EUR / USD

EUR/USD is exhibiting short-term technical weakness against a backdrop of medium-term fundamental dynamics that we see as more supportive for the single currency. The pair has slipped around 0.3% towards 1.165, trading below key moving averages at 1.17 and holding support at the 200-day SMA near 1.16, while an RSI reading of 37.8 signals oversold conditions that could precede a mean-reversion rebound.

We see narrowing yield differentials emerging as a potential medium-term tailwind for euro valuations, with eurozone inflation moderating to the ECB’s 2.0% target and expectations for Fed easing building beyond mid-year. Several forecasters now expect appreciation towards the 1.20–1.25 area by year-end, contingent on continued disinflation and relative growth stability.

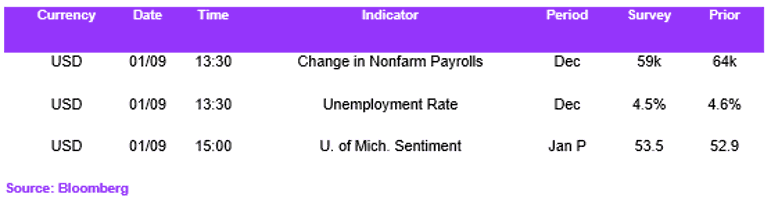

The key near-term catalyst is today’s Change in Nonfarm Payrolls release. Consensus expects an improvement from November with positive job creation after a run of softer labour indicators. With markets pricing only one 25bp Fed cut in H1 2026, we see NFP risks skewed asymmetrically. Softer data would likely prompt a repricing in rates and FX, supporting EUR/USD via weaker yields and reduced US exceptionalism. Technically, we would monitor 1.164 as critical support; a defence of this level alongside oversold conditions could facilitate recovery towards 1.17, while a break below risks accelerating losses towards 1.160.

USD / JPY

USD/JPY continues to reflect substantial monetary policy divergence, with restrictive Fed policy still providing a yield advantage despite gradual BoJ normalisation. We expect the US-Japan rate differential to remain a dominant driver in the near term, though rising Japanese yields and prospective intervention risk temper the bullish USD/JPY narrative.

Technically, the pair remains supported above primary moving averages, including the 200-day SMA near 150, the 50-day at 156, and the 20-day near 156.50, signalling sustained upward momentum. The daily RSI at 56 suggests room for further upside without immediate overbought constraints. We see resistance at 158, with potential extension towards the December highs should US yields remain firm. On the downside, a failure to sustain gains above 157 could bring the 50-day SMA back into focus.

Looking forward, we expect NFP to be pivotal. Consensus anticipates a rebound in job creation, though we think FX reaction remains asymmetric. Labour weakness would strengthen expectations for earlier Fed cuts and weigh on USD/JPY, while a stronger print may deliver only modest upside given already-priced resilience and BoJ normalisation. We see downside risks as more event-sensitive into NFP.

GBP / USD

Sterling has softened against the dollar, declining around 0.75% across three sessions as investors adopt a defensive stance ahead of US labour data. Dollar strength has broadened, with the DXY approaching one-month highs, while UK domestic softness, including a 0.6% monthly fall in Halifax house prices, has highlighted structural vulnerabilities and weighed on sentiment. Rate differentials continue to favour the dollar, as markets anticipate the BoE is closer to easing while the Fed remains cautious.

Technically, GBP/USD is trading near 1.3427, just below the 20-day SMA at 1.35, with RSI moderating to ~51 after failing to sustain momentum above 1.3550. We view the 200-day SMA at 1.34 as an important inflection level. A decisive break could accelerate selling towards 1.3297, while stabilisation above 1.34 would keep the medium-term range intact.

For GBP/USD, we expect NFP to be the principal directional driver today. Consensus looks for a rebound in job creation, but with only one 25bp cut priced for H1 2026, labour data remain asymmetric for market reaction. A weaker-than-expected NFP print risks repricing Fed expectations and supporting GBP/USD, while a stronger release may struggle to extend dollar gains beyond current levels. We expect volatility into and through the release window.

Economic Calendar