EUR / USD

EUR USD continues to show resilience, holding above the 200 day moving average at 1.16, while eurozone inflation edged higher to 2.2 per cent in November from 2.1 per cent in October. The technical backdrop remains cautiously constructive, with the RSI at 59 signalling firm but not overstretched bullish momentum.

Policy divergence remains a central driver. Markets are pricing roughly 90 basis points of US rate cuts through 2026, while the ECB is expected to keep rates steady. Any progress in Russia Ukraine peace negotiations could lower the eurozone risk premium, although resistance near 1.173 remains a significant barrier.

Near term direction will hinge on upcoming US releases, particularly the ADP employment report and PCE inflation. A drop below 1.154 would expose the psychological 1.150 area.

USD / JPY

USD JPY is trading with elevated volatility as expectations diverge between the Federal Reserve and the Bank of Japan. Markets now assign an 80 per cent probability to a BOJ rate increase in December, marking a potential shift away from Japan’s long standing ultra loose stance, while the Fed is widely expected to begin cutting rates.

Japanese government bond yields have surged to multi year highs, with the 10 year reaching 1.87 per cent. The narrowing US Japan rate differential raises the risk of a broader unwind of yen funded carry trades. Despite a slight recent decline, USD JPY remains above key averages, with the 20 day at 155.67 and the 50 day at 153.72.

The medium term outlook favours yen strength, supported by above target inflation and the prospect of policy normalisation, though the risk of intervention remains elevated near 158.

GBP / USD

GBP USD is presenting mixed signals as recent UK data show a steadier labour market and stronger services activity, offering underlying support for sterling. The Bank of England is expected to cut rates at its 18 December meeting in response to softer labour and inflation dynamics, while the Federal Reserve’s easing cycle is projected to begin later in 2026, creating an unusual policy mix for the pair.

The pair has held within a narrow range, finding support at 1.3197 and resistance around 1.3262, with the RSI at 52.65 indicating modest but building bullish sentiment. A break above the 50 day moving average at 1.32 would open a move towards the 200 day moving average at 1.34.

The UK’s improving growth outlook, supported by the OECD’s upward revision and a less restrictive fiscal stance in the recent budget, adds to sterling support. Even so, diverging central bank paths may limit upside as the BOE edges gradually towards more accommodative conditions.

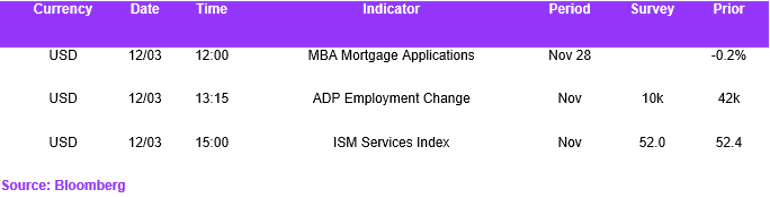

Economic Calendar: