EUR / USD

EUR/USD strengthened toward 1.1650 last week, driven by several significant macro factors heading into the Federal Reserve's December meeting. The Fed is widely expected to deliver a 25bps rate cut, with markets pricing in a 95% probability of easing. However, there appears to be a notable division among Fed policymakers, with five of the twelve voting members expressing scepticism about further cuts.

Although we believe the delay in labour and inflation data leaves the Fed without the information normally required for a fully data-driven decision, policymakers are unlikely to move against such entrenched market pricing at this stage. We therefore expect a 25bps cut, followed by an explicit commitment to restoring a data-dependent approach once the flow of releases normalises.

The European Central Bank is facing its own challenges, with French President Macron calling for a rethink of monetary policy to focus beyond just inflation targeting. Macron has also warned that the EU may need to take strong measures against China, including potential tariffs, if Beijing fails to address the widening trade imbalance - a factor that could impact EUR/USD dynamics.

With the dovish market sentiment for this week’s Fed meeting priced in, a cut from policymakers will bring little surprise to the market. However, we note that a diverging view from Fed officials on subsequent cuts might add a more hawkish bias, weighing on the pair slightly this week.

USD / JPY

The macroeconomic landscape for USD/JPY is increasingly bearish as markets anticipate diverging monetary policy paths between the Federal Reserve and Bank of Japan.

The BOJ is showing growing hawkish signals ahead of its December 19th meeting, with Governor Ueda's recent comments and rising Japanese Government Bond yields pointing to a likely rate hike. A probability for a BOJ hike next week is highly priced in, boosting the yen’s appeal.

Mounting expectations of Fed rate cuts in 2026, supported by softer US inflation data, are creating conditions for a significant narrowing of the US-Japan interest rate differential. Japanese wage growth trends and services sector inflation remain supportive of BOJ policy normalization, though weak household spending data presents some concern.

Global investors have already positioned for yen strength, with speculators holding net long positions since February, suggesting any immediate rally may be more measured rather than abrupt. The combination of BOJ tightening expectations and a dovish Fed outlook is creating fundamental pressure for yen appreciation, which could prompt the pair to break the 155.00 support level in the near term. A key risk to the bearish USD/JPY outlook would be if markets have overestimated the pace of Fed rate cuts or if Japanese economic data deteriorates significantly.

GBP / USD

The British pound faces significant headwinds against the US dollar as markets await a pivotal Federal Reserve meeting this week. While the Fed is widely expected to cut rates by 25bps, growing internal division among policymakers over inflation concerns could lead to a more hawkish tone than markets anticipate. However, the appointment of Kevin Hassett as the likely successor to Fed Chair Powell in May 2026 adds another layer of uncertainty, as his dovish stance could potentially undermine dollar strength in the medium term.

The recent weakness in the US dollar index, which has slipped to 98.99, reflects market positioning ahead of the upcoming Fed meeting. However, analysts caution that excessive dovish expectations could lead to disappointment if the Fed signals a more measured approach to future cuts. We see a pronounced bias toward further pound weakness in the near term, with resistance at 1.3366 (100 DMA) likely to cap any rallies for now.

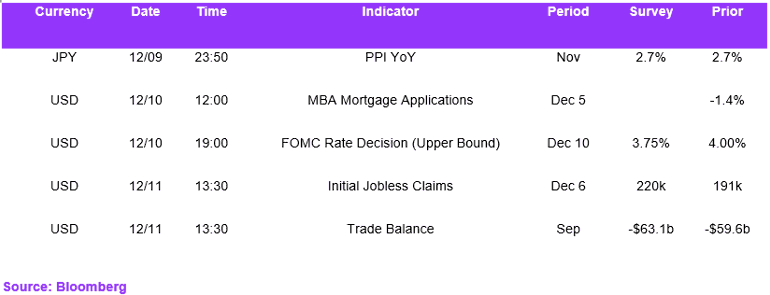

Economic Calendar