EUR / USD

The EUR/USD pair remains in a precarious position as market expectations for a December Fed rate cut have decreased from 60% to approximately 40% in recent weeks, creating additional downward pressure on the currency pair. Those rate-cut bets are now starting to rebuild, and a stronger-than-expected Nonfarm Payrolls print on Thursday could briefly revive speculation of a late-year move. However, we expect the Fed to remain on hold through December, maintaining a more hawkish posture until clearer evidence of genuine labour-market cooling emerges, particularly as this week’s payrolls data cover September and offer only limited insight into the most recent economic dynamics.

Technical analysis reveals the pair's resilience above the 200-day moving average at 1.15, though it faces notable resistance at 1.168, with intermediate barriers around the 50-day and 20-day moving averages near 1.16. The European Central Bank's apparent conclusion of its rate-hiking cycle, coupled with weak Eurozone economic growth and cooling inflation, presents a challenging environment for sustained euro strength.

The upcoming September jobs report and Fed's October meeting minutes will be critical in determining the pair's direction, while current price consolidation between 1.1580-1.1600 suggests a potential breakout scenario. A decisive move above 1.168 could target the recent peak of 1.187, whereas a breakdown below the 200-day moving average might trigger a decline toward the early November lows near 1.147.

USD / JPY

The USD/JPY pair continues to demonstrate significant bullish momentum, driven primarily by the widening interest rate differentials between the US and Japan, with the Federal Reserve maintaining a hawkish stance while the Bank of Japan remains dovish under Prime Minister Takaichi's administration. The Japanese currency faces mounting pressure from domestic fiscal concerns, as the government prepares a substantial stimulus package exceeding 23 trillion yen, which has pushed 20-year Japanese government bond yields to 26-year highs.

Technical analysis reveals strong upward momentum with the pair trading well above key moving averages, including the 20-day SMA at 153.94 and the 50-day SMA at 151.79, suggesting continued bullish sentiment in the near term. Despite verbal intervention from Japanese officials expressing concern over rapid currency movements, the market appears to be testing authorities' tolerance levels, with limited impact from these warnings.

The combination of reduced expectations for Fed rate cuts, with only a 50% chance priced in for December, along with Japan's expansionary fiscal and monetary policies, indicates potential further upside for USD/JPY, with technical indicators suggesting a possible move toward the yearly peak near 158.55 if the recent high of 155.72 is breached.

GBP / USD

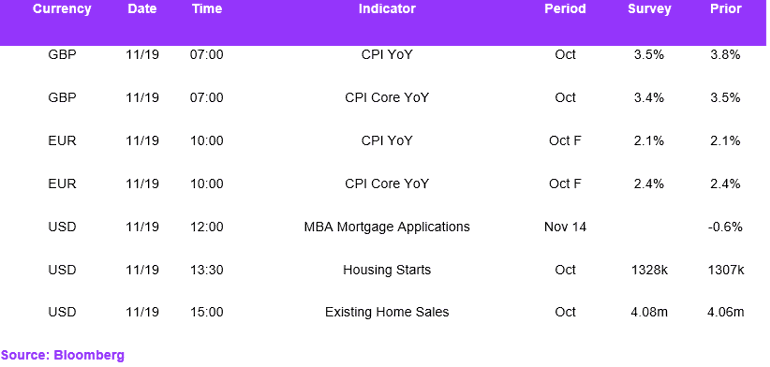

The GBP/USD pair faces downward pressure as the Bank of England's increasingly dovish stance contrasts sharply with the Federal Reserve's more hawkish positioning, with markets pricing in a 75% probability of a BoE rate cut in December. Our base-case is a 25bps reduction to 3.75% at the December meeting. UK inflation data, due today, is expected to soften further, and keeping a BoE cut firmly in play.

Technical indicators paint a bearish picture, with the currency pair trading below all major moving averages and the 30-day VWAP of 1.32, suggesting sustained selling pressure. The upcoming UK budget on November 26th represents a critical event that could accelerate sterling's decline if markets deem the fiscal approach inadequate.

The combination of domestic pressures and a resilient US macroeconomic environment creates a challenging backdrop for sterling, with immediate technical resistance at 1.322 and support at 1.301 serving as key levels to monitor.

Economic Calendar