EUR / USD

EUR/USD remains under pressure as softer German inflation, with December CPI falling to 1.8%, reinforces expectations that euro area price pressures are easing more quickly than previously anticipated. Technically, the pair is struggling to regain traction, with the 20-day and 50-day SMAs converging near 1.17 and the 200-day SMA providing broader support at 1.16. The RSI at 44 highlights fading momentum and leaves the pair vulnerable to further downside.

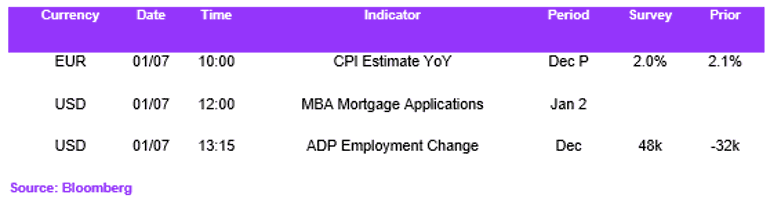

Attention now turns to US labour data, with today’s ADP Employment report likely to be a key near-term driver for the dollar. While consensus looks for a return to modest private-sector job growth, markets appear asymmetrically positioned. With only one 25bp Federal Reserve cut priced for H1 2026, EUR/USD is likely to be more sensitive to a downside surprise than to a positive print. Even a mildly weaker ADP reading could trigger renewed dollar selling and allow the pair to stabilise above 1.165, while a firmer outcome would likely offer only limited USD upside. A break below the 200-day SMA would expose the 1.150 area.

USD / JPY

USD/JPY continues to trade with a firm bias, supported by a still-wide yield differential despite Japanese 10-year yields rising to 2.12%. The pair remains above key moving averages, with resistance at 157.75 and scope for a retest of the July 2024 highs near 162.00 should US yields remain supported.

However, US labour data poses a growing risk to the upside. With positioning increasingly stretched and Fed easing expectations only lightly priced, USD/JPY appears vulnerable to any signal from ADP that US labour market momentum is deteriorating. A softer print would likely weigh disproportionately on US yields, encouraging profit-taking in long USD/JPY positions and increasing the risk of a move back towards support at 155.43. Conversely, a stronger ADP outcome may struggle to generate sustained follow-through, particularly given ongoing intervention sensitivity and rising Japanese yields. The 200-day SMA at 149.76 remains a key longer-term anchor.

GBP / USD

GBP/USD retains a broadly constructive structure, trading above its major moving averages, though recent gains appear driven more by dollar weakness than by a marked improvement in UK fundamentals. Support is centred around the 1.33 area, with resistance near the recent high at 1.36.

Today’s ADP Employment release is likely to be pivotal for near-term direction. With markets primed to react more forcefully to negative labour surprises, a softer-than-expected ADP print could reinforce expectations of earlier or deeper Fed easing, supporting a renewed push higher in GBP/USD. In contrast, a stronger print would likely have a muted impact, given that much of the labour market resilience narrative is already priced. A break below the 30-day VWAP at 1.34 would shift focus back towards 1.30, while a benign or weak ADP outcome could keep the pair supported above 1.33.

Economic Calendar