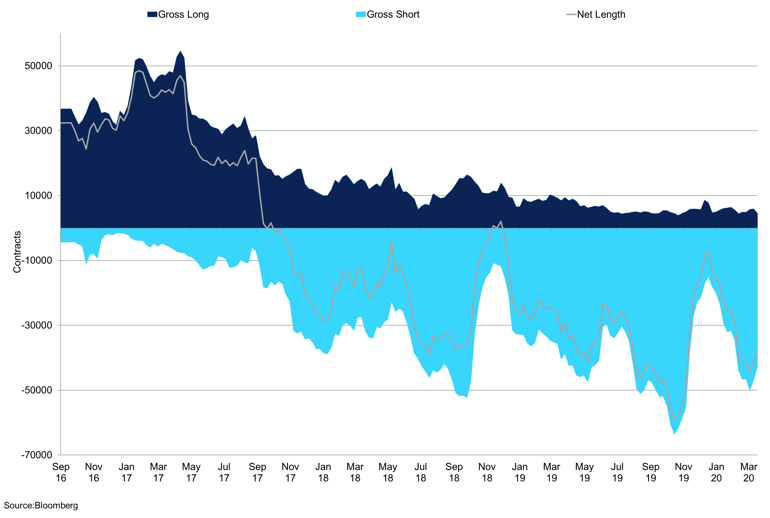

Commitment of Traders

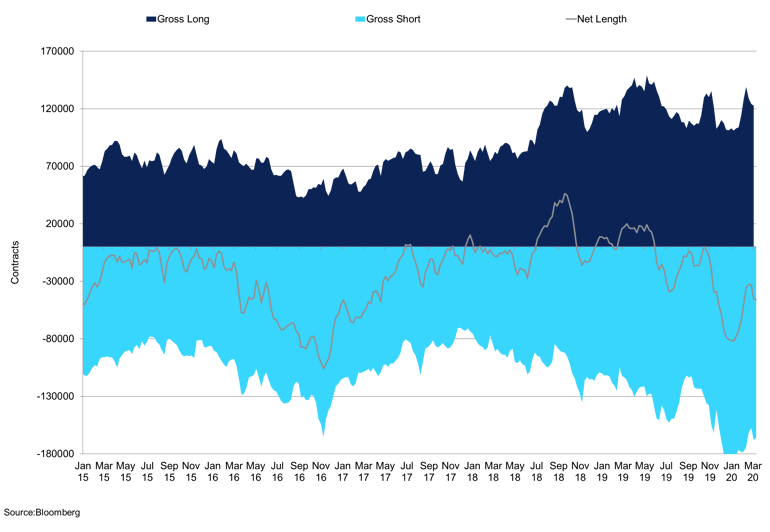

During the February rally, we saw open interest increase as new longs entered the market and some shorts were stopped out. The rally was in part as a result of issues in Central America and significantly wet weather in Brazil damaging forecasts for the 20/21 season. Total open interest tailed off from their high in February of 407,087 as investor sentiment was damaged from lack of risk appetite due to the economic implications of the coronavirus to 325,245 as of April 3rd.

Arabica Producer/Merchant Commitment of Traders

The gross short reached a record low earlier this year and remains high.

CFTC data shows an improvement in market sentiment as the net short position narrowed from -16,523 on February 18th, to 8,840 contracts as of April 3rd. The New York contract has started to rally but recent volatility has caused some system funds to turn off their machine re-aligning the contract with the fundamentals. Investors look at the shipment delays and stock drawdown to give rise to the flat price. The market is in the hand of the speculators as we do not believe roaster appetite for prices at 130cts/lb will be strong at this time. We believe the macro is holding back prices but if the speculators look at the fundamental outlook and see the value, we will see the rally continue.

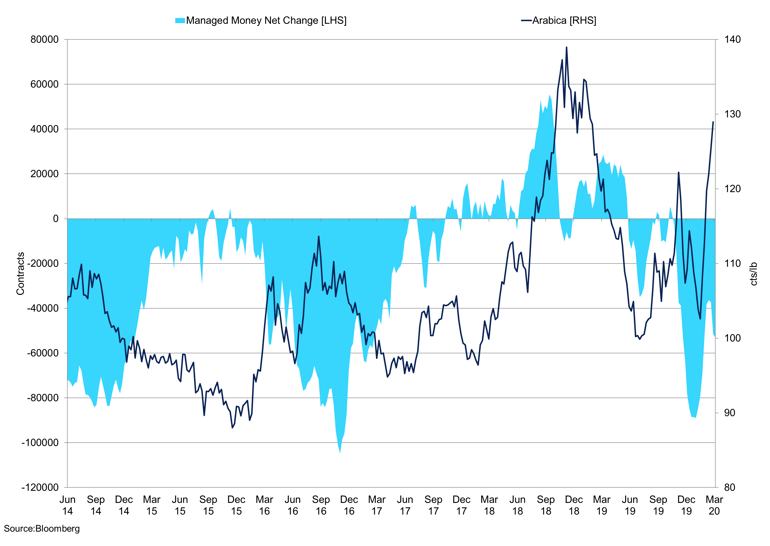

Arabica Managed Money Commitment of Traders

Recent volatility has seen some funds reduce risk as intraday swings cause pain.

Commercials have decreased their short positions to 189,551 contracts as of April 3rd from 214,594 the beginning of February 4th, 2020. The record low BRL aids producers, with the BRL losing 31% so far this year, this gives rise to local prices. The gross long positions did, however, decrease to 131,400 contracts, as prices started to gain some traction, and the net position has decreased to 58,151 short as of April 3rd.

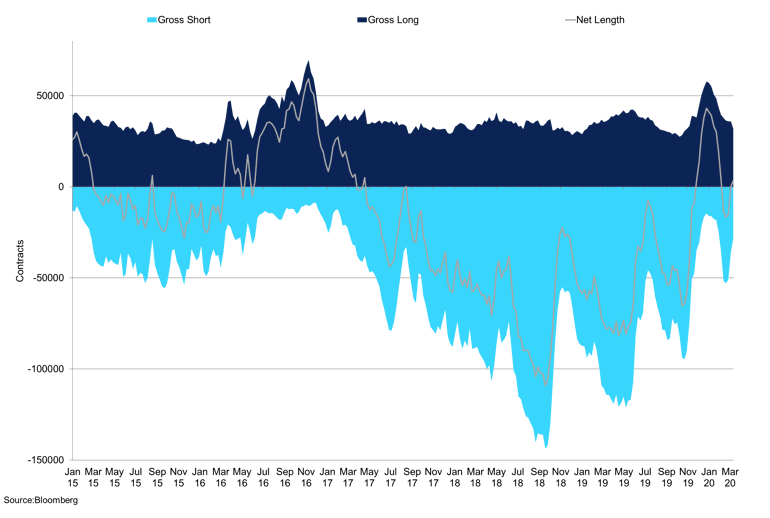

The Robusta producer/merchant disaggregated futures and options net position increased drastically, with the net long-reaching 34,212 net long contracts as of March 31st, just off the years high of 46,685 contracts from March 10th. So far in this year, the net length has risen approximately 170%. The gross longs have increased to record levels at 110,000 in the same time period, outlining that roasters are well covered. The shorts, however, whipsawed through January to February, and as of March 31st, stand at 70,787. DF prices have lost as much as 15.53% so far in Q1. The managed money net position was seen to move in reversal to producer/merchant, as managers increased their shorts from 19,928 to 34,773 contracts, yielding a net length at 30,119 net short on March 31st. The risk-reward is against you at current prices, especially when you look at Robusta prices on a cents per lb basis.

Robusta Managed Money Commitment of Traders

Robusta speculators hold their shorts.

Appendix

Brazil

Managed Money Net Position vs 2nd Month Arabica

Brazil Conillon & Arabica Exports

Brazil Roasted vs Green Coffee Exports

Robusta

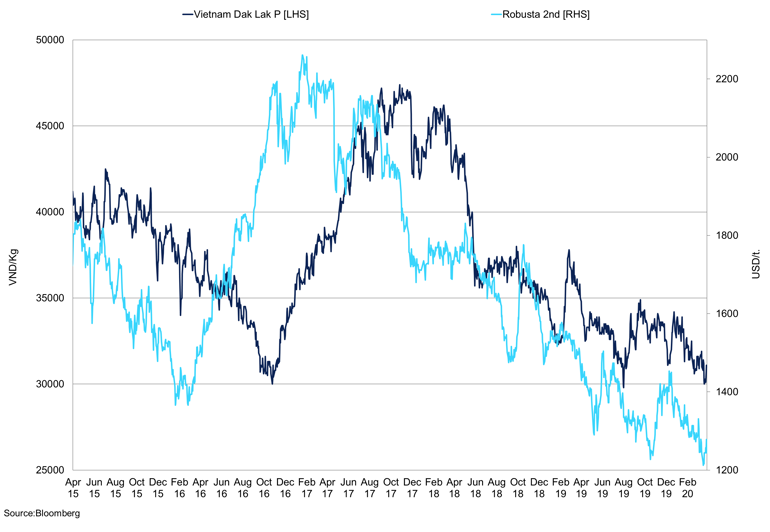

Vietnam Dak Lak Robusta Price vs 2nd Month Robusta

2nd Month Robusta vs Brazil Robusta 7/8 Cash

Vietnam Exports vs Monthly Dak Lak Price

Global Coffee Supply

Global Coffee Supply Calendar Year

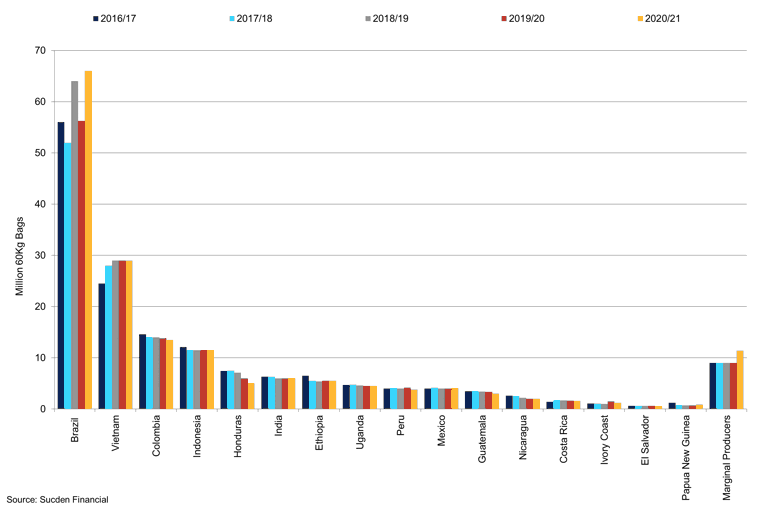

Global Coffee Supply 2020/21

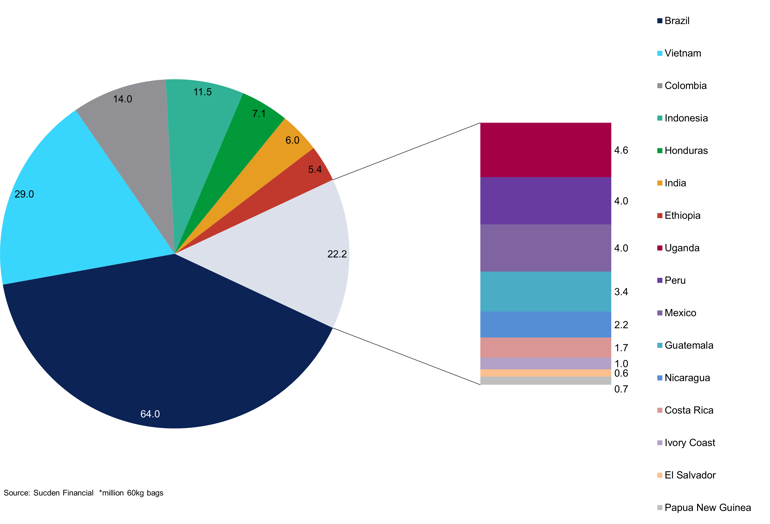

Global Coffee Supply 2019/20

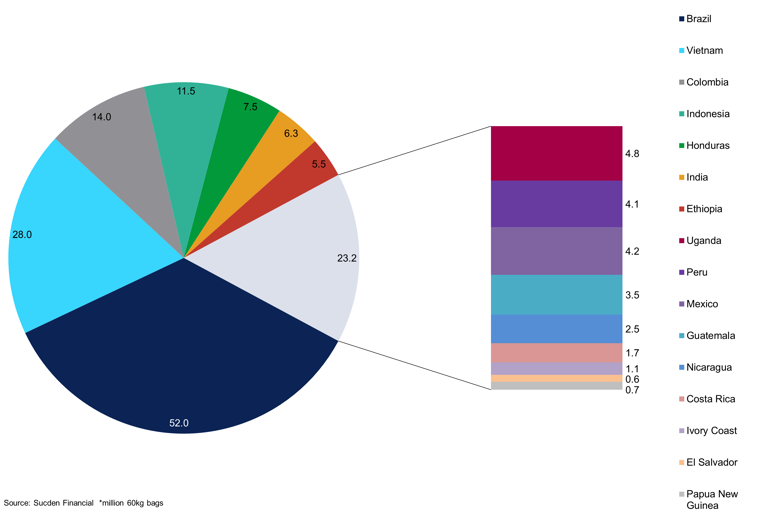

Global Coffee Supply 2018/19

Global Coffee Supply 2017/18

Big Four Exports

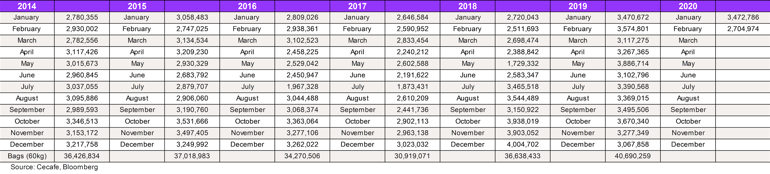

Brazil Exports

Vietnam Exports

Colombia Exports

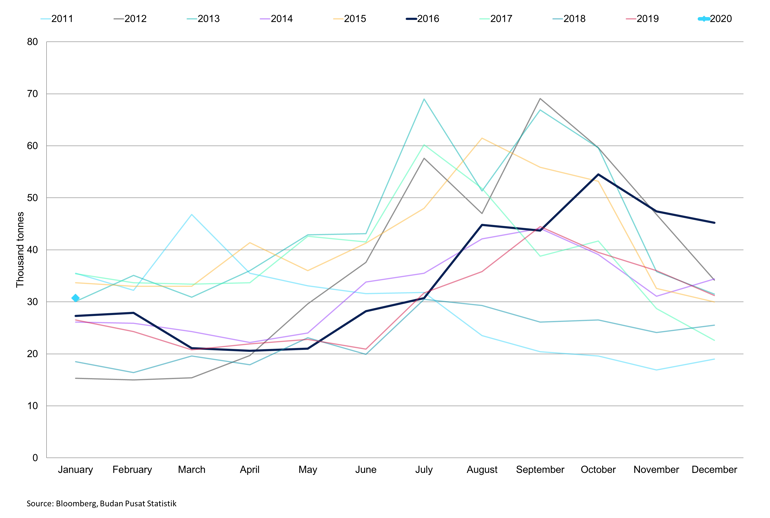

Indonesia Exports

Brazil Coffee Exports Calendar Year

Vietnam Coffee Exports Calendar Year

Indonesia Coffee Exports Calendar Year

Colombia Coffee Exports Calendar Year