EUR / USD

EUR/USD continues to draw support from a widening transatlantic policy gap, with the ECB signalling it will hold its 2% deposit rate through 2026 while the Federal Reserve edges closer to a cutting cycle. Macro data reinforce the divergence: Eurozone services remain resilient, whereas US manufacturing has now contracted for nine consecutive months.

From a technical perspective, the bias is cautiously constructive. The pair is holding above key supports, including the 200-day moving average near 1.160, while RSI at 57 suggests moderate bullish momentum. The narrowing US-EU rate differential looks increasingly structural as expectations for Fed cuts harden, offering ongoing support for the euro.

Constructive US-EU trade dialogue and firmer global risk appetite add tailwinds, though upcoming Eurozone HICP data could introduce volatility. A push through 1.167 would open the path towards 1.173, while 1.160 remains an important downside marker.

USD / JPY

USD/JPY sits at a pivotal moment as the Bank of Japan signals the strongest hint yet of a December rate hike, a decisive departure from its long-running ultra-loose stance. Above-target inflation and the jump in JGB yields, with the 2-year above 1% for the first time since 2008, underscore the shift.

The pair has held a narrow 154.8–155.8 range, supported by the 20-day moving average at 155.6, though the broader macro story suggests growing downside risks for USD/JPY. With the BOJ tilting hawkish and the Fed leaning towards cuts, the long-standing policy divergence that fuelled dollar strength is beginning to unwind.

Despite this, the pair still trades well above key longer-term levels, including the 50-day SMA at 153.6 and the 200-day SMA at 147.9. The evolving stance of both central banks, combined with political backing in Tokyo, keeps the potential for yen appreciation firmly in focus.

GBP / USD

GBP/USD remains delicately balanced as it trades beneath key moving averages but shows pockets of upward momentum. Continued weakness in US manufacturing, the ISM index contracting for a ninth month at 48.2, has strengthened expectations of a December Fed cut, now priced at an 88% probability.

Sterling’s appeal is anchored by comparatively high G10 interest rates, though this support could fade as markets begin to price Bank of England cuts next year. Technicals highlight notable congestion around 1.325, with falling volumes during recent dips indicating softer selling pressure.

The pair’s near-term direction hinges on whether it can reclaim the 50-day moving average at 1.32. A sustained break would expose 1.339, while failure to hold current levels risks a move towards 1.301. Despite lingering domestic and global headwinds, institutional flows ahead of December’s central-bank calendar should keep volatility elevated while offering pockets of support for the pound.

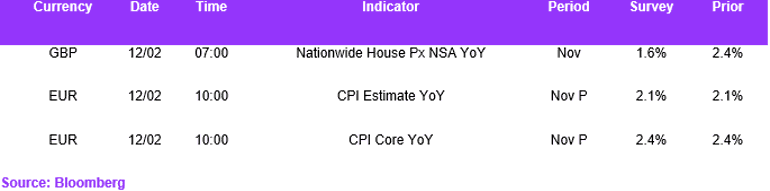

Economic Calendar: