EUR / USD

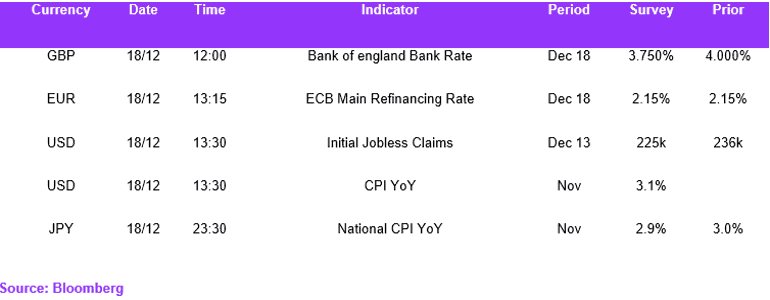

EUR/USD held its nerve at 1.1740, with markets now turning their attention to today’s US CPI print for November, currently forecast at around 3.1% YoY. A reading near this level would reinforce the view that inflation remains way above the Fed’s 2% target despite a cooling labour market. This combination risks creating a problematic start to 2026, where easing employment conditions coexist with inflation that remains elevated, complicating the policy outlook and keeping volatility high across rates and FX markets.

The ECB is expected to leave policy unchanged at its December meeting. While some market participants continue to flag the possibility of renewed tightening later in the cycle, we expect rates to remain on hold through 2026, as policymakers balance the progress of inflation against a still-fragile growth backdrop across the euro area.

With the ECB expected to keep rates on hold and the potential for a more hawkish stance from the US, near-term sentiment could weigh on the pair. However, any shifts in the US CPI are likely to influence only the longer-term monetary policy outlook. Given the recent muted response of FX markets to policy divergence, downside risks for the pair may remain limited.

USD / JPY

The USD/JPY bounced back above the 155.00 mark as the pair faces significant headwinds, with the Bank of Japan preparing for a historic interest rate hike to 0.75% in December, marking a decisive shift from its longstanding ultra-loose monetary policy. Strong Japanese economic indicators, including 6.1% export growth and improving wage dynamics, provide a solid foundation for this monetary tightening cycle.

The anticipated policy divergence between the BOJ and the Federal Reserve, with the latter expected to begin rate cuts in mid-2026, creates a structural environment that could support yen strength.

The contrast between rising US unemployment at 4.6% and Japan's improving economic indicators suggests a possible narrowing of the interest rate differential, which could accelerate yen appreciation. However, market concerns about Japan's fiscal policy and a potential record budget exceeding 120 trillion yen for fiscal 2026 may introduce volatility and limit the currency's upside potential. The 155 mark remains crucial, and only a sustained breach of this level might suggest a potential for the yen’s weakness in the longer term.

GBP / USD

GBP/USD weakened as UK inflation unexpectedly dropped to 3.2% in November, falling below market expectations and confirming the upcoming cut in the Bank of England's monetary policy stance. The deteriorating labour market conditions, marked by rising unemployment and decelerating wage growth, have strengthened the case for monetary easing. Markets are now almost fully priced for the cut outcome today, leaving the BoE’s forward guidance as the key driver for sterling and gilt yields, particularly in terms of how policymakers frame the pace and extent of any further easing.

Technical analysis reveals a complex picture, with the currency pair showing resilience above key moving averages despite recent volatility, as it maintains support above the 20-day moving average at 1.33. The pair's neutral-to-bullish technical outlook, supported by an RSI of 61 and positioning above both the 50-day SMA at 1.3255, suggests potential for upward movement despite fundamental headwinds.

While the immediate resistance level at 1.3390 remains crucial for further upside potential, the combination of softening economic indicators and anticipated monetary policy easing could limit the pair's gains in the medium term.

Economic Calendar