EUR / USD

EUR/USD is currently trading at 1.1645 following a modest 0.2% decline over the past 24 hours, positioning the pair just below a significant cluster of resistance at the 50-day, 20-day moving averages at 1.1660. The daily RSI reading near 40 indicates subdued momentum, while the 200-day moving average at 1.1585 provides critical near-term support that buyers must defend to prevent accelerated selling toward the 1.1503 support zone.

The macroeconomic backdrop reveals divergent central bank trajectories, with December's U.S. CPI confirming 2.7% YoY inflation and supporting expectations for Fed rate cuts beginning in June, while the ECB maintains a prolonged pause stance as eurozone inflation moves closer to target levels. Political uncertainty surrounding Fed Chair Powell's position and concerns about central bank independence have created safe-haven demand pressures that are cross-currenting with technical deterioration in the euro. Currency flows indicate investors are repositioning away from traditional dollar dominance toward European and Asian assets, even as solid December employment data reinforced expectations that the Fed will hold rates through January.

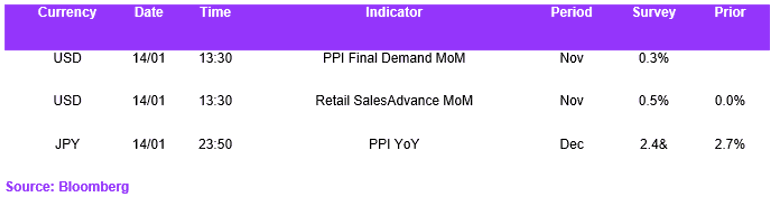

Today brings PPI and November retail sales, neither of which we expect to shift the macro narrative. Instead, geopolitics remains the dominant driver of near-term market tone, but its impact is being felt less by the dollar, and in turn, the euro. We expect the pair to remain capped by the shorter-term moving average resistance levels.

USD / JPY

USD/JPY continues to demonstrate strong bullish momentum, climbing to approximately 159.13 and approaching levels not seen since mid-2024, driven primarily by the fundamental divergence in monetary policy between the Federal Reserve and the Bank of Japan. The substantial yield advantage for dollar-denominated assets continues to fuel persistent carry trade demand, while recent speculation regarding a snap election in Japan has amplified yen weakness through anticipated fiscal stimulus measures. Capital outflows from Japanese investors seeking higher-yielding alternatives provide additional structural support for dollar appreciation.

From a technical perspective, the daily RSI has surged to 72.42, indicating overbought conditions; however, price action remains well-supported above the 20-day SMA at 157 and the 50-day SMA at 156.93. Currency intervention risk has emerged as a key constraining factor, with Japanese authorities signalling escalating concern near the psychologically significant 160 level based on historical intervention precedents. The convergence of favourable carry dynamics against official intervention thresholds creates an asymmetric risk profile that balances fundamental support for higher levels against potential policy-driven constraints on further yen depreciation. As a result, we expect the upside to continue but to moderate as the pair approaches the key 160 threshold.

GBP / USD

GBP/USD declined approximately 0.4% to close near 1.342, with the RSI retreating to neutral levels around 50 and price now sitting below the 20-day moving average at 1.3464 but maintaining support above the 50-day SMA at 1.33 and 30-day VWAP at 1.3326. The convergence of weakening UK domestic demand, divergent monetary policy expectations, and technical positioning below near-term resistance establishes a moderately bearish medium-term bias for the pair.

Domestically, UK economic conditions present a sobering backdrop, with consumer spending contracting significantly and retail sales growth decelerating for the fourth consecutive month amid intensifying household caution over tax burdens and labour market softness. Inflation dynamics remain mixed, though persistent rental inflation constrains Bank of England policy flexibility. Market pricing of two US rate cuts against single-cut BoE guidance amplifies interest rate differentials that typically pressure lower-yielding currencies.

Economic Calendar