EUR / USD

EUR/USD continues to display strong momentum, underpinned by an increasingly clear divergence in monetary policy between the ECB and the Federal Reserve. While the ECB has maintained a steady stance, the Fed is now firmly in an easing cycle. The eurozone’s underlying resilience, reflected in Q3 GDP growth of 0.3% and inflation holding above target at 2.2%, provides a solid fundamental backdrop for euro strength against the dollar.

From a technical perspective, momentum indicators point to stretched conditions, with RSI at 72 signalling an overbought market. Nonetheless, the pair remains comfortably above its key moving averages, suggesting bullish sentiment is still intact in the near term. The recent high at 1.177 marks an important resistance level, with scope for a move towards September’s peak at 1.187 should incoming data continue to favour the euro.

The Fed’s third rate cut, alongside growing internal debate within the FOMC, has effectively capped dollar upside. At the same time, the ECB’s fourth consecutive decision to leave rates unchanged has enhanced the euro’s relative appeal. While capital flows remain supportive, the risk of near-term profit-taking has increased, with initial support seen around 1.169.

USD / JPY

USD/JPY is experiencing elevated volatility as markets position ahead of a potentially significant policy shift from the Bank of Japan, with expectations centred on a rate increase to 0.75% from 0.5% at Friday’s meeting. Recent Japanese data, including firmer business confidence and improved manufacturing indicators, strengthen the case for further policy normalisation.

Technically, the pair has so far held above support at 154.62 while encountering resistance near 155.38, pointing to a consolidation phase ahead of the BOJ decision. A clear break above 155.38 would open the way towards November’s high at 157.73, whereas a move below the 50-day moving average would increase the risk of a pullback towards 153.75.

The yen’s recent appreciation reflects both safe-haven demand and positioning ahead of the BOJ meeting. Market expectations increasingly point to a gradual but sustained tightening cycle, with policy rates potentially reaching 1.0% by mid-2026. Political backing for normalisation, driven by concerns over import-led inflation stemming from prolonged yen weakness, further reinforces the medium-term case for yen strength.

GBP / USD

GBP/USD is approaching a pivotal moment ahead of the Bank of England’s policy decision on Thursday, with markets assigning around a 90% probability to a 25bp rate cut to 3.75%. Recent soft UK data, including weaker-than-expected GDP figures and rising unemployment, have weighed on sterling, although broader dollar weakness following the Fed’s recent dovish shift has provided some offsetting support.

From a technical standpoint, the pair has encountered resistance near 1.34, with RSI at 65 indicating moderately overbought conditions. Price action remains contained between key moving averages, suggesting a period of consolidation as markets await clearer policy signals. Near-term direction is likely to be shaped by forthcoming UK wage and inflation data, which will be critical in shaping the BoE’s guidance.

Looking further ahead, GBP/USD’s broader trajectory will depend on the relative pace of policy easing by the Fed and the BoE into 2026. While markets currently expect at least two further Fed cuts next year, a sustained break above the 200-day moving average at 1.34 would expose 1.343. Conversely, a failure to hold support at 1.329 would raise the risk of a drift back towards the 1.33 area, where the 20- and 50-day moving averages converge.

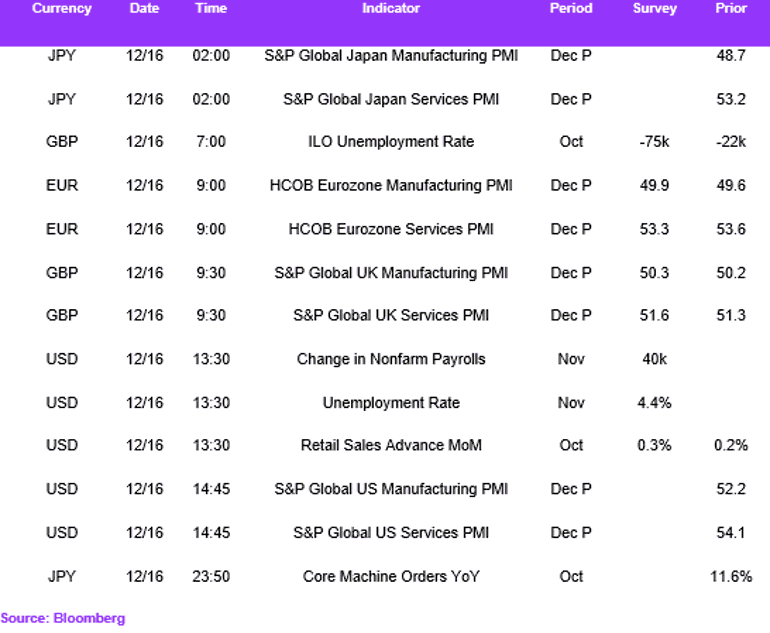

Economic Calendar