EUR / USD

The ECB’s latest economic updates have left investors cautiously optimistic entering 2026, with robust growth projections driven by higher investment and exports leading to stronger wage growth forecasts. The central bank is now maintaining a moderately hawkish stance with the deposit rate expected to remain at 2.0% throughout 2026, though uncertainty remains high according to ECB President Lagarde.

Meanwhile, the Federal Reserve has already delivered meaningful rate cuts in 2025, with markets now pricing in at least two additional 25-basis-point reductions in 2026, creating a widening interest rate differential that could pressure the dollar. Recent US data confirmed labour market weakness, with job creation slowing, potentially increasing the chances of earlier Fed cuts.

The diverging monetary policy paths between the ECB and Fed, with the ECB holding steady while the Fed moves toward easing, should provide fundamental support for the euro against the dollar in the medium term. However, thin holiday trading conditions could create periods of heightened volatility. The euro's strength may also be tempered by ongoing geopolitical uncertainties and questions about the sustainability of Europe's economic recovery, particularly given its reliance on external demand and exposure to global trade tensions.

USD / JPY

The Bank of Japan's recent rate hike to 0.75%, marking a three-decade high, has triggered significant pressure on the Japanese yen, with the currency continuing to weaken against major peers despite the monetary tightening. The cautious rhetoric from BOJ Governor Ueda and the lack of clear guidance on future rate hikes have failed to support the currency, leading to the yen trading near record lows against the euro and testing critical levels against the US dollar.

Japanese authorities have expressed concern about "one-sided and sharp" currency moves, with top currency diplomat Atsushi Mimura warning of possible intervention if excessive depreciation continues. The persistent yen weakness persists despite Japan's shift away from ultra-loose monetary policy, suggesting that markets remain unconvinced about the pace of future tightening amid significant interest rate differentials with other major economies.

Global carry trades estimated at up to $4 trillion, which were fuelled by years of ultra-low Japanese rates, now face potential disruption as yields rise, creating risks of abrupt capital reversals. The structural challenges facing the yen include Japan's massive public debt burden and significantly low real yields compared to peers, indicating that modest rate hikes alone may not be sufficient to stabilise the currency. The BOJ's careful balancing act between normalising policy and avoiding market disruption continues to weigh on the yen's trajectory, with markets closely monitoring both verbal and actual intervention from Japanese authorities.

GBP / USD

The Bank of England's December rate cut to 3.75% has established a clear easing cycle, with most analysts expecting further cuts in 2026 as the UK economy shows signs of weakness while inflation continues falling toward the 2.0% target. The UK labour market has deteriorated notably, with job vacancies dropping sharply in November and unemployment rising to 5.1%, the highest since 2021, suggesting growing economic headwinds.

Meanwhile, the Federal Reserve has also cut rates but now appears more cautious about the pace of easing, with some officials like Cleveland Fed President Beth Hammack signalling rates could stay steady for months amid sticky inflation concerns.

This policy divergence between a more dovish BOE and relatively hawkish Fed is likely to pressure sterling in the coming months. Market expectations are coalescing around at least two more BOE rate cuts in 2026, likely coming before the Fed moves again. The combination of UK economic fragility, earlier BOE easing, and a cautious Fed stance points to downside risks for GBP/USD in the first half of 2026.

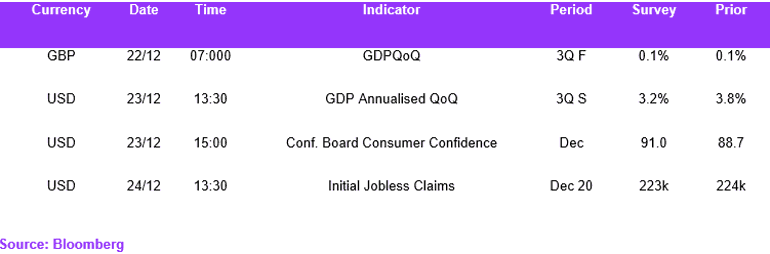

Economic Calendar