EUR / USD

The EUR/USD pair saw moderate upward pressure during the day, as it rejected prices below the critical 1.1500 mark. Markets continued to price in dovish Fed comments, with market expectations for a December rate cut surging to 75-80% following recent comments from key Fed officials. The European Central Bank's contrasting "higher for longer but no further hikes" position is creating a monetary policy divergence that fundamentally supports the euro against the dollar.

Despite weaker German data, the pair’s trajectory appears more driven by the dollar and, in turn, the Fed moves. Moreover, potential developments in Ukraine peace negotiations are providing additional, albeit marginal support for the euro by reducing geopolitical risk premiums and easing energy market pressures.

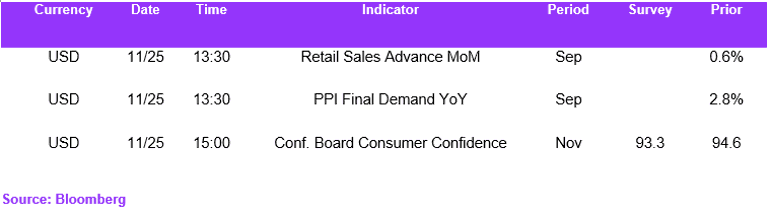

Technical analysis suggests that the support at 1,1500 appears solid, and this could trigger a modest uptick in the near term. We expect US retail sales growth to slow, with a projected monthly increase of approximately 0.2% MoM, reflecting softer discretionary spending and higher price pressures. This should give the EUR/USD an additional boost.

USD / JPY

USD/JPY continues to demonstrate significant upward momentum, trading well above key technical indicators, reflecting persistent bullish sentiment in the market. The Bank of Japan's accommodative monetary stance, combined with Japan's expansionary fiscal policies, has been a primary driver of yen weakness against the dollar.

Japanese officials, including Finance Minister Satsuki Katayama, have expressed mounting concerns about the currency's depreciation, with authorities signalling readiness to intervene in markets if necessary, particularly as the pair approaches the psychologically significant 160 level. Despite the Federal Reserve's evolving position, particularly the recent dovish sentiment, the individual dollar's impact seems minimal, with markets being guided by wide yield differentials, which boost the pair.

Market participants are particularly attentive during periods of reduced liquidity, such as the US Thanksgiving holiday and a shorter trading week in Japan, which could present an opportunity for Japanese intervention.

While trend support at 156.00 appears robust in the near term, we anticipate that bearish pressures will intensify toward year-end. Japanese policymakers have signalled growing discomfort with the yen's weakness and are prepared to intervene if necessary. As a result, downward momentum could drive USD/JPY toward 151.00 by year-end.

GBP / USD

Read our comprehensive outlook for the upcoming UK Budget to see detailed analysis on fiscal policy changes, and the potential impact on Gilts and sterling.

GBP/USD held its ground above 1.3100 as market focus shifted to the UK Budget on Wednesday, with market participants awaiting clear announcements from Chancellor Reeves. The key market risk is any deviation from strict fiscal discipline: if Reeves announces measures perceived as unfunded or inconsistent with her fiscal rules, gilt markets could react sharply, echoing sensitivities still lingering after the Truss episode.

A surprise increase in long-dated issuance or weaker-than-expected consolidation plans would lift yields and widen the risk premium. Sterling would likely come under further pressure in such a scenario. That said, a shock on the scale of the Truss episode is unlikely, so overall market risk remains muted.

Moreover, with growing dovishness from the BOE, with markets now anticipating 50bps worth of cuts until May 2026, the structural risks for GBP/USD are tilted to the downside.

Economic Calendar