EUR / USD

EUR USD continues to display considerable strength, driven primarily by widening policy divergence between the Federal Reserve and the European Central Bank. Markets are now pricing a 90 per cent probability of imminent Fed rate cuts, while the ECB maintains a resolutely hawkish stance. Recent eurozone data have reinforced this momentum, with business activity expanding at its fastest pace in 30 months and offering solid fundamental support for the single currency.

The technical backdrop remains constructive, with the pair holding above the key 200 day moving average at 1.16 and repeatedly testing upper resistance levels. The daily RSI at 63 indicates further room for upside. Speculation around the potential nomination of Kevin Hassett as Fed Chair has added to dollar weakness, as his perceived preference for deeper rate cuts would widen US–eurozone policy divergence further.

Strong regional fundamentals, supportive technicals, and persistent US twin-deficit concerns all point to continued euro strength, with resistance at 1.167 acting as the immediate hurdle. A break above this level would open a move towards 1.173, while support at 1.155 remains the key threshold guarding against a deeper correction towards 1.147.

USD / JPY

USD JPY is coming under sustained pressure as the Bank of Japan signals a possible rate increase in December, marking a significant departure from its long-standing negative interest rate policy. Japanese government bond yields have climbed to their highest levels since 2007, with the 10 year JGB reaching 1.91 per cent, adding further downward pressure on the pair.

Technically, USD JPY is trading close to its 20 day moving average at 155.77, remaining comfortably above the 50 day average at 153.87. Recent sessions have seen the pair dip to lows of 154.56, yet the broader trend remains underpinned above the psychological 155 level.

Expectations of BOJ tightening, alongside Japan’s substantial fiscal stimulus, are producing a complex trading landscape, while long-term structural flows such as pension allocation trends are tempering the speed of yen appreciation. The near-term outlook will hinge on the balance between policy expectations and technical supports, with 157.73 acting as key resistance and 152.67 defining crucial downside protection.

GBP / USD

GBP USD has shown notable resilience, supported by diverging policy expectations between the Bank of England and the Federal Reserve. Markets are assigning a 90 per cent probability to an upcoming Fed rate cut, while the BoE remains comparatively hawkish. Sterling has also benefited from improved domestic data, including the upward revision to November’s services PMI to 51.3 and the smooth passage of the Chancellor’s budget through bond markets.

The pair is trading above both the 20 day and 50 day moving averages around 1.32, though it remains capped by the 200 day moving average at 1.34. The RSI at 67 signals strong bullish momentum, albeit edging towards overbought territory. The dollar’s broader weakness, with the currency on track for its largest annual decline since 2007, has provided an additional boost.

Sterling’s short-term direction is likely to be shaped by the upcoming Federal Reserve meeting, with 1.302 acting as initial support and the 200 day moving average at 1.34 representing the key resistance barrier to further gains.

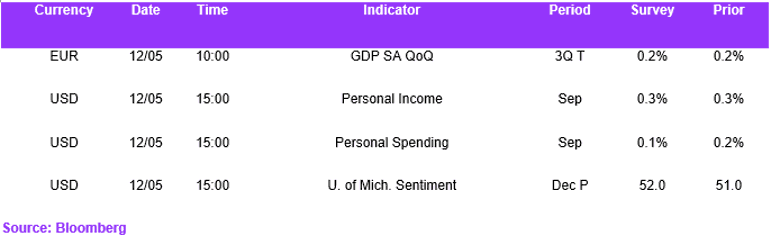

Economic Calendar: