EUR / USD

EUR/USD weakened, as the dollar index pushed above 100.0 today, with the move driven more by tightening USD liquidity conditions than by shifts in rate expectations. Despite steady 10-year yields and limited changes in Fed pricing, elevated overnight funding costs, reflected in GC repo trading above the top of the Fed’s target range, suggest reserves are approaching the lower bound of what the Fed views as “ample.”

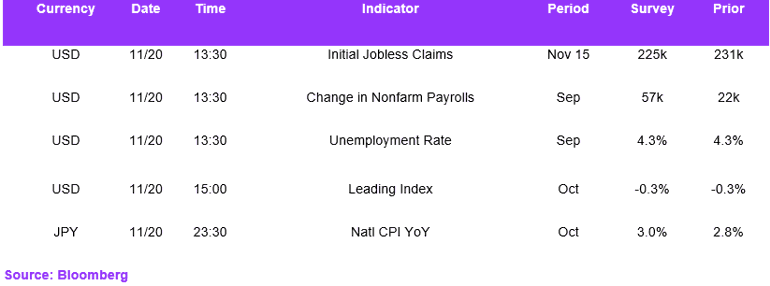

From the macroeconomic perspective, the ECB's unwavering commitment to its "higher for longer" approach, supported by inflation near target and record-low unemployment, provides substantial backing for the euro's position. In the US, the nonfarm payrolls release today is expected to show an increase from 22k to 50k on Thursday. Even if new data emerges supporting a cut, we maintain our view that the Fed will not cut rates in December. We expect policymakers to respond with more proactive hawkish statements, fuelling further volatility in the dollar index and US Treasury yields as markets continuously readjust.

As markets continue to discount the probability of a December rate cut from the Fed, the case for EUR/USD is likely to keep the rate in the lower end of recent ranges, with support at 1.1500 well defined.

USD / JPY

USD/JPY rallied above 155.00 toward 157.00, as the Japanese government's aggressive fiscal expansion plans, including a massive stimulus package exceeding 20 trillion yen, coupled with the Bank of Japan's persistently accommodative monetary stance, are creating substantial headwinds for the yen.

As Sunday's GDP printed weak, markets have taken the December BoJ hike off the table, and a higher CPI print today should only partially revive expectations as markets try to rebalance.

Technical analysis indicates an overbought condition, with the daily RSI at 76, which may suggest a potential dip today as profit-takers emerge. However, the combination of expansionary fiscal policy and low interest rates has effectively eroded the yen's traditional safe-haven status, with market expectations indicating no rate hikes until March 2026. This should help maintain the 155.00 support level intact from a fundamental perspective.

GBP / USD

GBP/USD sold off following October's inflation data, which showed core CPI rising less than expected and headline inflation easing to 3.6%. The data provide timely support ahead of next week’s Budget and reinforce expectations for a December rate cut. We expect a 25bps reduction from the BoE next week.

The technical outlook appears bearish, while the daily RSI at 33 suggests oversold conditions, which help identify support at 1.3000 as markets price in the BOE’s more dovish rate-cutting cycle. The currency's weakness is also being amplified by broader dollar strength and rising gilt yields, which have reached one-month highs as investors grow increasingly concerned about the UK's fiscal position.

Economic Calendar